6 Places Cash Flow Delays Hide in Your Payment Stack

Diagnose the exact setup variables slowing your deposits — most are fixable without switching processors

Learn how to pinpoint six specific variables in your payment pipeline that quietly delay deposits and disrupt cash flow management. This diagnostic guide helps eCommerce operators identify fixable friction points in platform settings, gateway configurations, and batch timing.

TL;DR

- Deposit speed is a system, not a single setting – Six independent variables (platform, gateway, processor cut-off, bank, transaction type, sale timing) each add their own delay, and the total lag is the sum of all of them.

- Gateway batch timing and processor cut-off time zones cause the most common “lost day” – Misalignment between when your gateway submits and when your processor’s daily window closes can push deposits out by a full business day.

- Weekend and holiday sales create compounding cash flow gaps – If 30% or more of your weekly revenue falls on weekends, standard ACH settlement means that money sits idle for two to three extra days.

- Your transaction mix triggers hidden holds – Card-not-present transactions, international cards, and high-ticket orders can flag risk reviews that delay entire batches, especially during sale events.

- Start with two fixes – Align your batch close time with your processor’s cut-off, and confirm that cut-off in your local time zone. These two changes require minimal effort and eliminate the most common unnecessary delays.

Where Your Deposit Delays Are Actually Hiding

Your payment processing speed is not a single setting. It is a chain of handoffs, and any weak link slows down when money reaches your bank account. Most eCommerce operators treat funding speed as something their processor either offers or doesn’t. In reality, FedNow Service resources continue to demonstrate how payment speed directly affects liquidity management and cash flow visibility for businesses.

The difference between same-day and next-day funding gets all the attention. But the difference between next-day and “three days later” is where most businesses are losing ground without realizing it. Weekend sales surges, batch timing mismatches, and gateway configurations quietly compound into gaps that look like normal processor behavior but are actually fixable setup problems.

What This Guide Covers (and What It Doesn’t)

This guide is for eCommerce managers at established online businesses who suspect their deposits take longer than they should but aren’t sure where the friction lives. If you run a store doing consistent volume and you’ve accepted your current settlement timeline as “just how it works,” this is for you.

We are not comparing processor brands or ranking funding speeds. We are walking through six specific points in your payment pipeline where delays accumulate, explaining why each one matters, and giving you diagnostic steps to identify which ones apply to your setup. The goal is to turn cash flow management from a vague concern into a concrete checklist.

How We Selected These Six Delay Points

Each item on this list meets three criteria: it introduces measurable delay to your deposit timeline, it is configurable or negotiable by the merchant (not hardcoded into card network rules), and it disproportionately affects eCommerce businesses compared to brick-and-mortar. If a delay point didn’t meet all three, it didn’t make the list.

6 Points in Your Payment Stack Where Deposit Delays Hide

Deposit delays are rarely caused by one issue. Most are the result of multiple small delays stacking together.

