Interchange Fees Explained for Merchants

Interchange Fees Explained: A Guide for Ecommerce Managers

Key Takeaways

- Interchange fees are generally set within the card ecosystem, but processor markup and account-level fees can often be negotiated.

- eCommerce merchants usually pay more than card-present businesses because online transactions involve greater fraud and data risk.

- Interchange-plus pricing gives merchants better visibility into real costs than bundled or tiered pricing.

- Better transaction data can reduce downgrades and improve the effective rate you pay over time.

- A strong merchant services relationship should help you optimize cost, transparency, and chargeback performance.

Why Interchange Fees Matter for eCommerce

For eCommerce businesses, payment costs affect margin on every order. Unlike many other operating expenses, card fees scale directly with transaction volume. As revenue grows, payment costs rise with it. That makes fee structure especially important for online merchants trying to manage profitability, customer acquisition costs, and cash flow at the same time.

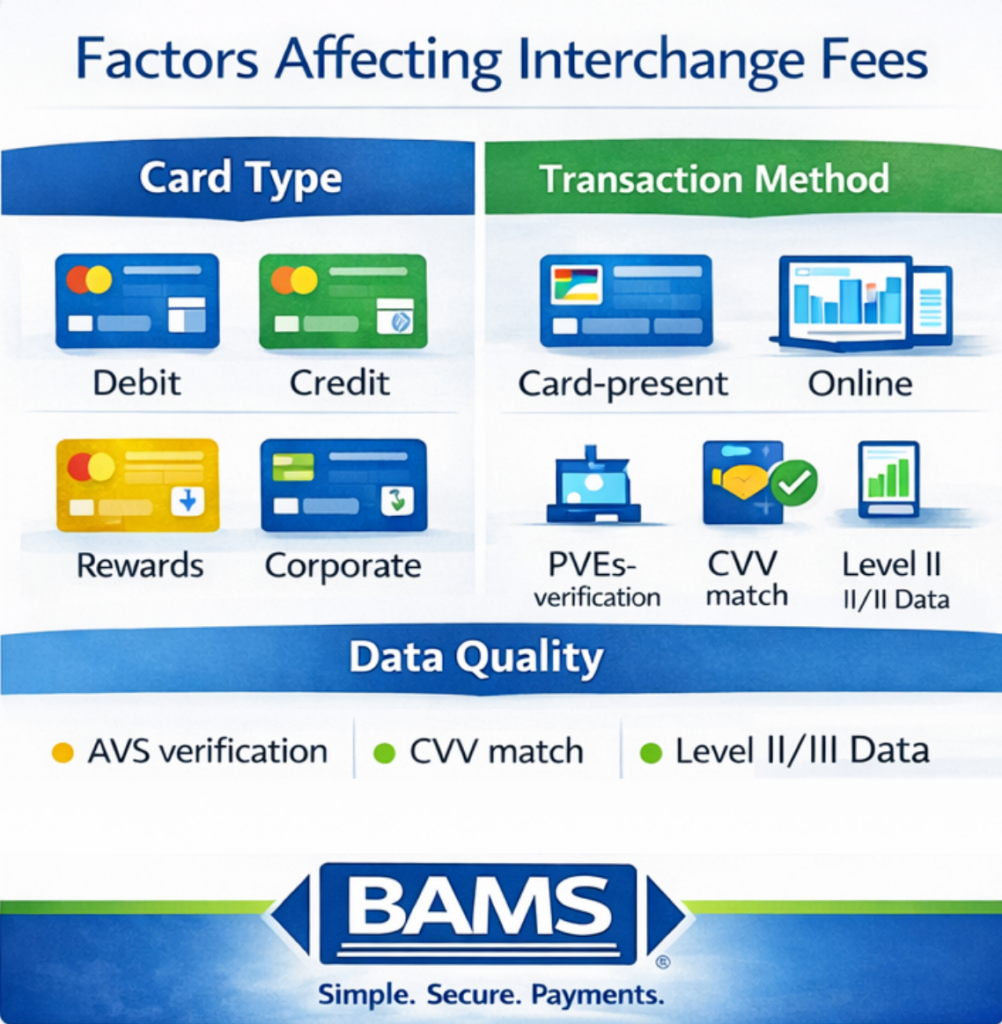

In addition, the fee environment can be difficult to interpret. Merchant Payments Coalition notes that swipe fees vary based on card type, transaction type, and merchant size, with hundreds of combinations possible. As a result, many merchants do not know the full cost of a particular transaction at the time of purchase. That complexity often leads businesses to focus only on the total percentage they see on a statement rather than the cost drivers underneath it.

ECommerce merchants also face a structural challenge: online transactions are card-not-present, which generally means more fraud exposure, higher verification requirements, and stricter qualification standards. Consequently, an eCommerce business that ignores interchange mechanics may overpay without realizing that some of the problem comes from preventable transaction quality issues rather than unavoidable card costs alone.

