Surcharge vs Convenience Fee: A Guide for eCommerce

How to legally pass credit card processing costs to customers without hurting sales

Understanding the difference between a surcharge vs convenience fee for eCommerce is critical for businesses trying to reduce rising credit card processing costs. Learn the legal and strategic differences between surcharges and convenience fees. This guide covers state compliance, implementation best practices, and how to protect margins without alienating customers.

TL;DR

- Processing fees hit record highs – Average credit card swipe fees reached 2.35% according to Visa merchant fee documentation.

- Surcharges and convenience fees aren’t interchangeable – Surcharges apply to credit card payment methods; convenience fees apply to alternative payment channels. Using the wrong term creates compliance risk.

- 34% of small businesses now surcharge – But customer satisfaction drops 24 points for merchants who add fees, so weigh the tradeoffs carefully.

- Negotiate your processor markup – Interchange and assessment fees are fixed, but your processor’s cut is negotiable, especially with volume and competitive quotes.

- Alternatives exist beyond surcharging – Cash discount programs, minimum purchase requirements, and encouraging debit payments can reduce costs without the customer friction of surcharges.

What This Guide Covers

This guide breaks down the real differences between surcharges and convenience fees, two strategies that can dramatically change how much you pay to accept credit cards. You’ll learn exactly when each approach makes legal and financial sense for your business.

By the end, you’ll understand how to evaluate whether passing processing costs to customers fits your brand, which compliance requirements apply to your state, and how to implement fee strategies without damaging customer relationships. This guide is for eCommerce managers and business owners processing enough volume that a 0.5% difference in fees meaningfully impacts your bottom line.

We won’t cover every payment method or dive into cryptocurrency. The focus stays on credit card processing fees and the strategic decisions that reduce them.

Why Processing Fee Strategy Matters Now

The cost of accepting credit cards hit record highs in 2024. Average credit card swipe fees reached 2.35%, up from 2.26% just two years earlier. That gap might sound small until you calculate it across your annual revenue.

Credit card companies collected $148.5 billion in swipe fees from U.S. merchants in 2024, a 70% increase since the pandemic. This isn’t a temporary spike. It’s a structural shift in how much it costs to do business.

For eCommerce managers dealing with delayed deposits and tight margins, these fees compound. Every transaction that costs 2.5% instead of 1.8% erodes the profit you worked to build. Meanwhile, 34% of U.S. small businesses added credit card surcharges in 2024, signaling that many merchants have decided the status quo isn’t sustainable.

The question isn’t whether processing fees affect your business. It’s whether you’re making strategic choices about them or simply absorbing costs by default.

Core Concepts: Surcharges vs. Convenience Fees

Understanding the difference between surcharges and convenience fees helps eCommerce businesses reduce payment processing costs while staying compliant with card network rules.

Misunderstanding surcharge and convenience fee rules can lead to compliance violations or customer dissatisfaction.

Before choosing a fee strategy, you need to understand what each term actually means. These aren’t interchangeable, and using the wrong one can create legal problems.

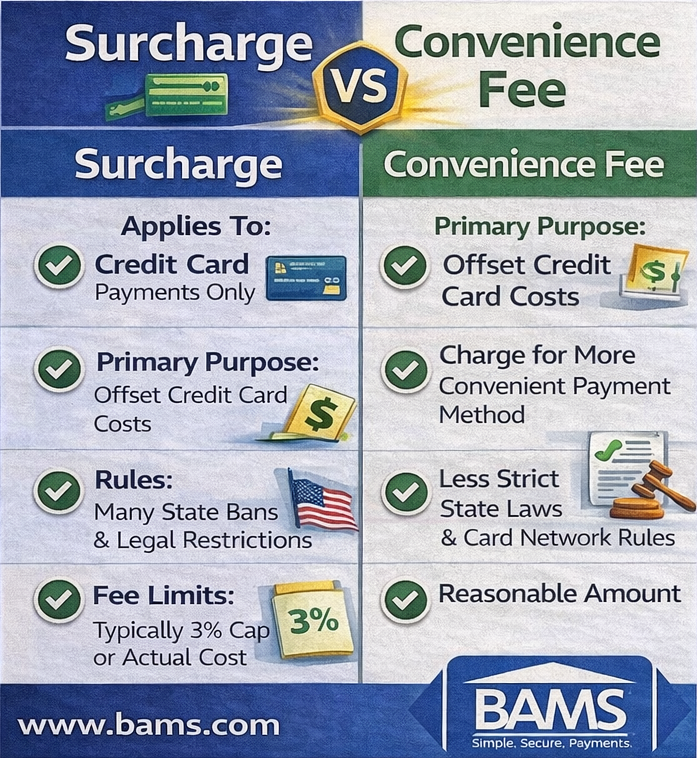

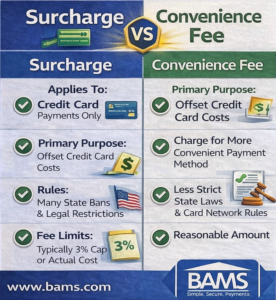

What Is a Surcharge?

