How to Lower Credit Card Processing Fees by 15-30% in One Billing Cycle

A step-by-step action plan to negotiate better rates, choose the right pricing model, and stop overpaying your payment processor

Learn exactly which transaction fees to target and how to negotiate with your payment processor for lower rates to lower credit card processing fees. This 2-4 hour tutorial gives you a complete system to reduce credit card costs and monitor savings monthly.

TL;DR

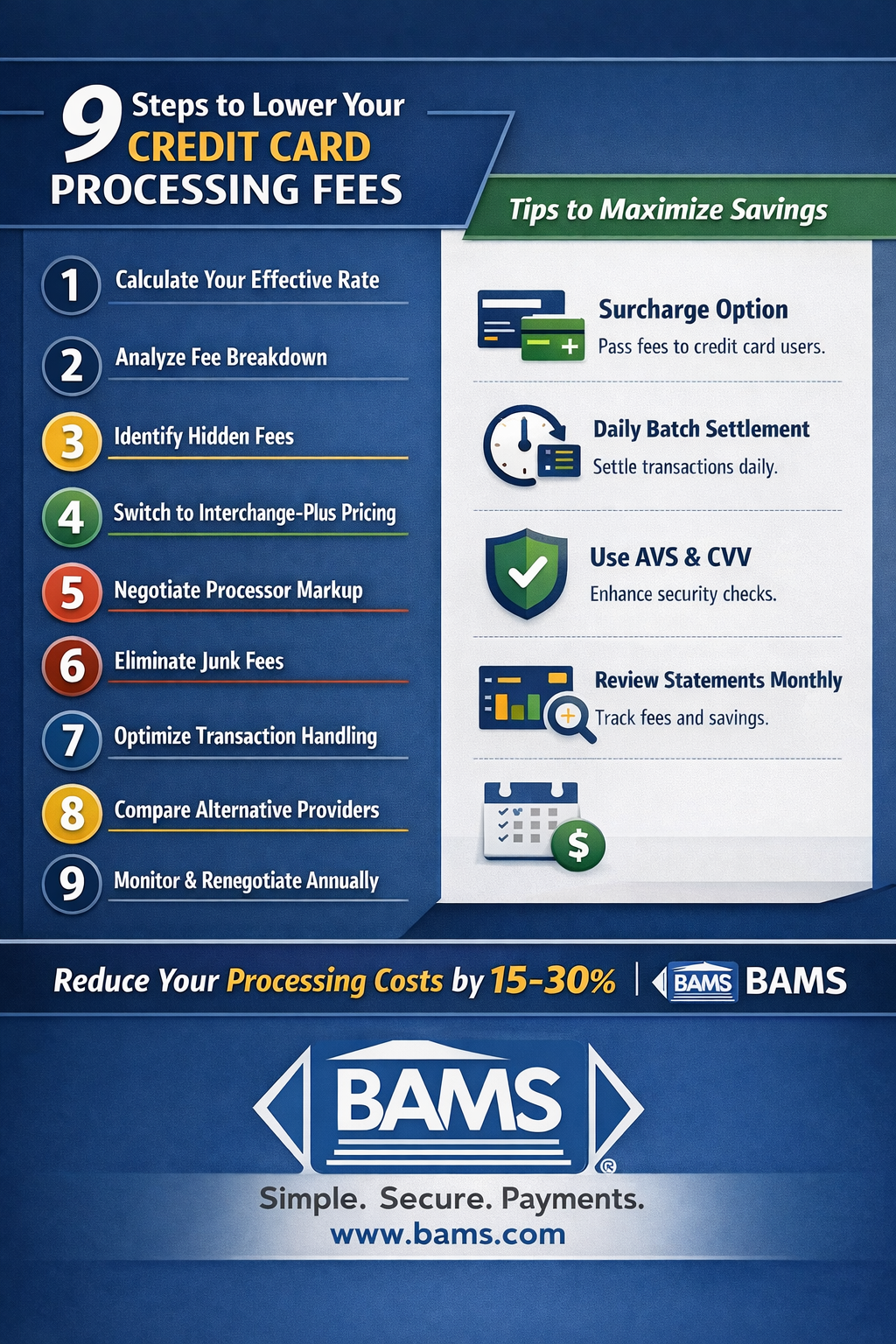

- Calculate your effective rate first – Divide total fees by total sales volume. If you are above 3%, you are likely overpaying and have room to negotiate.

