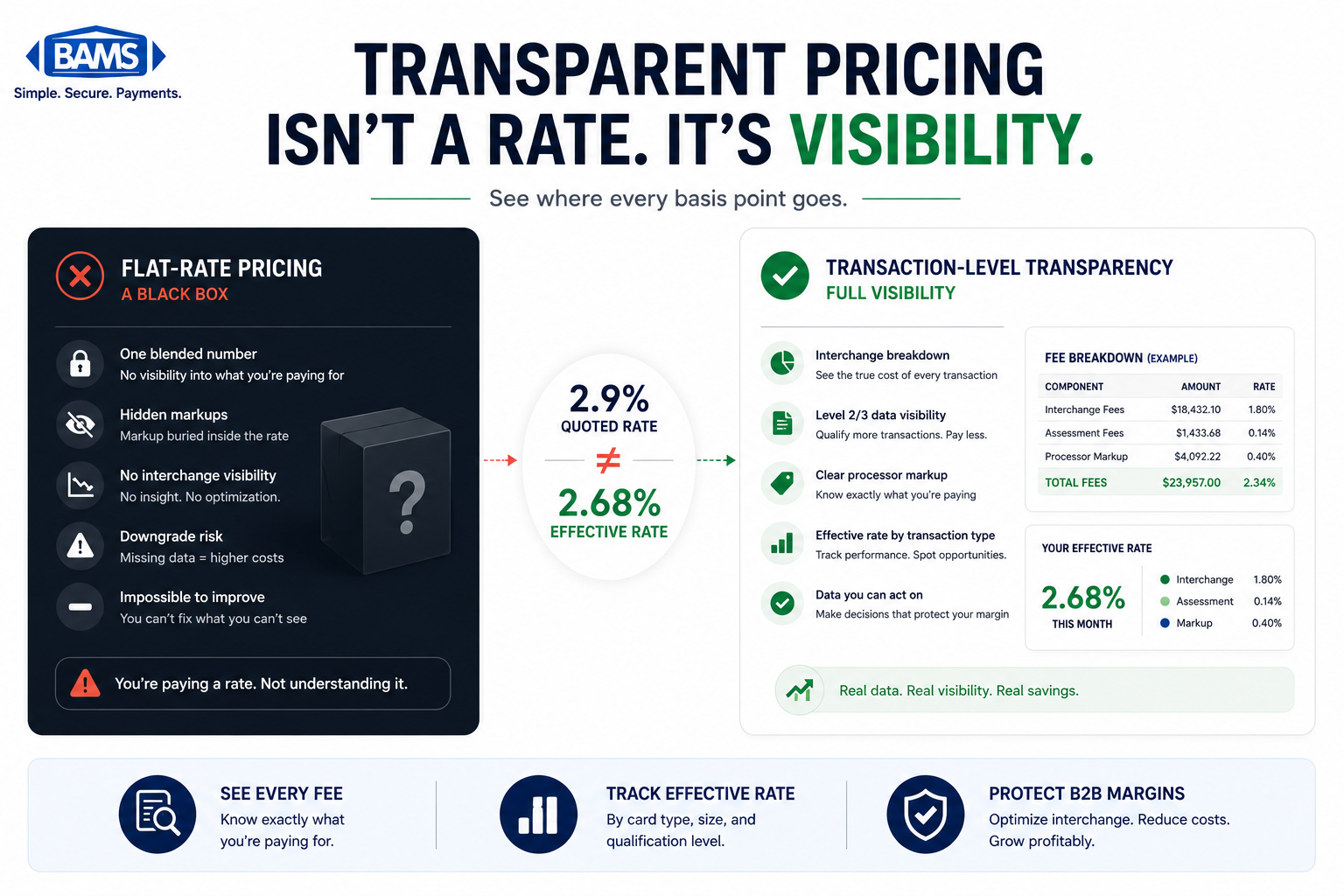

Why a single quoted rate tells you nothing about where your processing margin actually goes Learn why flat-rate pricing marketed as transparent actually obscures your true costs. Discover how to evaluate merchant service charges at the transaction level and what mid-market eCommerce businesses should demand from a processor. TL;DR Flat-rate pricing isn’t transparent – It […]

