How Payment Gateways Work: Payment Gateway Glossary for Merchants

Glossary of Key Terms Every Merchant Should Know About Payment Gateways

Digital payments power nearly every modern business transaction, but many merchants still ask how do payment gateways work and what role they play in payment processing. Whether customers are shopping online, paying through a mobile app, or tapping a card at a point-of-sale terminal, the payment ecosystem works behind the scenes to move money securely between banks and merchants.

Yet for many merchants, the terminology surrounding payment technology can feel overwhelming. Terms like payment gateway, processor, interchange fees, and PCI DSS compliance often get used interchangeably, even though they represent different parts of the payment infrastructure.

Understanding how do payment gateways work is critical for merchants who want to manage costs, reduce risk, and scale their businesses effectively. Payment technology directly impacts approval rates, fraud prevention, customer experience, and regulatory compliance.

This guide was designed for:

-

eCommerce merchants

-

omnichannel retailers

-

small and mid-sized businesses (SMBs)

-

subscription and recurring-billing businesses

Below, you’ll find a clear explanation of how payment gateways work, followed by a glossary of essential payment terms every merchant should know.

As a trusted payment technology provider, BAMS helps businesses navigate these complexities and implement secure, scalable payment solutions tailored to their needs.

Key Takeaways

-

A clear explanation of how do payment gateways work

-

Definitions of essential payment terms affecting cost and approvals

-

The difference between gateways, processors, merchant accounts, and PSPs

-

How chargebacks, PCI DSS compliance, and ACH payments affect risk

-

How choosing the right gateway partner supports business growth

How Do Payment Gateways Work?

To understand the digital payment ecosystem, merchants first need to understand how do payment gateways work.

A payment gateway acts as a secure bridge between a customer, the merchant’s website or POS system, and the financial institutions responsible for approving the transaction. Payment gateways securely collect and protect cardholder information during checkout before it is routed to processors and banks.

The payment gateway process connects merchants, processors, card networks, and issuing banks to securely authorize and settle digital payments.

Here’s how a typical payment gateway transaction works.

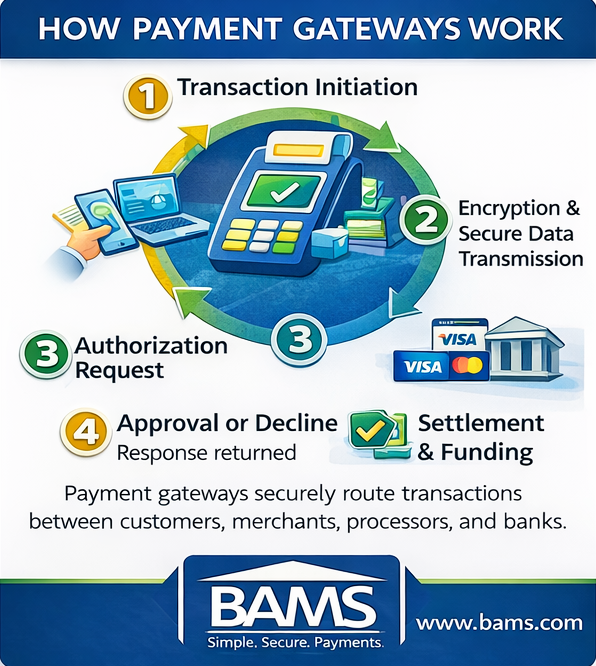

1. Transaction Initiation

The process begins when a customer enters their payment information.

This may occur through:

-

an online checkout page

-

a mobile payment form

-

a POS terminal in a physical store

The payment gateway securely captures the card or bank data and prepares it for transmission.

2. Encryption and Secure Data Transmission

Before the payment data leaves the merchant’s system, the gateway encrypts the information to protect sensitive cardholder data.

Encryption is essential for payment security and compliance with PCI DSS standards, which help protect consumer financial information across the payment ecosystem. Visa explains that PCI DSS helps ensure merchants properly safeguard cardholder data during payment processing.

The encrypted data is then sent to the payment processor.

3. Authorization Request

The payment processor routes the transaction through the appropriate card network (such as Visa or Mastercard) to the customer’s issuing bank.

The issuing bank evaluates several factors, including:

-

available credit or account balance

-

suspected fraud indicators

-

card validity

The bank then sends an authorization response back through the network.

