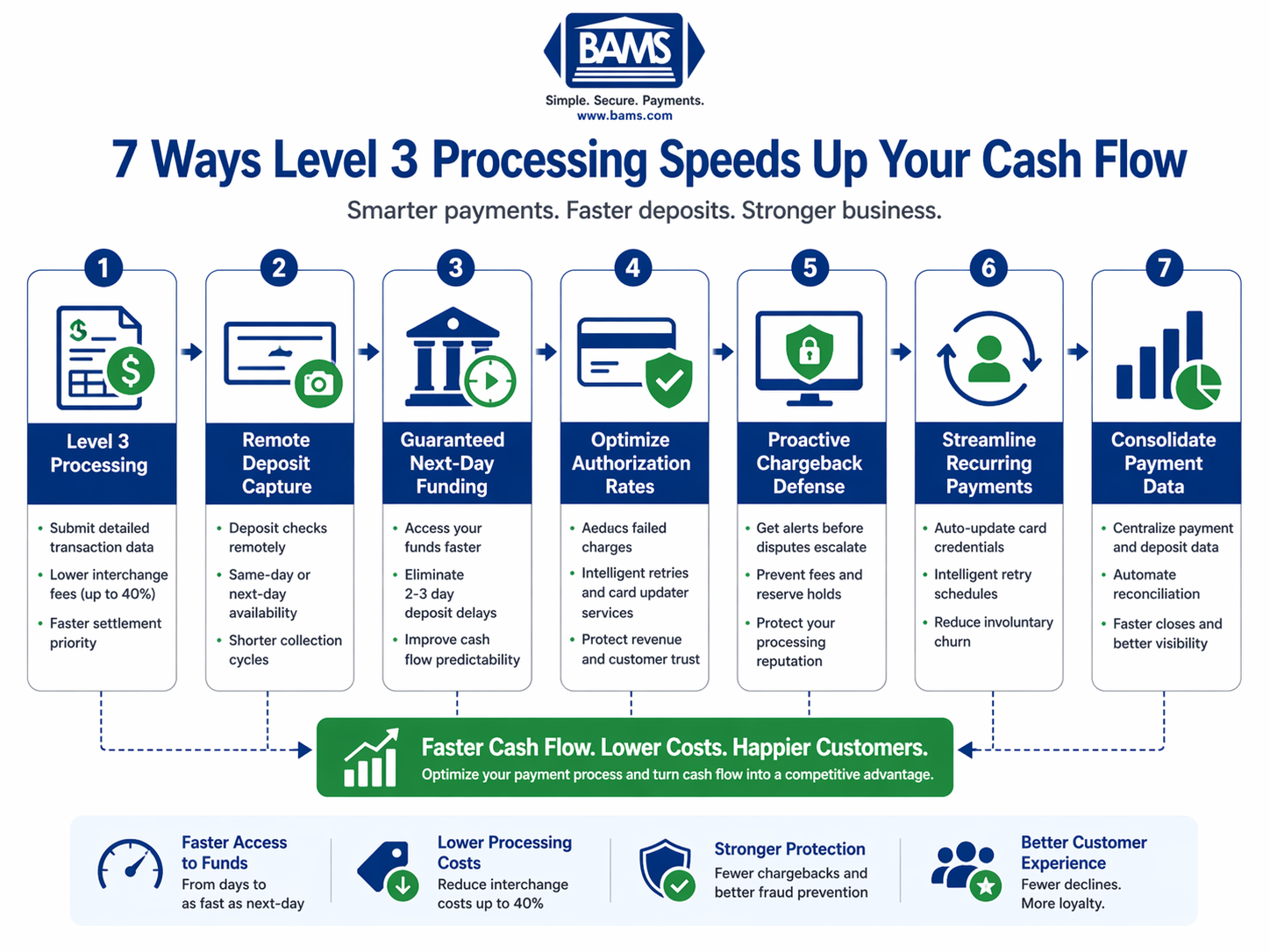

Level 3 Processing Speeds Up Cash Flow

How modern payment infrastructure helps eCommerce managers reduce deposit delays and build lasting customer loyalty

Learn how level 3 processing and remote deposit capture can cut your cash flow gaps from days to hours. This guide covers practical strategies for mid-size eCommerce businesses to modernize payments without enterprise budgets.

