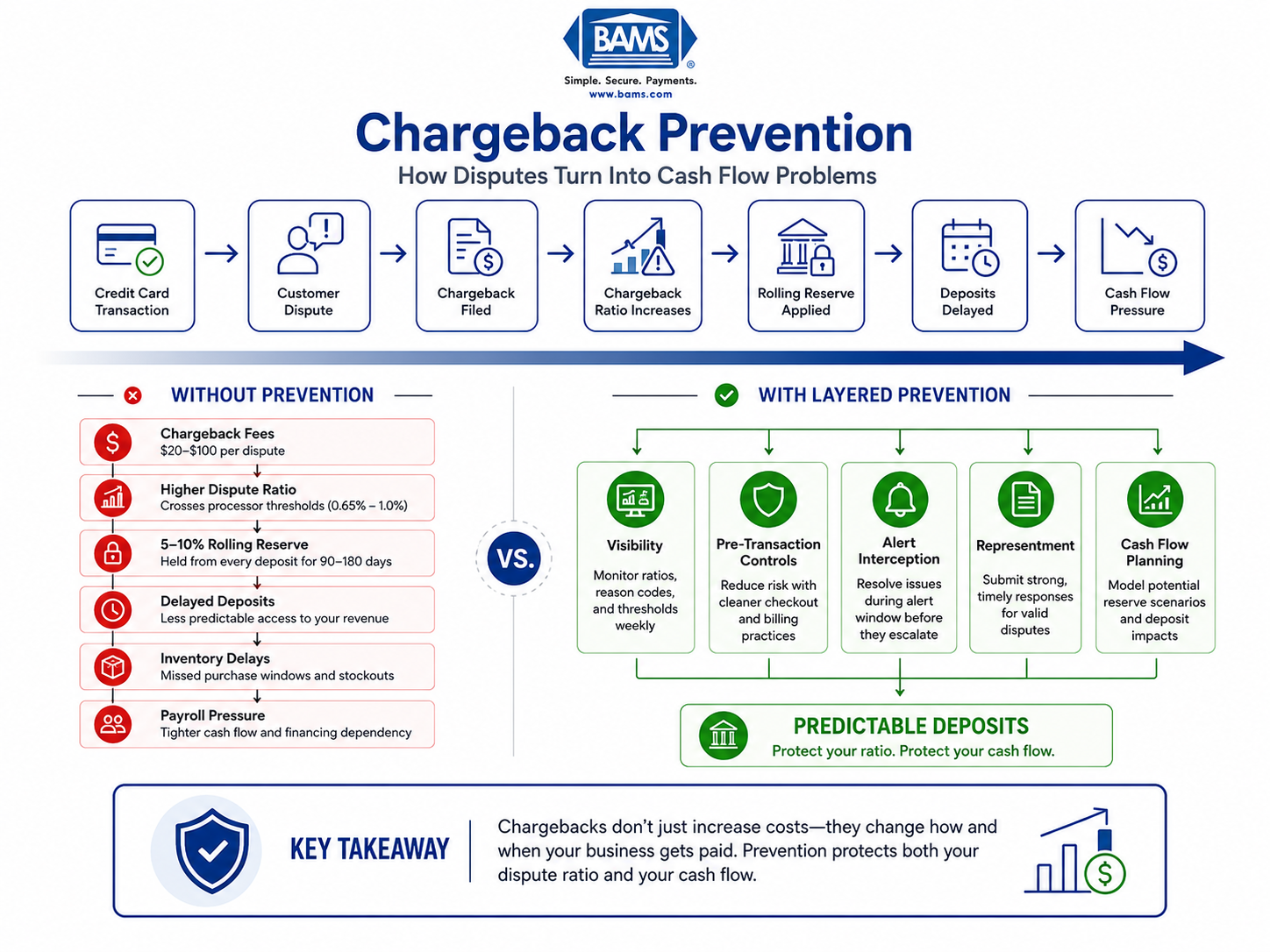

How undefended chargebacks trigger rolling reserves, freeze deposits, and quietly wreck your weekly cash plan Learn how chargeback spikes cascade into rolling reserves and delayed deposits that destabilize your funding cycles. This guide shows eCommerce operators how to build a layered prevention posture that protects predictable cash flow. TL;DR Chargebacks are a cash flow architecture […]

Category: Online Payments

Featured Article

Chargeback Prevention: A Cash Flow Protection Guide

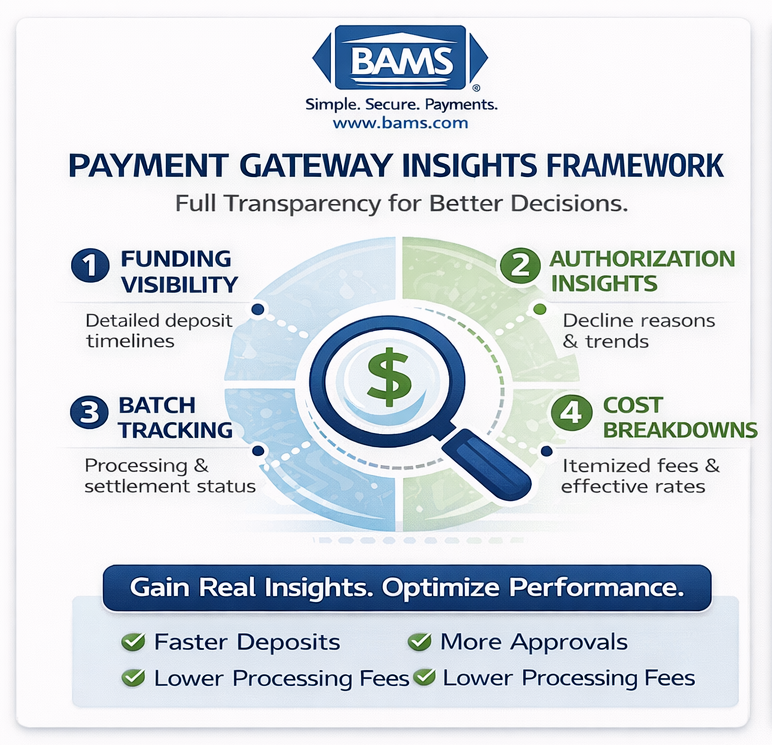

Why most transaction reporting keeps you in the dark—and what real payment gateway insights should look like Discover why payment gateway dashboards show you what happened but not why it matters. Learn what true transparency looks like and how better insights can end deposit delays. TL;DR Payment gateways profit from opacity – The less you understand […]

