How to Reduce Credit Card Processing Fees for eCommerce

Unlock strategies to lower merchant discount rates and boost profits in your online store.

Learn to audit and negotiate credit card processing fees to retain more profits. This guide helps e-commerce managers reduce fees by 15-30%, enhancing cash flow.

TL;DR

- Know your effective rate – Divide total fees by total volume to get your true processing cost. E-commerce businesses should target below 3% if possible.

- Processor markup is negotiable – Interchange and assessment fees are fixed, but your processor’s cut is not. Annual renegotiation with competitive quotes typically saves 0.1% to 0.5%.

- Transaction optimization reduces interchange – Capture complete card data, settle batches daily, and match authorization amounts to qualify for lower interchange categories.

- Chargebacks cost more than the dispute – Each chargeback triggers fees, consumes staff time, and risks rate increases. Prevention delivers better ROI than winning disputes.

- Monitor monthly, renegotiate annually – Processors add fees quietly and rarely volunteer rate reductions. Active management keeps costs competitive over time.

What This Guide Covers

This guide breaks down credit card processing fees into clear, actionable components so you can identify where your money goes and how to keep more of it. You’ll learn the exact structure of the merchant discount rate, which fees you can negotiate, and which you cannot.

By the end, you’ll understand how to audit your current processing costs, negotiate better rates with providers, and implement operational changes that reduce fees by 15-30%. This guide is built for e-commerce managers processing $10,000 or more monthly who want to stop accepting inflated fees as a cost of doing business.

Understanding your ecommerce processing structure begins with identifying the core drivers of your credit card processing fees.

We focus on strategic fee reduction, not switching processors (though that may be one outcome). We exclude point-of-sale hardware considerations and industry-specific compliance requirements.

Why Processing Fees Deserve Your Attention Now

Credit card processing fees are climbing while your margins face pressure from every direction. U.S. merchants paid $148.52 billion in credit card processing fees in 2024, a 9.3% increase from 2023. That growth rate outpaces most businesses’ revenue increases.

For e-commerce specifically, the math is brutal. Online transactions incur fees between 1.8% and 3.5%, compared to 1.3% to 2.7% for in-person retail. Your business model carries a built-in fee premium that compounds with every sale.

Consider the real numbers: processing $100,000 monthly at average rates means paying $1,500 to $3,500 in fees. That’s $18,000 to $42,000 annually, often your second-highest operating cost after labor. Yet most e-commerce managers review these costs once a year, if at all.

The cost of inaction compounds. Card networks adjust interchange rates twice yearly, and processors quietly layer on additional fees. Without active management, your effective rate creeps upward by 0.1% to 0.3% annually. On $100,000 monthly volume, that’s an extra $1,200 to $3,600 per year in fees you never agreed to.

Core Concepts: Understanding What You’re Actually Paying

The Three-Part Fee Structure

Every credit card transaction involves three distinct costs bundled into your merchant discount rate. Understanding each component reveals where you have leverage and where you do not.

Interchange fees go directly to the card-issuing bank. These are non-negotiable and set by Visa and Mastercard. They averaged 2.24% in 2023 and range from 1.8% to over 3% depending on card type, transaction method, and merchant category.

Assessment fees go to the card networks (Visa, Mastercard, Discover, American Express). These are also non-negotiable and typically add 0.13% to 0.15% per transaction.

Processor markup is what your payment processor charges for their services. This is entirely negotiable and where most savings opportunities exist.

Why E-Commerce Pays More

Card-not-present transactions carry higher fraud risk, so card networks charge higher interchange rates. Your customer cannot physically present their card, which means the issuing bank assumes more liability. You pay for that risk transfer through elevated fees.

Additionally, e-commerce merchant accounts attract more rewards cards. Customers shopping online tend to use premium cards with cashback or travel points. Those rewards are funded partly through higher interchange fees charged to you.