BAMS Blog

Featured Article

Transparent Pricing Model: What It Actually Means

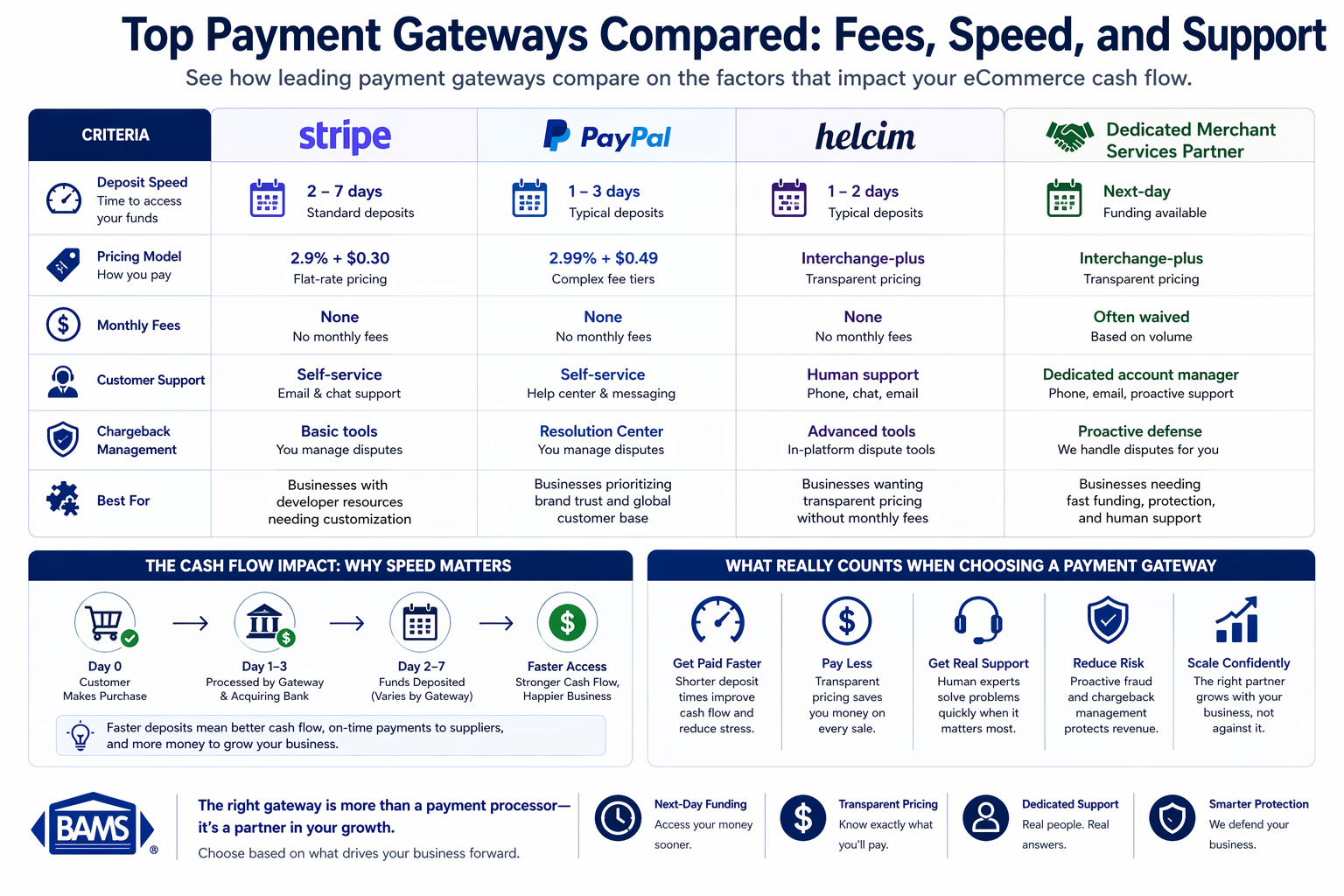

How deposit timing, pricing transparency, and real human support affect your eCommerce cash flow Compare top payment gateways on what actually matters: how fast you get paid, what you really pay in fees, and whether support answers when problems hit. Find the right fit for your 10-50 employee eCommerce operation. TL;DR Deposit speed varies dramatically […]

How settlement mechanics, cut-off times, and bank relationships create hidden delays — and how to fix them Learn why your weekend eCommerce revenue doesn’t hit your bank account until midweek. This guide breaks down the settlement pipeline, identifies where delays occur, and shows you how to audit and optimize your setup for faster funding. TL;DR […]

Calculate your real B2B processing cost in under an hour using only your existing statements Learn to audit your merchant statements line by line, calculate your true effective processing rate, and identify every buried markup inflating your B2B costs. No new software or contracts required — just your last three statements and 60 minutes. TL;DR […]

How default settings at signup quietly drain your margins—and the configuration choices that stop it Learn which processor setup defaults silently inflate your merchant processing fees every month. This guide covers pricing models, batch timing, and PCI fee structures so you can audit your configuration for maximum cost control. TL;DR Setup is the highest-leverage moment […]