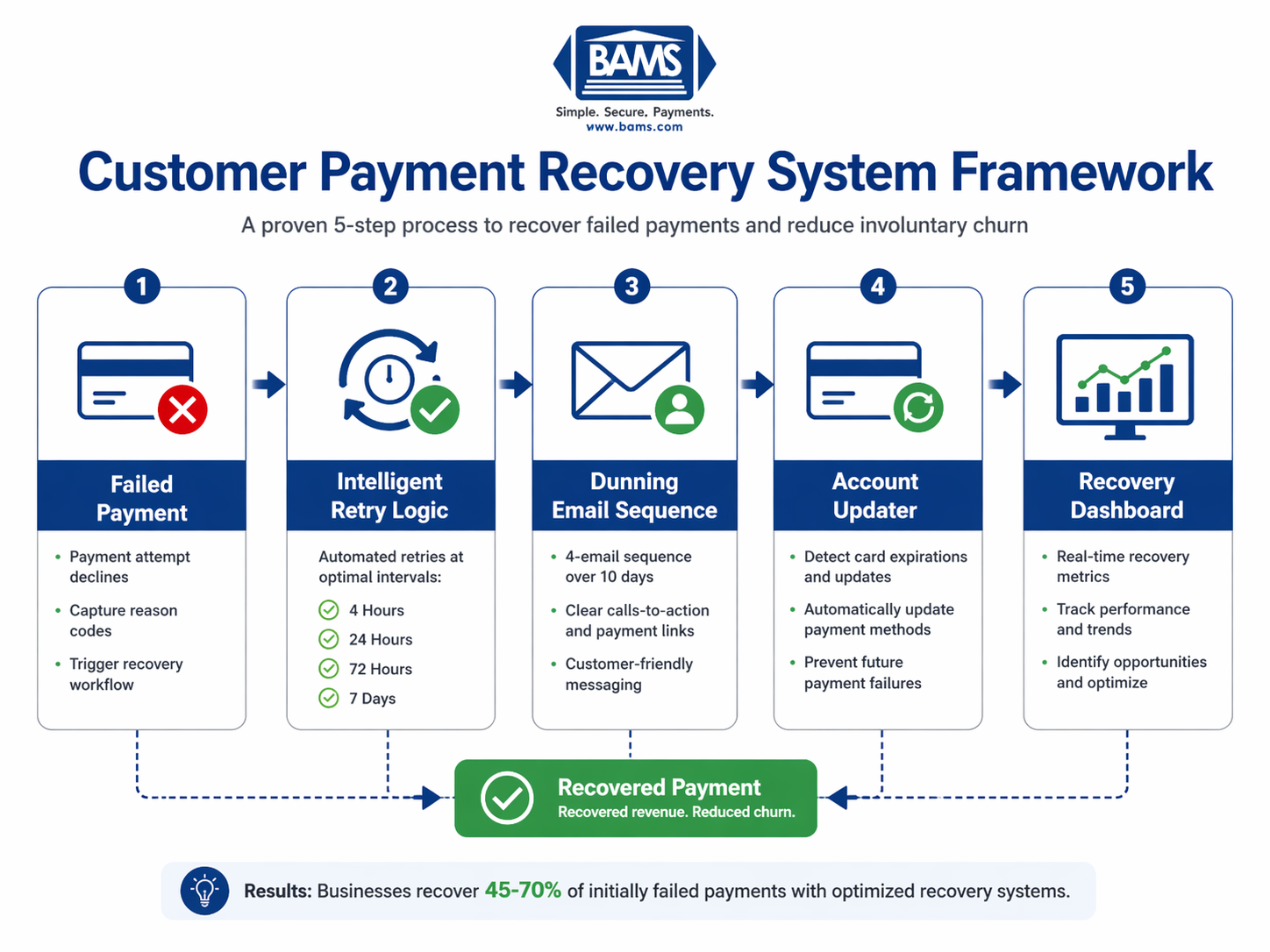

Configure automated retries, dunning sequences, and dashboards to recover 45-85% of failed payments Learn to capture failed transactions before they become lost revenue. This tutorial walks you through retry logic, email sequences, and real-time monitoring to reduce involuntary churn. TL;DR Failed payments are recoverable revenue – Optimized retry strategies recover 45-70% of initially failed transactions, […]