The Pricing Model Matters

Processors use three main pricing structures: flat-rate, tiered, and interchange-plus. Flat-rate pricing (like 2.9% + $0.30) is simple but expensive at scale. Tiered pricing bundles transactions into qualified, mid-qualified, and non-qualified categories, often obscuring true costs. Interchange-plus pricing passes through actual interchange rates plus a fixed markup, offering the most transparency and typically the lowest effective rates for established businesses.

Learn how an optimized ecommerce merchant account structure improves cost transparency here: https://www.bams.com/industries/e-commerce-merchant-account/

The Strategic Framework for Fee Reduction

Reducing processing fees requires action across three interconnected areas: visibility, negotiation, and optimization. Skip any one area, and you leave money on the table.

Visibility means understanding exactly what you pay, broken down by fee component, card type, and transaction category. Without this baseline, you cannot measure improvement or identify the highest-impact opportunities.

Negotiation targets the processor markup, the only truly flexible component of your fees. This requires leverage (transaction volume, competitive quotes) and knowledge (understanding what rates are actually achievable).

Optimization involves operational changes that qualify your transactions for lower interchange categories. This includes how you capture card data, when you settle batches, and how you handle chargebacks.

These three areas create a continuous improvement cycle. Better visibility reveals negotiation opportunities. Successful negotiation funds optimization investments. Optimization improvements generate data for the next round of visibility analysis.

Step 1: Audit Your Current Processing Costs

Objective

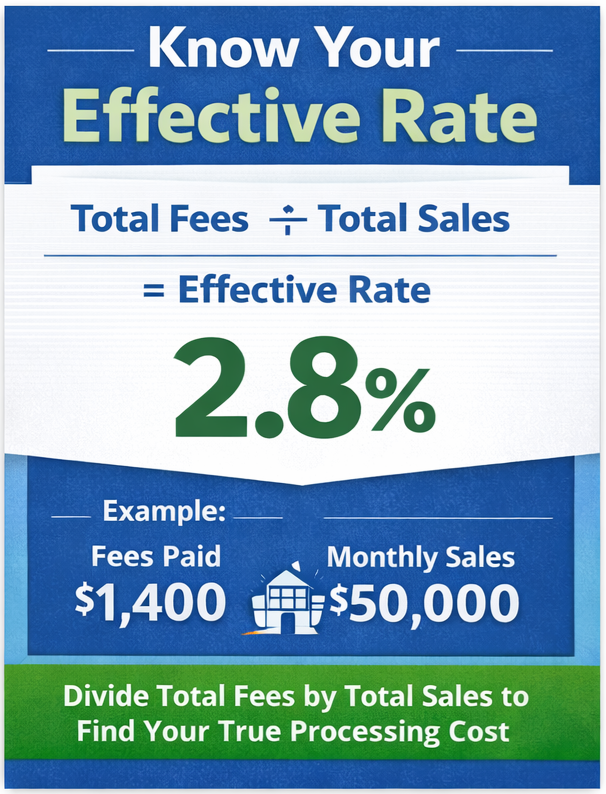

Establish your true effective rate and identify the specific fee categories consuming the most margin. Every ecommerce merchant account should start with calculating its true effective rate.

Execution

Pull your last three months of processing statements. Calculate your effective rate by dividing total fees paid by total transaction volume. For a business processing $50,000 monthly and paying $1,400 in fees, the effective rate is 2.8%.

Break down fees by category. Separate interchange, assessments, and processor markup. If your statements do not show this breakdown, your processor uses tiered or flat-rate pricing, which typically means you are overpaying.

Identify your most expensive transaction types. Rewards cards, corporate cards, and international cards all carry premium interchange rates. Knowing which card types dominate your mix reveals where optimization efforts will have the greatest impact.

What to Avoid

Do not accept summary statements that bundle all fees together. Demand itemized breakdowns. If your processor cannot provide them, that opacity is a red flag.