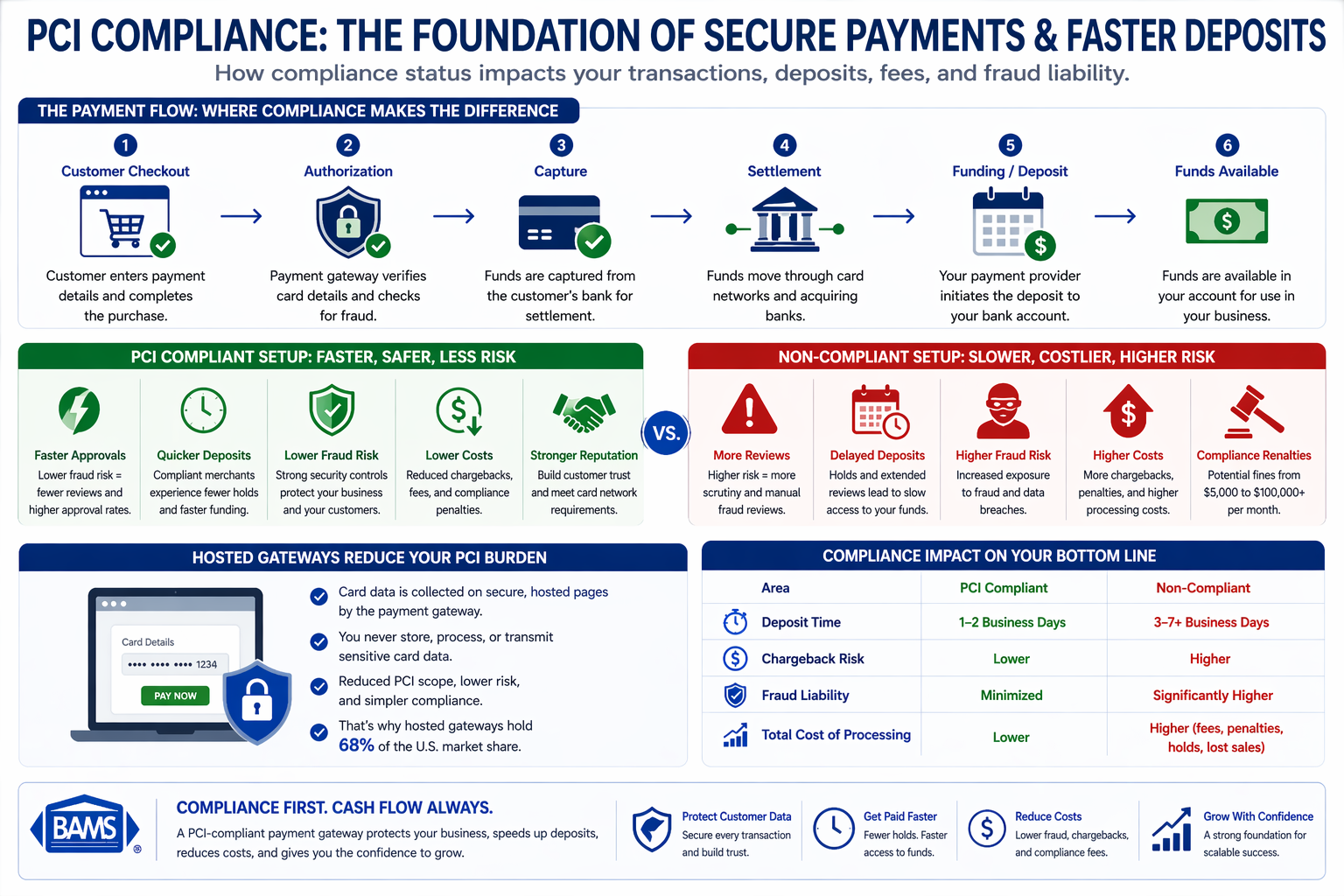

How compliance status affects your deposits, fees, and fraud liability—and what to look for Learn why PCI compliance should be your primary filter when comparing payment gateways. This guide shows how compliance impacts deposit timing, fee structures, and fraud exposure for eCommerce businesses. TL;DR PCI compliance determines deposit speed – Non-compliant setups trigger more fraud […]