Understanding Interchange Fees

What Interchange Fees Actually Are

Visa explains that interchange reimbursement fees are transfer fees between acquiring banks and issuing banks for each card transaction. Merchants do not directly pay interchange to Visa itself. Instead, merchants negotiate and pay a merchant discount to their financial institution or processor, and interchange is one component within that broader total cost.

In simple terms, interchange is the largest foundational cost in many card transactions. It helps support issuing banks that provide cards, extend credit, and manage fraud risk. Because interchange is built into the card ecosystem, the merchant’s real opportunity is usually not to eliminate it, but to make sure transactions qualify as efficiently as possible.

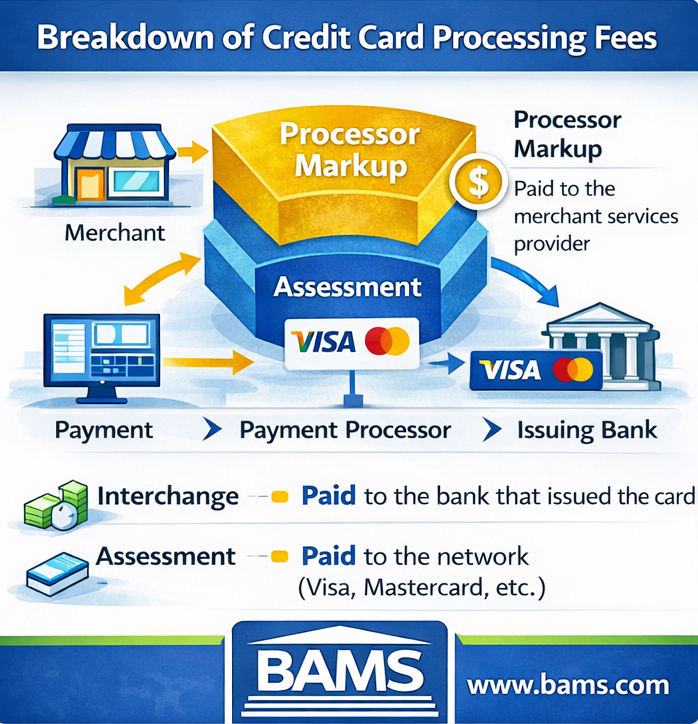

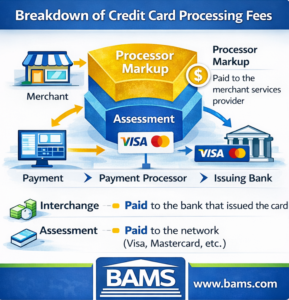

The Three Layers of Card Processing Cost

Most card transactions include three broad cost layers:

- Interchange fees, which are associated with the issuing side of the transaction

- Assessment or network fees, which relate to the card network

- Processor markup, which is charged by the payment processor or merchant services provider

This distinction matters because not every part of the fee stack behaves the same way. Interchange and many network fees are structural. Processor markup, gateway fees, statement fees, PCI-related fees, and some chargeback-related costs are often where pricing flexibility exists.

Every credit card transaction includes interchange fees, network assessments, and processor markup.

Why eCommerce Transactions Often Cost More

eCommerce transactions are not handled the same way as in-person card-present payments. Online merchants usually need stronger verification controls because the card is not physically presented at checkout. Therefore, transaction risk tends to be higher, and qualification standards become more important. Card type, transaction method, merchant category, and the completeness of submitted data can all influence the final result.

The Federal Reserve describes the payment system as the infrastructure that facilitates financial transactions between consumers, businesses, and institutions. In practice, eCommerce merchants operate inside that broader system while also carrying the added burden of remote acceptance risk. That is why data quality and processor configuration matter so much for online businesses.

Negotiable vs. Non-Negotiable Processing Fees

One of the biggest mistakes merchants make is assuming all card fees are equally negotiable. They are not. A better approach is to separate the costs you can influence from the costs you mostly cannot.

What Is Usually Not Negotiable

- Core interchange structures

- Many card network assessments

- Some network-imposed pass-through charges

What Is Often Negotiable

- Processor markup

- Gateway or platform fees

- Monthly account fees

- PCI-related administrative fees

- Statement fees

- Some chargeback administration fees

This is why transparency matters so much. Merchants should understand how merchant account pricing works before accepting a quote at face value. A transparent pricing structure makes it easier to see what portion of your total rate reflects ecosystem costs and what portion reflects your processor relationship.

How Merchants Can Reduce Interchange-Related Costs

1. Audit Your Current Statements

Start by reviewing at least three months of detailed processing statements. You should be able to identify total volume, total fees, effective rate, monthly account charges, and chargeback-related costs. If your statement does not clearly separate pricing components, ask for more detailed reporting.

