Digital Wallet Payments vs Broad Expansion Strategies

Compare two payment strategies to find which delivers faster deposits without adding operational complexity

Learn which payment expansion approach fits your business. This comparison examines digital wallets versus broad payment options, covering deposit timing, processing costs, and customer experience impact.

TL;DR

- Focused beats broad for most businesses – Digital wallet expansion delivers faster deposits, lower costs, and better security compared to adding every payment method available

- Wallets dominate customer interactions – One-click checkout reduces abandonment more than adding payment buttons

- Deposit timing depends on your processor – Payment method mix matters less than whether your processor offers guaranteed next-day funding and predictable settlement

- Recurring payments need wallet support – Tokenized wallet payments update automatically when cards expire, protecting subscription revenue from involuntary churn

- Go broad only for international markets – Region-specific payment methods make sense when serving markets like Netherlands (iDEAL) or Brazil (Boleto) where customers expect local options

The Payment Expansion Dilemma: Speed vs. Complexity

E-commerce managers face a frustrating paradox. You want to offer customers more ways to pay, but each new payment method can introduce processing delays, reconciliation headaches, and unpredictable deposit timing. According to Visa, digital payments continue to scale globally, and your customers expect these options at checkout.

The question isn’t whether to expand payment options. It’s which expansion strategy actually speeds up your cash flow instead of slowing it down. This comparison breaks down two approaches: broad payment method expansion versus focused investment in digital wallets and recurring payments support.

We’ll examine deposit timing, processing costs, customer experience impact, and operational complexity to help you decide which path fits your business.