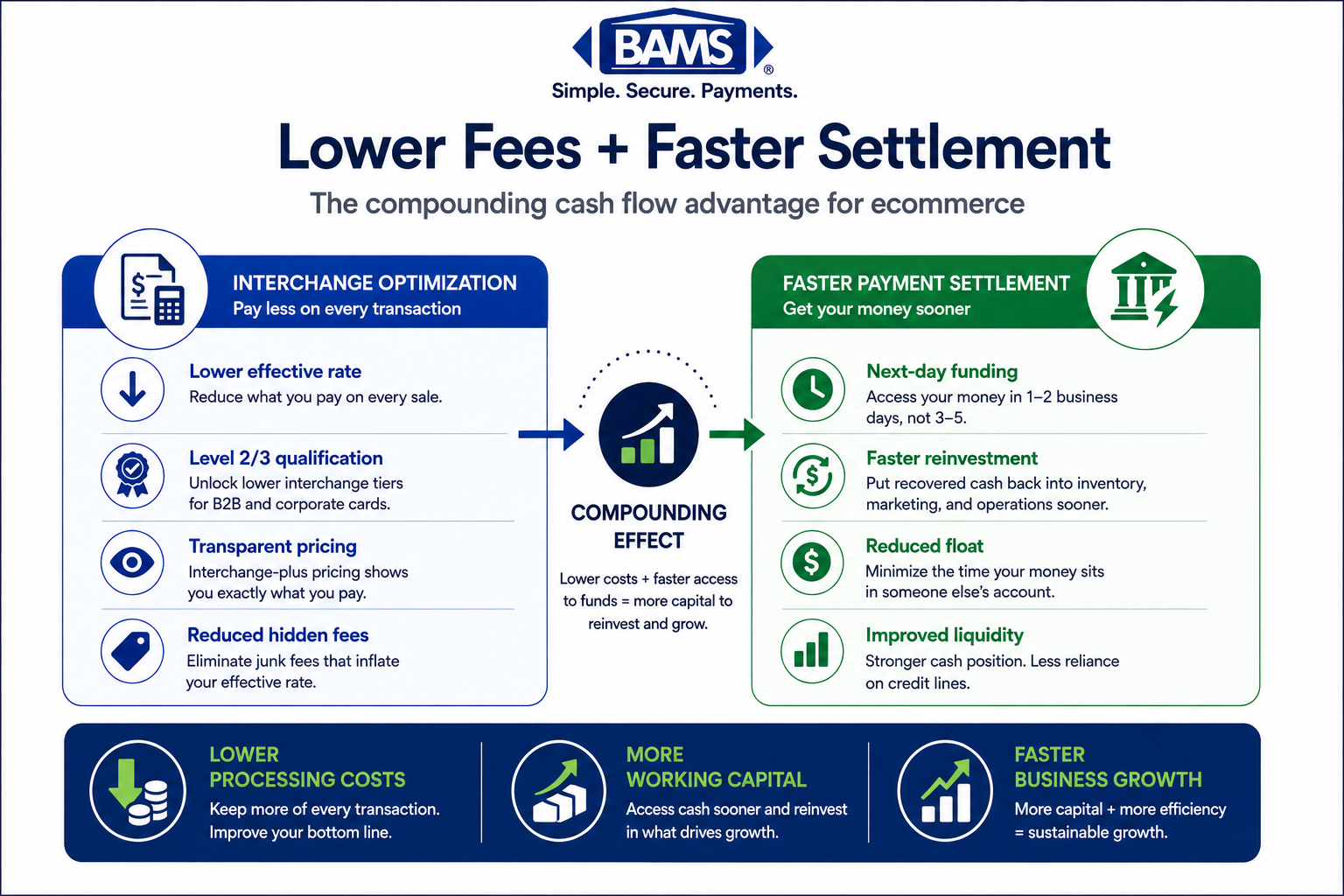

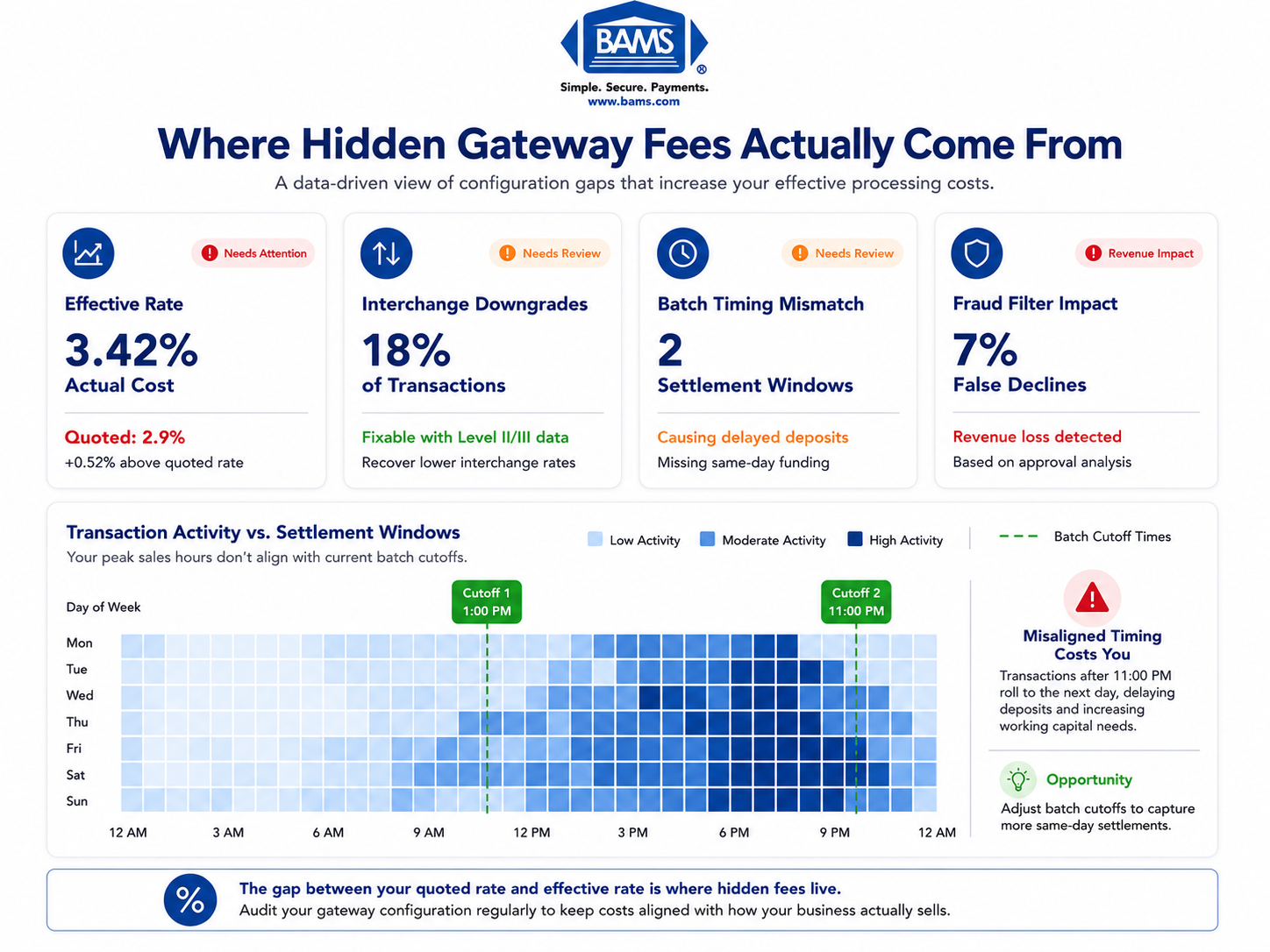

How connecting interchange optimization with settlement speed creates a compounding cash flow advantage for eCommerce Learn how to audit your processing setup, qualify for lower interchange tiers, and link those transaction cost savings to faster payment settlement. This guide shows mid-market eCommerce operators how the combined effect drives reinvestable cash flow. TL;DR Your effective processing […]

Eliminate hidden merchant processing fees by matching your gateway configuration to your actual transaction patterns Learn how to audit your payment gateway defaults, spot mismatches between your configuration and real transaction patterns, and reconfigure the settings silently inflating every batch. Built for eCommerce managers at established stores who know fees are too high but can’t […]

