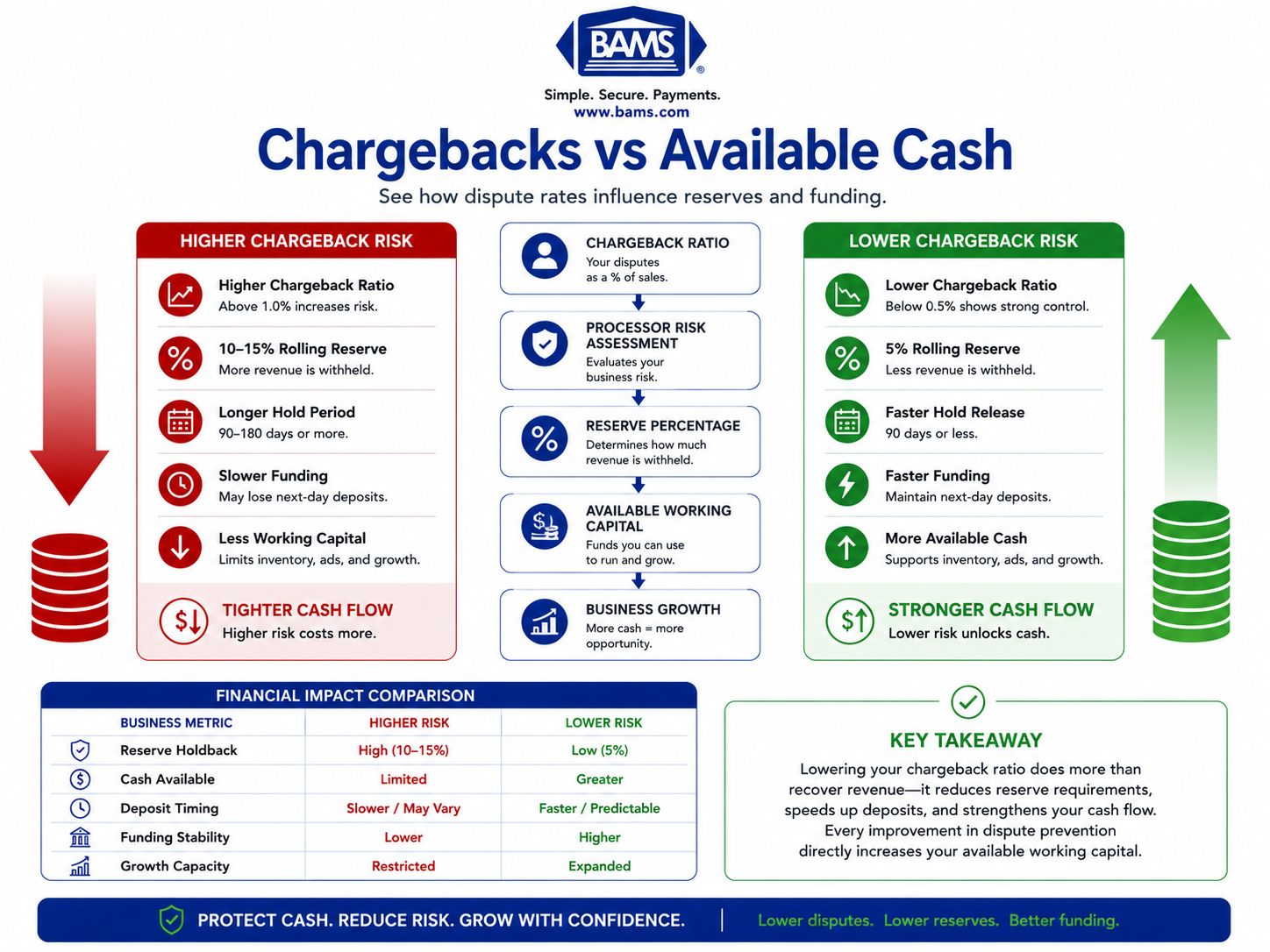

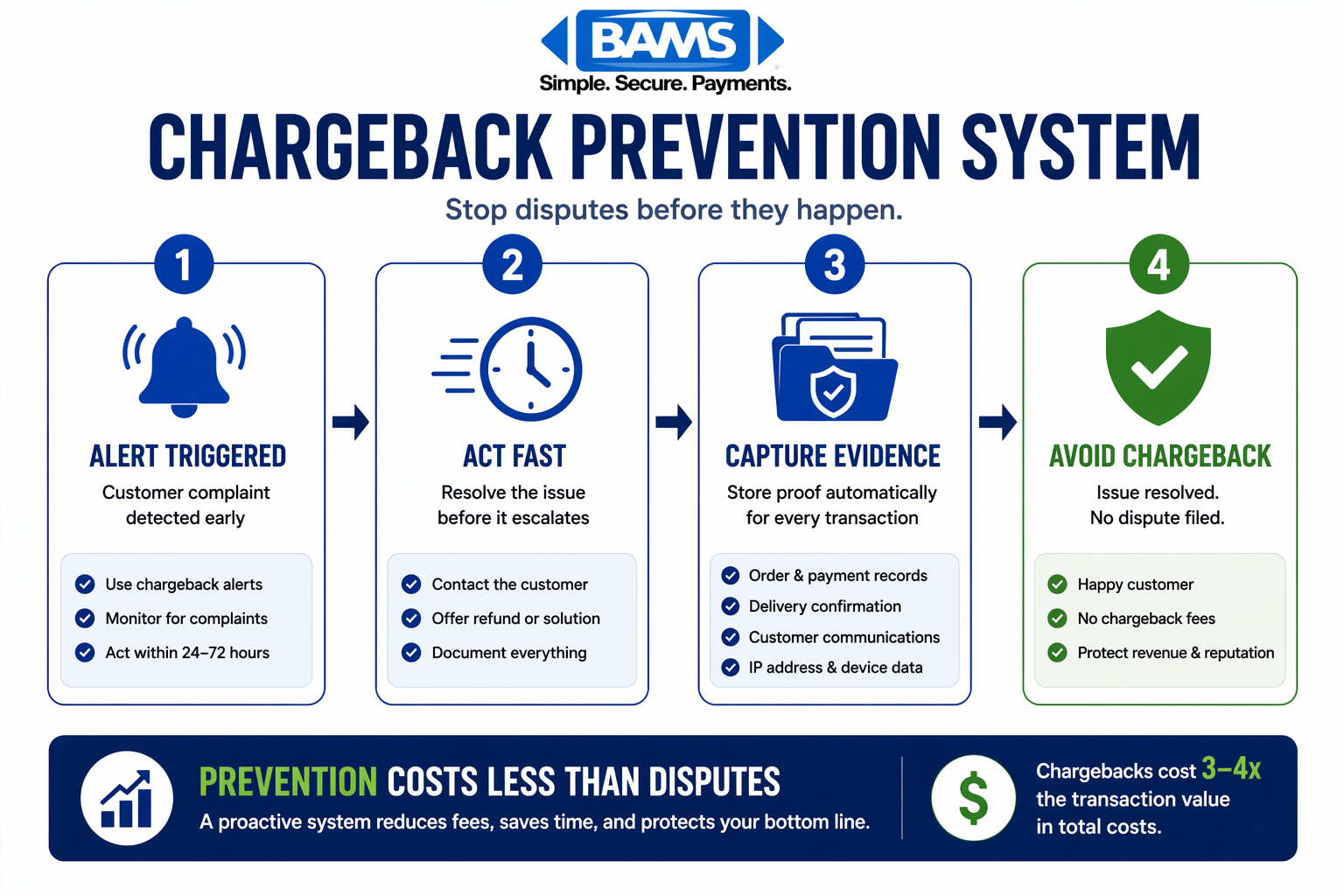

A step-by-step chargeback defense workflow that lowers rolling reserves and protects next-day funding Learn a layered chargeback prevention workflow that directly reduces rolling reserve holdbacks and keeps your deposit schedule predictable. Each step connects a specific defense action to a measurable funding outcome. TL;DR Chargebacks directly control your funding terms – Your chargeback ratio determines […]

Category: Chargeback Prevention