Many merchants look only at the blended percentage and assume that is enough. However, a clear line-item review often reveals recurring charges or pricing structures that deserve closer attention.

2. Move Toward Better Pricing Transparency

Interchange-plus pricing is often preferred by established merchants because it separates interchange and network charges from processor markup. That does not automatically make it the lowest-cost option in every scenario, but it usually makes cost analysis easier and negotiations more grounded in real numbers.

By contrast, bundled or tiered pricing can hide the true cost of downgrades, markups, and category shifts. Therefore, merchants who want to manage cost proactively usually benefit from a clearer pricing structure.

3. Improve Transaction Data Quality

Better transaction data can help reduce unnecessary downgrades and qualification problems. eCommerce merchants should review whether their checkout and payment setup consistently support:

- complete billing information

- address verification checks

- CVV verification

- prompt settlement and batching practices

- enhanced business transaction data where relevant

Small improvements here can create compounding savings over time, especially for businesses processing higher monthly volume.

4. Reduce Downgrades and Avoidable Friction

A downgrade happens when a transaction does not qualify for a better available category and instead clears at a more expensive level. This can happen because of missing data, delayed settlement, or inconsistent processor configuration. Merchants often focus on headline pricing while overlooking downgrade performance, even though it can have a real effect on the effective rate.

Therefore, one of the smartest questions to ask your provider is not just, “What rate am I paying?” but also, “Why are certain transactions qualifying the way they are?”

5. Negotiate Processor Markup and Administrative Fees

Once you understand your statement and pricing model, negotiate the charges that your provider controls. Focus on markup, monthly fees, PCI-related charges, statement fees, and chargeback administration costs. Additionally, ask for any rate changes or fee reductions in writing so that future statements can be checked against the agreement.

Competitive quotes can help support this conversation, but the goal is not always to switch providers immediately. In many cases, a good merchant services provider can improve pricing and operational support without requiring a disruptive migration.

6. Treat Chargeback Performance as a Cost Issue

Chargebacks do more than create administrative work. They can add direct fees, increase operational burden, and weaken account performance over time. Clear billing descriptors, faster support response, accurate fulfillment documentation, and a more proactive dispute process can all help reduce unnecessary losses.

For eCommerce merchants, chargeback management is closely connected to payment cost management. Lower dispute volume often supports a healthier processing relationship overall.

7. Review Your Processor Relationship Regularly

Payment optimization should not be treated as a one-time event. Transaction mix changes, products evolve, fraud patterns shift, and fee structures can become less favorable over time. Quarterly review is often enough to catch issues before they become expensive habits.

The best processor relationships are consultative, not passive. Merchants should expect clarity, guidance, and practical recommendations rather than generic support alone.

Common Mistakes eCommerce Merchants Make

- Looking only at the headline rate: Blended pricing can hide where costs actually come from.

- Ignoring per-transaction economics: Flat fees matter more when ticket size is smaller.

- Assuming interchange can be negotiated away: The smarter move is to optimize qualification and negotiate markup.

- Overlooking transaction data quality: Missing verification data can quietly make processing more expensive.

- Accepting weak reporting: Poor visibility makes it difficult to manage cost with confidence.

- Reviewing statements too infrequently: Ongoing monitoring helps prevent fee creep.

Conclusion

Interchange fees are a core part of the card acceptance ecosystem, and eCommerce merchants cannot ignore them simply because they are not directly negotiable. The better path is to understand where interchange fits inside the total processing stack, improve transaction quality, and focus negotiation energy on the parts of pricing that your provider controls.

Over time, this approach can improve visibility, reduce unnecessary costs, and create a more strategic payments operation. For eCommerce managers, that means interchange fees should not be viewed as a mystery line item. They should be treated as part of a measurable system that can be managed more intelligently.

Frequently Asked Questions

What are interchange fees?

Interchange fees are transaction-related fees built into card processing and associated with the issuing side of the payment flow. They are a major component of the total cost merchants pay to accept cards.

Why do eCommerce merchants usually pay more than in-store merchants?

eCommerce transactions are card-not-present, which generally means greater fraud risk and tighter qualification requirements. That often leads to higher overall processing costs than traditional card-present acceptance.

Can merchants negotiate interchange fees?

Usually, no. However, merchants can often negotiate processor markup and account-level fees, and they can improve transaction quality so that payments qualify more efficiently.

What is interchange-plus pricing?

Interchange-plus pricing separates interchange and network fees from processor markup. Many merchants prefer it because it improves transparency and makes statement analysis easier.

How can businesses lower interchange-related costs?

Merchants can lower overall cost by improving transaction data, reducing downgrades, negotiating processor-controlled fees, and reviewing statements regularly for pricing drift or avoidable charges.

Sources