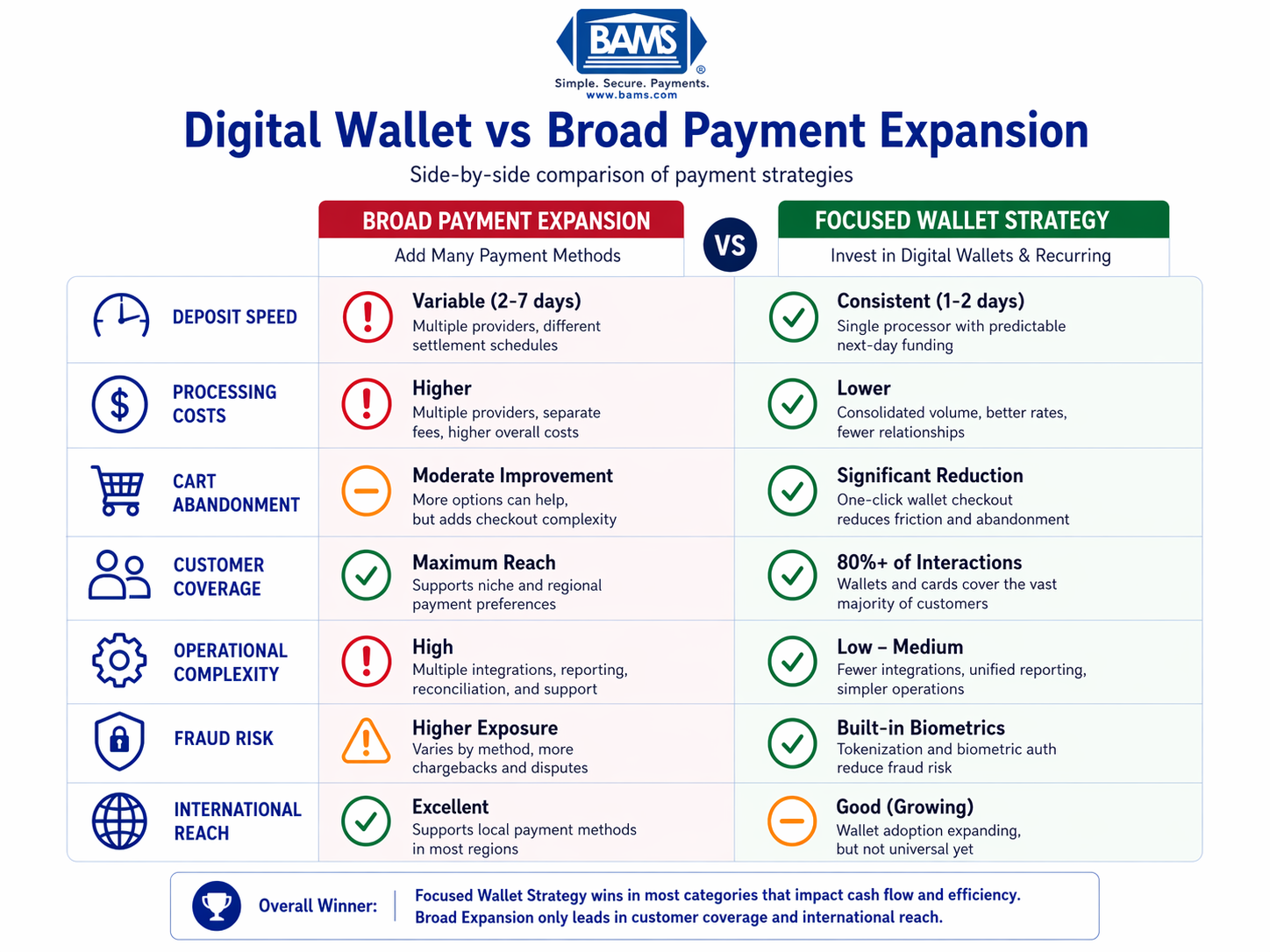

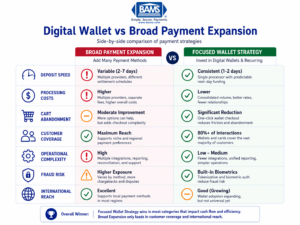

Quick Verdict: Choose Your Priority

A side-by-side comparison showing how digital wallet strategies outperform broad payment expansion in speed, cost, and operational efficiency.

Choose focused digital wallet expansion if you want faster deposits, lower cart abandonment, and streamlined operations. Wallets like Apple Pay and Google Pay offer one-click authentication that speeds transactions without adding backend complexity.

Choose broad payment option expansion if you serve international markets with region-specific payment preferences or niche customer segments that require specific methods like buy-now-pay-later or cryptocurrency.

For most established eCommerce businesses processing $500K+ annually, focused wallet integration delivers better ROI with fewer operational headaches.

|

Criterion |

Broad Payment Expansion |

Focused Wallet + Recurring |

Winner |

|---|---|---|---|

|

Deposit Speed |

Variable (2-7 days) |

Consistent (1-2 days) |

Focused |

|

Processing Costs |

Higher (multiple providers) |

Lower (consolidated) |

Focused |

|

Cart Abandonment |

Moderate improvement |

Significant reduction |

Focused |

|

Customer Coverage |

Maximum reach |

80%+ of interactions |

Broad |

|

Operational Complexity |

High |

Low-Medium |

Focused |

|

Fraud Risk |

Higher exposure |

Built-in biometrics |

Focused |

|

International Reach |

Excellent |

Good (growing) |

Broad |

How We’re Comparing These Approaches

Deposit timing matters most for cash flow management. Delayed deposits force you to float operational costs, and unpredictable timing makes financial planning difficult.

Processing costs directly impact margins. Each payment provider takes a cut, and managing multiple relationships often means higher aggregate fees.

Customer experience affects conversion rates. Checkout friction causes abandonment, but offering unfamiliar options can also create confusion.

Operational complexity determines how much time your team spends on reconciliation, dispute management, and provider relationships instead of growth activities.

Fraud protection varies significantly between payment methods. Some require additional security layers, while others include built-in verification.

Scalability determines whether your payment infrastructure supports growth or becomes a bottleneck.

Digital Wallet Payments: Head-to-Head Analysis

Deposit Speed and Cash Flow Impact

Broad expansion approach: Adding multiple payment methods typically means working with multiple processors or aggregators. Each has different settlement schedules. ACH transfers take 3-5 business days. International methods can take longer. Your cash flow becomes unpredictable.