Featured Article

eCommerce Funding Solutions: Defend Your Deposits

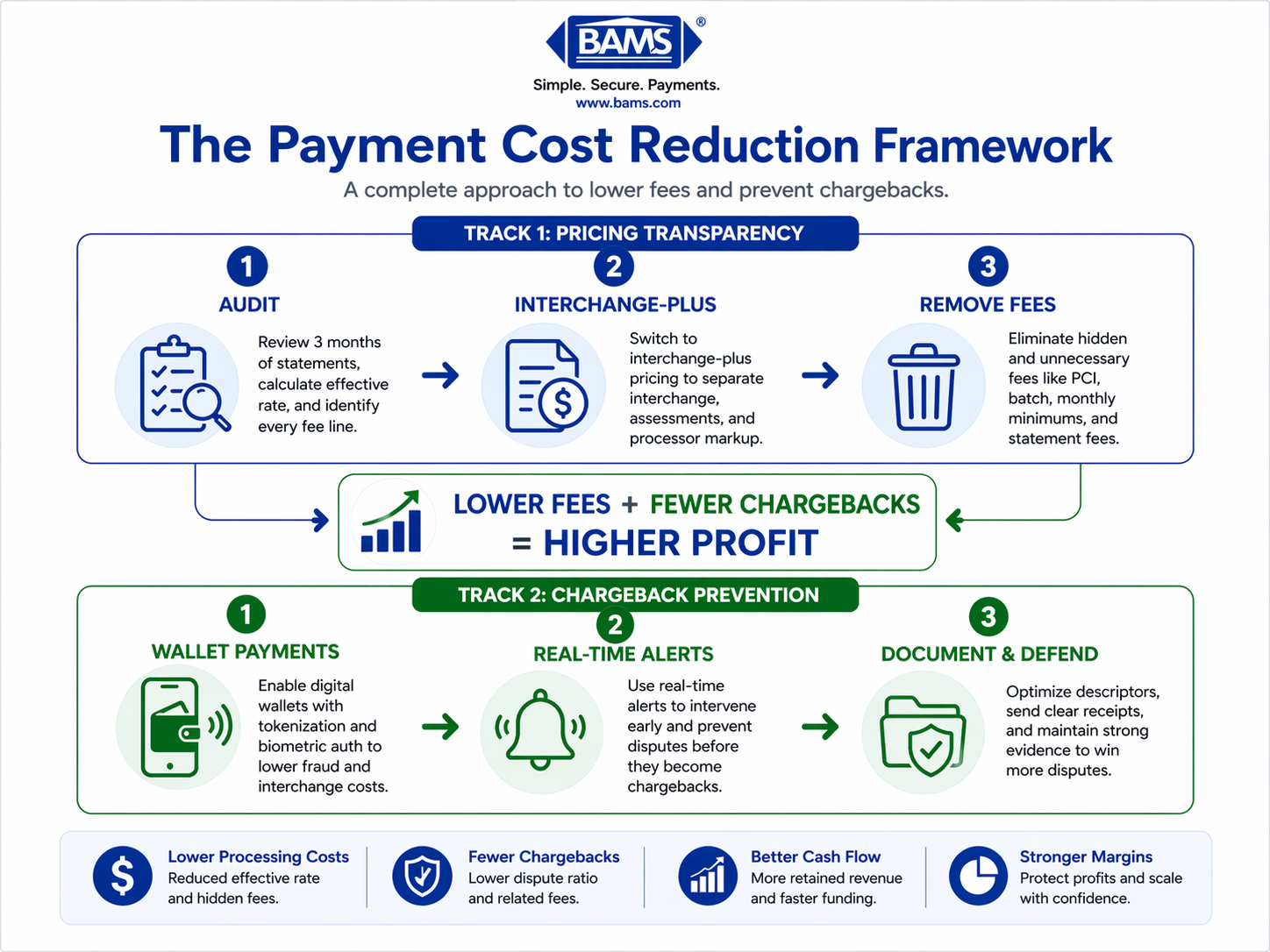

How eCommerce managers can cut processing fees and dispute losses with transparent pricing and digital wallet strategies Learn how to audit your effective processing rate, eliminate hidden fees, and implement chargeback prevention methods that protect margins. This guide covers processor statement analysis, digital wallet payment optimization, and building a prevention-first cost reduction system. TL;DR Transparency […]

