The Real Cost of Capital: Why Investors Should Read a Term Sheet Like a Merchant Statement Most business owners learn to distrust the headline number eventually, usually after paying it.The difference between the rate you were quoted and the money that actually leaves your account often lives in fees nobody explained at signing. Real estate […]

Category: Fraud Prevention

Featured Article

The Real Cost of Capital: Private Lending Q&A | We Lend

Why treating security as a revenue driver—not a cost center—unlocks the approval rates your business deserves Learn why authorization rate improvement depends on fraud protection more than most realize. This guide reveals how security signals influence bank decisions and which changes produce measurable gains. TL;DR Fraud protection drives authorization rates – Banks reward merchants with […]

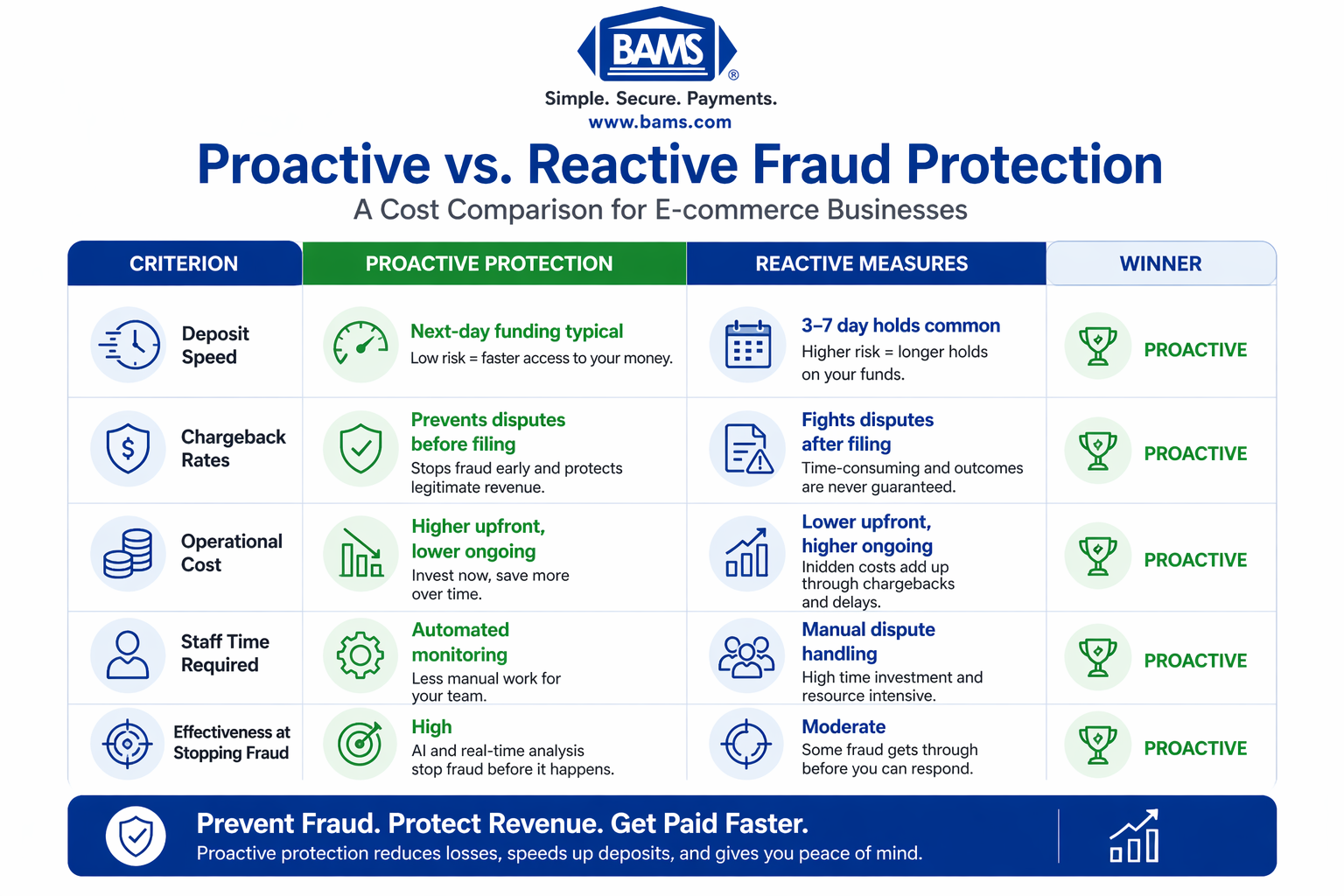

Why waiting for chargebacks to happen costs more than preventing them in the first place Compare proactive and reactive fraud protection measures side-by-side. Learn which approach delivers faster deposits, lower chargeback rates, and better ROI for your e-commerce business. TL;DR Proactive fraud protection prevents chargebacks before they happen – AI-based systems analyze transactions in real-time, […]