- Focus on processor markup, not interchange – Interchange fees are non-negotiable, but your processor’s margin (often 20-40% of total fees) is where you have leverage.

- Switch to interchange-plus pricing – Tiered and flat-rate models hide true costs. Transparent pricing lets you see exactly what you pay and makes negotiation easier.

- Eliminate junk fees – PCI non-compliance fees, statement fees, and monthly minimums add up. Many can be removed or reduced with a phone call.

- Monitor monthly and renegotiate annually – Card networks raise rates twice yearly. A $1 million business at 2.5% loses $25,000 annually to fees. Reducing that to 2.2% saves $3,000 per year

What You Will Achieve

By the end of this tutorial, you will have a clear action plan to reduce your credit card transaction costs by 15-30%. You will know exactly which fees to target, how to negotiate with your payment processor, and which pricing model fits your business best.

Your success criteria: a lower effective rate on your next statement, documented savings projections, and a system to monitor fees monthly. Most ecommerce managers complete these steps in 2-4 hours and see results within one billing cycle.

Prerequisites and Setup

Before you start, gather these items:

- Your last 3 months of processing statements (PDF or online access)

- Your current processor contract and any rate agreements

- A spreadsheet to track your findings

- Calculator or access to a payment processing fee calculator

- 30-60 minutes of uninterrupted time per step

Potential blockers: Some processors bury fee details in confusing statements. If you cannot locate specific line items, contact your processor’s support team and request an itemized breakdown before proceeding.

Why This Approach Works

Merchants paid a record $172 billion in processing fees in 2023, with most of that going to interchange and assessment fees. The problem is not that transaction fees exist. The problem is that most businesses accept whatever rate they are given without question.

This tutorial focuses on systematic fee reduction rather than switching processors immediately. You may find your current provider offers better terms once you understand the numbers. Alternatively, you may discover a better fit elsewhere. Either way, you will make decisions based on data, not guesswork.

Step 1: Calculate Your True Effective Rate

Visual breakdown of credit card processing fees showing how businesses can calculate their effective rate, identify processor markup, and reduce costs with interchange-plus pricing.

Action: Open your most recent processing statement and locate two numbers: total fees charged and total sales volume processed.

Divide total fees by total sales volume, then multiply by 100. This gives you your effective rate as a percentage. For example: $2,500 in fees ÷ $100,000 in sales = 2.5% effective rate.

Expected result: A single percentage between 1.5% and 3.5%.

Checkpoint: If your effective rate exceeds 3%, you are likely overpaying and have significant room for improvement.

Common failure: Statement shows multiple merchant IDs or locations. Fix: Calculate effective rate for each separately, then combine for a weighted average.

Step 2: Break Down Your Fee Categories

Action: Identify and categorize every fee on your statement into three buckets: interchange fees, assessment fees, and processor markup.

Interchange fees go to the card-issuing bank. These are non-negotiable and vary by card type. Average rates range from 1.30% to 3.25% depending on the network (Visa, Mastercard, American Express, Discover).

Assessment fees go to the card networks themselves. Also non-negotiable, but typically small (0.13% to 0.15%). Interchange fees are set by card networks and paid to issuing banks, while assessment fees are paid directly to the card networks that maintain payment infrastructure.

Processor markup is where you have leverage. This includes the margin your processor adds on top of interchange, plus any monthly fees, PCI compliance fees, batch fees, and statement fees.

