Reduce Processing Fees: Strategic Guide for Merchants

How to Reduce Processing Fees: A Strategic Guide

Key Takeaways

- To reduce processing fees effectively, merchants must separate interchange, assessments, and processor markup instead of treating all fees as one blended cost.

- Only part of your total rate is negotiable, so statement analysis is the foundation of any cost-reduction strategy.

- Interchange-plus pricing usually offers better visibility than tiered pricing, especially for established merchants.

- Quarterly review of statements helps catch hidden fees, downgrades, and rate creep before they erode margin.

- Price matters, but support, funding speed, and chargeback management also affect total payment cost.

Why Processing Fee Optimization Matters

Card payments continue to play a central role in U.S. commerce. The Federal Reserve describes the payment system as the infrastructure that supports financial transactions between consumers, businesses, and financial institutions. Meanwhile, newer Federal Reserve payments data releases continue to track large national volumes of card and alternative payments, showing how important electronic payments remain for both online and in-person commerce. As a result, even small inefficiencies in your payment setup can create a meaningful margin drag when applied across months of transaction volume.

At the same time, merchant groups continue to warn that swipe fees remain a major operating expense for businesses. The Merchant Payments Coalition has repeatedly emphasized that card fees vary widely by card type, transaction type, and merchant profile, making them difficult for many businesses to interpret. That complexity is exactly why many merchants overpay. They may accept confusing statements, stay on outdated pricing models, or miss avoidable charges that quietly accumulate over time.

Understanding Payment Processing Costs

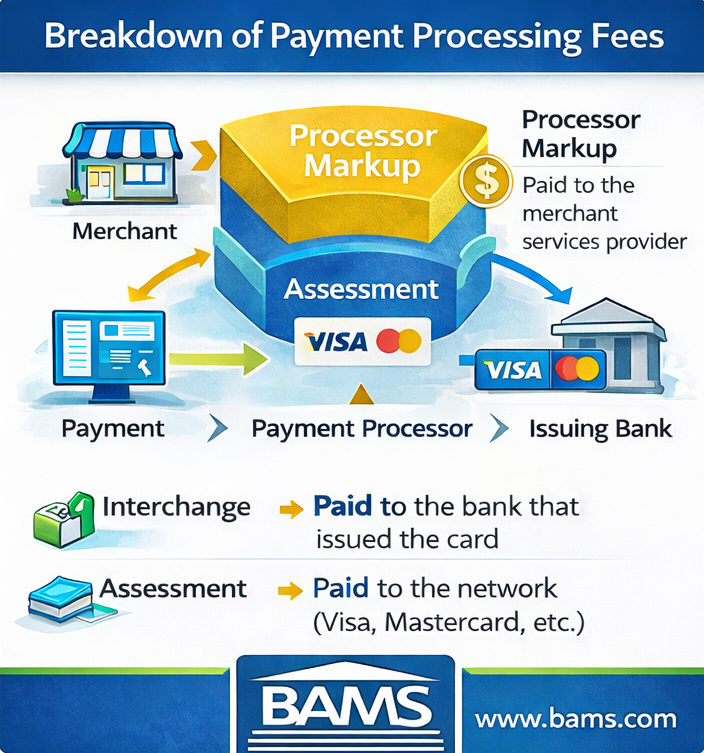

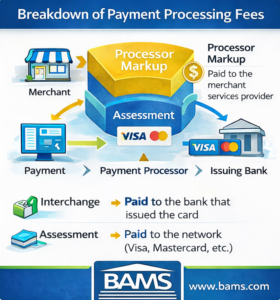

The three components of payment processing fees: interchange, card network assessments, and processor markup.

Interchange Fees

Interchange is the largest component of most card processing costs. Visa explains that interchange reimbursement fees are transfer fees between acquiring banks and issuing banks for each transaction. In practical terms, this is the baseline cost associated with a card payment. Interchange can vary based on card type, merchant category, transaction method, and the data submitted with the transaction. For example, rewards cards, commercial cards, and card-not-present transactions often cost more than basic debit transactions. Card networks such as Visa publish interchange fee schedules that determine the baseline cost of card acceptance for merchants.

Assessment and Network Fees

Card networks also charge assessment and related network fees. Mastercard’s rules and standards framework shows that the network sets requirements and fee structures that apply across participants in the card ecosystem. These network charges are generally not something an individual merchant negotiates directly. However, they are still important to understand because they affect the total cost shown on your statement.