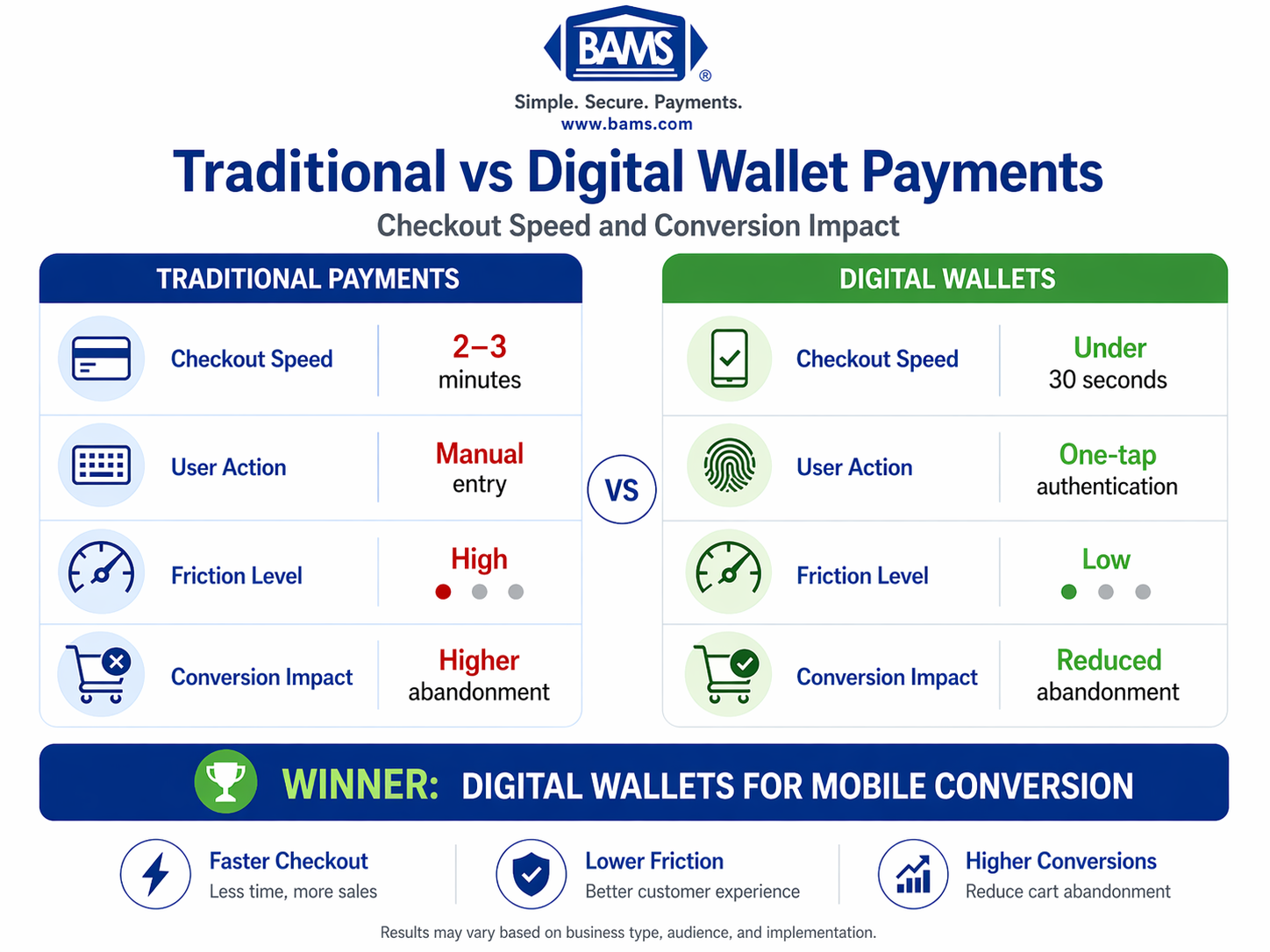

A data-driven comparison of checkout options to help eCommerce managers capture more sales Compare traditional payment methods against digital wallets across mobile performance, checkout friction, and deposit timing. Learn which approach best reduces your cart abandonment rate. TL;DR Offer both payment types – Restricting to traditional-only costs you sales; digital wallets reduce the 80% mobile abandonment […]

