4 Ways to Lower Credit Card Processing Fees for Your Business

Fees matter. In the earliest days of your business, when sales volume was low and your priority was simply reaching customers, transaction costs may not have seemed like a big concern. After all, what difference does a small percentage or a few cents per transaction really make? But as your company grows, those costs add up quickly. Even a small difference in rates can mean thousands of dollars lost each year. That is why many growing businesses look for ways to lower credit card processing fees and keep more revenue from every sale.

However, as sales increase, those small fees can add up quickly. Even a fraction of a percent in extra fees can cost a business thousands of dollars each year. According to the Merchant Payments Coalition, merchants in the United States paid more than $170 billion in card processing fees in recent years, highlighting how significant these costs can become at scale.

For growing businesses, it is critical to regularly review payment processing costs and work with a merchant services provider that can help reduce unnecessary expenses.

Below are four practical ways businesses can lower credit card processing fees and keep more revenue.

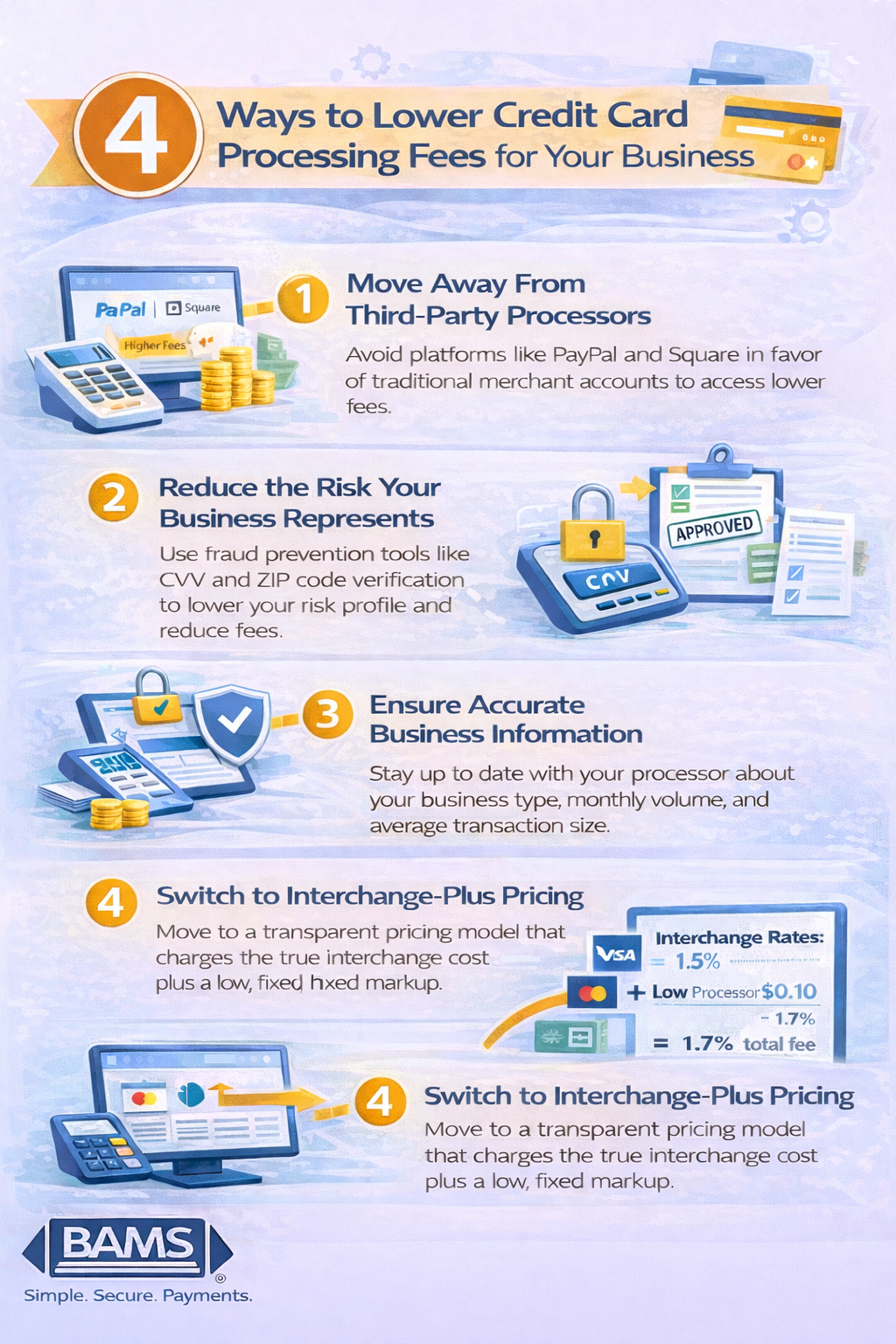

Four practical strategies businesses can use to lower credit card processing fees and keep more revenue from every transaction.