Do not average across months without examining seasonality. Holiday periods may show different card mixes and fee patterns than typical months.

Success Indicators

- You can state your effective rate to two decimal places.

- You know what percentage of fees go to interchange versus processor markup.

- You have identified your three most expensive card types by total fees paid.

Step 2: Benchmark Against Industry Standards

Objective

Determine whether your current rates are competitive or inflated relative to businesses with similar profiles.

Execution

Compare your effective rate against published benchmarks. Credit card processing fees typically range between 1.5% and 3.5% for small businesses in 2025. E-commerce businesses should expect rates toward the higher end of this range, but above 3% warrants investigation.

The average merchant discount rate falls between 2.87% and 4.35% per transaction when including all fee components. If you are above 3.5% with clean transaction history and reasonable volume, you have significant negotiation room.

Request quotes from two or three competing processors. Even if you do not intend to switch, these quotes establish market rates and provide leverage for renegotiation with your current provider.

What to Avoid

Do not compare your blended rate against interchange-only benchmarks. Interchange represents only part of your total cost. Compare apples to apples: total fees divided by total volume.

Do not assume the lowest quote is the best deal. Hidden fees, poor customer support, and funding delays can cost more than a slightly higher transparent rate.

Success Indicators

- You know where your effective rate falls relative to industry benchmarks.

- You have at least two competitive quotes with itemized fee breakdowns.

- You can identify the specific gap between your current rate and achievable market rates.

Step 3: Negotiate Processor Markup

Objective

Reduce the negotiable portion of your fees by 0.1% to 0.5% through direct negotiation with your processor.

Execution

Contact your processor’s retention department, not general customer service. Retention teams have authority to adjust pricing that frontline representatives lack.

Lead with your competitive quotes and your history as a customer. Processors value stable, predictable volume. A business processing $50,000 monthly with low chargebacks represents significant lifetime value worth protecting.

Request interchange-plus pricing if you currently use flat-rate or tiered models. For established e-commerce businesses, interchange-plus typically delivers 0.3% to 0.7% savings compared to flat-rate pricing.

Negotiate specific line items. Ask for pricing with reduced per-transaction fees, lower monthly minimums, or eliminated statement fees. Small wins across multiple fee categories compound into meaningful savings.

What to Avoid

Do not accept vague promises of “better rates.” Get specific numbers in writing before agreeing to anything.

Do not sign long-term contracts with early termination fees to secure better rates. The flexibility to switch processors is itself valuable leverage.

Success Indicators

You have a written rate reduction or pricing structure change. Your new effective rate is measurably lower than your audited baseline. You understand exactly which fees changed and by how much.

Step 4: Optimize Transaction Qualification

Objective

Ensure your transactions qualify for the lowest possible interchange categories through operational improvements.

Execution

Capture complete transaction data. Interchange rates drop when you provide AVS (Address Verification Service) data, CVV codes, and complete billing information. Missing data elements trigger downgrades to higher-cost categories.

Settle batches daily. Transactions settled more than 24 hours after authorization often qualify for higher interchange rates. Configure your payment gateway for automatic daily settlement.

Use Level 2 and Level 3 data for B2B transactions. If you sell to businesses or government entities, providing enhanced transaction data (purchase order numbers, tax amounts, item descriptions) can reduce interchange by 0.5% to 1.0% on qualifying transactions.

Match authorization and settlement amounts. Split shipments or partial fulfillments that create mismatches between authorized and settled amounts trigger interchange downgrades.

What to Avoid

Do not batch transactions weekly to reduce processing effort. The interchange penalties far exceed any administrative savings.

Do not ignore AVS failures. Transactions that fail address verification not only cost more in fees but also carry higher chargeback risk.

Success Indicators

- Your downgrade rate (transactions qualifying for higher interchange categories) decreases month over month.

- Your effective rate drops even without rate renegotiation.

- Your processor statements show fewer non-qualified transactions.