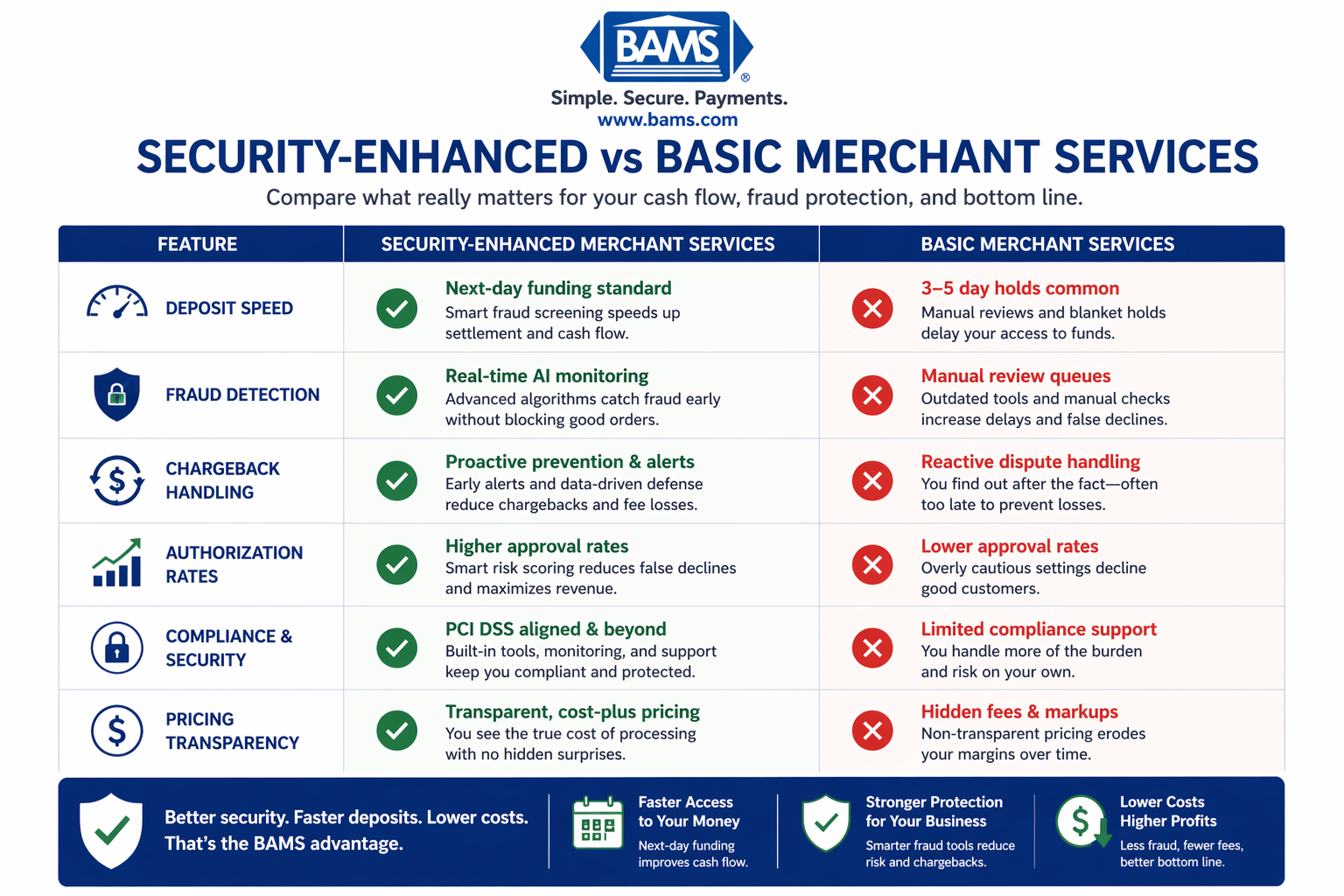

How payment security enhancements affect your cash flow, fraud rates, and deposit speed Learn which merchant services protect your revenue without delaying deposits. This comparison reveals how fraud protection measures impact cash flow and why security-first providers outperform reactive alternatives. TL;DR Security-enhanced merchant services speed up deposits by using real-time fraud detection instead of manual […]