A surcharge for credit card fees is an additional charge applied specifically to credit card transactions. It’s designed to offset the interchange fees and assessment fees your payment processor charges you. The customer pays more because they chose to use a credit card instead of another payment method.

Surcharges can only apply to credit cards, not debit cards. The maximum surcharge is typically capped at 3% or your actual processing cost, whichever is lower.

What Is a Convenience Fee?

A convenience fee applies when you offer an alternative payment channel that’s genuinely more convenient for the customer. Think of a utility company that normally accepts checks by mail but offers online payment for a fee. The fee covers the convenience of using a non-standard channel.

The key distinction in the convenience fee vs surcharge debate: convenience fees relate to the payment channel, while surcharges relate to the payment method.

Why the Distinction Matters

Card networks like Visa and Mastercard have strict rules governing merchant surcharges and fee disclosures. Mislabeling a surcharge as a convenience fee, or applying either incorrectly, can result in fines or loss of your merchant account. Several states also prohibit surcharges entirely, making compliance a genuine operational concern.

The Strategic Framework for Reducing Processing Costs

Reducing credit card processing fees isn’t a single decision. It’s a system of choices that work together. Here’s the framework:

- Audit: Understand exactly what you’re paying now

- Evaluate: Assess which fee strategies fit your business model

- Comply: Ensure legal and network compliance

- Implement: Execute with clear customer communication

- Optimize: Monitor results and adjust

Each stage builds on the previous one. Skipping the audit means you won’t know if your changes actually saved money. Skipping compliance means you risk penalties that dwarf any savings.

Step 1: Audit Your Current Processing Costs

Objective: Know exactly what you pay per transaction, broken down by fee type.

Most merchants know their overall processing rate but can’t identify what portion goes to interchange fees, assessment fees, or their processor’s markup. This matters because some fees are negotiable and others aren’t.

Pull your last three months of processing statements. Identify these components:

- Interchange fees (paid to the card-issuing bank, non-negotiable)

- Assessment fees (paid to card networks like Visa/Mastercard, non-negotiable)

- Processor markup (paid to your merchant services provider, negotiable)

- Monthly fees, PCI compliance fees, and chargeback fees

Average credit card processing fees for small businesses typically range from 1.5% to 3.5% per transaction depending on card type and transaction method. If you’re at the high end without premium card types or high-risk transactions, there’s likely room to negotiate or switch providers.

What to avoid: Don’t assume your current rate is competitive just because you negotiated it two years ago. Interchange rates change twice yearly, and your transaction mix evolves.

Success indicator: You can state your effective rate (total fees divided by total volume) and identify which fee components are highest.

Step 2: Evaluate Surcharge Viability for Your Business

Objective: Determine whether surcharging makes strategic and legal sense.

Surcharging can eliminate or reduce your processing costs, but it comes with tradeoffs. Customer satisfaction scores were 24 points lower for merchants adding surcharges (628 vs. 652 on a 1,000-point scale in J.D. Power’s research).

As John Cabell, managing director of payments intelligence at J.D. Power, notes: “A lot of consumers are saying that [surcharges] are influencing their payment decision.” This means surcharging might shift customers toward debit cards (which you can’t surcharge) or drive them to competitors.

Evaluate these factors:

- State legality: Connecticut, Massachusetts, and Puerto Rico prohibit surcharges. Other states have specific disclosure requirements.

- Competitive landscape: If your competitors don’t surcharge, you may lose price-sensitive customers.

- Average order value: A 3% surcharge on a $20 purchase feels different than on a $500 purchase.

- Customer relationship: B2B customers with corporate cards may accept surcharges more readily than retail consumers.

What to avoid: Don’t implement surcharges without checking your state’s current laws. Regulations change, and what was prohibited last year may now be permitted (or vice versa).

Success indicator: You’ve documented the legal requirements for your operating states and estimated the revenue impact of surcharging based on your transaction data.

Step 3: Assess Convenience Fee Applicability

Objective: Determine if convenience fees fit your payment model.

Convenience fees work only in specific situations. The payment channel must be genuinely alternative to your standard method. For most eCommerce businesses, online payment is the standard channel, which means convenience fees typically don’t apply.