1. Move Away From Third Party Processors

Third party payment processors such as PayPal and Square are popular because they are easy to set up. Businesses can often begin accepting payments within minutes.

However, this convenience usually comes with higher transaction fees.

Because third party platforms allow merchants to sign up quickly with minimal underwriting, they assume greater financial risk. To offset this risk, these providers typically charge higher flat rate fees for every transaction.

Businesses that switch to a traditional merchant account often gain access to lower rates. While the onboarding process may take more time and require additional documentation, the long term savings can be substantial.

Merchant accounts also provide greater flexibility and customization for businesses that process higher volumes of transactions.

2. Reduce the Risk Your Business Represents

Payment processors determine fees based partly on the risk level of each merchant. Businesses that are considered higher risk often face higher transaction costs.

Reducing fraud risk can help lower these fees.

In physical retail environments, businesses should ensure their payment hardware supports modern security standards such as EMV chip cards.

For online transactions, several simple practices can improve security and reduce fraud risk.

Examples include:

Require CVV security codes for every card transaction

Require billing ZIP code verification

Enable additional authentication tools such as Verified by Visa or Mastercard SecureCode

Implementing stronger fraud protection measures not only improves security but can also help businesses qualify for lower interchange categories.

Research from the Federal Reserve indicates that card not present transactions carry significantly higher fraud risk than in store purchases, making security measures especially important for online merchants.

3. Ensure Your Processor Has Accurate Business Information

When applying for a merchant account, businesses must complete a detailed application process. This information is used by processors during underwriting to evaluate the risk profile of the merchant.

If incorrect or outdated information is provided, it can result in higher fees.

Businesses should review the following details to ensure accuracy:

Business model and industry category

Estimated monthly processing volume

Average transaction size

Website or storefront details

If your business has grown or changed since the original application, updating this information with your merchant services provider may unlock better pricing.

Small corrections in underwriting data can sometimes lead to lower risk classification and reduced processing costs.

4. Switch to Interchange Plus Pricing

Not all payment processors use the same pricing models.

There are three common pricing structures used in the payment processing industry.

Flat rate pricing

Tiered pricing

Interchange plus pricing

Flat rate pricing charges the same fee regardless of the transaction type. While simple, it often results in merchants paying higher fees overall.

Tiered pricing groups transactions into different pricing categories. However, these tiers can still obscure the true cost of each payment.

Interchange plus pricing offers the most transparency. With this model, merchants pay the exact interchange rate set by card networks plus a clearly defined processor markup.

Even small reductions in payment processing fees can create major annual savings as transaction volume grows.

Since interchange rates are published publicly, businesses can clearly see how their processing costs are structured.

For many merchants, switching to interchange plus pricing can significantly reduce transaction fees while improving pricing transparency.

To learn more about how payment structures impact your business costs, you can explore our guide on key factors impacting eCommerce payment processing costs.

Businesses interested in improving their payment strategy can also review our article on cutting payment processing fees and improving margins.

Why Reducing Payment Processing Fees Matters

Payment processing costs are often one of the largest hidden expenses for growing businesses. As transaction volume increases, small fee differences can significantly impact profitability.

The Nilson Report estimates that global card transaction fees continue to rise each year as digital payments expand worldwide.

Businesses that regularly review their processing setup and work with transparent providers can reduce unnecessary costs while maintaining secure and reliable payment infrastructure.

To find out more about how the BAMS interchange-plus pricing model can slash your merchant fees to industry lows – guaranteed – get started with your free comprehensive five-point price comparison today.

Frequently Asked Questions

What are credit card processing fees

Credit card processing fees are charges merchants pay whenever a customer uses a debit or credit card. These fees typically include interchange fees paid to the issuing bank, assessment fees paid to card networks, and processor markup.

Why do some payment processors charge higher fees

Processors that allow fast onboarding or assume higher fraud risk often charge higher fees to compensate for that risk.

What is interchange plus pricing

Interchange plus pricing is a payment processing model where merchants pay the exact interchange rate set by card networks plus a transparent processor markup.

Can businesses negotiate payment processing fees

Yes. Businesses with higher transaction volumes can often negotiate better rates with their payment processor.

What is the best way to reduce payment processing costs

Businesses can reduce fees by using a traditional merchant account, improving transaction security, ensuring accurate underwriting information, and choosing transparent pricing models such as interchange plus.