Expected result: A clear picture of where your money goes. Most ecommerce businesses find 20-40% of their total fees come from processor markup.

Common failure: Cannot find interchange breakdown. Fix: Request an interchange-plus statement from your processor. If they refuse, this is a red flag about pricing transparency.

Step 3: Identify Hidden and Junk Fees

Action: Scan your statement for fees that do not directly relate to processing transactions. Circle or highlight each one.

Watch for these common culprits:

- Monthly minimum fees (charged when you do not process enough volume)

- PCI non-compliance fees (often $19-$99/month if you have not completed your annual questionnaire)

- Statement fees ($5-$15/month for paper statements you may not need)

- Gateway fees (sometimes charged twice if you use a third-party gateway)

- Batch fees ($0.10-$0.30 per daily settlement)

- Annual fees or “account maintenance” fees

Expected result: A list of 3-8 fees that may be reducible or eliminable.

Common failure: Fee names are vague or abbreviated. Fix: Call your processor and ask them to explain each line item. Document their answers.

Step 4: Understand Your Pricing Model

Action: Determine which pricing structure your processor uses. This affects how much room you have to negotiate.

Interchange-plus pricing shows you the actual interchange rate plus a fixed markup (e.g., interchange + 0.25% + $0.10). This is the most transparent model and easiest to optimize.

Tiered pricing groups transactions into “qualified,” “mid-qualified,” and “non-qualified” buckets with different rates. This model often hides true costs and benefits the processor.

Flat-rate pricing charges the same percentage regardless of card type.

Expected result: You know your pricing model and can compare it to alternatives.

Checkpoint: If you process over $10,000/month and use flat-rate pricing, interchange-plus will almost certainly save you money.

Step 5: Audit Your Transaction Types

Action: Review which card types and transaction methods drive your fees. Your statement should show a breakdown by card brand and transaction type.

Key factors that increase interchange rates:

- Card-not-present transactions (ecommerce) cost more than card-present (retail)

- Rewards cards and corporate cards carry higher interchange than basic debit

- American Express typically costs 1.80%-3.25% compared to Visa’s 1.30%-2.60%

- Keyed-in transactions cost more than chip or tap payments

Expected result: You identify which transaction types cost you the most and can prioritize optimization efforts.

Common failure: Statement does not break down by card type. Fix: Request a detailed interchange qualification report from your processor.

Step 6: Negotiate With Your Current Processor

Action: Contact your processor’s retention or account management team. Come prepared with your effective rate calculation, competitor quotes, and specific asks.

Use this script as a starting point:

“I have been reviewing my processing costs and found my effective rate is [X%]. I have received quotes from other providers at [Y%]. Before I consider switching, I wanted to see if you can match or improve my current terms.”

Specific items to negotiate:

- Reduce the markup percentage on interchange-plus pricing

- Eliminate or reduce monthly fees, PCI fees, and statement fees

- Lower the per-transaction fee

- Remove early termination fees from your contract

Expected result: A written offer with improved terms, or confirmation that your current rates are competitive.

Common failure: Representative claims rates are “set by the card networks.” Fix: Clarify you are asking about their markup, not interchange. Interchange is non-negotiable; their margin is not.

Step 7: Optimize Your Transaction Handling

Action: Implement operational changes that qualify your transactions for lower interchange rates.

For ecommerce businesses:

- Use Address Verification Service (AVS) on every transaction to qualify for lower rates

- Include CVV verification to reduce fraud risk and qualify for better interchange

- Settle batches daily rather than letting them accumulate

- Send Level 2 and Level 3 data for B2B transactions (includes tax amount, customer code, and line-item details)

- Avoid manual keyed entries when possible

Expected result: More transactions qualify for lower interchange tiers, reducing your effective rate by 0.1%-0.5%.

Checkpoint: After implementing changes, compare your next statement to your baseline. You should see fewer “downgraded” transactions.