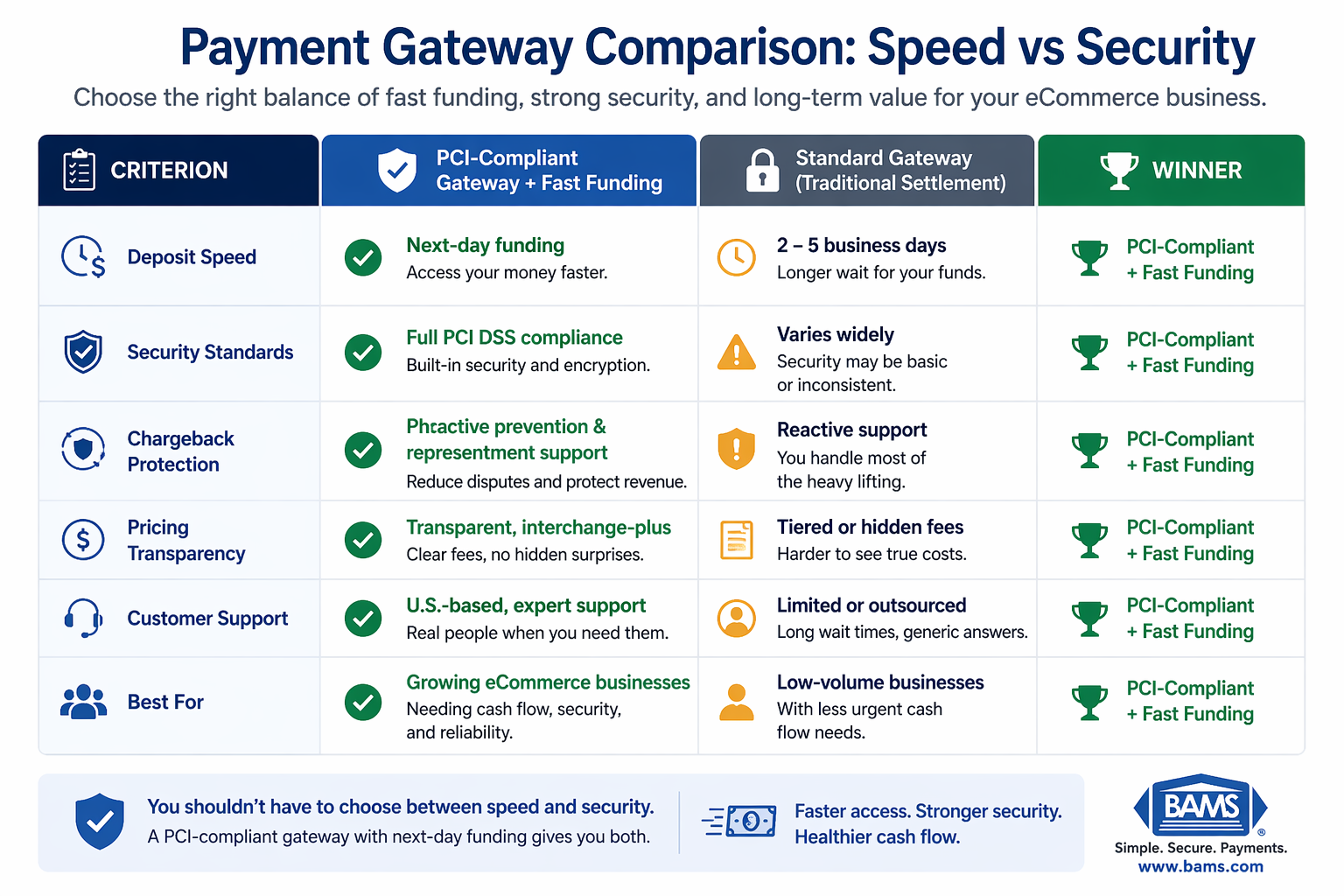

How to choose a PCI-compliant gateway that protects transactions without trapping your cash flow Compare PCI-compliant payment gateways with rapid funding against standard options. Learn which approach delivers both security and speed for predictable eCommerce cash flow. TL;DR Guaranteed next-day funding beats standard 2-5 day settlement for established eCommerce businesses where cash flow directly impacts […]