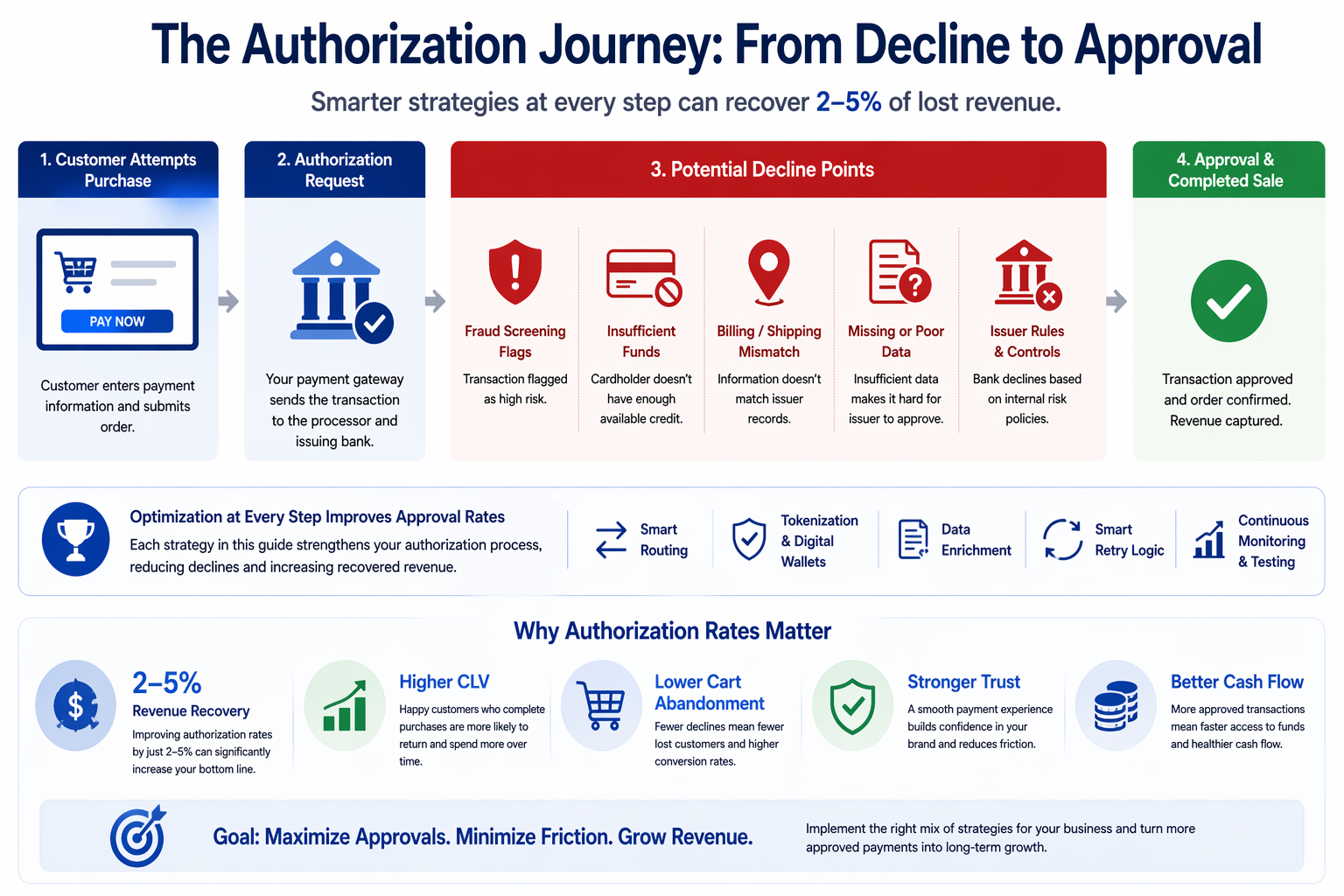

Actionable strategies for eCommerce managers to recover declined payments and capture lost revenue Learn the specific tactics that separate high-performing payment stacks from the rest. This guide covers network tokenization, smart retry logic, and data optimization techniques that can recover 2-5% of previously lost transactions. TL;DR Smart routing recovers 5% of declines by directing transactions […]

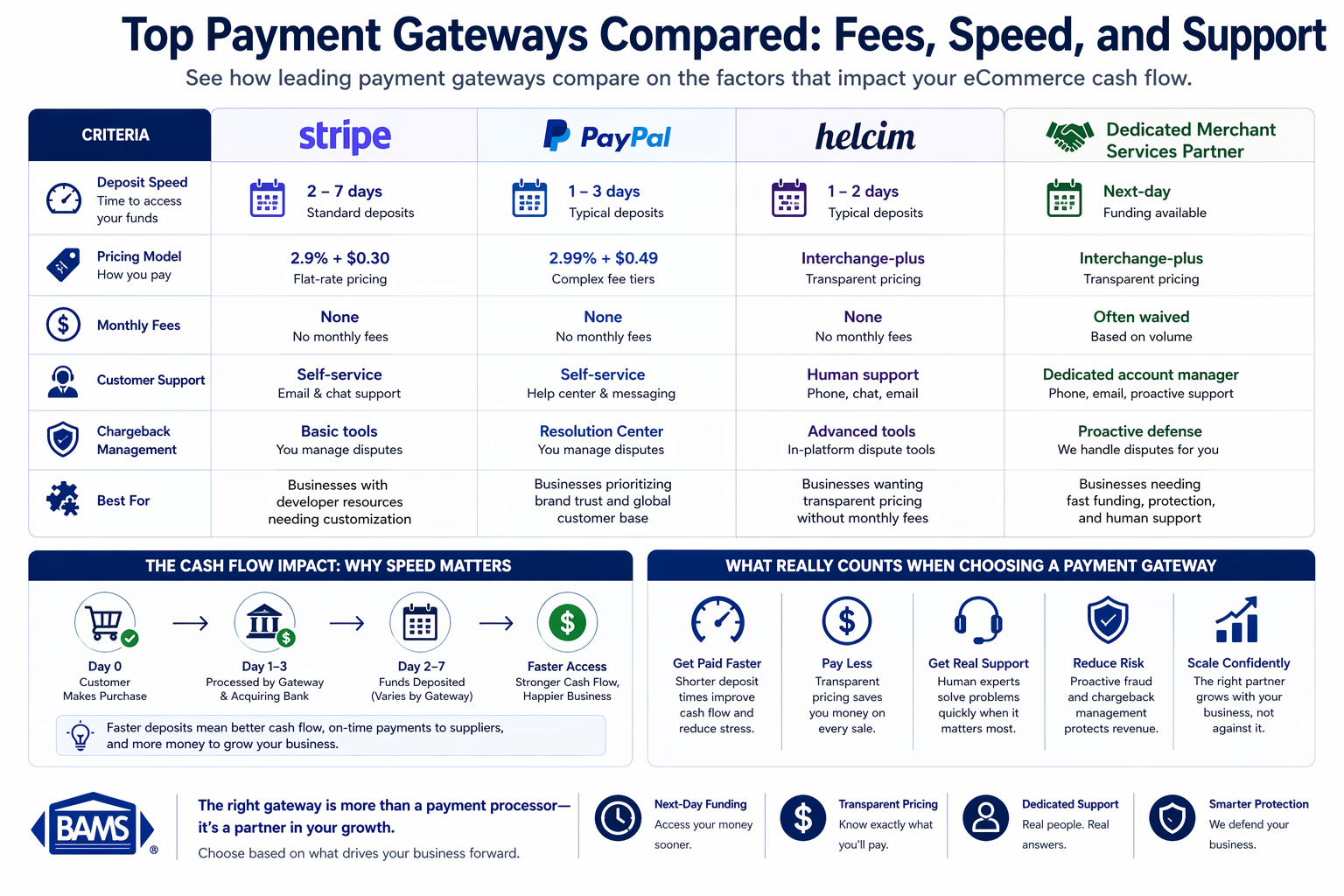

How deposit timing, pricing transparency, and real human support affect your eCommerce cash flow Compare top payment gateways on what actually matters: how fast you get paid, what you really pay in fees, and whether support answers when problems hit. Find the right fit for your 10-50 employee eCommerce operation. TL;DR Deposit speed varies dramatically […]