Step 8: Evaluate Alternative Processors

Action: Request quotes from 2-3 alternative processors. Provide them with your monthly volume, average transaction size, and card type mix for accurate comparisons.

Questions to ask each provider:

- What is your interchange-plus markup?

- What monthly fees apply?

- Do you charge PCI compliance fees?

- What is your contract length and early termination policy?

- How quickly do funds deposit (next-day funding vs. 2-3 days)?

- What chargeback protection do you offer?

A merchant services partner like BAMS offers next-day funding and transparent pricing, which directly addresses the cash flow concerns that high fees create. Faster access to your money compounds the benefit of lower fees.

Expected result: Detailed quotes you can compare apples-to-apples with your current costs.

Step 9: Consider Passing Fees to Customers

Action: Evaluate whether surcharging or cash discounting makes sense for your business.

Surcharging adds a fee (typically 2-4%) to credit card transactions. This is legal in most U.S. states but requires proper disclosure and cannot apply to debit cards.

Cash discounting offers a lower price for cash or debit payments. This achieves similar results with different framing.

Consider these factors:

- Your competitive landscape (do competitors surcharge?)

- Customer price sensitivity

- Average transaction size (surcharges hurt more on small purchases)

- State regulations (surcharging is prohibited in Connecticut, Massachusetts, and Puerto Rico)

Expected result: A decision on whether to implement surcharging, with a compliance plan if you proceed.

Common failure: Implementing surcharges incorrectly and violating card network rules. Fix: Consult your processor about proper disclosure requirements before launching.

Step 10: Set Up Ongoing Monitoring

Action: Create a monthly review process to catch fee increases and ensure your optimization efforts stick.

Build a simple tracking spreadsheet with these columns:

- Month

- Total sales volume

- Total fees

- Effective rate

- Notes on any anomalies

Set a calendar reminder to update this within 5 days of receiving each statement. Flag any month where your effective rate increases by more than 0.1%.

Expected result: A dashboard that shows your fee trends over time and alerts you to problems early.

Step-by-step guide outlining how businesses can reduce credit card processing costs by auditing fees, negotiating processor markup, switching pricing models, and monitoring statements.

Checkpoint: After 3 months of tracking, you should have a clear baseline and be able to quantify your savings from this tutorial.

Configuration and Customization

Your optimization strategy depends on your business profile. Adjust these variables based on your situation:

Monthly volume under $10,000: Flat-rate processors may actually be cost-effective. Focus on eliminating monthly fees rather than negotiating interchange markup.

Monthly volume $10,000-$100,000: Interchange-plus pricing becomes valuable. Negotiate markup aggressively and implement transaction optimization.

Monthly volume over $100,000: You have significant leverage. Expect interchange-plus markups under 0.20% + $0.10. Consider dedicated account management.

High average ticket ($200+): Per-transaction fees matter less than percentage rates. Prioritize lower percentage markups.

Low average ticket (under $20): Per-transaction fees add up quickly. Look for processors with lower flat fees per transaction.

Verification and Testing

To confirm your optimization worked, compare your effective rate before and after implementation.

Test procedure:

- Calculate your baseline effective rate from the 3 months before changes

- Wait for 2 full billing cycles after implementing changes

- Calculate your new effective rate

- Multiply the difference by your annual volume to see dollar savings

Success definition: Your effective rate drops by at least 0.2%, or you eliminate at least $50/month in junk fees.

A business processing $1 million annually that reduces their effective rate from 2.5% to 2.2% saves $3,000 per year. That is real money back in your operating budget.

Common Errors and Fixes

Error: “Your rates are already the lowest possible.”

Cause: You are speaking with a sales rep, not a retention specialist. Fix: Ask to speak with the retention or loyalty department. Mention you are considering switching providers.

Error: Effective rate increased after “negotiating” lower rates.