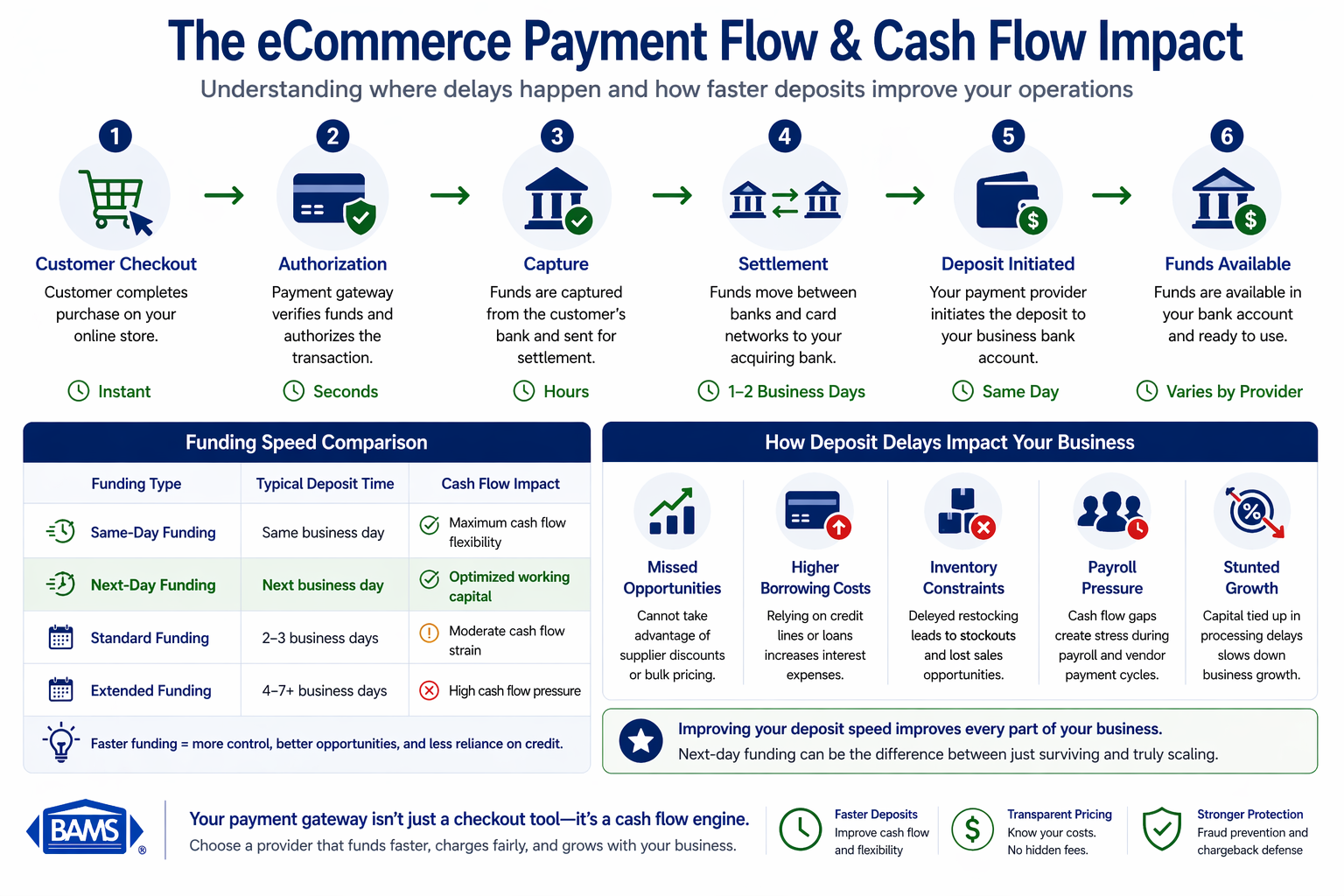

A practical guide to evaluating payment processors for faster deposits and healthier operations Learn how deposit timing from your payment gateway creates cash flow strain and what features to prioritize when switching. This guide covers practical selection criteria for eCommerce managers ready to optimize their payment stack. TL;DR Deposit timing directly impacts operations – The […]

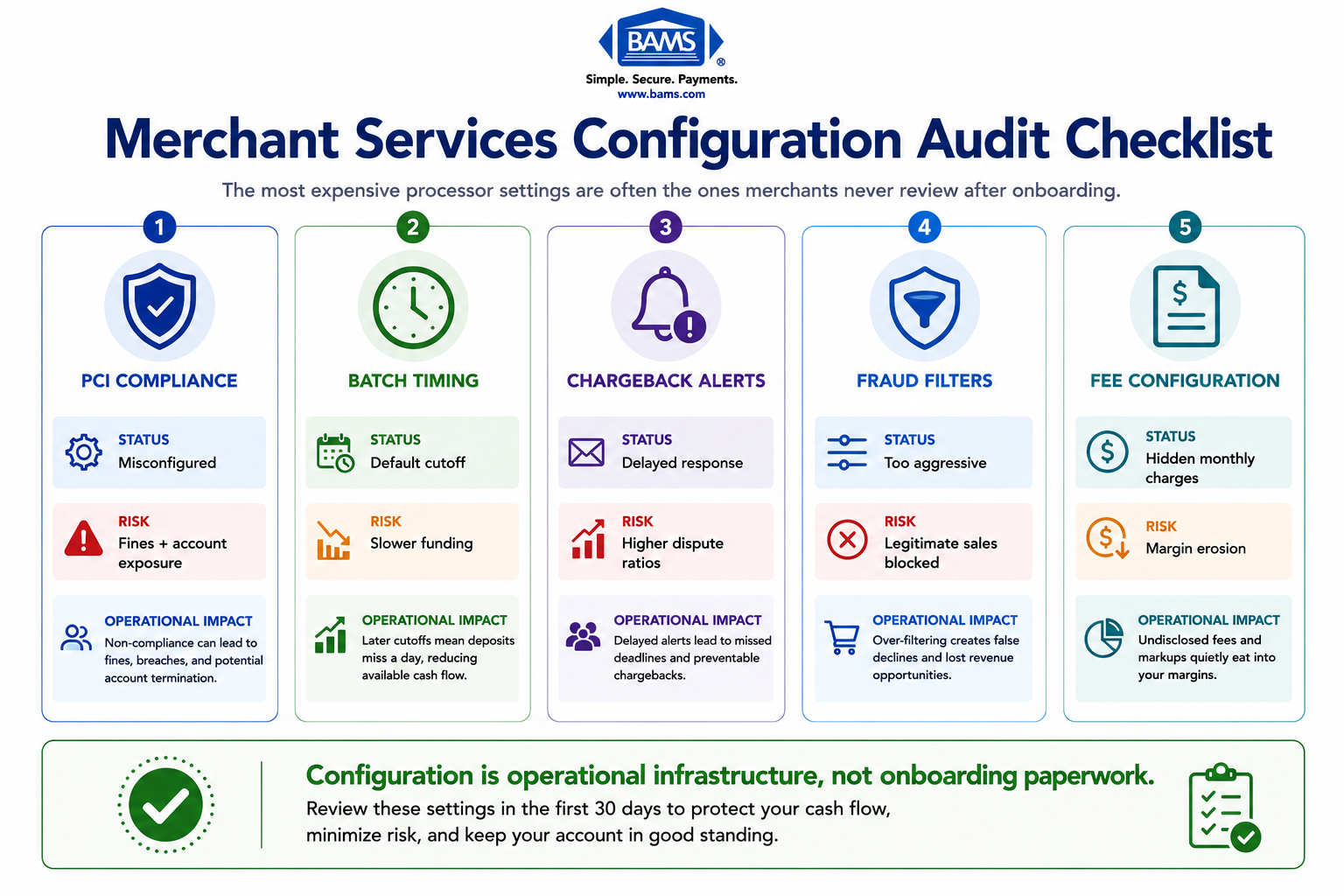

Why the compliance configurations you skipped during onboarding are freezing funds and creating holds weeks after launch Learn why default processor settings for PCI compliance, batch timing, and chargeback thresholds create real cash flow risk. This piece examines the downstream consequences of treating compliance setup as a checkbox during onboarding. TL;DR Default processor settings protect […]