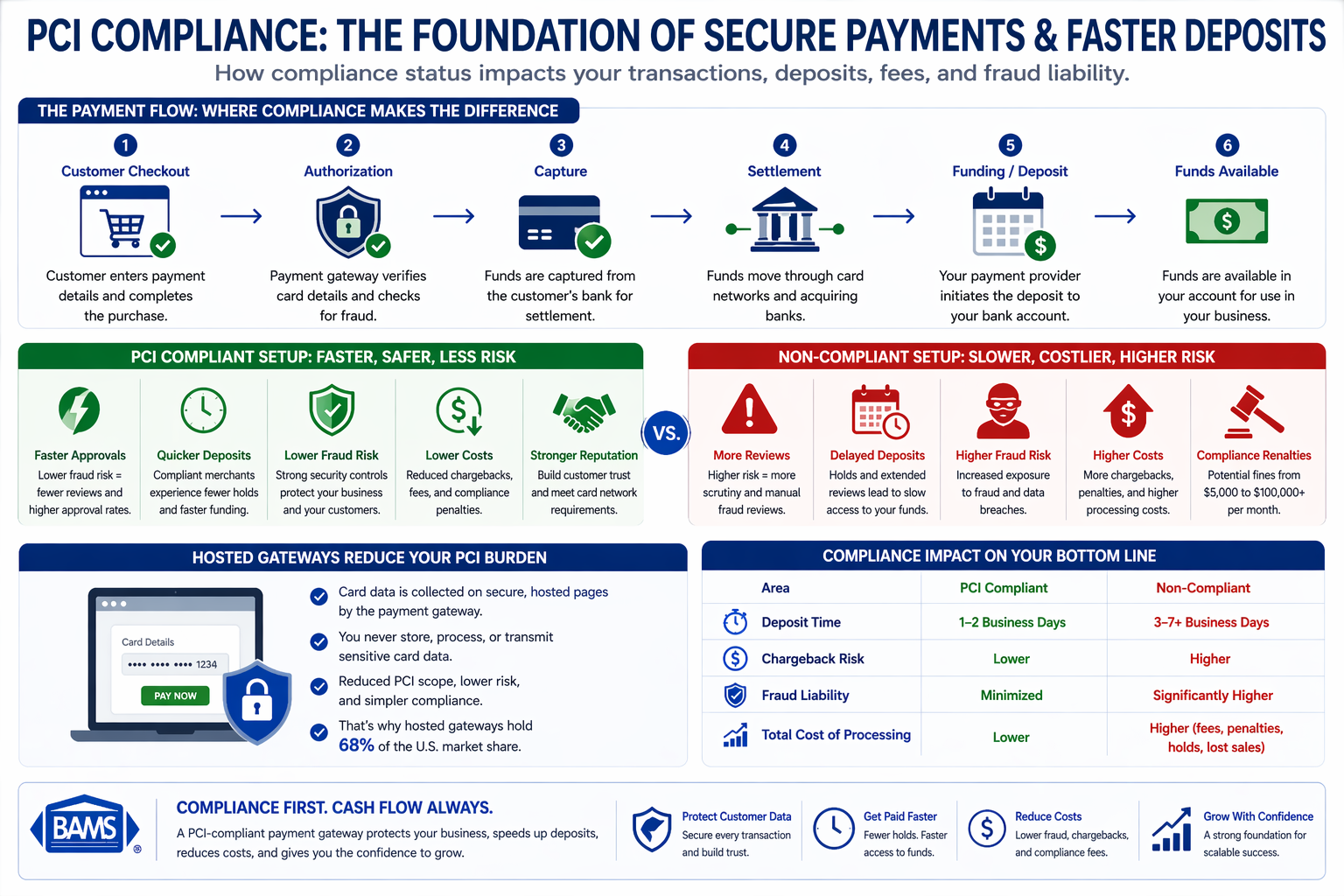

How compliance status affects your deposits, fees, and fraud liability—and what to look for Learn why PCI compliance should be your primary filter when comparing payment gateways. This guide shows how compliance impacts deposit timing, fee structures, and fraud exposure for eCommerce businesses. TL;DR PCI compliance determines deposit speed – Non-compliant setups trigger more fraud […]