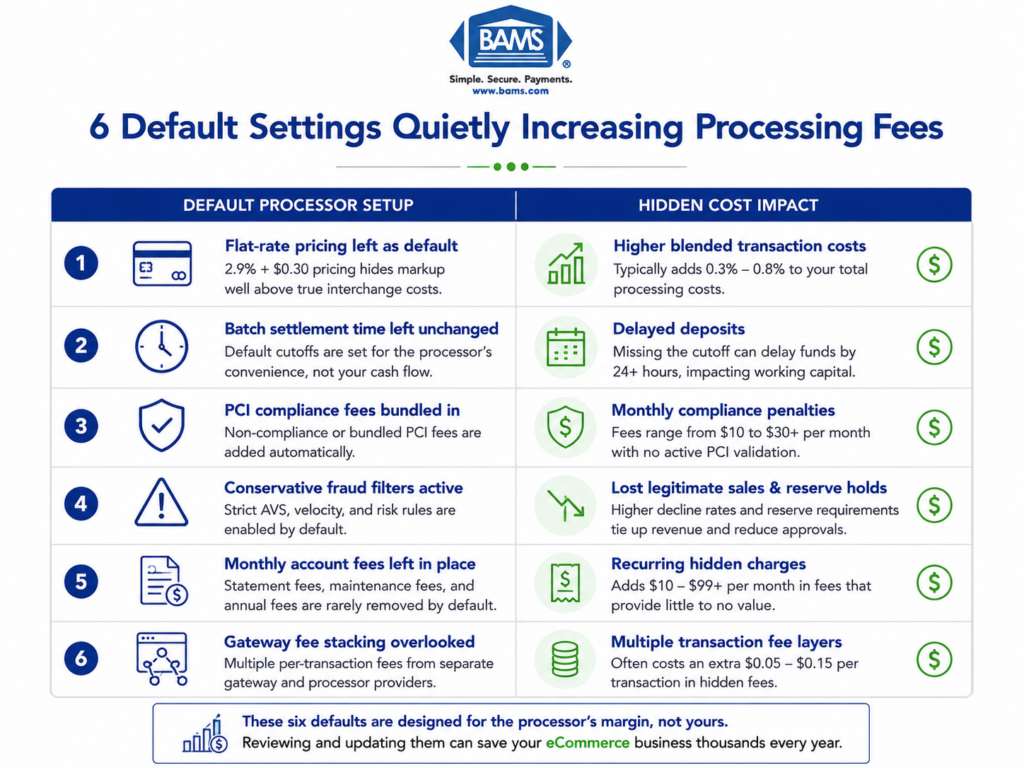

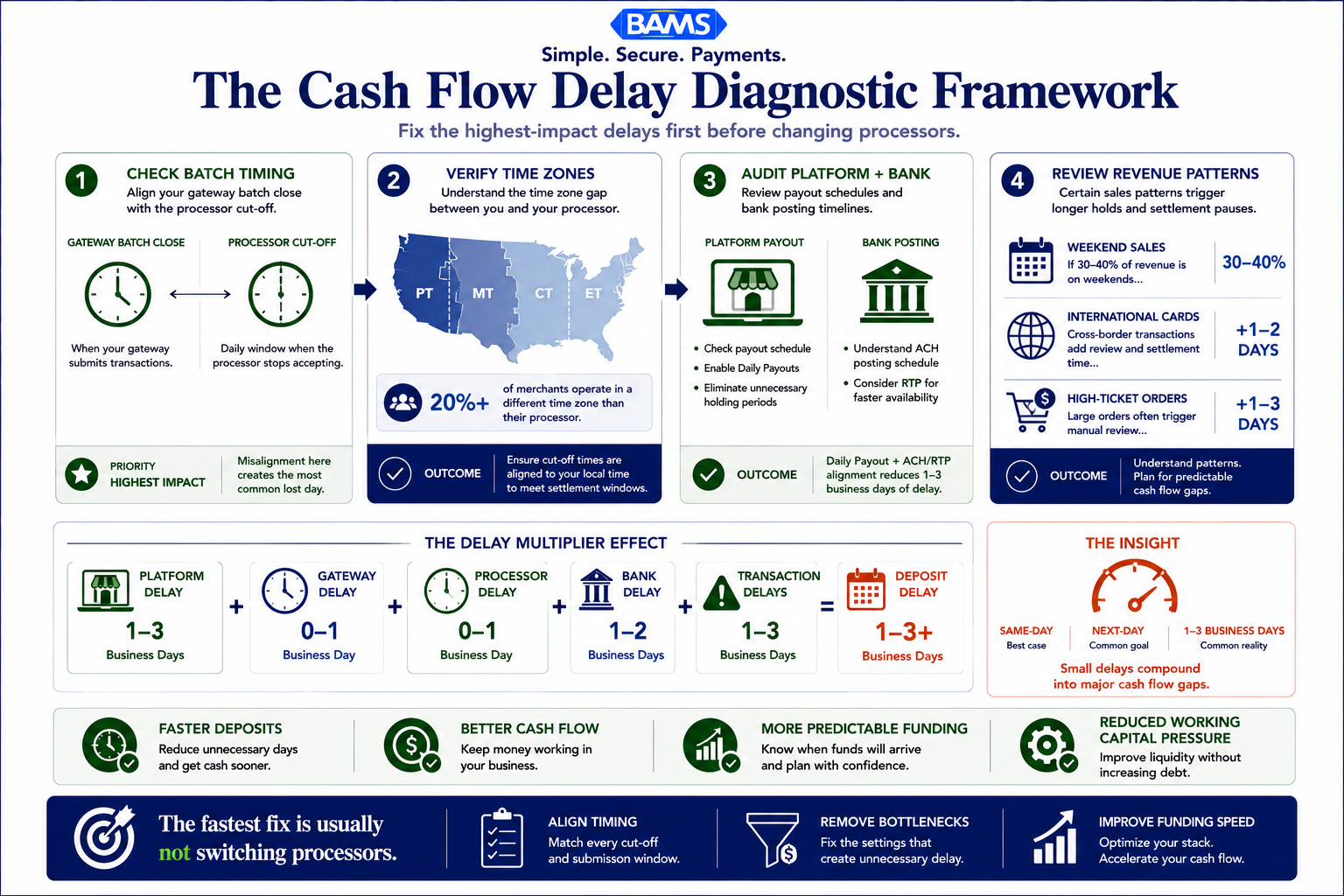

1. Your Ecommerce Platform’s Default Payout Schedule

Why it matters: Most eCommerce platforms ship with conservative payout defaults. Shopify, WooCommerce, BigCommerce, and others each handle settlement differently, and the gap between what’s possible and what’s configured out of the box can be one to three business days. Operators often assume their payout schedule reflects their processor’s speed. It usually reflects the platform’s default.

What it looks like today: Platforms bundle transactions and release payouts on their own cycle. Some hold funds for new accounts or flag certain order types for review, adding invisible delays on top of the processor’s timeline. Funds typically move from issuing bank to acquiring bank within one to three business days, but your platform may add its own buffer before releasing to your account.

How to apply it: Log into your platform’s payment settings and compare your current payout frequency to the fastest option available at your account tier. If you’re on a daily payout cycle, confirm whether it’s truly daily or “daily with a two-day rolling hold.” Document the actual timeline from sale to deposit for five recent transactions.

2. Your Gateway’s Batch Window and Submission Timing

Why it matters: Your payment gateway collects authorized transactions and submits them to your processor in batches. The timing of that batch submission determines which settlement cycle your sales enter. A batch that closes at 10 PM Eastern catches the current day’s cycle. A batch that closes at 2 AM may push your transactions to the next cycle, adding a full business day to your deposit.

What it looks like today: Traditional processors take two to three business days to settle, and a misaligned batch window makes that timeline even longer. Many gateways let you configure batch close times, but the setting is buried in admin panels that rarely get revisited after initial setup. NACHA ACH Network resources explain how ACH settlement schedules and business-day processing windows directly affect when merchants receive funds.

How to apply it: Find your gateway’s batch close time and compare it to your processor’s cut-off for same-day or next-day settlement. If there’s a gap, adjust the batch window to close 30 to 60 minutes before the processor’s cut-off. For high-volume days (flash sales, product launches), consider whether a manual batch close before the cut-off captures more revenue in the earlier cycle.

