Interchange Plus vs Surcharge eCommerce Comparison

How each model affects your transaction costs, customer experience, and bottom line

Learn which payment processing model fits your eCommerce business. This comparison breaks down fee transparency, customer impact, and true cost differences between interchange-plus and surcharge programs.

TL;DR

- Interchange-plus pricing shows every fee component so you can see interchange, assessments, and processor markup separately.

- Surcharge programs shift costs to customers, which can increase cart abandonment, add compliance complexity, and strain customer relationships.

- Legal restrictions limit surcharging because some jurisdictions restrict or prohibit it, and card network rules require disclosures and registration.

- Interchange-plus works better for most eCommerce businesses because the transparency supports optimization and customers do not see surprise fees at checkout.

- Start with an audit of your current costs so you can compare your effective rate against interchange-plus alternatives for your volume level.

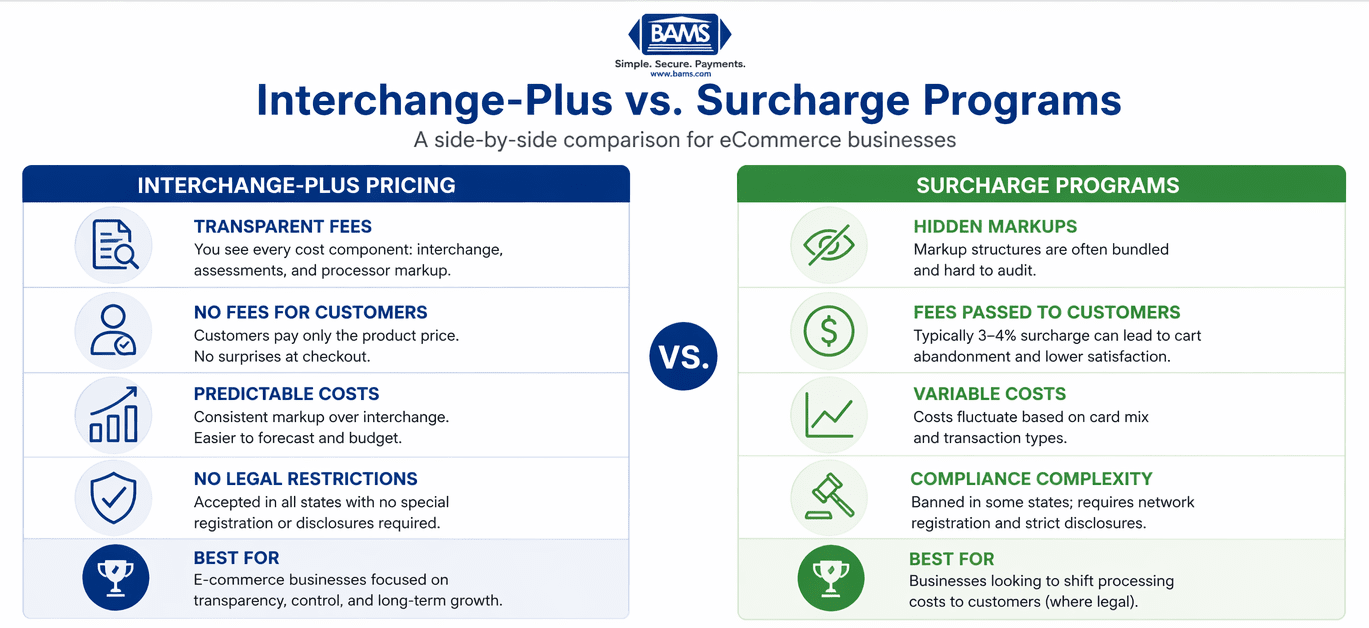

Interchange-Plus Pricing vs. Surcharge Programs: What eCommerce Managers Need to Know

You’re processing thousands of transactions monthly, but your statement reads like a foreign language. Fees appear from nowhere. Your effective rate fluctuates without explanation. Sound familiar?

