Transaction Fees and eCommerce Margins Explained

Why Transaction Fees Are Quietly Killing Your Margins

The “cost of doing business” mindset may be costing eCommerce brands more than they realize. Transaction fees are one of the most overlooked profit drains in modern eCommerce. Every online payment includes interchange, card network fees, and processor markup, yet many businesses still treat these costs like unavoidable overhead. That mindset can become expensive over time. Therefore, merchants that want stronger margins should stop viewing payment costs as a passive expense and start evaluating them as a strategic variable. In practice, even small improvements in pricing transparency, chargeback management, and cash flow timing can create meaningful gains for growing brands.

Key Takeaways

- Transaction fees are not just an accounting line item. They directly affect eCommerce margin, cash flow, and growth capacity.

- Payment costs usually include interchange, network fees, and processor markup, but the total burden can also include chargeback and account-level fees.

- Businesses that understand their effective rate are better positioned to reduce hidden costs and negotiate better processor terms.

- Fast funding, clearer pricing, and stronger chargeback defense can materially improve operating flexibility.

- A processor should function as a margin partner, not just a vendor that passes costs through without guidance.

The Silent Leak in Your eCommerce Business

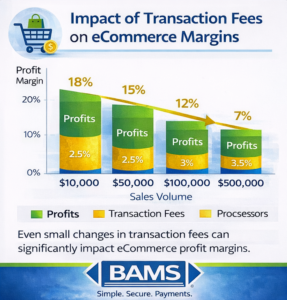

Even small increases in transaction fees can significantly reduce profit margins for growing eCommerce businesses.

Many eCommerce teams track marketing metrics closely, yet transaction fees often receive far less attention. Industry groups such as the National Retail Federation note that card swipe fees are among the largest operating costs for many retailers accepting digital payments.The problem is rarely just the headline percentage on a quote. It is the broader mix of pass-through costs, processor markup, chargeback exposure, and timing frictions that affect how much value a business keeps from each sale.

The “Cost of Doing Business” Trap in eCommerce

A common assumption is that transaction fees are simply the price of accepting cards online. However, merchant advocacy groups note that swipe fees remain one of the largest and fastest-growing operating costs for businesses accepting card payments according to the Merchant Payments Coalition.

When businesses accept this cost structure without analysis, they lose leverage. They stop asking whether pricing is transparent, whether chargeback prevention is strong enough, or whether funding timelines are slowing down growth. In addition, they miss the fact that some portions of their payment expense are more flexible than others.

Transaction Fees as a Strategic Growth Lever

Transaction fees should be viewed as a strategic decision, not just a background cost. Visa explains that interchange reimbursement fees are transfer fees between acquiring banks and issuing banks for each card transaction, while merchants negotiate and pay a broader merchant discount to their financial institution or processor. That distinction matters because it shows merchants where pricing flexibility usually exists and where it generally does not.

In other words, the smartest merchants do not waste time trying to eliminate structural card-system costs entirely. Instead, they focus on the parts of the fee stack they can influence, such as processor markup, account-level fees, dispute performance, and funding efficiency.

Reducing transaction fees through pricing transparency, dispute management, and processor negotiation can turn payments into a growth lever.

The Math Behind Margin Pressure

The direct effect of transaction fees is simple: when the effective rate rises, margin falls. For a business processing meaningful monthly volume, even a modest reduction in total payment cost can create meaningful annual savings. Meanwhile, the reverse is also true. Small increases in pricing, fee creep, or dispute costs can quietly erode profitability over time.

That is why effective rate matters so much. A business may believe it is paying one price based on a sales quote, yet the actual statement can tell a different story once network fees, processor markup, monthly charges, and dispute-related costs are included.

The Chargeback Problem

Chargebacks add another layer of cost that many merchants underestimate. They do not just create fee exposure. They also consume team time, weaken unit economics, and introduce operational friction. For some eCommerce businesses, poor dispute management can become a recurring source of margin pressure. Therefore, chargeback prevention should be treated as part of payment cost management rather than as a separate isolated problem.

The Hidden Cost of Slow Funding

Funding speed also affects profitability more than many businesses realize. Faster access to settled funds supports inventory replenishment, advertising flexibility, and working-capital efficiency. By contrast, slower funding can create timing gaps that make a growing business less agile. While funding speed is not always the first metric merchants review, it is often part of the broader economics of a processing relationship.

What This Means for Your Business

If transaction fees are a strategic variable, then the quality of your payment setup becomes a high-leverage business decision. The goal is not only to pay less. The goal is to create a payments operation that supports healthier margins, clearer forecasting, and stronger day-to-day execution.

Merchants that do this well usually know their effective rate, understand their pricing structure, and review their statements with consistency. They also know whether their processor relationship is creating transparency or confusion.

A Better Way to Think About Payments

Instead of treating a processor as a simple vendor, many merchants benefit from treating the relationship as a margin partnership. A strong processor relationship should support clearer reporting, proactive guidance, and more practical help with pricing, disputes, and funding expectations. Understanding how merchant account pricing works is one of the first steps in evaluating whether a payment setup is actually aligned with business goals.

The Federal Reserve describes the payment system as the infrastructure that facilitates financial transactions for consumers, businesses, and institutions. In practical terms, that means every payment flows through a larger ecosystem. Merchants that understand this ecosystem are usually better prepared to analyze what they are paying and where improvements are possible.

The Businesses That Get This Right

eCommerce businesses that manage payment costs strategically tend to share a few habits. They review statements regularly. They calculate what a change in effective rate would mean for annual profit. They distinguish structural fees from negotiable fees. Most importantly, they stop accepting vague answers about payment costs and start asking for real transparency.

Over time, those habits matter. The businesses that monitor payment economics with discipline are often better positioned to preserve margin and move faster when growth opportunities appear.

Conclusion

Transaction fees are not just a routine operating expense. They are a recurring factor in how much value an eCommerce business keeps from every sale. Therefore, businesses that want stronger profitability should look beyond quoted rates and evaluate the full economics of their processing relationship, including pricing structure, chargeback exposure, and funding performance.

A knowledgeable merchant account provider can help businesses make that analysis more practical by improving transparency and reducing unnecessary cost. For merchants that want better control over margin, that shift in mindset can be more valuable than it first appears.

Frequently Asked Questions

How are credit card processing fees determined?

Processing fees usually combine interchange, card network fees, and processor markup. The total cost depends on factors such as card type, transaction method, risk profile, and account pricing structure.

Which transactions incur higher processing fees?

Card-not-present transactions, premium rewards cards, corporate cards, and transactions in higher-risk categories often carry higher overall payment costs.

How can businesses minimize credit card processing fees?

Merchants can improve outcomes by using transparent pricing, reviewing their effective rate, reducing avoidable disputes, optimizing transaction data, and negotiating processor-controlled fees.

What is an effective processing rate?

The effective processing rate is calculated by dividing total processing fees by total card transaction volume. It is one of the best ways to understand real payment cost beyond a quoted rate.