Focused wallet approach: Digital wallets process through established card networks with predictable settlement. When paired with a processor offering guaranteed next-day funding, you get consistent deposit timing.

Verdict: Focused wins. Consolidating around wallets and cards with a processor offering guaranteed next-day funding eliminates the deposit timing variability that makes cash flow planning difficult.

Processing Costs and Fee Structures

Broad expansion approach: Each payment method carries its own fee structure. Buy-now-pay-later services charge 2-8% per transaction. Regional payment methods often require separate processor relationships with monthly minimums. Costs add up quickly.

Focused wallet approach: According to the Federal Reserve, interchange and transaction structures vary widely, and consolidating payment methods reduces the number of processor relationships and their associated fees.

Verdict: Focused wins. Fewer processor relationships mean lower aggregate costs and simpler fee negotiations. You also gain leverage for better rates as volume consolidates.

Customer Experience and Conversion Rates

Broad expansion approach: More options can reduce abandonment for customers who prefer specific methods. However, cluttered checkout pages create decision fatigue. Each additional button requires explanation and support.

Focused wallet approach: Digital wallets captured a growing share of eCommerce volume through one-click authentication that reduces cart abandonment. Customers already have payment credentials stored. Checkout becomes faster, not more complicated.

Verdict: Focused wins for most audiences. One-click wallet checkout outperforms adding five more payment buttons. The exception is international markets with strong regional payment preferences.

Recurring Payments Support and Subscription Revenue

Broad expansion approach: Not all payment methods support recurring billing. Some require customers to re-authorize each charge. Others have high decline rates for subscription renewals. Managing multiple recurring payment systems creates reconciliation nightmares.

Focused wallet approach: Digital wallet usage continues to grow rapidly, with strong recurring payment support. Tokenized wallet payments update automatically when cards expire, reducing involuntary churn.

Verdict: Focused wins decisively. Digital wallet integration for eCommerce provides reliable recurring billing with automatic credential updates that protect subscription revenue.

Fraud Protection and Security

Broad expansion approach: Each payment method has different fraud profiles. Some require additional verification layers you must implement and maintain. Chargebacks vary by method, and dispute processes differ across providers.

Focused wallet approach: Digital wallets include biometric authentication (Face ID, fingerprint) at no additional cost. Tokenization protects card data. According to the PCI Security Standards Council, secure payment environments reduce fraud exposure and simplify compliance.

Verdict: Focused wins. Wallet-based biometric verification reduces fraud without adding friction. You spend less on third-party fraud tools and chargeback disputes.

Operational Complexity and Team Resources

Broad expansion approach: Each payment provider requires its own integration, reporting dashboard, reconciliation process, and support relationship. Your finance team spends hours matching deposits to orders across multiple systems.

Focused wallet approach: Consolidating around major wallets and card payments means fewer integrations, unified reporting, and simpler reconciliation. Your team focuses on growth instead of payment administration.

Verdict: Focused wins. The operational overhead of managing multiple payment providers often exceeds the revenue gained from niche payment methods.

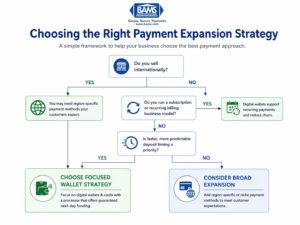

Payment Option Expansion: Use Case Mapping

A simplified decision framework to help businesses determine whether to focus on digital wallets or expand payment methods.

When Focused Wallet Strategy Wins

If you process primarily domestic transactions, choose focused wallet expansion. Apple Pay, Google Pay, and major cards cover the vast majority of your customers. Setting up wallet acceptance takes hours, not weeks, and the conversion lift is immediate.

If cash flow predictability matters, choose focused expansion with a processor offering guaranteed next-day funding. Variable deposit timing from multiple providers makes it impossible to forecast working capital needs accurately.