3. Your Processor’s Cut-Off Time (and the Time Zone It Lives In)

Why it matters: Every processor has a daily cut-off time after which transactions roll to the next business day’s settlement. This is the single most misunderstood variable in merchant services funding speed. A West Coast business using a processor with an Eastern Time cut-off effectively loses three hours of sales from each day’s settlement window.

What it looks like today: Cut-off times vary widely, from 5 PM to 11 PM Eastern depending on the processor and funding tier. Some processors offer extended cut-offs for next-day funding customers. Others apply the same cut-off regardless of your plan. The time zone mismatch issue is especially acute for eCommerce businesses with customers shopping across multiple zones.

How to apply it: Call your processor and ask for the exact cut-off time in your local time zone. Then pull your sales data and calculate what percentage of daily revenue arrives after that cut-off. If a meaningful share of transactions (20% or more) consistently misses the window, you have a structural delay worth addressing, either by negotiating a later cut-off or by aligning your batch timing more aggressively.

4. Your Bank Relationship and Deposit Rails

Why it matters: Your processor sends funds to your bank, but the speed of that transfer depends on which payment rails are used and whether your bank processes incoming ACH on the same schedule. Real-time payment networks like RTP can deliver funds on any day, at any time, but most merchant deposits still travel via standard or same-day ACH, which operates on banking-day schedules with specific processing windows. FedNow participating organizations provide visibility into which financial institutions have adopted faster payment capabilities, helping merchants evaluate potential funding speed improvements.

What it looks like today: A processor may release funds for next-day deposit, but if your bank doesn’t process incoming ACH until the afternoon, you won’t see the balance until late in the day or the following morning. Smaller community banks and credit unions sometimes have later ACH processing windows than large national banks.