Convenience fees make sense when:

- Your primary business accepts payment in person or by mail

- You offer phone or online payment as an added convenience

- The fee applies to all card types in that channel, not just credit cards

For eCommerce-native businesses, this option rarely fits. If online payment is your default (and for most eCommerce operations, it is), labeling a fee as a “convenience fee” misrepresents the transaction and violates card network rules.

What to avoid: Don’t use “convenience fee” as a workaround for surcharge restrictions. Card networks audit this, and the penalties aren’t worth the risk.

Success indicator: You’ve determined whether convenience fees legally apply to your business model, or confirmed they don’t and moved on to other strategies.

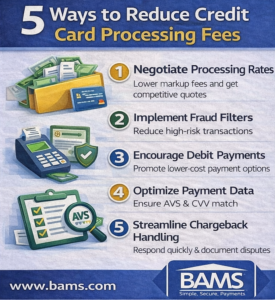

Step 4: Negotiate with Your Payment Processor

Objective: Reduce the negotiable portion of your processing costs.

Interchange and assessment fees are set by card networks. You can’t negotiate them. But your processor’s markup? That’s entirely negotiable, especially if you have leverage.

Leverage comes from:

- Volume: Higher monthly processing volume means more revenue for processors, giving you negotiating power.

- Low chargebacks: A clean history signals lower risk.

- Competitive quotes: Get offers from other merchant services providers before negotiating.

- Contract timing: Negotiate when your contract is up for renewal.

Ask your processor about interchange-plus pricing, which separates the interchange fee from their markup. Transparent pricing structures like the BAMS Merchant Account Pricing page explain exactly how interchange and processor markups work. This transparency helps you see exactly what you’re paying for. Avoid tiered pricing models that obscure the true cost of each transaction.

What to avoid: Don’t accept the first rate offered. Processors expect negotiation, and the initial quote often includes room to move.

Success indicator: You’ve received quotes from at least two processors and negotiated your current rate down or switched to a more competitive provider.

Step 5: Implement with Clear Customer Communication

Objective: Execute your fee strategy without damaging customer trust.

If you decide to surcharge, transparency isn’t optional. Card network rules require disclosure at the point of entry (your website’s homepage or store entrance) and at the point of sale (checkout).

Effective disclosure includes:

- Clear signage or website notice before checkout

- The exact surcharge percentage (not just “a fee may apply”)

- Explanation that debit cards aren’t surcharged

- The surcharge as a separate line item on receipts

65% of U.S. credit cardholders encountered higher prices due to merchant surcharges in 2025. Customers are increasingly aware of this practice. Surprising them at checkout damages trust more than the fee itself.

You must also notify the card networks before implementing surcharges. Visa and Mastercard require 30 days advance notice. Your payment processor can guide you through this requirement.

What to avoid: Don’t bury surcharge disclosure in fine print. Customers who feel deceived leave negative reviews and dispute charges.

Success indicator: Your surcharge disclosure appears clearly before checkout, on receipts, and you’ve filed required notifications with card networks.

Step 6: Explore Alternative Cost Reduction Strategies

Merchants can lower credit card processing costs by negotiating processor markup, encouraging debit payments, and optimizing payment data to qualify for lower interchange rates.

Many merchants lower processing costs significantly by combining several of these strategies rather than relying on a single approach.

Objective: Reduce processing costs through methods that don’t involve customer-facing fees.

Surcharges aren’t the only path to lower costs. Consider these alternatives:

Cash discount programs: Instead of adding a fee for credit cards, offer a discount for cash or debit. This achieves similar economics with different customer psychology. A “3% cash discount” feels like a reward rather than a penalty.

Minimum purchase requirements: Card networks allow minimum purchase amounts up to $10 for credit cards. If small transactions erode your margins, this sets a floor.

Encourage debit and ACH: Debit card interchange fees are regulated and typically lower than credit. ACH transfers cost even less. Incentivizing these methods shifts your payment mix toward lower-cost options.

Optimize for lower interchange categories: Some transactions qualify for lower interchange rates based on how they’re processed. Ensure your payment gateway captures all required data (like AVS and CVV) to qualify for the best rates.

What to avoid: Don’t implement minimum purchase requirements for debit cards. The Durbin Amendment prohibits this.

Success indicator: You’ve evaluated at least two alternatives to surcharging and implemented the ones that fit your customer base.

Step 7: Monitor and Optimize Continuously

Objective: Track the impact of your fee strategy and adjust based on data.