How eCommerce managers can cut processing fees and dispute losses with transparent pricing and digital wallet strategies Learn how to audit your effective processing rate, eliminate hidden fees, and implement chargeback prevention methods that protect margins. This guide covers processor statement analysis, digital wallet payment optimization, and building a prevention-first cost reduction system. TL;DR Transparency […]

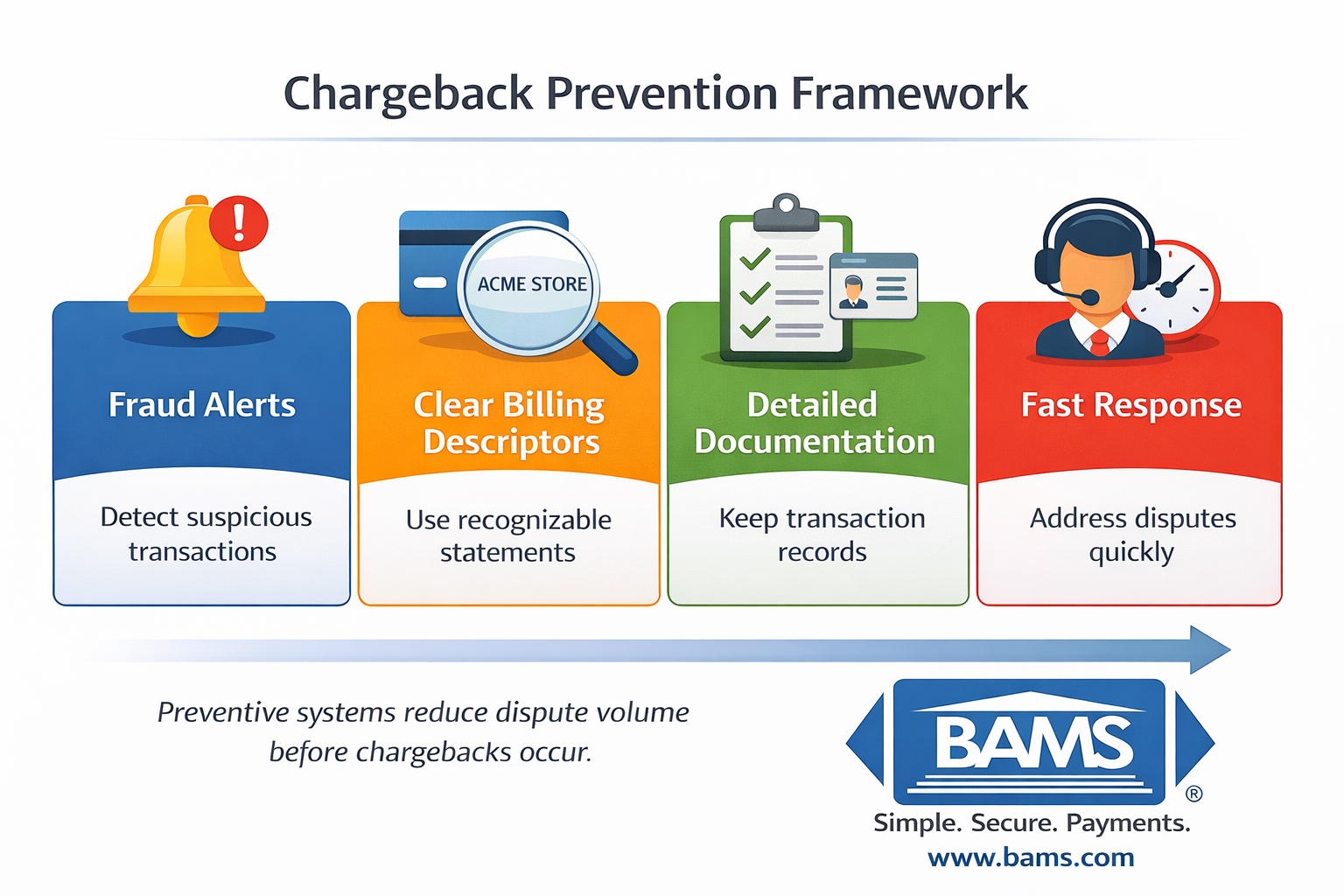

Configure fraud filters, optimize billing descriptors, and automate alerts that catch disputes before they cost you money Learn to build a layered fraud protection system that blocks suspicious transactions while keeping authorization rates above 95%. This step-by-step guide covers real-time filters, descriptor optimization, and automated monitoring. TL;DR Audit your chargebacks first – Export 90 days […]