How to apply it: Ask your bank when incoming ACH credits are posted to your account. Compare that to when your processor releases the funds. If there’s a mismatch, consider whether your bank offers faster posting for business accounts or whether a banking relationship change would close the gap. Some processors, including BAMS with its next-day funding, structure their release timing to align with common bank posting windows, reducing the last-mile delay.

5. Your Transaction Type Mix (and Its Risk Profile)

Why it matters: Not all transactions settle at the same speed. Card-not-present transactions (your entire eCommerce volume) carry higher fraud risk than card-present swipes, and processors often apply longer hold times or additional review steps to CNP batches. International cards, high-ticket orders, and first-time customers can trigger further delays. Your transaction mix directly shapes your effective settlement speed.

What it looks like today: Processors use risk scoring to flag batches or individual transactions for review. A batch with a high percentage of international cards or orders above your typical average ticket may be held for manual review, delaying the entire batch’s settlement. During sale events when order volume spikes and average ticket sizes shift, these risk triggers fire more frequently.

How to apply it: Review your processor’s hold and review policies. Ask specifically which transaction characteristics trigger delays. Then cross-reference against your actual sales data: what percentage of your transactions are international, above your average ticket, or from new customers? If the answer is “a lot,” work with your processor to adjust risk thresholds or pre-clear expected volume changes before major sales events. Proactive communication with your processor before a planned promotion can prevent surprise holds.

6. Your Sale Timing and Weekend Volume Patterns

Why it matters: eCommerce revenue doesn’t pause on weekends, but most settlement infrastructure does. Friday evening through Sunday represents a significant revenue window for many online stores, and every dollar earned during that period typically doesn’t settle until Monday or Tuesday. For businesses running weekend promotions or flash sales, this creates a compounding cash flow gap where your highest-revenue period produces the longest deposit delay.

What it looks like today: Standard ACH does not process on weekends or federal holidays. A Friday evening sale batched on Saturday won’t enter the settlement cycle until Monday, with funds arriving Tuesday or Wednesday. For a business doing 30% to 40% of weekly volume on weekends, that’s a meaningful portion of revenue sitting in limbo. This is where next-day funding structures and real-time payment rails offer the most tangible advantage.

How to apply it: Pull your sales data by day of week and calculate what percentage of weekly revenue falls on Friday after your cut-off through Sunday. Multiply that by your average settlement delay to quantify the cash flow gap in dollar-days. If the number is significant, evaluate whether your processor offers weekend or holiday funding. If not, consider adjusting promotional timing so that your highest-volume campaigns land earlier in the week, or negotiate a funding arrangement that accounts for weekend volume patterns.