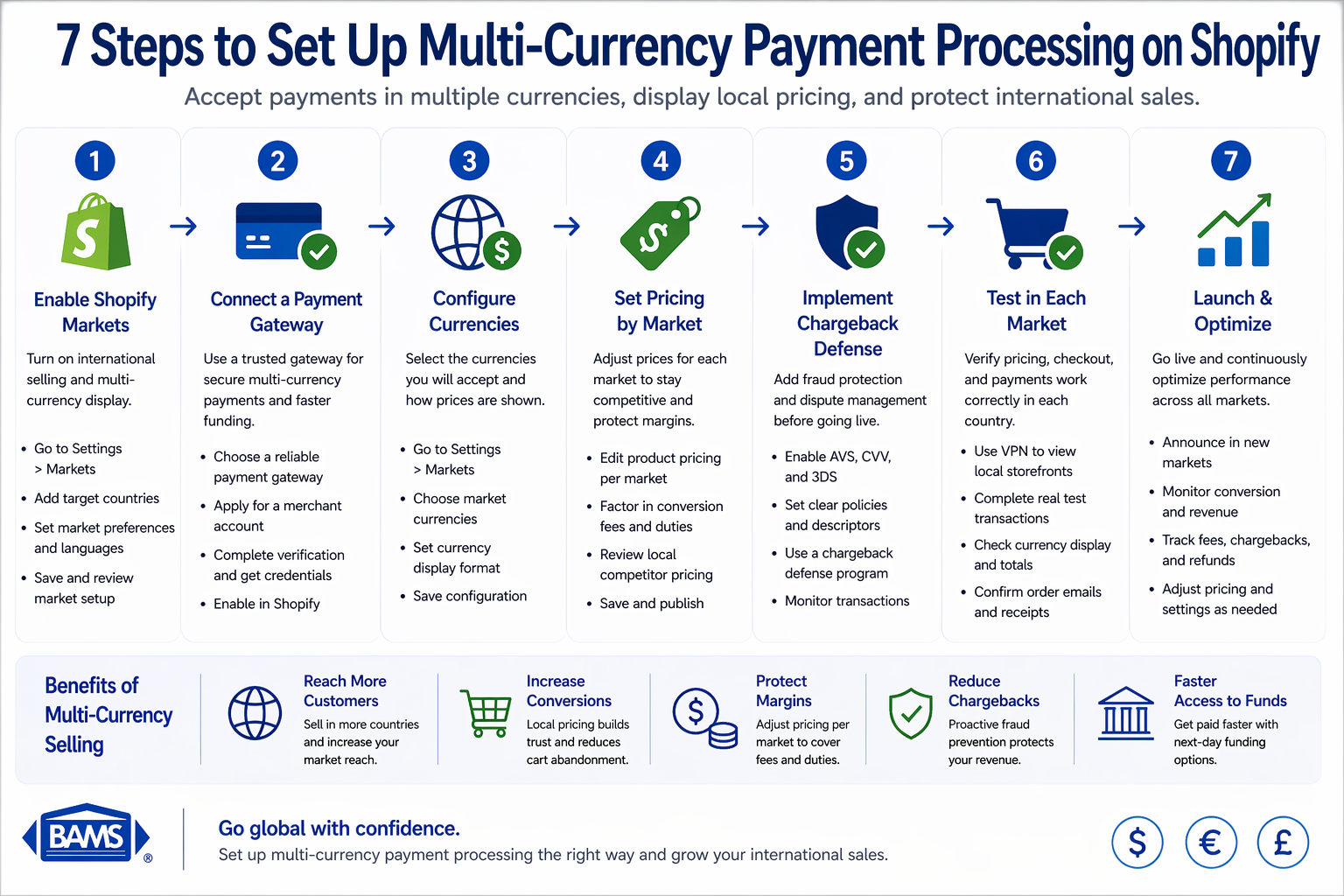

Configure local pricing, connect a secure payment gateway, and protect cross-border sales with chargeback defense Learn to accept payments in multiple currencies on your Shopify store. This tutorial covers currency settings, payment gateway setup, and chargeback protection for international sales. TL;DR Enable Shopify Markets first – This unlocks multi-currency display and international selling features that […]

Why hidden fees kill sales and how clear pricing recovers lost revenue at checkout Learn why unexpected costs drive 70% cart abandonment and how transparent pricing rebuilds trust. Get actionable steps to optimize your checkout experience and recover lost sales. TL;DR Hidden fees cause most cart abandonment – With 70% of carts abandoned and $260 […]