TL;DR

- Level 3 processing cuts costs and speeds settlement – Submitting detailed transaction data can reduce interchange costs for qualifying B2B and corporate card transactions while improving processing efficiency.

- Guaranteed next-day funding is now accessible – Competition among processors has made accelerated deposits available to mid-size businesses without enterprise volume requirements or premium pricing.

- Authorization optimization prevents invisible revenue loss – Failed charges damage customer relationships and delay deposits; card updater services and intelligent retry logic address root causes automatically.

- Proactive chargeback defense protects cash flow – Alert systems allow intervention before disputes escalate, avoiding fees, reserve holds, and the processing rate increases that follow elevated chargeback ratios.

- Start with 2-3 strategies based on your pain points – Focus on B2B processing improvements if corporate cards dominate your mix, or authorization optimization if decline rates exceed internal benchmarks.

Why Delayed Deposits Cost More Than You Think

Your eCommerce business processed $50,000 in sales last week. The money sits in limbo for 3-5 business days while your suppliers demand payment, payroll looms, and inventory needs restocking. This cash flow gap forces otherwise healthy businesses into short-term borrowing or missed opportunities.

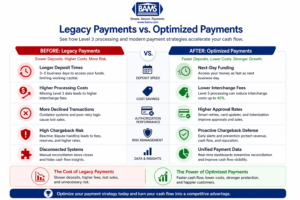

A side-by-side comparison of legacy payment systems versus optimized payment strategies, highlighting improvements in speed, cost, and cash flow.

The problem runs deeper than inconvenience. According to the Federal Reserve, interchange and routing economics remain central to how card payments move through the system, which means processing efficiency directly affects margins and cash flow planning.

Level 3 processing and modern deposit solutions have matured significantly. What once required enterprise-level resources now sits within reach of mid-size online retailers. The gap between businesses using optimized payment systems and those stuck with legacy approaches widens each quarter.

What This Guide Delivers

This guide targets eCommerce managers at established online businesses handling meaningful transaction volume who need faster access to funds without sacrificing security or inflating costs. You will not find generic advice about “accepting more payment methods” or surface-level tips.

Each strategy addresses a specific bottleneck in the deposit-to-cash timeline. We exclude tactics requiring dedicated finance teams or enterprise software budgets. The focus stays on customer retention methods that compound, turning payment efficiency into competitive advantage rather than administrative overhead.

How We Selected These Strategies

Selection criteria prioritized three factors: measurable impact on deposit timing, implementation feasibility for teams under 50 people, and downstream effects on customer experience. Strategies that solve deposit delays while creating new friction points did not make the cut. Each item earned its place by addressing root causes rather than symptoms.

A structured framework showing how Level 3 processing and modern payment strategies improve cash flow, reduce costs, and accelerate deposits.

1. Upgrade to Level 3 Processing for B2B and High-Value Transactions

Why It Matters

Most eCommerce platforms default to Level 1 processing, which captures minimal transaction data. This creates two problems: higher interchange fees and slower settlement times. Level 3 processing submits detailed line-item data that helps issuers and networks evaluate transactions more efficiently.

The misconception that Level 3 only benefits government contractors persists. In reality, any business processing corporate cards, fleet cards, or high-value B2B transactions may benefit from reduced costs and cleaner transaction data.

What It Looks Like Today

Modern payment systems can auto-populate Level 3 data fields from your order management workflow. A connected payment gateway can help merchants pass tax amounts, customer codes, and line-item details more consistently, reducing manual entry and improving transaction quality.