4. Approval or Decline Response

The issuing bank returns either:

-

Approved — funds are reserved for the transaction

-

Declined — insufficient funds or risk concerns

The payment gateway sends the response to the merchant in real time so the transaction can be completed or declined.

5. Settlement and Funding

Approved transactions move into the settlement stage, where funds are transferred from the issuing bank to the merchant’s acquiring bank and eventually deposited into the merchant account.

This process typically takes one to three business days, depending on the processor and transaction type.

Payment gateways connect multiple stakeholders within the payment ecosystem:

-

customers

-

merchants

-

payment processors

-

issuing banks

-

acquiring banks

-

card networks

A common misconception is that payment gateways and processors are the same thing. In reality, a gateway verifies and securely transmits customer payment information while the processor handles the routing of transactions and settlement between banks.

Understanding this distinction is essential when selecting the right payments partner.

Payment Gateway Glossary: Key Terms Every Merchant Should Know

Below is a merchant-friendly glossary explaining the most important payment terms.

Understanding key payment gateway terminology helps merchants manage payment processing costs, security, and transaction approvals.

A–C Terms

Automated Clearing House (ACH)

The Automated Clearing House (ACH) is an electronic payment network used for bank-to-bank transfers within the United States.

Unlike card payments, ACH transactions move funds directly between bank accounts.

Common ACH use cases include:

-

subscription billing

-

B2B payments

-

payroll deposits

-

utility bill payments

ACH payments typically carry lower transaction fees than card payments, making them attractive for recurring billing and high-value transfers.

However, ACH processing times can be slower than card transactions.

The ACH network processes billions of payments annually and is overseen by NACHA, the organization responsible for managing ACH rules and standards.

Authorization

Authorization occurs when the issuing bank verifies that a cardholder has sufficient funds or credit available for a purchase.

This step is a core component of how do payment gateways work.

During authorization, the issuing bank confirms:

-

card validity

-

account status

-

available funds

-

potential fraud indicators

Authorization does not transfer funds immediately. It simply reserves the amount until the settlement stage.

Chargeback

A chargeback occurs when a cardholder disputes a transaction with their issuing bank.

Chargebacks can result from:

-

fraud or unauthorized transactions

-

products not delivered

-

billing errors

-

customer dissatisfaction

When a chargeback occurs, the issuing bank temporarily reverses the transaction while the dispute is investigated.

Excessive chargebacks can lead to:

-

higher processing fees

-

monitoring programs from card networks

-

potential account termination

For this reason, merchants often implement fraud detection tools and strong customer support processes to minimize disputes.

D–F Terms

Data Encryption

Encryption converts payment information into a secure code before transmission.

Payment gateways use encryption to protect sensitive cardholder data while it travels between systems.

Encryption plays a key role in PCI DSS compliance and helps prevent data breaches.

Card networks require encryption and other security protocols to safeguard payment transactions across the ecosystem.

Funding / Settlement

Settlement refers to the process of transferring funds from the issuing bank to the merchant’s acquiring bank.

After a transaction is authorized, it enters a settlement batch where funds are processed and deposited into the merchant account.

Typical settlement timing ranges from:

-

Next-day funding

-

Two to three business days

Settlement speed may vary depending on the processor, payment method, and merchant risk profile.

Fraud Detection Tools

Many payment gateways include built-in fraud detection capabilities.

These tools may analyze:

-

IP address location

-

card verification values (CVV)

-

address verification service (AVS)

-

transaction behavior patterns

Advanced fraud detection systems use machine learning models to detect suspicious transactions before they are approved.

Reducing fraud risk also reduces the likelihood of chargebacks.

G–I Terms

Issuer Bank

An issuer bank is the financial institution that issues a credit or debit card to the customer.

When a transaction occurs, the issuing bank determines whether to approve or decline the purchase.

Approval decisions may depend on:

-

available balance

-

credit limit

-

fraud indicators

-

card status

Issuer banks play a critical role in maintaining payment security and managing risk.

Interchange Fees

Interchange fees are charges paid by merchants to the cardholder’s issuing bank for processing card transactions. These fees are established by card networks and form one of the largest components of merchant payment processing costs.

These fees are typically set by card networks such as Visa and Mastercard.

Interchange fees help cover costs related to:

-

fraud protection

-

payment processing infrastructure

-

credit risk

Interchange fees form a major component of the merchant discount rate (MDR).

M–P Terms

Merchant Account

A merchant account is a specialized bank account that allows businesses to accept card payments.