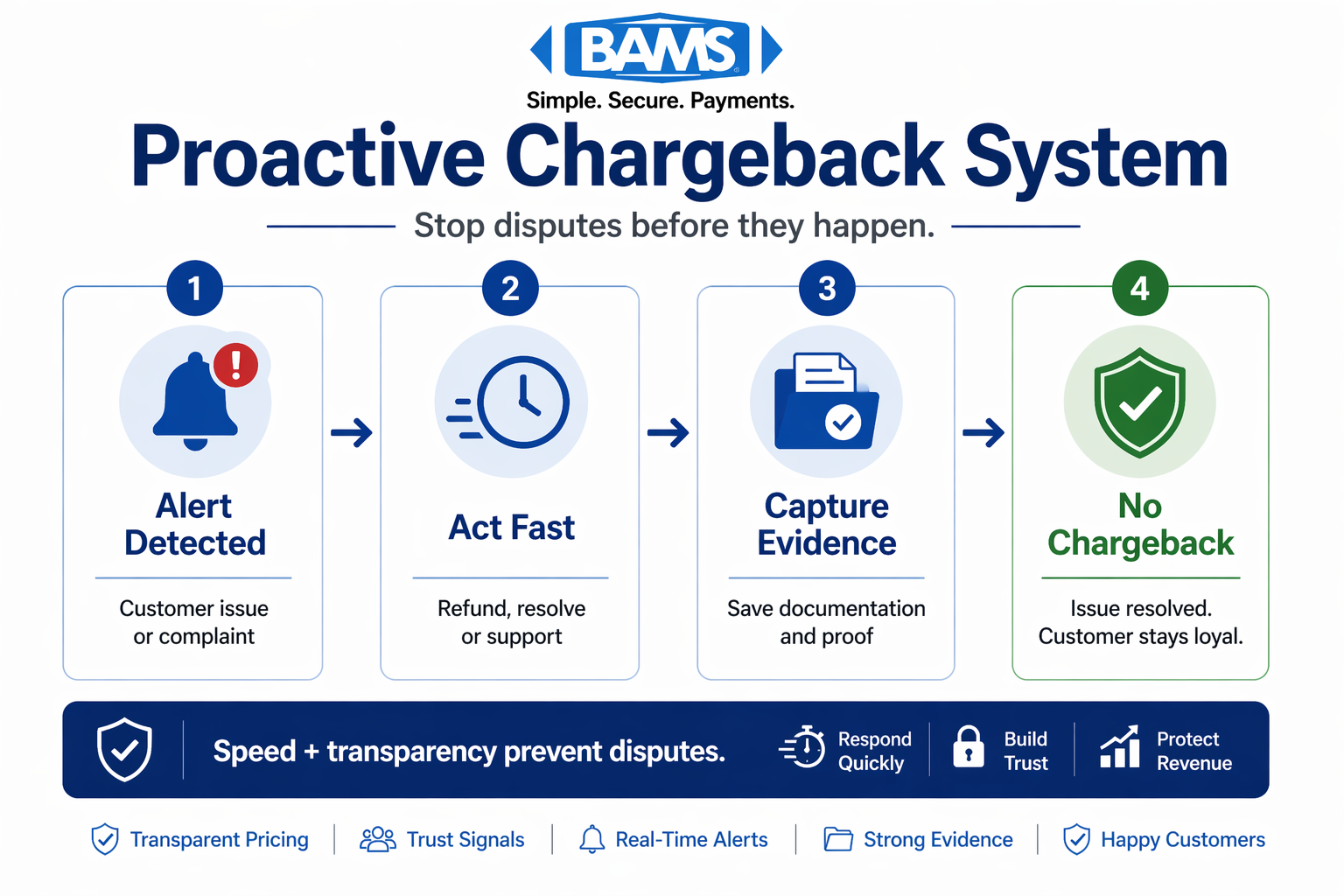

A step-by-step tutorial for catching disputes early, displaying transparent pricing, and adding trust signals that protect your cash flow Learn to configure dispute alerts, create pricing transparency, and integrate checkout trust signals. This 4-6 hour implementation gives you a documented workflow that catches chargebacks before they escalate. TL;DR Audit your exposure first – Export 90 […]

Why the small line item you never question says everything about your merchant services relationship Learn why PCI compliance fees are the clearest indicator of whether your payment processor treats you as a partner or a revenue source. Discover what you should actually receive for this charge and how to evaluate providers based on transparency. […]

The Growing Challenge of Card-Not-Present Fraud At BAMS, payments are central to everything we do and card-not-present fraud prevention is important to us. That is why we closely track emerging threats across the payments ecosystem. One of the most significant challenges facing merchants today is the rise of card-not-present (CNP) fraud and first-party fraud, sometimes […]

Chargebacks are an unfortunate reality of doing business, and sometimes customers are fully within reason to file one. But, what happens when chargebacks are abused? Unfortunately, the dispute process is heavily weighted towards the customer, and far too many merchants have fallen victim to lost revenue from fraudulent chargebacks. But, like all types of fraud, […]

The coronavirus pandemic that rocked the world in 2020 saw people flock to the web for everything from entertainment to education to work to shopping, and beyond. But with that surge in web traffic came a surge in cyberattacks and ecommerce fraud. With payment fraud losses already set to reach $6.4 billion in 2021 prior […]

Fraud is expensive. Not only does it have the potential to rob your ecommerce store of revenue and inventory, but, if left unchecked, it can also put you in the doghouse with card issuers and payment processors, driving up your fees as well. That makes combating fraud an important part of your online business strategy. […]

Learn how to lower your credit card processing fees and save money.