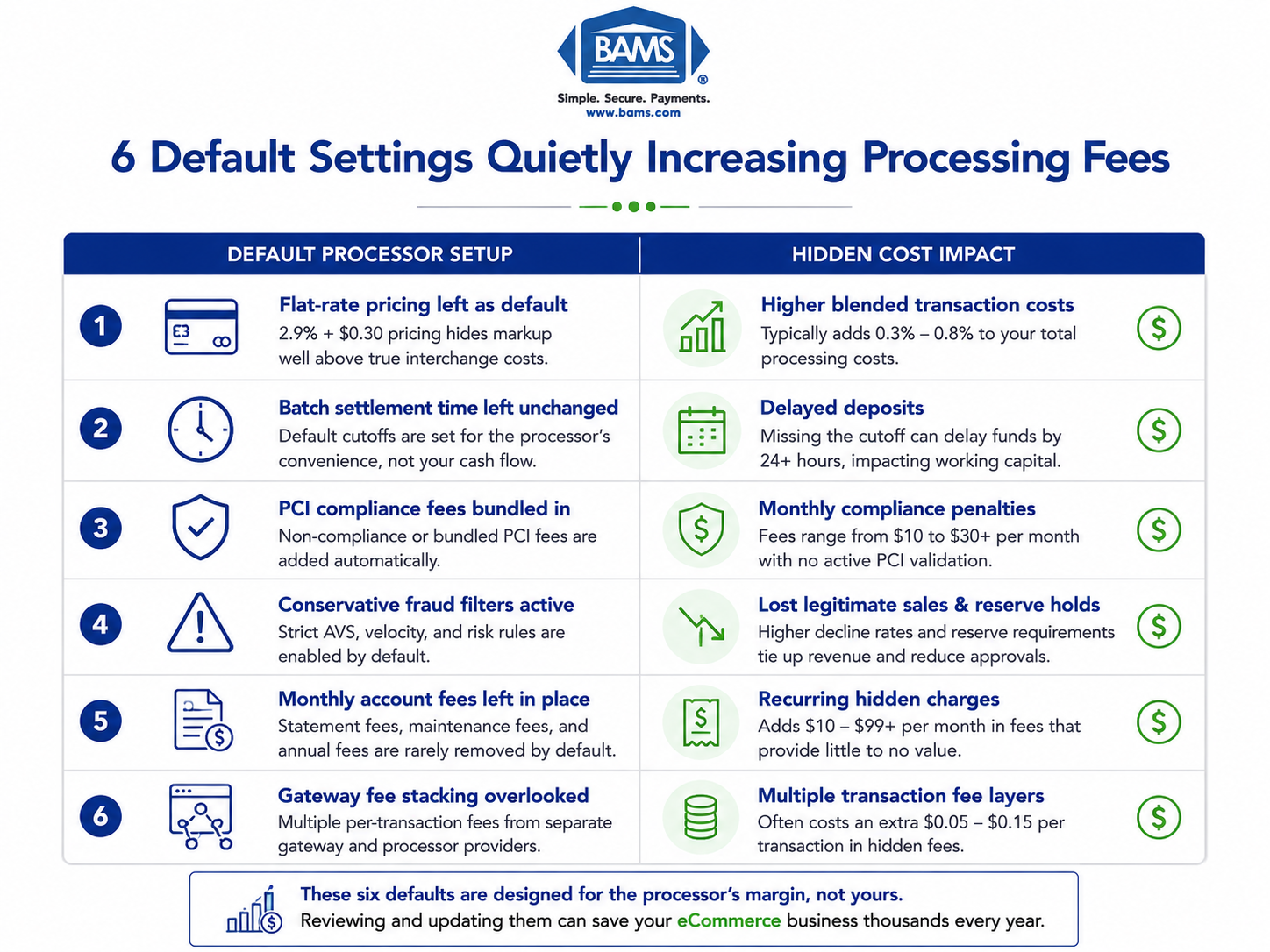

The onboarding configurations your processor set for their margin — and the exact cost each one adds to your statement Learn which six default merchant account settings silently inflate your processing costs and the specific dollar signals each leaves on your monthly statement. Built for eCommerce teams ready to audit configurations they accepted without a […]