Cause: Processor lowered one fee but raised others. Fix: Always get changes in writing and compare total fees, not individual line items.

Error: Cannot find interchange breakdown on statement.

Cause: You are on tiered pricing, which obscures true costs. Fix: Request a switch to interchange-plus pricing or request a detailed interchange report.

Error: Processor claims they cannot provide interchange-plus pricing.

Cause: Some processors only offer tiered or flat-rate models. Fix: This is a sign to switch providers. Transparent pricing should be standard.

Error: Savings disappeared after a few months.

Cause: Card networks raised interchange rates (Visa and Mastercard adjust rates twice yearly). Fix: Review statements monthly and renegotiate annually. Major networks raised several fees in 2024-2025, including Visa’s Misuse of Authorization Fee (from $0.09 to $0.15).

Next Steps and Extensions

Once you have optimized your processing fees, consider these follow-up actions:

Implement chargeback prevention: Chargebacks cost $20-$100 each in fees, plus the lost sale. Proactive chargeback defense, like what low cost merchant account offers, protects your revenue and keeps your merchant account in good standing.

Accelerate your cash flow: If you are waiting 2-3 days for deposits, next-day funding puts that money to work faster. Calculate the value of having funds available sooner.

Automate reconciliation: Connect your processor to your accounting software to reduce manual work and catch discrepancies automatically.

Review your processing costs quarterly. As your business grows and your transaction mix changes, new optimization opportunities will emerge.

Frequently Asked Questions

What are credit card processing fees?

`are the costs merchants pay to accept card payments. These fees typically range from 1.5% to 3.5% per transaction and include three components: interchange fees paid to the card-issuing bank, assessment fees paid to the card network (Visa, Mastercard, etc.), and markup fees charged by your payment processor.

<h3>Why do merchants have to pay processing fees for credit card transactions?

Processing fees cover the infrastructure, fraud protection, and risk management that enable electronic payments. The card-issuing bank takes on the risk of non-payment and fraud, the card network maintains the payment rails, and your processor handles the technical connection between your business and the financial system. Each party takes a cut for their role.

How are credit card processing fees determined?

Interchange fees are set by card networks based on factors like card type (rewards vs. basic), transaction method (in-person vs. online), merchant category, and transaction size. Your processor’s markup is negotiable and depends on your volume, industry, and negotiating leverage. Assessment fees are fixed percentages set by each card network.

Which types of transactions incur higher processing fees?

Card-not-present transactions (ecommerce, phone orders) cost more than in-person transactions because they carry higher fraud risk. Rewards cards and corporate cards have higher interchange than basic debit cards. American Express typically charges the highest rates (1.80%-3.25%), while Discover tends to be lowest among major networks (1.55%-2.45%).

How can businesses minimize their credit card processing fees?

Start by calculating your effective rate and understanding your fee breakdown. Negotiate your processor’s markup, eliminate junk fees, switch to interchange-plus pricing if you are on tiered pricing, and optimize your transaction handling (use AVS, include CVV, settle daily). For high-volume businesses, even small percentage reductions translate to thousands in annual savings.

When do interchange fees change, and what factors influence them?

Visa and Mastercard typically adjust interchange rates twice per year, in April and October. Changes reflect shifts in fraud rates, competitive dynamics between networks, regulatory pressure, and economic conditions. Recent years have seen increases in several fee categories, making ongoing monitoring essential for merchants.

Sources

- Merchant Payments Coalition: https://merchantspaymentscoalition.com/visa-mastercard-credit-card-swipe-fees-hit-record-100-billion-first-time-2023-underscoring-need

- Federal Reserve – Payment Systems: https://www.federalreserve.gov/paymentsystems.htm

- Visa – Interchange Fee Overview: https://usa.visa.com/support/small-business/regulations-fees.html

- CNBC – https://www.cnbc.com/2025/11/10/visa-mastercard-reach-revised-swipe-fee-settlement-with-merchants-.html