Step 5: Implement Chargeback Prevention

Objective

Reduce chargebacks that trigger fee penalties, reserve holds, and potential account termination.

Execution

Deploy fraud screening tools that flag suspicious transactions before fulfillment. Address mismatches, unusual order sizes, and velocity patterns (multiple orders from the same card in short periods) warrant manual review.

Use clear billing descriptors. Customers who do not recognize charges on their statements file chargebacks. Ensure your business name appears clearly and matches what customers expect to see.

Respond to chargeback alerts immediately. Many chargebacks can be resolved through rapid refunds before they become formal disputes. The cost of a refund is far lower than the cost of a lost chargeback plus associated fees.

Document everything. Delivery confirmation, customer communications, and signed agreements provide evidence for chargeback disputes. Winning disputes protects both immediate revenue and long-term processing rates.

What to Avoid

Do not ignore chargeback notifications hoping they will resolve themselves. Response deadlines are strict, and missed deadlines mean automatic losses.

Do not fight every chargeback regardless of merit. Some disputes are not worth the time investment. Focus resources on high-value transactions with strong evidence.

Success Indicators

Your chargeback ratio stays below 1% (the threshold where processors impose penalties). You win a higher percentage of disputed chargebacks. Your processor has not imposed reserve requirements or rate increases due to chargeback concerns.

Step 6: Evaluate Alternative Payment Methods

Objective

Reduce credit card volume by offering lower-cost payment alternatives where appropriate for your customer base.

Execution

Offer ACH or bank transfer options for high-value transactions. ACH fees typically run $0.25 to $1.00 per transaction regardless of amount, making them dramatically cheaper than credit cards for large orders.

Consider debit card incentives. Debit transactions carry lower interchange rates than credit. Some businesses offer small discounts for debit payments, though this requires careful margin analysis.

Evaluate buy-now-pay-later options. Services like Affirm or Klarna charge merchant fees, but they may convert customers who would otherwise abandon carts. The net impact depends on your specific conversion rates and average order values.

For B2B sales, offer net terms with ACH payment. Business customers often prefer invoice-based purchasing, and you avoid credit card fees entirely while potentially increasing order sizes.

What to Avoid

Do not add friction to the checkout process by pushing alternative payment methods too aggressively. Lost sales cost more than processing fees.

Do not offer cash discounts that violate card network rules or create compliance issues. Surcharging is legal in most states but requires specific disclosures.

Success Indicators

A measurable percentage of transactions shift to lower-cost payment methods. Your blended effective rate across all payment types decreases. Customer satisfaction and conversion rates remain stable or improve.

Step 7: Establish Ongoing Monitoring

Objective

Create systems that catch fee increases early and maintain negotiating leverage over time.

Execution

Calculate your effective rate monthly. A simple spreadsheet tracking total fees divided by total volume reveals trends before they become expensive problems.

Review processor statements for new fees. Processors add charges for PCI compliance, account maintenance, or “technology fees” that may not appear in your original agreement. Question any new line items immediately.

Track interchange rate changes. Visa and Mastercard adjust rates in April and October each year. Understanding these changes helps you distinguish network increases from processor markup creep.

Renegotiate annually. Even without switching processors, annual rate reviews maintain competitive pricing. Your transaction volume and history improve your negotiating position over time.

What to Avoid

Do not assume stable fees mean optimal fees. Processors rarely volunteer rate reductions even when your profile improves.

Do not wait for problems to review processing costs. Proactive monitoring catches issues when they are small and fixable.

Success Indicators

You can identify your effective rate for any month within 48 hours. You catch and question new fees within one billing cycle. Your annual rate review produces measurable improvements or confirms competitive positioning.

Common Mistakes That Inflate Processing Costs

Accepting the first rate offered. Processors expect negotiation. Initial quotes include margin for concessions. Businesses that accept without pushback pay 0.2% to 0.5% more than necessary.