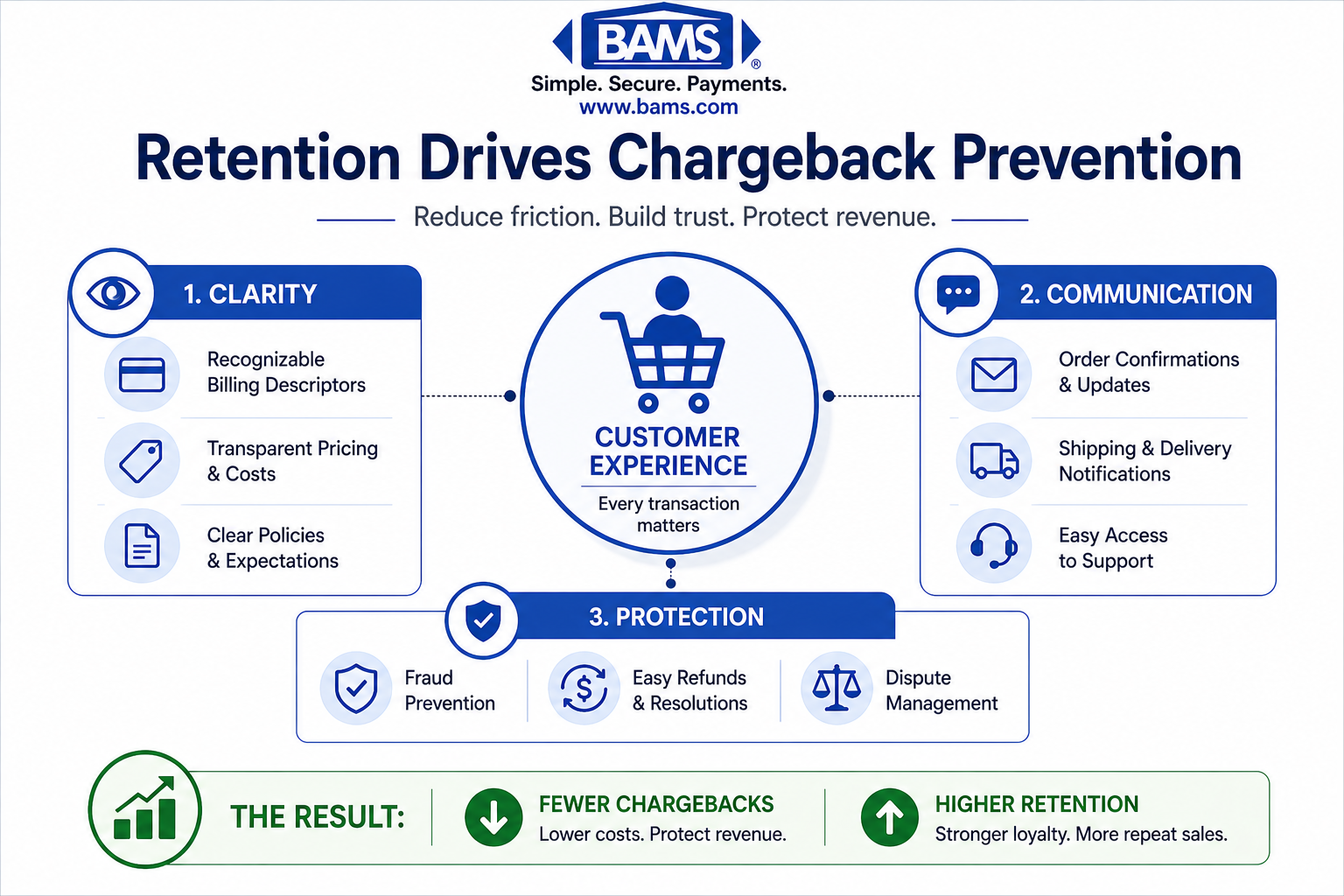

How payment security enhancements build loyalty and protect your revenue from costly disputes Learn customer retention methods that reduce chargebacks and build trust. This guide covers payment security enhancements that keep customers returning while protecting your bottom line. TL;DR Billing descriptors matter – Customers dispute charges they don’t recognize. Update your descriptor to show your […]

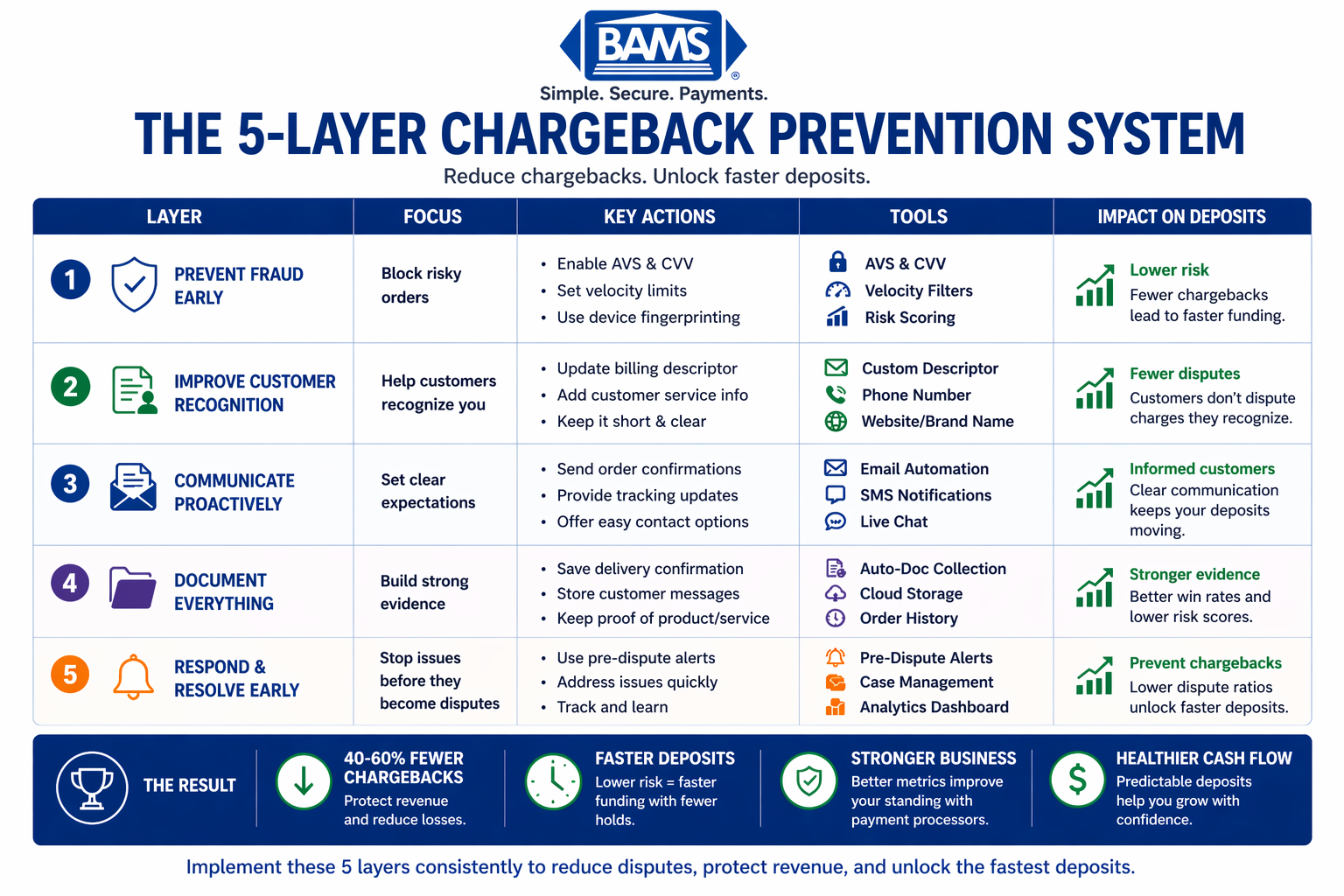

Build a multi-layer defense system that cuts disputes by 40-60% and qualifies you for accelerated funding Learn to implement a complete chargeback prevention system that reduces disputes and speeds up your deposit timeline. This step-by-step tutorial covers transaction verification, customer communication, and dispute response automation. TL;DR Chargebacks directly delay your deposits – Processors use your […]