This comparison breaks down two fundamentally different approaches to managing credit card processing costs: interchange-plus pricing and surcharge programs for credit cards. Both promise savings, but they work in opposite ways and carry different risks for your business.

If you manage payments for an established eCommerce operation, understanding these models is not optional. It is the difference between predictable costs you can budget around and monthly surprises that erode your margins.

Quick Verdict: Which Model Fits Your Business?

A side-by-side comparison of interchange-plus pricing and surcharge programs across transparency, customer experience, and cost predictability.

Choose interchange-plus pricing if you want complete visibility into every fee component, predictable costs you can forecast, and full control over your customer experience without passing fees to buyers.

Choose surcharge programs if you’re comfortable shifting credit card costs to customers, operate in a state where surcharging is legal, and your customer base will not push back against the added fee at checkout.

For most eCommerce businesses prioritizing customer experience and long-term growth, interchange-plus delivers better value. Here’s why.

| Criterion | Interchange-Plus | Surcharge Programs | Winner |

|---|---|---|---|

| Fee Transparency | Complete breakdown of every cost | Often opaque markup structures | Interchange-Plus |

| Customer Experience | No added fees at checkout | 3% to 4% fee surprises customers | Interchange-Plus |

| Cost Predictability | Consistent markup over interchange | Variable based on card mix and customer response | Interchange-Plus |

| Legal Complexity | No special restrictions | Restricted or prohibited in some jurisdictions | Interchange-Plus |

| Immediate Cost Reduction | Gradual optimization | Shifts costs to customers | Surcharge Programs |

| Cart Abandonment Risk | None from added payment fees | Meaningful risk when fees appear late in checkout | Interchange-Plus |

How We’re Evaluating These Models

This comparison focuses on six dimensions that matter most to eCommerce managers handling substantial transaction volumes:

- Fee transparency: Can you trace every dollar charged to a specific cost component?

- Customer experience impact: Does the model affect conversion rates or customer satisfaction?

- Cost predictability: Can you accurately forecast monthly processing expenses?

- Legal and compliance burden: What regulatory requirements apply?

- Implementation complexity: How difficult is setup and ongoing management?

- Long-term scalability: Does the model grow efficiently with your business?

We are weighting transparency and customer experience heavily because eCommerce businesses live and die by conversion rates and repeat purchases.

Fee Transparency: The Core Difference

How Interchange-Plus Works

Interchange-plus pricing separates your processing costs into three visible components: the interchange fee paid to the card-issuing bank, the card network assessment paid to Visa or Mastercard, and your processor’s markup. You see each piece on every statement.

For example, a transaction might show: 1.80% interchange + 0.13% assessment + 0.25% processor markup = 2.18% total.

This visibility lets you identify exactly where your money goes. When a transaction costs more, you know whether it is because the customer used a rewards card or because your processor raised their markup.

How Surcharge Programs Work

Surcharge programs take a different approach. Instead of optimizing what you pay, they shift credit card fees directly to customers. When someone pays with credit, they see an additional 3% to 4% fee added at checkout.

The transparency problem is that many surcharge programs bundle their own markup into the “credit card fee” passed to customers. You may tell customers they are paying the processing cost, but you cannot always verify that is true.

Verdict: Interchange-Plus Wins on Transparency

If you want to know exactly what you’re paying and why, interchange-plus is the only model that delivers. Surcharge programs often obscure the true cost structure, making it impossible to audit whether you’re getting fair rates. For businesses serious about optimizing payments, using a reliable payment gateway supports better visibility and control over processing costs.

Customer Experience: The Hidden Cost of Surcharging

Interchange-Plus: Invisible to Customers

With interchange-plus pricing, your customers see one price. They pay it. Transaction complete. The processing model stays behind the scenes, creating zero friction in your checkout flow.

Your pricing strategy remains yours to control. You can build processing costs into your margins, offer free shipping thresholds, or run promotions without worrying about fee surprises undermining customer trust.