Ignoring statement details. Monthly statements contain fee breakdowns that reveal optimization opportunities. Most businesses file these without review, missing both errors and trends.

Prioritizing rate over total cost. A lower percentage rate with higher per-transaction fees may cost more depending on your average order value. Calculate total expected fees, not just rates.

Treating chargebacks as inevitable. Every chargeback carries direct fees ($15 to $100), indirect costs (staff time, potential rate increases), and risk of account termination. Prevention investment pays returns.

Staying loyal without leverage. Long-term processor relationships have value, but loyalty without periodic competitive evaluation means paying more than necessary. Processors reward retention efforts, not passive acceptance.

What to Do Next

Start with Step 1. Pull your last three processing statements and calculate your effective rate. This single number tells you whether you have a significant problem or minor optimization opportunities.

If your effective rate exceeds 3% and you process more than $25,000 monthly, you likely have meaningful savings available through negotiation alone. If your rate is already competitive, focus on optimization and monitoring to maintain that position.

Treat this guide as a reference rather than a one-time checklist. Processing costs require ongoing attention because fees, rates, and your business profile all change over time. Return to relevant sections as your situation evolves.

The goal is not perfection but progress. Reducing your effective rate by 0.3% on $100,000 monthly volume saves $3,600 annually. That is real money returned to your business through attention and action rather than acceptance of the status quo.

Want a professional review of your ecommerce merchant account rates?

Request a cost analysis and see how much you could reduce your ecommerce processing fees.

Frequently Asked Questions

What are credit card processing fees?

Credit card processing fees are the costs merchants pay to accept card payments. They include three components: interchange fees paid to the card-issuing bank, assessment fees paid to card networks like Visa and Mastercard, and processor markup charged by your payment processor. Together, these fees typically range from 1.5% to 3.5% of each transaction for small businesses.

Why do merchants have to pay processing fees for credit card transactions?

Processing fees compensate the multiple parties that make card payments possible. The issuing bank assumes fraud and default risk when extending credit to cardholders. The card network maintains the payment infrastructure connecting millions of merchants and banks. Your processor handles transaction routing, settlement, and customer support. Each party takes a portion of the fee for their role in completing the transaction.

How are credit card processing fees determined?

Interchange fees are set by card networks based on card type (rewards, corporate, debit), transaction method (in-person versus online), merchant category, and transaction size. Assessment fees are fixed percentages set by Visa, Mastercard, and other networks. Processor markup is negotiated between you and your payment processor based on your transaction volume, history, and negotiating leverage.

When do interchange fees change, and what factors influence them?

Visa and Mastercard adjust interchange rates twice yearly, typically in April and October. Changes reflect shifts in fraud patterns, competitive dynamics between card networks, regulatory pressure, and economic conditions. Individual transaction rates also vary based on how much data you provide (AVS, CVV), how quickly you settle transactions, and whether the card is present or not.

Which types of transactions incur higher processing fees?

E-commerce transactions carry higher fees (1.8% to 3.5%) than in-person transactions (1.3% to 2.7%) due to increased fraud risk. Rewards cards, corporate cards, and international cards also incur premium interchange rates. Transactions missing data elements like billing address or CVV may be downgraded to higher-cost categories.

How can businesses minimize their credit card processing fees?

Focus on three areas: negotiate your processor markup (the only truly flexible fee component), optimize transactions to qualify for lower interchange categories by providing complete data and settling daily, and prevent chargebacks that trigger fee penalties. For established businesses, switching from flat-rate to interchange-plus pricing often delivers immediate savings of 0.3% to 0.7%.

Sources

- https://www.investopedia.com/terms/m/merchant-discount-rate.asp

- https://www.globenewswire.com/news-release/2025/03/19/3045828/0/en/Merchant-Processing-Fees-in-the-United-States-Exceeded-187-Billion-in-2024.html

- https://www.bankrate.com/credit-cards/business/merchants-guide-to-credit-card-processing-fees/