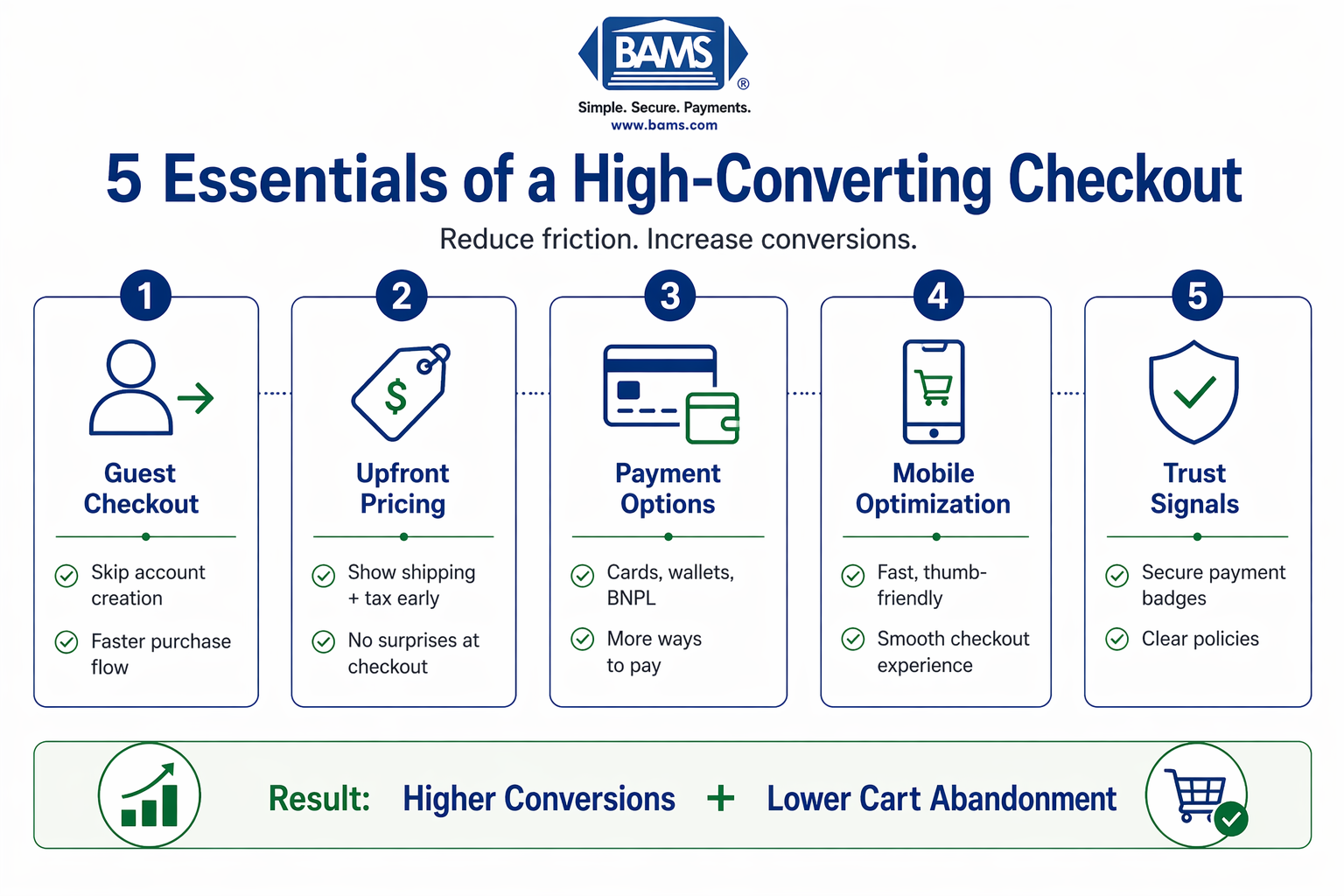

How to Build a Transparent, High-Converting Checkout Set up guest checkout, multiple payment options, and zero hidden fees in under 45 minutes Learn to configure payment gateway solutions that eliminate cart abandonment. This step-by-step tutorial covers guest checkout setup, payment method variety, and transparent pricing displays. TL;DR Enable guest checkout options to eliminate the 24% […]

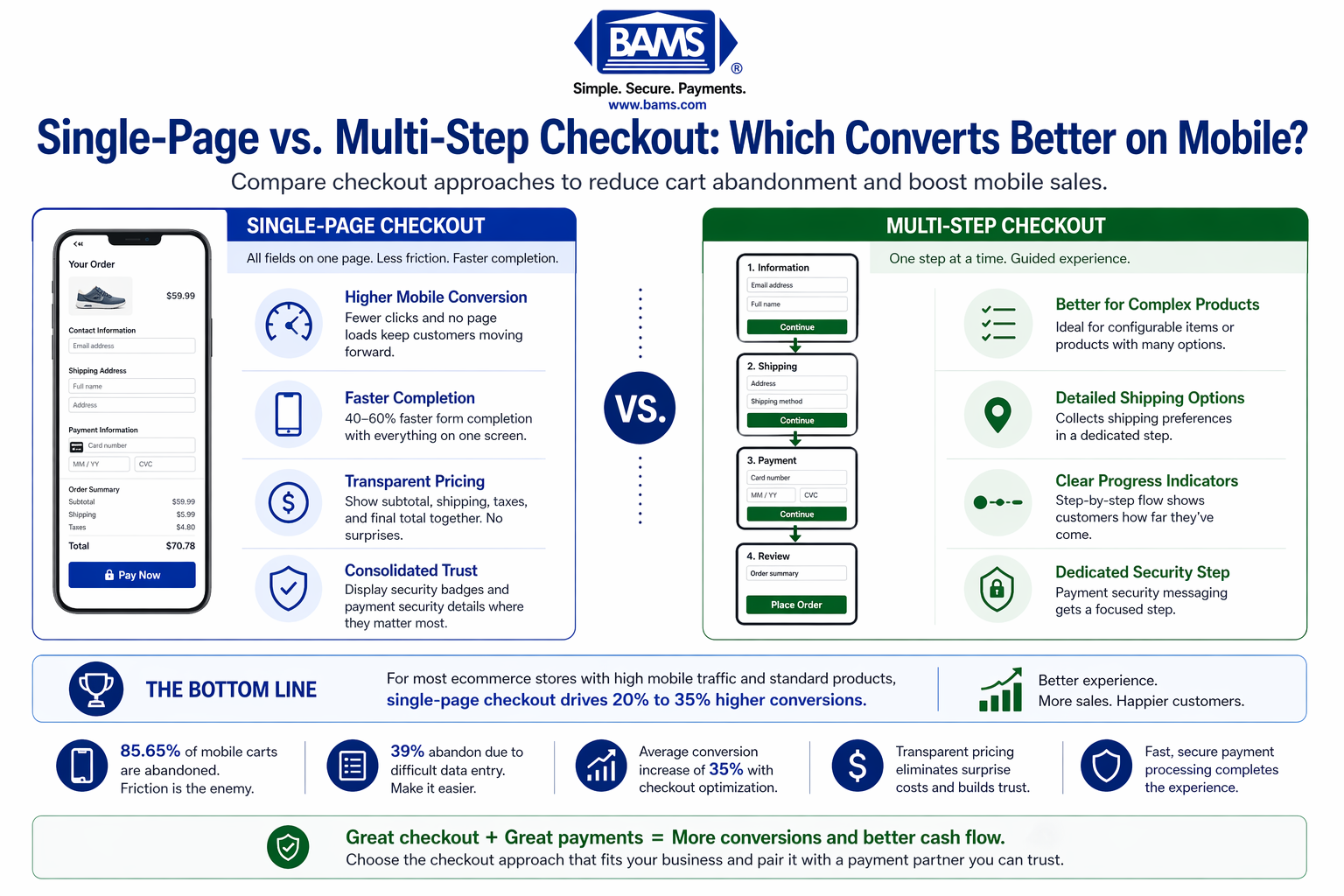

Compare checkout approaches to reduce cart abandonment and boost mobile sales for your eCommerce store Learn which checkout style converts better on mobile devices. This comparison breaks down conversion rates, implementation complexity, and security considerations to help you choose the right approach for your business. TL;DR Single-page checkout wins for mobile – Reduces friction, eliminates […]