Step-by-step tutorial to recover failed transactions, prevent chargebacks, and reduce cart abandonment Learn to build a payment recovery system that boosts recovery rates from 40% to 85%. This tutorial covers automated retry logic, strategic recovery emails, and chargeback prevention tactics. TL;DR Audit your failures first – Export 90 days of decline data and identify your […]

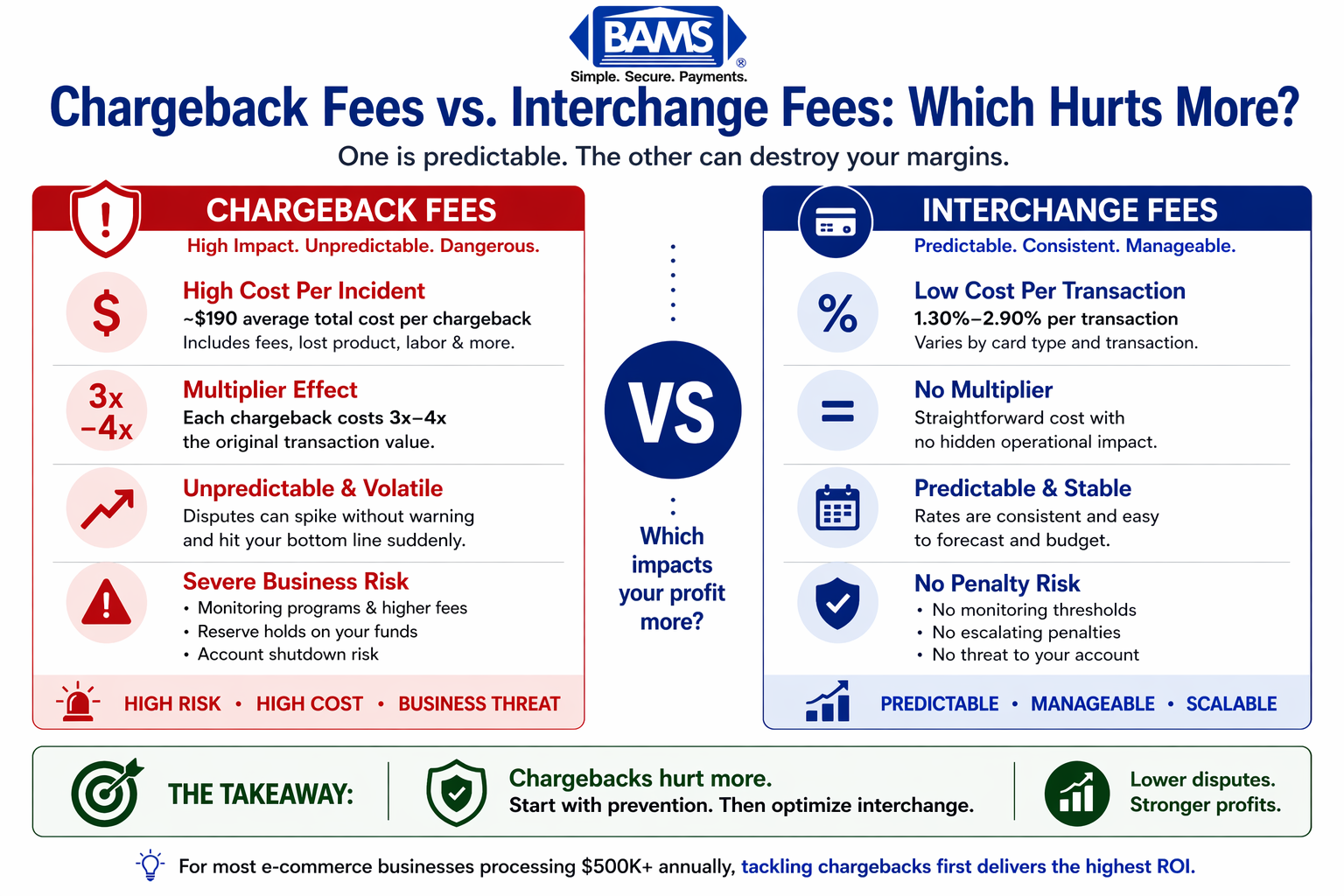

A side-by-side comparison to help eCommerce owners decide where to focus their cost-reduction efforts first Learn which payment fee deserves your attention first. This comparison breaks down the true costs of chargeback and interchange fees, with a decision framework for businesses processing $500K or more annually. TL;DR Chargeback fees hurt more per incident – Each […]