If you run subscription or membership models, choose focused wallet expansion. Recurring payments support with automatic credential updates protects your revenue stream from involuntary churn.

When Broad Expansion Makes Sense

If you sell internationally across diverse markets, you may need region-specific methods. iDEAL in the Netherlands, Boleto in Brazil, and Alipay in China serve customers who won’t convert otherwise.

If your average order value exceeds $500, buy-now-pay-later options can lift conversion enough to justify the higher processing costs and operational complexity.

Edge Cases Where Neither Excels

High-risk product categories face payment restrictions regardless of strategy. Both approaches require specialized processors willing to underwrite your risk profile.

What Both Approaches Get Wrong

Neither payment expansion strategy solves fundamental processor relationship problems. If your current provider has slow deposits, poor dispute support, or opaque pricing, adding or consolidating payment methods won’t fix those issues.

The payment industry also hasn’t solved cross-border fee complexity. International transactions still carry higher costs and slower settlement regardless of which payment methods you offer.

Both approaches assume your checkout flow is already optimized. Payment method selection matters less if customers abandon before reaching that step.

Switching Costs and Migration Considerations

Moving from broad to focused: Removing payment options carries risk. Analyze transaction data to identify which methods actually drive revenue versus which just add complexity. Phase out low-volume methods gradually while monitoring conversion rates.

Moving from focused to broad: Each new payment method requires integration work, testing, and ongoing maintenance. Budget 2-4 weeks per method for proper implementation. Factor in ongoing reconciliation time.

Processor switching: If deposit delays stem from your processor rather than payment method mix, switching providers may deliver faster results than restructuring payment options. Look for processors offering guaranteed next-day funding, transparent pricing, and dedicated support.

Mobile merchant account services can also bridge gaps during transitions, letting you accept payments while restructuring your primary processing relationship.

Data portability: Ensure you can export transaction history, customer payment tokens, and subscription billing data before switching. Some providers make migration deliberately difficult.

The Faster Deposit Strategy That Actually Works

For established eCommerce businesses processing significant volume, focused expansion around digital wallets and recurring payments delivers better outcomes than adding every payment method available. You get faster deposits, lower costs, better security, and simpler operations.

The exception is international businesses serving markets with strong regional payment preferences. Even then, start with wallets and cards, then add regional methods only where transaction data proves demand.

Your payment infrastructure should accelerate growth, not consume management attention. Choose the approach that gets you paid faster with less complexity, then focus your energy on what actually grows revenue.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies include choosing processors that offer next-day funding, consolidating payment methods to reduce settlement variability, and prioritizing digital wallets that process through established card networks. The key is reducing the number of different settlement schedules you’re managing.

Why is payment optimization important for businesses?

Payment optimization directly impacts cash flow, profit margins, and customer conversion rates. Delayed deposits force you to float operational costs. High processing fees eat into margins. Poor checkout experiences cause abandonment. Optimizing payments addresses all three problems simultaneously.

How can I improve my payment authorization rates?

Digital wallets typically have higher authorization rates because they use tokenized credentials and biometric verification. Reducing the number of payment methods also helps because you can focus on optimizing the checkout flow for your primary methods rather than supporting many options poorly.

When should I consider expanding my payment options?

Expand payment options when transaction data shows customers abandoning checkout due to missing payment methods, when entering international markets with strong regional payment preferences, or when your average order value justifies buy-now-pay-later options despite higher fees.

Which payment processing fees can I reduce to optimize costs?

Consolidating payment methods reduces aggregate fees by eliminating multiple processor relationships and their associated monthly minimums. Digital wallets can also reduce interchange costs through pay-by-bank options. Negotiating rates becomes easier when volume consolidates with fewer providers.

What role does fraud protection play in payment optimization?

Strong fraud protection reduces chargebacks, which carry fees and can threaten your merchant account standing. Digital wallets include biometric authentication that reduces fraud without adding checkout friction. Less fraud means lower costs and more reliable payment processing.

Sources