PCI Compliance Fees: What Merchants Should Actually Be Paying

Why the small line item you never question says everything about your merchant services relationship

Learn why PCI compliance fees are the clearest indicator of whether your payment processor treats you as a partner or a revenue source. Discover what you should actually receive for this charge and how to evaluate providers based on transparency.

TL;DR

- PCI compliance fees reveal processor transparency – How clearly a provider explains this small charge predicts how they’ll handle everything else.

- You should pay $70 to $120 annually – If you’re paying $100 monthly, ask exactly what services justify the premium.

- Non-compliance costs far more than compliance – Penalties reach $100,000 per month, making unclear “compliance support” a genuine business risk.

- Ask four specific questions – What’s covered, how often are scans run, what SAQ support exists, and is breach protection included.

The Fee You’re Paying Without Knowing Why

Somewhere in your monthly processing statement, there’s a line item you’ve probably never questioned. It’s small enough to ignore, vague enough to skip over, and persistent enough to drain thousands from your business over time.

I’m talking about PCI compliance fees — one of the most misunderstood costs in payment processing. And if you can’t explain exactly what you’re getting for that charge, you’re not alone. Most ecommerce managers can’t. That’s not an accident.

Why Nobody Questions the Compliance Line Item

The conventional wisdom around PCI compliance fees goes something like this: it’s a necessary cost of doing business, everyone pays it, and your processor handles the complicated security stuff so you don’t have to.

This framing worked for years. Payment security is genuinely complex.

Only 14.3% of organizations achieved full PCI compliance, which suggests most businesses prefer outsourcing payment security instead of managing it internally.

But here’s what changed: processors figured out that “compliance” sounds important enough that merchants won’t push back. So fees crept up. Services stayed vague. And a charge that should cost $79 to $120 per year somehow became $100 per month at some providers.

The Real Problem Isn’t the Fee (It’s the Fog)

Here’s what I actually believe: PCI compliance fees are the clearest indicator of whether your merchant services provider treats you as a partner or a revenue source. The fee itself matters less than what you get for it and whether anyone can explain it clearly.

What Transparent Compliance Actually Looks Like

Typical PCI compliance costs for merchants include annual PCI program fees, vulnerability scanning, SAQ completion support, and ongoing compliance monitoring.

Costs can vary depending on your provider, but transparent processors clearly explain every service included in the PCI program.

Let me break down what you should be paying and receiving.

Card service providers typically charge $70 to $120 annually for PCI compliance programs. That covers access to self-assessment questionnaires, basic vulnerability scanning tools, and documentation support. If you’re paying significantly more, ask what additional services justify the premium.

For small ecommerce operations processing under 20,000 transactions annually, your total PCI-related costs (including scans, training, and provider fees) should land between $1,000 and $10,000 per year. Approved Scanning Vendor scans run $500 to $2,000 annually, and routine processor fees add another $10 to $100 monthly.

Here’s the pattern I’ve observed: processors who can’t itemize these costs clearly usually can’t deliver the services clearly either. The fog is the feature.

One ecommerce manager I spoke with discovered she was paying $89 monthly for “PCI compliance support” that amounted to a PDF guide and an annual reminder email. Her previous processor had charged $79 per year for the same thing, plus quarterly vulnerability scans and a dedicated support line.

Same label. Wildly different value. The only way to spot the difference is to ask uncomfortable questions.

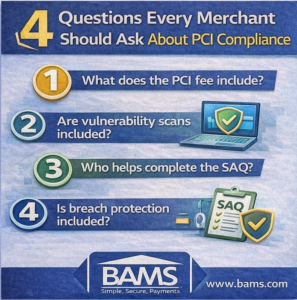

The Questions That Reveal Everything

Merchants should ask payment processors exactly what services their PCI compliance fee includes, such as vulnerability scans, SAQ support, and breach protection.

Clear answers to these questions often reveal whether a processor prioritizes merchant security or simply adds compliance fees as a revenue stream.

When evaluating any merchant services provider, ask these directly:

- What specific services does your PCI compliance fee cover?

- How often do you run vulnerability scans, and who performs them?

- What happens if I need help completing my Self-Assessment Questionnaire?

- Is there a separate charge for breach protection or is it included?

Providers who answer these questions quickly and specifically are telling you something important about how they operate. Providers who deflect or generalize are telling you something too.

The Stakes Are Higher Than You Think

If this perspective is right, then the PCI compliance fee isn’t just a line item to negotiate. It’s a diagnostic tool for your entire processor relationship.

Consider what unclear compliance support actually costs. Non-compliance penalties can reach $100,000 per month, with card networks adding up to $90 in additional transaction fees. A data breach without proper compliance documentation exposes you to fines between $500 and $500,000.

The businesses that get burned aren’t the ones who refused to pay compliance fees. They’re the ones who paid without understanding what they were buying.

A Better Way to Think About Processing Costs

Here’s the reframe: stop treating compliance fees as overhead and start treating them as a transparency test.

A processor who can explain your PCI costs clearly will probably explain your interchange fees clearly too. Working with a provider that offers transparent merchant account pricing helps merchants understand every processing cost before they sign an agreement.. They’ll likely be upfront about assessment fees, chargeback fees, and the actual merchant discount rate you’re paying. Clarity compounds.

The journey to transparent pricing doesn’t start with negotiating rates. It starts with understanding the charges that most businesses never question. PCI compliance fees are the canary in the coal mine.

What This Means for Your Next Conversation

The best merchant services relationships are built on specificity, not promises. When you can see exactly what you’re paying and exactly what you’re getting, you can make real decisions about value.

Your processor should make compliance easier, not more mysterious. If they can’t do that for a $100 annual fee, they probably can’t do it for the thousands you’re spending on credit card processing for small businesses either.

Demand the clarity. Businesses evaluating payment processors can also review the merchant services solutions offered by BAMS to better understand transparent pricing and compliance support options.

Frequently Asked Questions

What are PCI compliance fees actually supposed to cover?

Legitimate PCI compliance fees cover vulnerability scanning, self-assessment tools, documentation support, and sometimes breach protection insurance. If your provider can’t itemize these services, you’re likely overpaying for unclear value.

How much should small businesses expect to pay for PCI compliance?

Most small ecommerce businesses should pay $70 to $120 annually in processor fees, plus $500 to $2,000 for required scans. Total yearly costs typically range from $1,000 to $10,000 depending on transaction volume and security needs.

Can I negotiate PCI compliance fees with my processor?

Yes, but negotiating the fee matters less than understanding what it includes. Ask for an itemized breakdown first, then compare against what other providers offer for similar pricing.

Sources

- https://www.pcisecuritystandards.org/merchants/

- https://corporate.visa.com/en/resources/security-compliance.html

- https://www.mastercard.com/global/en/business/cybersecurity-fraud-prevention/site-data-protection-pci.html

- https://www.sisainfosec.com/blogs/pci-dss-compliance-cost-in-2025-everything-you-need-to-know/