Processor Markup

Processor markup is the portion paid to your merchant services provider or payment processor. This is where pricing flexibility usually exists. Therefore, when a merchant asks how to reduce processing fees, the answer often starts with understanding markup, monthly account fees, PCI-related charges, gateway fees, statement fees, and other processor-level costs.

Important: Interchange and many network fees are generally fixed within the card ecosystem, but processor markup and many account-level charges can often be reduced, restructured, or eliminated.

Pricing Models That Shape Your Costs

Interchange-Plus Pricing

Interchange-plus pricing breaks the total charge into two parts: the underlying interchange and assessments, plus the processor’s markup. This structure improves transparency because merchants can see what portion is driven by the card ecosystem and what portion is charged by the processor. Additionally, this model makes statement analysis easier and usually creates a more credible basis for negotiation.

Tiered Pricing

Tiered pricing groups transactions into buckets such as qualified, mid-qualified, and non-qualified. Although this model may appear simple, it often reduces transparency. A merchant may not clearly understand why certain transactions were downgraded into more expensive tiers. Consequently, tiered pricing can make it harder to identify savings opportunities.

Flat-Rate Pricing

Flat-rate pricing charges the same percentage across many transactions. This can be convenient for very small businesses or merchants that prioritize simplicity. However, businesses with higher volume or favorable transaction profiles may pay more than necessary under a flat-rate structure.

Before negotiating rates, merchants should first understand how merchant account pricing actually works. That knowledge makes it easier to compare providers on total cost rather than headline rates alone.

Framework to Reduce Processing Fees

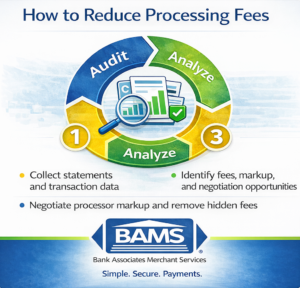

The most reliable approach to reduce processing fees follows three recurring phases: audit, analyze, and act. First, gather detailed statements and identify every line item. Next, analyze the data to understand your effective rate, pricing model, and avoidable charges. Finally, act by negotiating with your current provider or comparing alternatives. Meanwhile, continue monitoring statements after any pricing change so the savings actually materialize.

The Audit → Analyze → Act framework helps merchants systematically reduce payment processing costs.

The Audit → Analyze → Act framework helps merchants systematically reduce payment processing costs.

How to Reduce Processing Fees Step-by-Step

1. Collect at Least Six Months of Detailed Statements

Start with detailed merchant statements rather than summary invoices. You need line-item visibility into interchange, assessments, processor markup, monthly fees, PCI fees, gateway charges, chargeback fees, and any other recurring costs. If your statement is difficult to interpret, that alone may indicate a transparency problem.

Build a spreadsheet that tracks total monthly volume, number of transactions, total fees, effective rate, chargebacks, and any special fees. In addition, note whether your transactions are primarily eCommerce, recurring billing, MOTO, or in-person, because transaction type affects cost structure.

2. Calculate Your Effective Rate

Your effective rate is simple: total fees divided by total processing volume. This is one of the most useful metrics in payment cost analysis because it helps you compare months, providers, and pricing models on an apples-to-apples basis. However, the effective rate should always be interpreted in context. A card-not-present eCommerce business will often have a different cost profile than a low-risk retail merchant with mainly regulated debit volume.

3. Separate Fixed Ecosystem Costs from Negotiable Costs

Once you know your effective rate, break the statement into categories. Interchange and assessments generally represent the ecosystem-driven portion of cost. Processor markup, monthly minimums, PCI program fees, gateway charges, and statement fees are more likely to be negotiable or avoidable. Therefore, the goal is not to eliminate every fee line. The goal is to identify which fees are structural and which fees reflect pricing decisions by your provider.

4. Identify Hidden Fees and Administrative Charges

Many merchants focus only on the discount rate and overlook flat monthly or annual charges. Meanwhile, small recurring fees can compound into meaningful annual expense. Look carefully for:

- PCI noncompliance fees

- monthly minimum fees

- statement fees

- gateway or platform access fees

- batch fees

- annual account fees

- chargeback administration fees

If a fee is unclear, ask for a written explanation. If it does not support a meaningful service or if it duplicates another charge, it should be challenged.

5. Reduce Downgrades and Qualification Problems

Some merchants pay more because transactions are not qualifying for the best available categories. This can happen when required data is missing or when transactions are submitted in a way that increases risk. For eCommerce merchants, address verification, CVV capture, consistent descriptor management, and accurate transaction data can all support better processing outcomes. Similarly, B2B merchants may benefit from richer transaction data when supported by the processor and gateway.