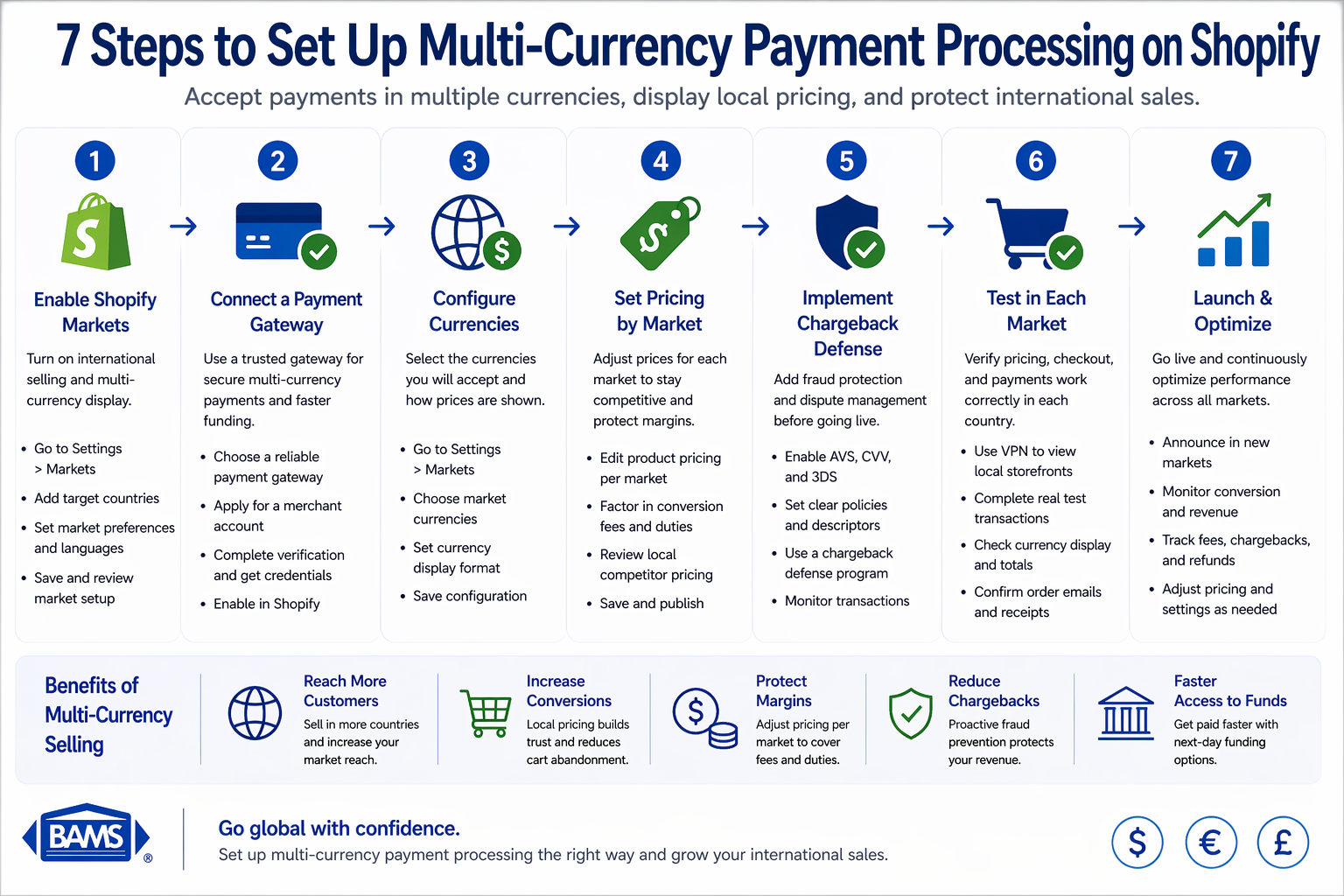

Configure local pricing, connect a secure payment gateway, and protect cross-border sales with chargeback defense Learn to accept payments in multiple currencies on your Shopify store. This tutorial covers currency settings, payment gateway setup, and chargeback protection for international sales. TL;DR Enable Shopify Markets first – This unlocks multi-currency display and international selling features that […]

Fast deposits, predictable fees, and built-in support for digital wallets and recurring billing Discover which payment gateways actually speed up fund access for growing eCommerce businesses. We compare features that matter: deposit timing, fee transparency, and modern payment support. TL;DR Funding speed matters as much as fees – Standard 3-5 day deposit windows lock up […]

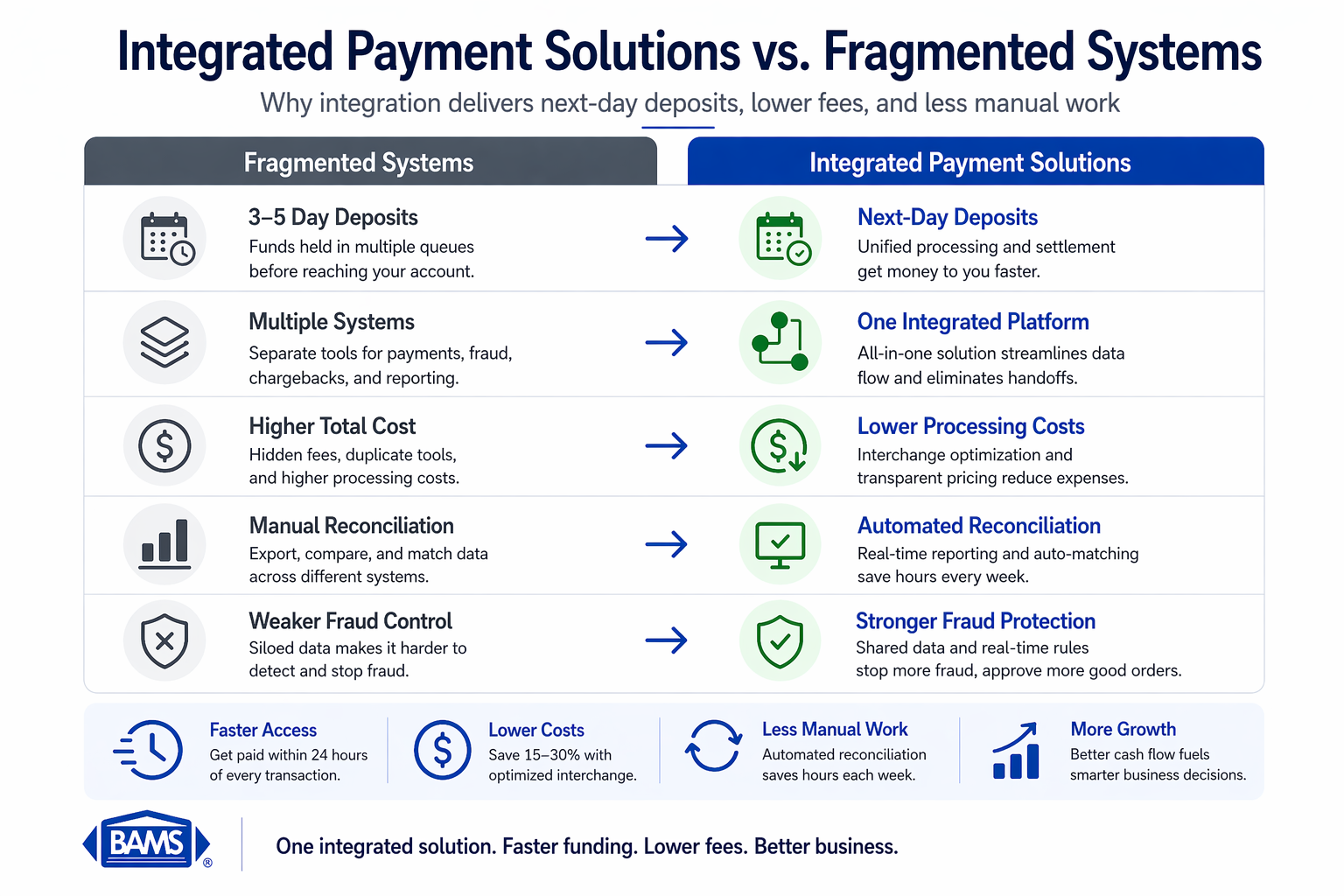

Step-by-step setup for faster funding, lower fees, and automated reconciliation in your eCommerce store Learn to configure integrated payment solutions that eliminate 3-5 day deposit delays. This tutorial covers gateway setup, interchange optimization, and automated reconciliation for measurable results in your first week. TL;DR Deposit delays cost you working capital – Switching to integrated payment […]