Surcharge Programs: Checkout Friction

Surcharging adds a visible fee at the moment customers are most likely to abandon their carts. A $100 purchase suddenly becomes $104. For customers who have already compared prices and chosen your store, this can feel like a bait-and-switch.

The psychological impact grows in eCommerce. Unlike in-person transactions, online shoppers can close the tab and find alternatives in seconds. Cart abandonment rates tend to rise when unexpected fees appear at checkout.

Verdict: Interchange-Plus Protects Conversions

eCommerce businesses spend significant resources driving traffic and optimizing funnels. Introducing a surprise fee at checkout can undermine that investment. Unless your customers have no alternatives, surcharging creates friction that may cost more in lost sales than it saves in processing fees.

Cost Predictability: Budgeting with Confidence

Interchange-Plus: Consistent Markups, Variable Base

Your processor’s markup stays fixed. The interchange portion varies by card type, but within predictable ranges. According to the Federal Reserve’s 2023 Interchange Fee Report, average interchange fees for regulated debit transactions were $0.24 for single-message networks and $0.22 for dual-message networks.

Over time, your card mix stabilizes. You can forecast monthly processing costs within a tighter range, which makes budgeting easier. If costs spike unexpectedly, you can trace the cause to specific transaction types or processor behavior.

Surcharge Programs: Shifted Costs, Hidden Variability

Surcharging appears to eliminate cost variability by passing fees to customers. However, it introduces new unpredictability: how will customers respond, will credit card usage drop, and will you lose sales to competitors who absorb processing costs?

The program itself may also include variable components. Some surcharge providers adjust their take based on volume, card types, or other factors you cannot fully control or predict.

Verdict: Interchange-Plus Offers True Predictability

Surcharging shifts costs rather than eliminating them. The variability moves from your processing statement to your sales metrics. Interchange-plus keeps costs visible and manageable so you can optimize systematically over time.

Legal and Compliance Considerations

Card networks impose their own rules: surcharges typically can’t exceed 3% (or 4% for some networks), must be disclosed before checkout, and can’t apply to debit cards even when run as credit. According to Visa’s surcharge guidelines, merchants must also register and follow strict disclosure requirements.

Interchange-Plus: No Restrictions

Interchange-plus pricing is a straightforward business arrangement between you and your processor. No special surcharge disclosures apply. You pay for processing, the model stays transparent, and the operational burden remains relatively low.

Surcharge Programs: A Compliance Minefield

Surcharging credit cards can trigger disclosure requirements and card network rules. In addition, jurisdiction-specific restrictions can make multi-state eCommerce selling more complex. You may need systems to detect customer location, present required notices, and ensure the surcharge only applies where permitted and only to eligible payment types.

Verdict: Interchange-Plus Avoids Legal Risk

Unless you sell only in surcharge-friendly areas and have strong compliance systems, the legal complexity of surcharging can outweigh the potential savings. Interchange-plus works with less friction and fewer operational variables.

Implementation and Ongoing Management

Interchange-Plus: Simple Setup, Active Optimization

Switching to interchange-plus pricing usually means negotiating with your processor or choosing a new provider. Once the model is in place, it runs automatically. Ongoing work centers on reviewing statements, improving qualification rates, and periodically negotiating markup.

Surcharge Programs: Complex Setup, Ongoing Compliance

Implementing surcharging can require checkout changes, updated disclosures, staff training, card network notifications, and ongoing compliance reviews. You also need to monitor customer reaction and determine whether the program saves money after any lost sales are considered.

Verdict: Interchange-Plus Is Simpler to Manage

Both models require attention, but interchange-plus lets you spend more energy on optimization rather than compliance. That simpler operational footprint supports focus on growth.

Use Case Mapping: Which Model Fits Your Situation?

A simple decision framework to determine whether interchange-plus or surcharge pricing fits your business model.

If you process $50,000 or more monthly and want to reduce costs systematically, choose interchange-plus. The transparency helps you identify savings opportunities, and the volume gives you negotiating leverage on markup.