This is also where a strong merchant services provider can add value. A capable provider should help merchants understand why downgrades occur and how operational changes can improve qualification.

6. Review Whether Your Pricing Model Still Fits

If you are on tiered pricing, compare it with an interchange-plus structure using your actual processing data. Established merchants often prefer interchange-plus because it improves transparency and gives them a better foundation for ongoing review. On the other hand, a flat-rate setup may still make sense for certain businesses that prioritize simplicity over granular optimization. The right answer depends on volume, card mix, risk profile, and operational preferences.

7. Negotiate with Data, Not Frustration

When you are ready to negotiate, bring evidence. Present your effective rate, your monthly volume, your transaction profile, your chargeback ratio, and any competing proposals you have received. Ask specifically for lower markup, removal of unnecessary monthly fees, and clarification of any charges that are difficult to justify.

Additionally, request that all changes be confirmed in writing. Verbal promises are not enough. Any pricing concession should appear in updated documentation and should be verified on future statements.

8. Compare Providers on Total Cost of Ownership

Switching providers may reduce costs, but merchants should compare more than just rate quotes. Funding speed, chargeback support, integration quality, reporting tools, contract terms, reserves, and customer support all affect the real economics of a processing relationship. Consequently, the cheapest quote is not always the best commercial outcome.

Ask potential providers to quote against actual historical processing data whenever possible. This makes comparisons more realistic and reduces the chance of being misled by simplified teaser rates.

9. Monitor for Rate Creep Every Quarter

Payment costs can drift upward over time through new fees, pricing changes, transaction mix shifts, or qualification issues. Therefore, cost optimization should be treated as an ongoing control process rather than a one-time project. Quarterly review is often enough to catch problems early without creating unnecessary administrative burden.

Should Merchants Pass Processing Fees to Customers?

Some merchants consider surcharging, cash discounts, or other fee-recovery models when trying to reduce processing costs. This decision should be approached carefully. Card brand rules, state law, customer experience, and conversion impact can all affect whether a pass-through strategy is practical. Meanwhile, many eCommerce businesses decide that a smoother checkout experience is worth more than visible fee recovery.

In many cases, the better first move is to optimize the back-end cost structure before changing the front-end customer experience. A transparent pricing model, lower markup, fewer hidden fees, and stronger operational controls can often generate meaningful savings without adding checkout friction.

Common Mistakes When Reducing Processing Fees

- Comparing only headline rates: Advertised rates rarely tell the full pricing story.

- Ignoring statement complexity: If you cannot clearly identify fee drivers, optimization becomes difficult.

- Accepting unnecessary monthly fees: Small charges often become large annual waste.

- Failing to review downgrades: Bad transaction qualification can raise cost quietly.

- Overlooking contract terms: Early termination fees, automatic renewals, and reserves may offset rate savings.

- Treating optimization as a one-time event: Ongoing review is necessary to preserve savings.

Conclusion

Merchants that want to reduce processing fees should not start with guesswork. They should start with statement analysis, pricing transparency, and a disciplined review process. Interchange and many network fees are structural parts of the card ecosystem, but processor markup, recurring account charges, and qualification problems often create room for improvement. Therefore, the smartest strategy is not simply chasing a lower advertised rate. It is building a payment setup that aligns pricing, reporting, support, and risk management with your actual business model.

Over time, that approach can improve margin, simplify financial planning, and strengthen your payments operation without disrupting customer experience.

Frequently Asked Questions

What are processing fees?

Processing fees are the costs a merchant pays to accept card payments. They typically include interchange, card network assessments, and processor markup, along with possible account-level fees such as gateway or PCI-related charges.

Can small businesses negotiate processing fees?

Yes. Many processors have flexibility on markup and account-level fees, especially when a business has stable volume, a manageable risk profile, and good payment history.

What is the easiest way to reduce processing fees?

The fastest starting point is to review detailed statements, calculate your effective rate, and identify fees that are negotiable or unnecessary. From there, compare pricing models and negotiate with documented data.

Is interchange-plus better than tiered pricing?

For many established merchants, interchange-plus offers better transparency and easier cost analysis. However, the best structure depends on transaction mix, volume, and operational priorities.

Should eCommerce businesses use surcharging to offset fees?

It depends on brand rules, legal requirements, and customer expectations. Many online businesses first try to lower back-end payment costs before introducing checkout friction.

Sources