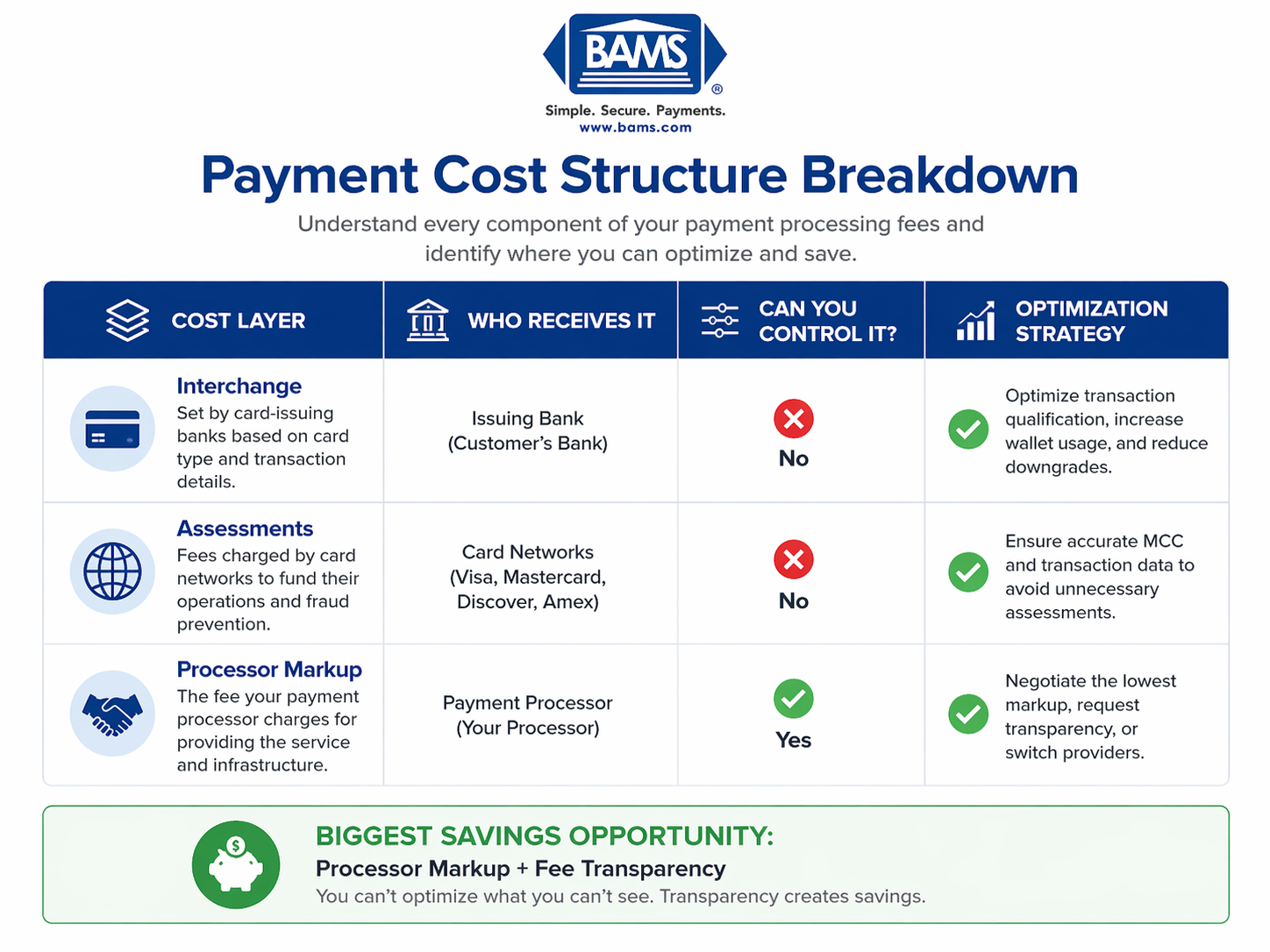

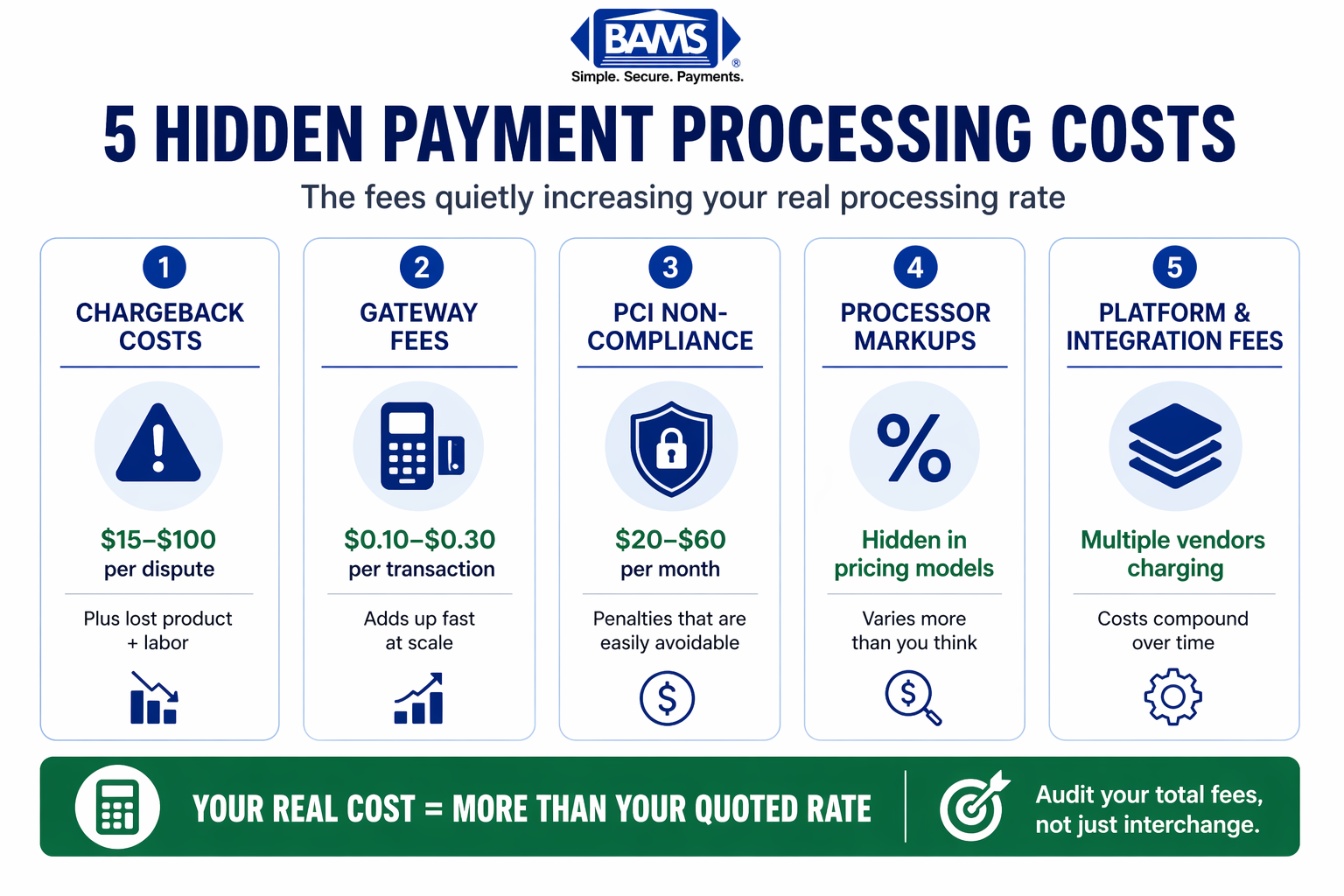

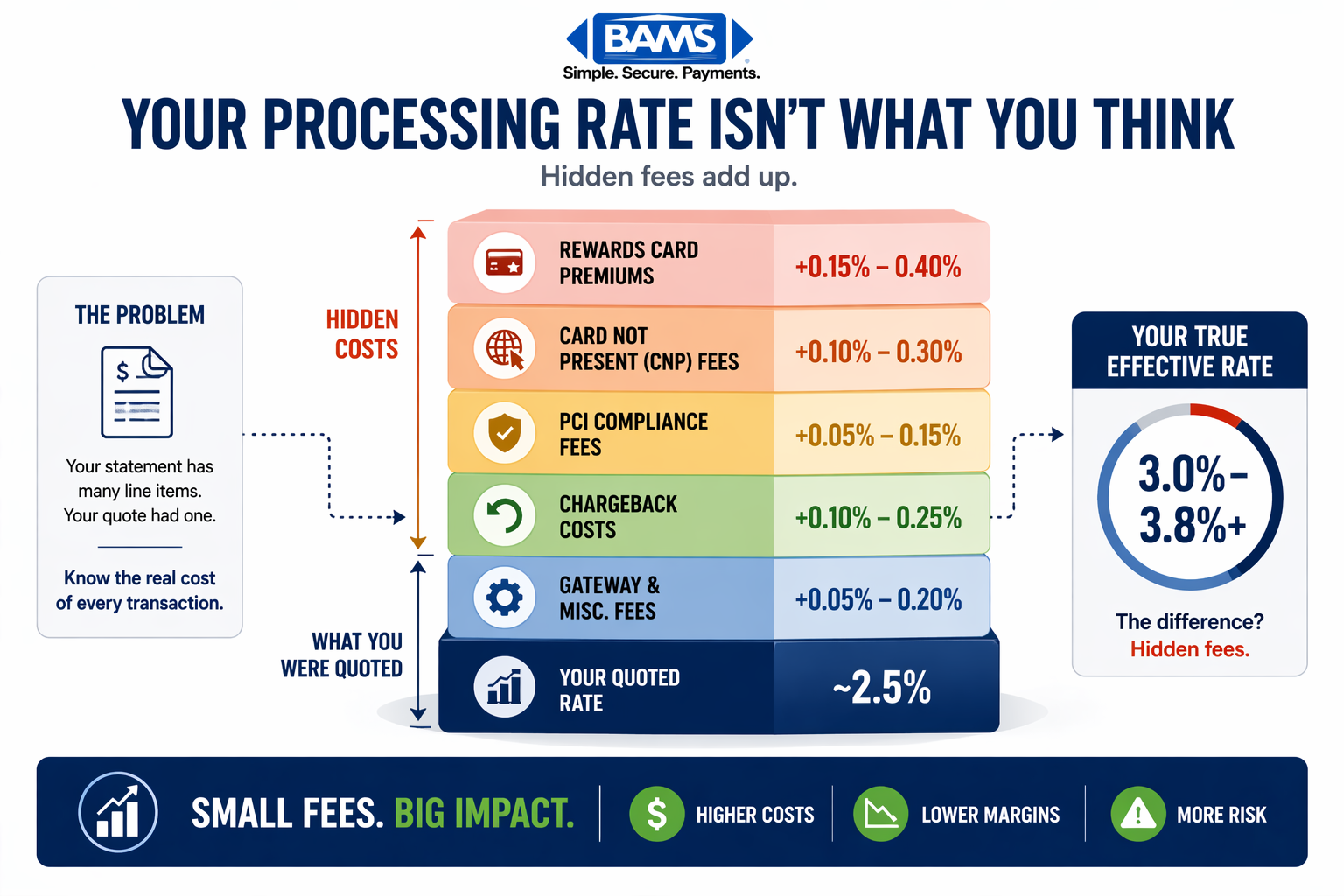

Beyond interchange fees: the overlooked charges silently eroding your margins each month Discover five specific cost categories your payment processor may be hiding or downplaying. Learn which line items to audit and how to calculate your true processing costs. TL;DR Chargeback fees multiply fast – Direct costs of $15 to $100 per dispute plus $50 […]

How to Cut Chargeback Fees by 40-60% in 90 Days A step-by-step defense system for eCommerce merchants processing $50K+ monthly Build a complete chargeback prevention system with early warning alerts, response protocols, and documentation practices. This tutorial transforms reactive firefighting into proactive revenue protection. TL;DR Chargebacks cost 3-4x the transaction value when you factor in […]