When a customer pays by card, funds are first deposited into the merchant account before being transferred to the merchant’s business bank account.

Merchant accounts are typically provided by acquiring banks or payment processors.

Merchant Acquirer (Acquiring Bank)

The acquiring bank processes payments on behalf of the merchant.

Its responsibilities include:

-

facilitating settlement

-

managing merchant risk

-

maintaining payment network connectivity

Acquiring banks work closely with payment processors and gateways to ensure transactions flow smoothly.

Merchant Discount Rate (MDR)

The merchant discount rate represents the total cost merchants pay to accept card payments.

MDR typically includes:

-

interchange fees

-

card network fees

-

payment processor fees

Rates may vary depending on transaction type, industry risk, and payment method.

Merchants seeking better cost transparency often choose providers that offer transparent interchange plus pricing so they can clearly see processor markup and network fees.

Payment Gateway

A payment gateway is the technology that securely captures and transmits payment data during a transaction.

Gateways support various payment environments, including:

-

online checkout pages

-

mobile applications

-

point-of-sale systems

Gateways may be implemented as:

-

hosted checkout pages

-

direct integrations

-

API-based payment systems

Payment Processor

A payment processor manages the routing of transaction data between banks and card networks.

Processors handle:

-

authorization requests

-

settlement

-

transaction reporting

The processor ensures funds are transferred correctly after a transaction is approved.

Payment Service Provider (PSP)

A payment service provider (PSP) offers an all-in-one solution that bundles gateways, processing, and merchant accounts into a single platform.

PSPs are often used by small businesses due to their simplified onboarding.

However, traditional merchant account setups can offer greater pricing transparency and flexibility for growing businesses.

PCI DSS Compliance

The Payment Card Industry Data Security Standard (PCI DSS) establishes security requirements for businesses that handle cardholder data.

PCI compliance helps protect against data breaches and fraud.

Payment gateways can help reduce the merchant’s PCI compliance scope by securely handling card data.

T–Z Terms

Tokenization

Tokenization replaces sensitive card information with a unique digital token.

The token can be stored and used for recurring transactions without exposing the actual card number.

Benefits include:

-

improved security

-

easier recurring billing

-

reduced PCI compliance burden

Transaction Lifecycle

The payment transaction lifecycle includes multiple stages:

-

transaction initiation

-

authorization

-

clearing

-

settlement

-

funding

Understanding this lifecycle reinforces how do payment gateways work and helps merchants diagnose payment issues.

How to Integrate Payment Gateways Into Your Business

Integrating a payment gateway into your business depends on your sales channels and technical infrastructure.

Common integration options include:

API integrations

Developers connect directly to the gateway using custom code.

Hosted checkout pages

Customers are redirected to a secure payment page managed by the gateway.

eCommerce plugins

Platforms such as Shopify, WooCommerce, and Magento offer built-in gateway integrations.

Merchants should evaluate several factors before implementing a gateway:

-

transaction fees and pricing transparency

-

security and PCI compliance features

-

fraud prevention tools

-

reporting capabilities

-

scalability for business growth

Choosing the right integration method ensures smooth payment experiences for customers.

Choosing the Right Payment Gateway Partner

Not all payment gateways are built the same.

Merchants should evaluate several criteria before selecting a payment provider:

Security and compliance

Gateways must meet PCI DSS requirements and implement strong encryption protocols.

Approval rates

A well-optimized gateway can improve authorization rates and reduce declined transactions.

Scalability

Your payment infrastructure should support future growth, new payment methods, and international expansion.

Reporting and analytics

Detailed transaction reporting helps merchants track performance and manage costs.

Businesses looking for scalable payment infrastructure can explore BAMS payment gateway solutions designed for merchants across multiple industries.

Conclusion: Turning Payment Knowledge Into Smarter Decisions

The digital payment ecosystem can appear complex at first, but understanding its core components empowers merchants to make smarter business decisions.

Learning how do payment gateways work helps businesses:

-

reduce payment processing costs

-

prevent fraud and chargebacks

-

maintain PCI compliance

-

improve transaction approval rates

This glossary provides a foundational reference for merchants navigating the modern payment landscape.

As your business grows, having the right payment technology partner becomes increasingly important.

With advanced payment gateway solutions, security tools, and transparent pricing, BAMS helps merchants simplify payment processing and scale confidently in the evolving digital economy.