Any fee strategy needs ongoing measurement. Track these metrics monthly:

- Effective processing rate (total fees / total volume)

- Payment method mix (credit vs. debit vs. other)

- Cart abandonment rate (especially if you implemented surcharges)

- Customer feedback and reviews mentioning fees

- Chargeback rates

If surcharges drive significant cart abandonment, the savings may not justify the lost revenue. If cash discount programs shift customers to debit without complaints, consider expanding the incentive.

Review your processing statements quarterly. Interchange rates change in April and October. Your transaction mix evolves. What worked six months ago may need adjustment.

What to avoid: Don’t set and forget. The merchants who save the most on processing treat it as an ongoing optimization, not a one-time project.

Success indicator: You have a dashboard or report tracking your key payment metrics, and you review it at least quarterly.

Common Mistakes That Undermine Fee Strategies

Even well-intentioned fee strategies fail when merchants make these errors:

Surcharging debit cards: This violates card network rules and can result in fines or account termination. Your system must distinguish between credit and debit transactions.

Exceeding surcharge caps: The maximum is typically 3% or your actual cost, whichever is lower. Charging more invites disputes and compliance issues.

Ignoring state law changes: Surcharge legality varies by state and changes over time. What’s permitted in Texas may be prohibited in Connecticut. Verify before you implement.

Poor disclosure: Customers who discover fees at checkout feel ambushed. This generates chargebacks, negative reviews, and lost repeat business.

Focusing only on rate: A low processing rate means nothing if your provider has slow deposits, poor chargeback support, or hidden monthly fees. Total cost of ownership matters more than the headline rate.

What to Do Next

Start with the audit. Pull your last three processing statements and calculate your effective rate. Identify the breakdown between interchange, assessments, and processor markup.

Once you know what you’re actually paying, the strategic choices become clearer. You might find that negotiating your processor markup saves more than surcharging ever could. Or you might discover that your customer base would accept a transparent surcharge without significant pushback.

This isn’t a decision you need to make this week. Use this guide as a reference as you gather data and evaluate options. The goal is sustainable cost reduction that supports your business growth, not a quick fix that creates new problems.

If you’re processing significant volume and haven’t reviewed your merchant services agreement recently, that’s the logical first step. A modern payment processor can help you identify savings opportunities you might miss on your own, from interchange optimization to transparent pricing structures that eliminate surprises.

Frequently Asked Questions

What are credit card processing fees and why do merchants pay them?

Credit card processing fees are charges merchants pay every time a customer uses a card. These fees compensate the card-issuing bank (interchange), the card network like Visa or Mastercard (assessments), and your payment processor (markup). Merchants pay because accepting cards increases sales and customer convenience, but the cost typically ranges from 1.5% to 3.5% per transaction.

How are credit card processing fees determined?

Interchange fees are set by card networks based on factors like card type (rewards cards cost more), transaction type (card-present vs. online), and merchant category. Assessment fees are flat percentages set by Visa and Mastercard. Your processor’s markup is negotiable and varies based on your volume, risk profile, and the pricing model you choose.

Can I add a surcharge for credit card fees in any state?

No. Connecticut, Massachusetts, and Puerto Rico currently prohibit credit card surcharges. Other states have specific disclosure requirements. Laws change, so verify current regulations for every state where you operate before implementing surcharges. Your payment processor can help confirm compliance requirements.

What’s the difference between a convenience fee vs surcharge?

A surcharge applies specifically to credit card transactions to offset processing costs. A convenience fee applies when you offer an alternative payment channel (like online payment when your standard is in-person). Most eCommerce businesses can’t use convenience fees because online payment is their standard channel, not an alternative convenience.

How can businesses minimize their credit card processing fees?

Start by auditing your current costs and negotiating with your processor. Consider interchange-plus pricing for transparency. Explore cash discount programs, encourage debit card use, and ensure your payment gateway captures all data needed to qualify for lower interchange categories. Surcharging is an option but comes with customer satisfaction tradeoffs.

When do interchange fees change, and what factors influence them?

Visa and Mastercard update interchange rates twice yearly, typically in April and October. Factors include card type (premium rewards cards have higher rates), how the transaction is processed (card-present vs. card-not-present), merchant category code, and whether you meet specific data requirements. Staying current on these changes helps you optimize your effective rate.

Sources

- https://usa.visa.com/support/small-business/regulations-fees.html

- https://www.axios.com/local/raleigh/2025/12/10/credit-card-fee-surcharge-legal-north-carolina

- https://www.mastercard.us/en-us/business/overview/support/merchant-surcharge-rules.html

- https://www.jdpower.com/business/press-releases/2025-us-credit-card-satisfaction-study