For business owners scaling specialized service operations, the challenges involve strategic equipment investments, multi-state expansion decisions, and positioning in premium market segments. David Rudisill, President of Pipe Restoration Solutions, a leading CIPP specialist for commercial, complex projects and multi-unit buildings in Florida and California, recently sat down to discuss how specialized contractors build sustainable commercial […]

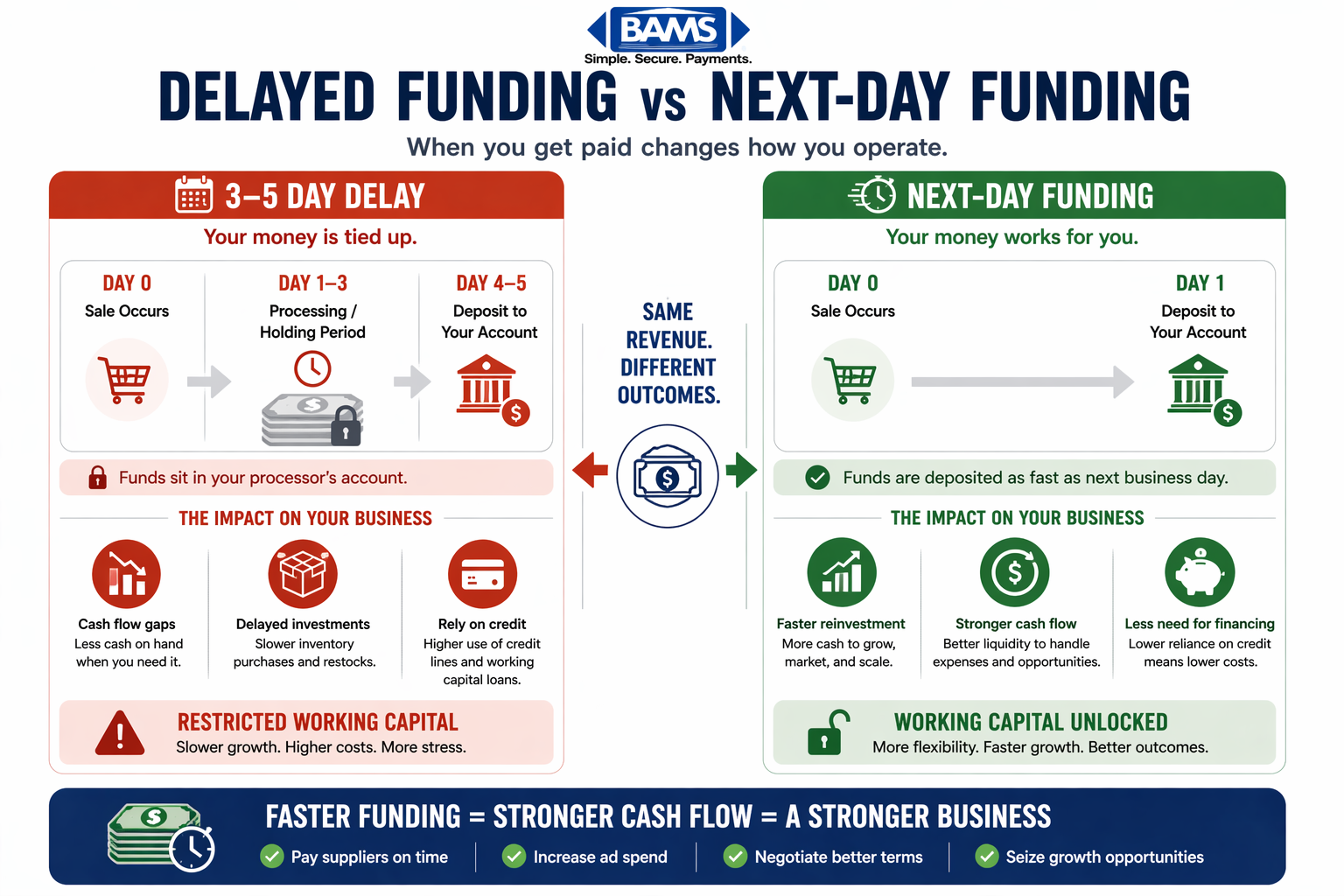

Why your payment gateway’s deposit timing matters more than processing fees for cash flow Learn how 3-5 day payment holds drain your working capital and what to look for in an eCommerce payment gateway that offers next-day funding. Built for established businesses managing real volume. TL;DR Delayed deposits are a growing problem – 58% of […]

How small businesses can reclaim cash flow with secure, faster payment solutions Discover why traditional payment processors hold your revenue hostage and how modern secure payment gateways eliminate costly delays. Learn to evaluate solutions that protect transactions while keeping cash flowing. TL;DR Deposit delays are a choice, not a necessity – Modern payment technology can […]

Expert Interview: Journey Advisory Group Recognized with 5 Stars on Newsweek’s List of America’s Top Financial Advisory Firms Disclosure: Newsweek’s America’s Top Financial Advisory Firms 2026, published in partnership with Plant-A Insights Group, is an annual ranking that evaluated over 16,000 SEC-registered financial advisory firms. To be eligible, firms were required to have more than […]

How modern payment processing combines faster funding with chargeback defense to stop cash flow leaks Discover recurring billing solutions that address delayed deposits and chargeback threats together. Learn which platforms offer faster funding, intelligent payment recovery, and proactive dispute prevention for established eCommerce businesses. TL;DR Guaranteed next-day funding with chargeback defense addresses both sides of […]