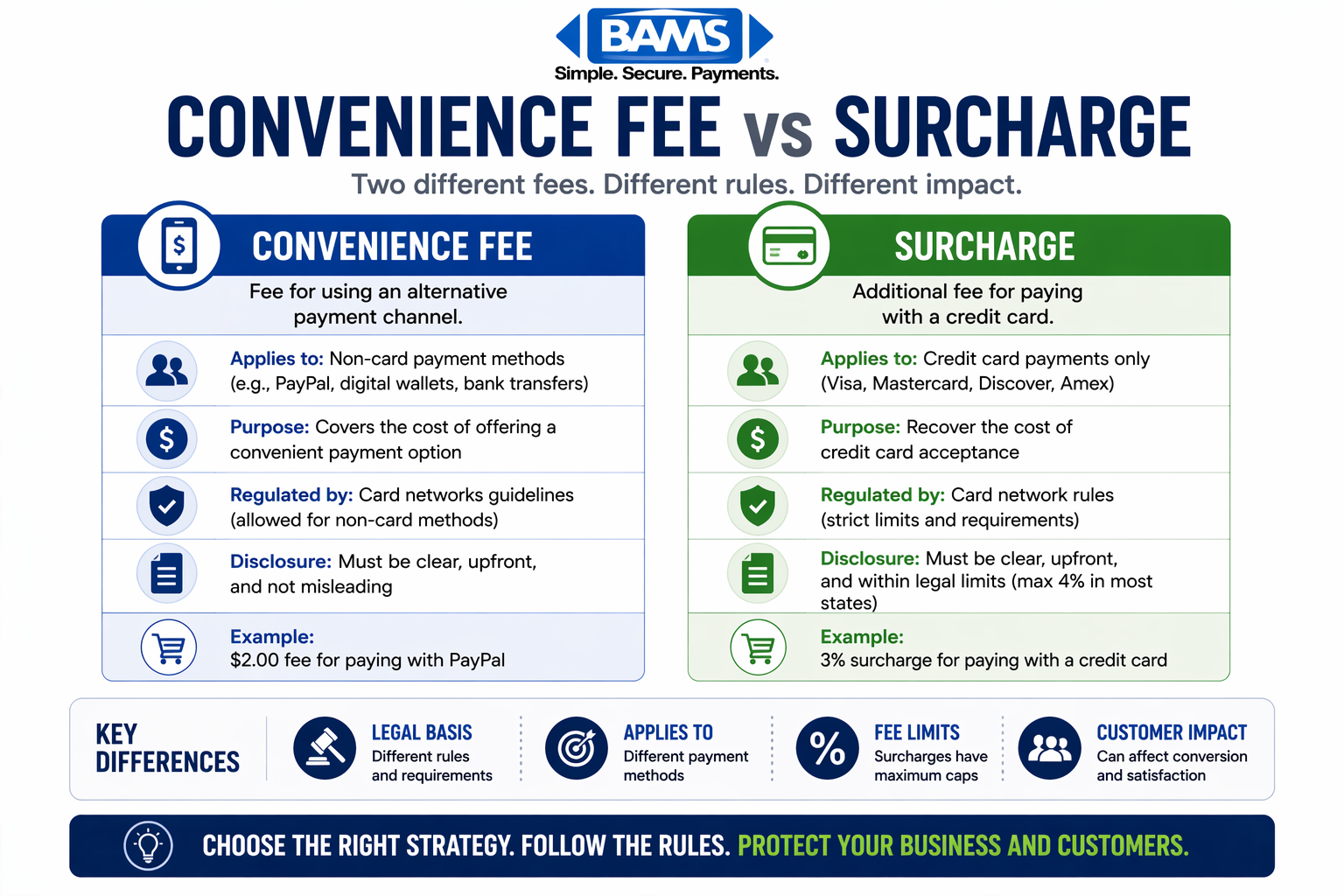

How to evaluate fee-passing strategies without triggering compliance violations or alienating customers Learn the legal and practical differences between convenience fees and surcharges. This guide helps you evaluate whether passing processing costs to customers makes sense for your margins and relationships. TL;DR Surcharges and convenience fees are legally distinct – Surcharges apply to credit card […]

Uncover Hidden Costs Inflating Average Processing Fees Learn about overlooked transaction fees that impact eCommerce businesses’ processing costs. Discover hidden transaction fees that inflate your average processing fees. This list helps eCommerce managers identify and evaluate these costs for better negotiation. TL;DR Over 90% of small businesses overpay on processing – Hidden fees add an […]

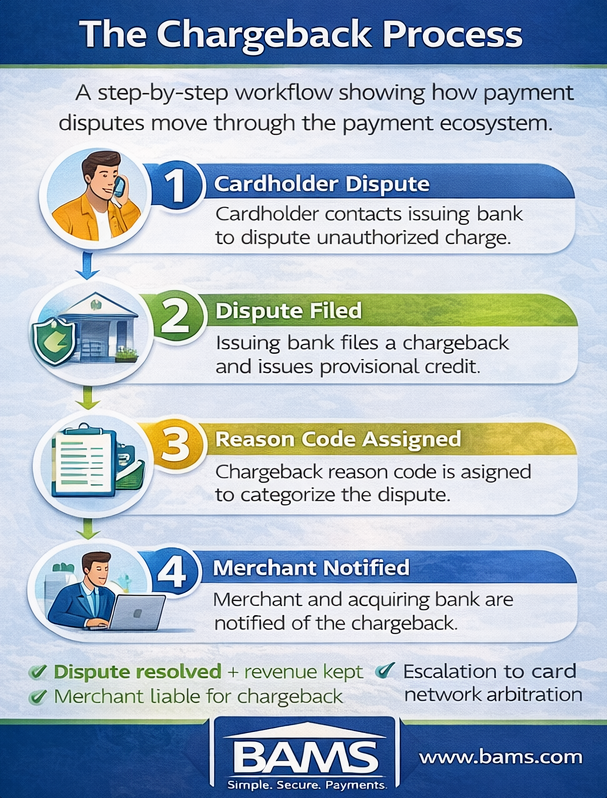

Chargeback codes play a critical role in how payment disputes are classified and resolved in the modern payments ecosystem. As credit card transactions continue to grow across eCommerce, retail, and subscription services, merchants are facing a rising number of payment disputes. Understanding chargeback codes and chargeback reason codes helps businesses identify why disputes occur, respond […]

Chargeback Defense: How to Reduce Disputes & Protect eCommerce Revenue If you accept credit cards online, you need a structured chargeback defense strategy. Chargebacks are not simply refunds—they are forced transaction reversals that increase payment processing costs, damage your processing reputation, and threaten the long-term stability of your merchant account. Without a proactive dispute management […]

Why transparent pricing for processing is no longer optional—and how to protect your margins before disputes hit Learn why chargeback fees catch most ecommerce managers off guard and how information asymmetry in credit card processing costs small businesses more than they realize. Discover what transparent pricing actually looks like. TL;DR Chargeback costs are exploding – […]

Chargebacks are an unfortunate reality of doing business, and sometimes customers are fully within reason to file one. But, what happens when chargebacks are abused? Unfortunately, the dispute process is heavily weighted towards the customer, and far too many merchants have fallen victim to lost revenue from fraudulent chargebacks. But, like all types of fraud, […]

Knowledge is power, yet many merchants operate with an incomplete picture of their payment processing, their transaction history, their ongoing and historical disputes, and more. Advanced merchant reporting tools offered by some payment processors are designed to provide merchants with insights into those key areas in a fast, efficient, and easily-digestible way. Merchant reporting tools […]

Merchants can fight chargebacks and, while many don’t, all should whenever possible because chargebacks matter. Chargebacks cost merchants money in the form of lost revenues and, in many cases, lost inventory. They also raise red flags when they start to rack up, causing potential strains in relationships with payment processors and the major card companies […]

One thing that any business should be aware of when processing digital payments are chargebacks and chargeback prevention. Chargebacks can have a huge impact on business owners, especially for small businesses. The last thing that a business owner wants is to have to refund a customer for services rendered or products shipped, especially when there […]