Chargeback Fees: The Hidden Cost Draining Small Businesses

Why transparent pricing for processing is no longer optional—and how to protect your margins before disputes hit

Learn why chargeback fees catch most ecommerce managers off guard and how information asymmetry in credit card processing costs small businesses more than they realize. Discover what transparent pricing actually looks like.

TL;DR

- Chargeback costs are exploding – Rates jumped 222% in one year, and each $1 lost actually costs you $3.75 to $4.61 in total expenses

- Hidden fees are the real problem – Most processors bury chargeback costs in fine print, making it impossible to budget accurately

- Your processor’s incentives matter – If they profit from dispute fees, they have no reason to help you prevent chargebacks

- Calculate your true processing cost – Add all fees including chargebacks and divide by volume; most businesses pay 30-50% more than they think

The Hidden Cost of Chargeback Fees After the Sale

You made the sale. The customer got their product. Then, weeks later, a chargeback lands in your inbox. Suddenly you owe $190 for a transaction you thought was done.

This is the moment most ecommerce managers realize their payment processor never explained what would happen next. The transaction fee was clear. The chargeback fee? Buried somewhere in page 47 of the terms.

I believe this information asymmetry is the real problem with credit card processing for small businesses. And it’s costing you more than you know.

The Pricing Model Nobody Questions

Most businesses accept that processing fees are just part of doing business. Interchange fees go to the card networks. Assessment fees go to Visa and Mastercard. Your payment processor takes a cut. Fine.

The industry trained us to focus on that headline rate. “2.9% plus 30 cents” became the number everyone optimizes around. Processors compete on fractions of a percentage point while the real costs hide in plain sight.

Chargeback fees, PCI compliance fees, monthly minimums, batch fees, statement fees. These line items add up quietly. When a dispute hits, that $15 subscription service suddenly costs you $50 in fees alone, before you even count the lost revenue. Mastercard notes that merchants often incur $15 to $70 in operational costs for every dispute, on top of the refunded transaction amount and other processing fees.

This model worked when chargebacks were rare. They’re not rare anymore.

Transparent Pricing for Processing Isn’t Optional Anymore

Here’s what I actually believe: the processors who hide chargeback costs are the ones who profit most when disputes spike.

Think about the incentive structure. If your processor charges $25 per chargeback and never mentions it upfront, they benefit when disputes increase. They have no reason to help you prevent them.

Transparent pricing for processing changes this dynamic entirely. When you see every fee before you sign, you can calculate your true cost of accepting credit cards. Merchants working with providers that offer transparent interchange plus pricing models can clearly see the processor markup applied to each transaction.

The Numbers That Should Keep You Up at Night

A single chargeback can cost small businesses far more than the original transaction once fees, lost product, and operational time are included.

Businesses can significantly reduce chargebacks by improving billing transparency, fraud screening, and dispute response processes. Let me show you why this matters right now.

Chargeback rates jumped 222% between Q1 2023 and Q1 2024, from 0.15% to 0.47%. That’s not a gradual trend. That’s a structural shift in how consumers interact with online purchases.

The total cost is staggering. Chargebacks will drain $33.79 billion from ecommerce in 2025, climbing to $41.69 billion by 2028. Your slice of that pie depends entirely on how prepared you are.

Here’s the number that changed how I think about this: for every $1 lost to a chargeback, businesses lose $3.75 to $4.61 in total costs. That multiplier has increased 37% since 2021.

A $50 disputed transaction doesn’t cost you $50. It costs you $187 to $230 when you factor in the chargeback fees, the operational time, the lost product, and the hit to your merchant account standing.

What Proactive Defense Actually Looks Like

Businesses can significantly reduce chargebacks by improving billing transparency, fraud screening, and dispute response processes.

Implementing these chargeback prevention strategies can reduce disputes and protect your revenue over time. I’ve watched businesses take two different approaches to this problem.

According to the National Retail Federation, ecommerce retailers report that payment fraud and chargebacks can account for over 3% of online orders in some sectors, showing how disputes are becoming a structural cost of digital commerce

The first group treats chargebacks as random bad luck. They pay the fees when disputes arrive, occasionally fight back, and hope next month is better. They win about 45% of the disputes they contest, matching the industry average.

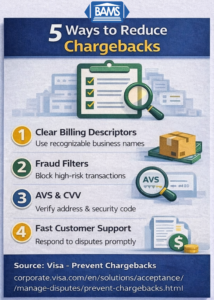

The second group builds systems. They implement fraud filters that flag suspicious transactions before shipping. They use clear billing descriptors so customers recognize charges. They respond to disputes within 24 hours with complete documentation.

Small businesses using basic fraud prevention tools reduce chargebacks by 10 to 15%. That’s not a magic bullet, but on a $500,000 annual revenue with a 0.95% chargeback rate (the ecommerce average), you’re looking at roughly $4,750 in disputed transactions. Cut that by 15% and you save over $700 in direct losses, plus another $2,600 in associated costs.

The difference between these two approaches isn’t sophistication or budget. It’s whether your processor told you chargebacks were coming and gave you tools to fight them.

Why Your Processor’s Incentives Matter

If your current merchant services provider profits from chargeback fees, ask yourself: why would they help you avoid them?

This isn’t conspiracy thinking. It’s basic economics. When chargeback fees range from $10 to $50 per dispute, a processor handling thousands of merchants can generate significant revenue from disputes alone. Prevention tools cost money to build and maintain. Reactive fee collection costs almost nothing.

The processors who invest in proactive chargeback defense are betting on a different model. They’re betting that merchants who stay in business and grow their volume are worth more than merchants who bleed out from dispute fees.

That’s the question to ask when evaluating any payment processor: do they make more money when you succeed, or when you struggle?

A Different Way to Think About Processing Costs

Stop optimizing for the lowest headline rate. Start optimizing for total cost of payment acceptance.

That means adding up your interchange fees, your assessment fees, your processor markup, your chargeback fees, your PCI compliance costs, and the operational time you spend managing disputes. Divide by your total transaction volume. That’s your real rate.

For most ecommerce businesses I’ve talked to, this number is 30 to 50% higher than the rate they thought they were paying. The gap is almost entirely chargeback-related costs they never budgeted for.

When you frame it this way, transparent pricing for processing isn’t just nice to have. It’s the only way to actually know what you’re paying.

The Shift That’s Coming

Chargeback volumes aren’t going back down. Consumers learned during the pandemic that disputing charges is easy. Card networks made it even easier. The 222% increase isn’t a spike; it’s a new baseline.

Businesses that treat chargeback fees as a surprise will keep getting surprised. Businesses that demand transparency, build prevention systems, and partner with processors who share their incentives will turn payments into something predictable. Learn more about how modern merchant services providers help businesses manage chargebacks and reduce processing costs.

The question isn’t whether you can afford proactive chargeback defense. It’s whether you can afford to keep paying $190 every time a customer decides to dispute instead of return.

Frequently Asked Questions

What are credit card processing fees?

Processing fees include interchange fees paid to card-issuing banks, assessment fees paid to card networks like Visa and Mastercard, and markups charged by your payment processor. Together, these typically range from 2% to 4% of each transaction.

How can businesses minimize their credit card processing fees?

Focus on total cost, not just the headline rate. Implement fraud filters to reduce chargebacks, negotiate transparent pricing that shows all fees upfront, and choose a processor that offers proactive dispute defense rather than just reactive fee collection.

Why do chargeback fees vary so much between processors?

Processors set their own chargeback fees, typically between $10 and $50 per dispute. The variation reflects different business models. Some processors profit from disputes while others invest in prevention tools that reduce overall costs for merchants.

Sources