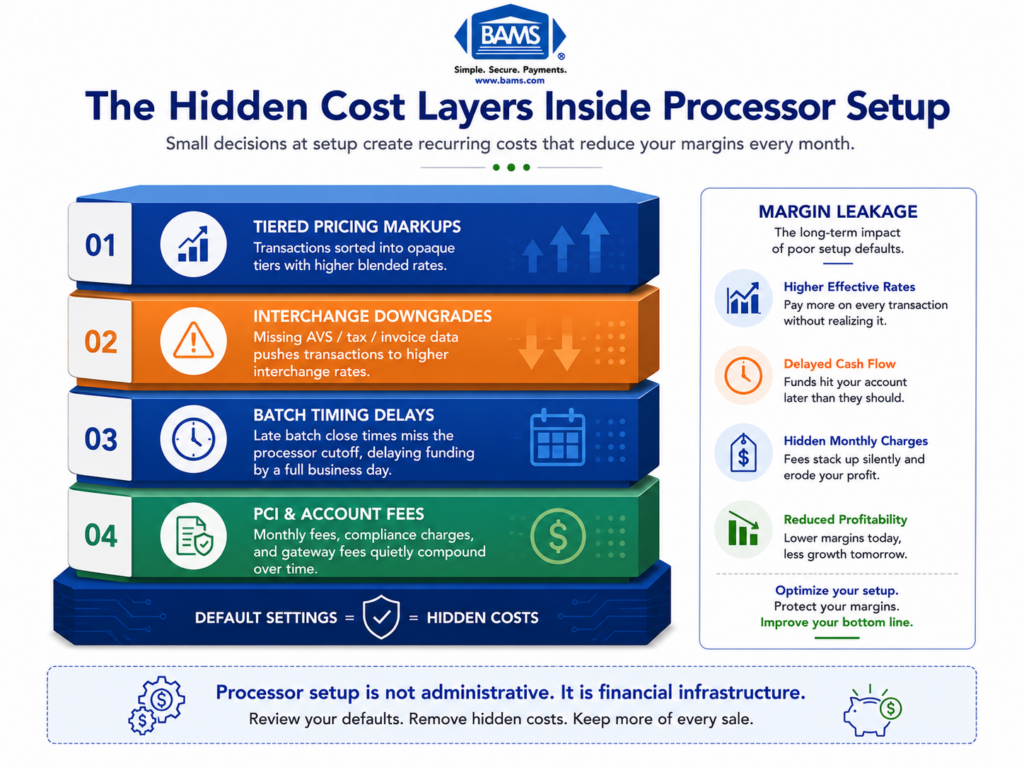

The Pattern Across All Six Delay Points

Three themes connect these variables. First, delays are layered: platform payout schedules, gateway batch timing, processor cut-offs, and bank posting windows each add their own buffer, and the total delay is the sum of all four, not the largest single one. Shaving 12 hours off three layers can matter more than eliminating one layer entirely.

Second, eCommerce-specific patterns (weekend volume, card-not-present risk, cross-border transactions) act as multipliers on structural delays. A two-day settlement lag is manageable when sales are evenly distributed. It becomes a real cash flow management problem when 35% of your weekly revenue hits during the slowest settlement window.

Third, most of these variables are negotiable or configurable, but only if you know they exist. The default assumption that “my processor is slow” often masks three or four independent settings that were never optimized after initial setup.

Where to Start: Prioritizing Your Fixes

Start with the settings that create the biggest delays before evaluating more complex funding options.

You don’t need to address all six at once. Start with the two that require the least effort and produce the most visibility: check your gateway batch close time (item 2) and confirm your processor’s cut-off in your local time zone (item 3). These two settings alone account for the majority of “lost day” delays and can often be adjusted in a single phone call or admin panel change.

Once those are aligned, move to your platform payout settings (item 1) and bank posting schedule (item 4). The transaction mix and weekend timing items (5 and 6) require more data analysis but yield the highest returns for businesses with seasonal spikes or heavy weekend traffic. If you find that your current processor can’t accommodate the adjustments you need, that’s a signal to evaluate providers like BAMS that structure their merchant services around faster, more transparent funding.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your payment processor deposits your settled transaction revenue into your bank account by the next business day after the sale. Instead of waiting the standard two to three business days, you get access to funds roughly 24 hours after your batch closes. Some processors front the funds before the full clearing cycle completes, while others simply operate on faster settlement rails.

How can a business qualify for next-day funding?

Qualification typically depends on your processing volume, business history, chargeback ratio, and industry risk category. Most processors require a minimum operating history (often three to six months) and a chargeback rate below a certain threshold. Some providers, including BAMS, offer next-day funding as a standard feature rather than a premium add-on, which simplifies the qualification process.

What are the differences between next-day funding and standard funding?

Standard funding typically takes two to three business days from the time your batch is submitted to when funds appear in your account. Next-day funding compresses that to one business day. The mechanical difference is usually a combination of earlier batch processing, faster payment rails (such as same-day ACH), and the processor’s willingness to release funds before the full interbank clearing cycle completes.

When should a business consider using same-day funding services?

Same-day funding is most valuable when your business has tight cash conversion cycles, such as needing to reorder inventory immediately after a sale event, meeting payroll on a specific schedule, or covering supplier payments that don’t align with your deposit timing. If your weekend and holiday sales volume is high, same-day or real-time funding can eliminate the multi-day gap that standard settlement creates.

Why do weekend sales take longer to deposit?

Standard ACH networks do not process transactions on weekends or federal holidays. Sales made Friday evening through Sunday are batched and submitted on Monday, entering the settlement cycle a full one to two days later than a Monday sale would. This means weekend revenue often doesn’t arrive until Tuesday or Wednesday, creating a cash flow gap for businesses with significant weekend traffic.

Which factors affect the approval for next-day funding?

The primary factors are your business’s chargeback history, average transaction size, monthly processing volume, industry classification, and how long you’ve been processing with your current provider. High-risk industries or businesses with elevated chargeback ratios may face longer holds regardless of their funding tier. Maintaining clean transaction data and low dispute rates is the most reliable way to qualify and maintain faster funding.