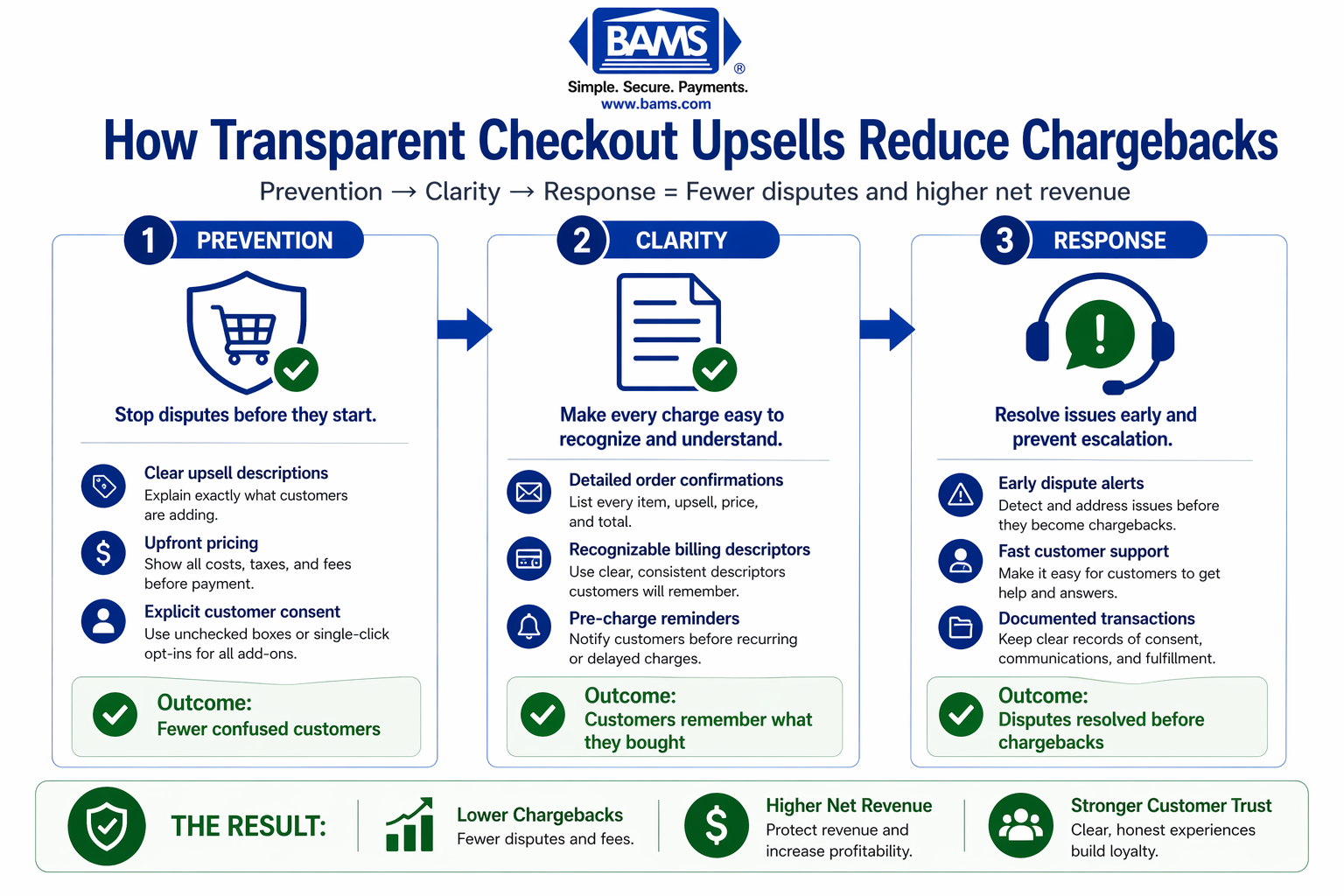

How Transparent Checkout Upsells Reduce Chargebacks A practical guide to implementing order bumps that boost revenue without triggering disputes Learn how to structure checkout upsells that customers trust and rarely dispute. This guide covers pricing transparency tactics that protect revenue while adding incremental sales through order bumps. TL;DR Chargebacks are surging – Global disputes projected […]

Payment gateways are a crucial tool in both ecommerce and brick-and-mortar sales, but many merchants don’t necessarily understand what their gateways do or why they really need to have one at all. With that in mind, the following is a quick refresher on what gateways are, how they work, and why they’re so important. […]

Payment gateways are software tools that enable transaction processing by acting as the bridge between the end customer and a merchant’s payment processor. Every transaction – both online and off – goes through some type of payment gateway. In ecommerce, payment gateways provide everything from payment data encryption to two-way communication to fraud protection and […]

As a small business owner, you should always be on the lookout for ways to improve your customer offerings to drive customer loyalty and satisfaction. There are a few things that have historically benefited small businesses such as loyalty programs, customer reviews, and community engagement. The bottom line is that without satisfied customers, your business […]

Mobile merchant services enable businesses to easily accept payments from a mobile device at any time, from anywhere. These services are essential for increasing reach for small businesses and growing customer satisfaction for larger businesses. There are many industries that can greatly benefit from having mobile merchant services, some of which may surprise you. Here […]

One thing that any business should be aware of when processing digital payments are chargebacks and chargeback prevention. Chargebacks can have a huge impact on business owners, especially for small businesses. The last thing that a business owner wants is to have to refund a customer for services rendered or products shipped, especially when there […]

With the retail world rapidly moving online, many companies are turning to online sales and e-commerce to keep pace with our evolving market. However, if retailers want to join the vast world of online sales, there are rules and procedures they have to follow, both to protect themselves from fines and their customers’ private information. […]

Making it today as a small business can be challenging. Between having to compete with big corporations and the ever-growing online market, it’s never been harder for brick and mortar stores. However, several tools, techniques, and technologies can help you integrate into the modern online market.