How to Apply It

Audit your transaction mix to identify what percentage involves corporate or purchasing cards. If B2B represents more than 15% of volume, the ROI calculation often favors Level 3 implementation. Start with your highest-value transaction categories and expand systematically. Request a processing statement review from your merchant services provider to quantify potential savings.

2. Implement Remote Deposit Capture for Check Payments

Why It Matters

eCommerce businesses often dismiss check payments as irrelevant. Yet B2B customers, particularly in manufacturing, wholesale, and government sectors, still prefer checks for large orders. Without remote deposit capture, these payments create 5-7 day deposit delays that distort cash flow projections.

What It Looks Like Today

Remote deposit capture has evolved beyond basic mobile scanning. Current solutions integrate with accounting software, automate reconciliation, and provide same-day or next-day availability for deposited funds. The technology eliminates physical bank visits while maintaining audit trails required for compliance.

How to Apply It

Evaluate your accounts receivable aging report. If check payments represent meaningful volume with extended collection cycles, remote deposit capture addresses the bottleneck directly. Prioritize solutions that integrate with your existing bank relationships and accounting stack rather than standalone apps that create reconciliation overhead.

3. Negotiate Guaranteed Next-Day Funding Terms

Why It Matters

Standard merchant accounts batch transactions daily but release funds on a 2-3 day rolling basis. This timing gap exists because processors use your money during the float period. Guaranteed next-day funding eliminates this gap, but many eCommerce managers assume it requires premium pricing or enterprise volume.

What It Looks Like Today

Competition among merchant services providers has made faster funding accessible to mid-size businesses. Providers offering guaranteed next-day funding help merchants improve cash flow predictability without layering on unnecessary operational friction.

How to Apply It

Review your current merchant agreement for funding timeline language. Request quotes from providers explicitly offering next-day funding without volume thresholds. Calculate the value of accelerated access: if your average daily processing volume is $5,000, two days of float represents $10,000 in working capital you could deploy elsewhere.

4. Optimize Authorization Rates to Prevent Revenue Leakage

Why It Matters

Failed authorizations do not just lose immediate sales. They trigger customer service inquiries, erode trust, and often result in permanent customer loss. As digital payments continue to grow, authorization performance becomes increasingly important for retention and repeat purchases.

The hidden cost: declined transactions often succeed on retry with different processors, meaning your authorization rate may reflect configuration issues rather than actual fraud or insufficient funds.

What It Looks Like Today

Modern gateways offer intelligent retry logic, automatic card updater services, and network tokenization that maintains authorization rates even when customers receive new card numbers. These features run silently, preventing declines before customers notice.

How to Apply It

Pull your decline reason codes from the past 90 days. Categorize by cause: expired cards, insufficient funds, fraud flags, or technical errors. Each category requires different intervention. Expired card declines respond to card updater services. Technical errors often indicate gateway configuration issues your processor can resolve.

5. Deploy Proactive Chargeback Defense

Why It Matters

Chargebacks do not just cost the disputed amount. They trigger reserve holds, increase processing rates, and in severe cases, result in account termination. The deposit impact compounds: processors hold additional funds as chargeback ratios rise, creating artificial cash flow constraints.

What It Looks Like Today

Chargeback prevention has shifted from reactive dispute management to proactive alert systems. Visa explains that chargebacks start when cardholders dispute transactions through their issuer, which is why early alerts and quick merchant response matter. Services now notify merchants of pending disputes before they escalate, allowing refunds that preserve customer relationships and avoid avoidable chargeback fees.

How to Apply It

Enroll in chargeback alert networks through your processor. Establish clear internal protocols: who reviews alerts, what refund thresholds apply, and how quickly responses must occur. Track your chargeback ratio monthly against the 1% threshold that triggers processor scrutiny.

6. Streamline Recurring Payment Infrastructure

Why It Matters

Subscription and recurring payment models create predictable revenue, but failed recurring charges create unpredictable deposit gaps. Each failed charge requires manual intervention, delays deposits, and risks involuntary churn. The customer retention methods that matter most are often invisible, preventing problems customers never see.