If your customers are less price-sensitive and you operate where surcharging is permitted, a surcharge program might work. This tends to fit a narrower set of businesses.

If you compete on price in a crowded market, choose interchange-plus. Added checkout fees can place you at a disadvantage against merchants that absorb processing costs.

If you sell subscriptions or recurring services, avoid surcharging. A fee accepted once may still create friction on every recurring charge, which can hurt long-term retention.

If you’re unsure about your current effective rate, start with an audit. You cannot choose the right model without knowing what you are actually paying. Divide total fees by total volume, then compare that result against interchange-plus alternatives.

What Both Models Get Wrong

Neither interchange-plus nor surcharging fully solves the broader issue that card acceptance costs remain a meaningful expense line for many merchants. In practice, both models still require operational discipline, pricing strategy alignment, and regular statement review.

Both models also assume card payments remain central. As digital wallets and alternative payment methods grow, merchants may need a broader payment strategy rather than relying on one pricing model alone.

Switching Costs and Lock-In Factors

Moving from flat-rate or tiered pricing to interchange-plus often involves relatively low switching friction. The bigger challenge is comparing proposals clearly and negotiating terms that make sense for your volume and card mix.

Switching away from a surcharge program can be more involved. You may need to update checkout logic, remove disclosures, and reset customer expectations if fees have become part of the buying process.

When switching makes sense: If your effective rate is high on a blended basis and you are processing enough volume to negotiate, it is worth exploring interchange-plus alternatives. Savings can add up quickly at scale.

Watch for lock-in factors like early termination fees, equipment commitments, and proprietary integrations. Review contracts carefully before committing to any processor, regardless of pricing model.

Final Recommendation: Transparency Wins

For eCommerce managers at established businesses, interchange-plus pricing delivers what surcharge programs promise but rarely achieve: better cost control without sacrificing customer experience.

Surcharging shifts costs rather than reducing them. It can add compliance complexity, strain customer relationships, and create unpredictable impacts on conversion rates. The apparent savings may fade once lost sales and operational overhead are considered.

Interchange-plus is not perfect. You still pay processing fees, and optimization takes ongoing attention. However, you pay with clearer visibility, more predictable markups, and no direct impact on the customer checkout experience.

Start by auditing your current costs. Calculate your effective rate. Compare it against the interchange-plus rates available to businesses your size. Then decide whether the switch makes sense and how much value it could create.

Your payment processing should be a predictable line item, not a monthly mystery. Interchange-plus makes that possible. Faster access to funds through guaranteed next-day funding can further support cash flow and operational stability.

Frequently Asked Questions

What are merchant fees and how do they work?

Merchant fees are the costs you pay to accept card payments. They usually include interchange fees paid to the issuing bank, assessment fees paid to the card network, and processor markup. With interchange-plus pricing, each component is easier to see and understand.

Which pricing model is better: interchange-plus or flat rate?

Interchange-plus is often a better fit for businesses processing higher monthly volume because it passes through actual card costs and separates processor markup. Flat-rate pricing is simpler, but it can be more expensive when your mix includes lower-cost transactions.

What are some common hidden fees associated with merchant services?

Common hidden fees include PCI compliance fees, statement fees, batch fees, monthly minimums, early termination fees, and “non-qualified” transaction surcharges. According to the PCI Security Standards Council, compliance requirements can also introduce additional operational costs if not managed properly.

Can I use surcharge programs for all payment types?

No. Surcharges do not apply universally across all payment types. Merchants need to confirm the applicable card network rules and local requirements before using them.

How can I negotiate lower merchant processing rates?

Start by calculating your effective rate. Then compare proposals from multiple providers, use your transaction volume as leverage, and ask directly for markup reductions or unnecessary fee removal.

When should I consider switching payment processors?

Consider switching if your effective rate is too high, your pricing lacks transparency, your provider will not negotiate, or you experience service issues such as delayed funding or weak support.