In 2018, almost 5,900 brick and mortar retail locations closed. 2019 has seen another 6,000 go the way of the dodo, and by 2026, as many as 75,000 stores will shut their doors permanently. The reality is, brick and mortar stores are expensive – far more expensive than their web-based eCommerce counterparts. As a result, […]

In part one of this two-part series, we looked at some of the technology-based solutions merchants have available to them to catch fraud early on and stop it before it can result in chargebacks and lost revenues. In part two, we’ll look at the other side of the coin – legitimate chargebacks filed by customers […]

A seller receives an order and delivers on their end of the bargain flawlessly, only to later find that the money they earned has been clawed back due to a chargeback. This is an all too common scenario, especially in commerce online where purchases are made without any physical, real-world interaction between customer and merchant. […]

Chargebacks are a reality of accepting credit card payments. While many chargebacks are requested for valid reasons, there are plenty of cases in which disputes are initiated despite the merchant holding up every aspect of their end of the bargain. Unfortunately, many merchants don’t really understand the dispute process, how to handle a chargeback, or […]

For obvious reasons, the major credit card companies take fraud and excessive chargebacks very seriously, and companies like Visa and Mastercard have put forward thorough monitoring and tracking systems to try to prevent the losses associated with them. In October 2019, both companies made changes to their chargeback and fraud defense programs, and it’s important […]

Part of establishing PCI compliance and maintaining it year in and year out is filling out an annual PCI self-assessment questionnaire (SAQ). These questionnaires are designed to accomplish two goals: to help businesses identify weaknesses that need to be dealt with and to help prove to institutions that a company is compliant. But not all […]

E-commerce transactions are all about trust. Customers need to feel 100% confident that their personal information and payment details are stored and transmitted with total security, or they simply won’t make a purchase. When breaches do happen, the damage – both financially and psychologically – can be immense, and as a result, businesses simply can’t […]