What It Looks Like Today

Account updater services automatically refresh stored card credentials when banks issue replacements. Intelligent retry scheduling attempts failed charges at optimal times based on historical success patterns. These systems maintain subscription continuity without customer friction.

How to Apply It

Measure your recurring payment failure rate and involuntary churn percentage. If failures exceed 3% monthly, infrastructure improvements will pay for themselves. Implement dunning sequences that communicate payment issues to customers before cancellation, giving them opportunity to update credentials proactively.

7. Consolidate Payment Data for Faster Reconciliation

Why It Matters

Deposit delays often stem from internal bottlenecks rather than processor timing. When payment data lives in disconnected systems, reconciliation consumes hours that delay financial close processes and obscure cash position visibility.

What It Looks Like Today

Modern platforms consolidate transaction data, deposit records, and fee breakdowns into single dashboards that eliminate manual spreadsheet reconciliation. According to the PCI Security Standards Council, merchants also benefit when payment handling processes stay standardized and documented, which supports both security and cleaner operational workflows.

How to Apply It

Map your current reconciliation workflow. Identify where manual data transfer occurs between systems. Prioritize integration between your payment gateway, accounting software, and bank feeds. Even partial automation of reconciliation reduces the effective deposit-to-usable-cash timeline by eliminating internal processing delays.

The Pattern Across These Strategies

Each strategy addresses a different node in the payment lifecycle, but they share common principles. First, they shift from reactive to proactive, preventing problems rather than resolving them. Second, they leverage data that already exists in your transactions but goes uncaptured or unused. Third, they recognize that customer retention and operational efficiency reinforce each other.

The tradeoff across all seven: implementation requires upfront configuration time that pays dividends through reduced ongoing friction. Businesses that treat payment infrastructure as a one-time setup miss the compounding benefits of continuous optimization. The most effective approach treats payments as a system where improvements in one area reduce friction throughout.

Where to Start

Implementing all seven strategies simultaneously would overwhelm any team. Begin with the highest-impact, lowest-effort combination for your specific situation. If B2B transactions represent significant volume, Level 3 processing can deliver immediate ROI. If authorization failures plague your checkout, tackle that bottleneck first.

Most eCommerce managers find that addressing 2-3 strategies in the first quarter creates momentum and frees resources for subsequent improvements. The goal is not perfection but directional progress that compounds over time. Start where the pain is sharpest and expand systematically.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies include negotiating next-day funding terms with your processor, implementing remote deposit capture for check payments, and optimizing authorization rates to prevent failed transactions that delay batching. The most effective approach combines processor selection with internal workflow improvements that eliminate reconciliation bottlenecks.

How does Level 3 processing reduce interchange fees?

Level 3 processing submits detailed transaction data including line items, tax amounts, customer codes, and shipping information. Card networks reward this transparency with lower interchange rates because the additional data reduces fraud risk and simplifies dispute resolution. Savings vary by transaction mix, card type, and processor setup.

Why do authorization failures affect customer retention?

Failed authorizations create immediate friction that damages customer trust. Even when customers have sufficient funds, technical declines force them to re-enter payment information, contact support, or abandon purchases entirely. Repeat failures on subscription charges cause involuntary churn, losing customers who intended to continue purchasing.

When should I consider upgrading from standard to Level 3 processing?

Consider Level 3 processing when B2B, government, or corporate card transactions exceed 15% of your total volume. The implementation cost and complexity have decreased significantly, making the upgrade worthwhile at lower thresholds than in previous years. Request a processing statement analysis to quantify your specific savings potential.

Which payment processing fees can I reduce through optimization?

Interchange fees offer the largest reduction opportunity through Level 2 and Level 3 data submission. Assessment fees from card networks are fixed, but processor markup fees are negotiable based on volume and risk profile. Chargeback fees decrease through proactive dispute prevention. Authorization fees reduce when retry logic prevents unnecessary decline attempts.

What role does fraud protection play in deposit timing?

Aggressive fraud filters delay legitimate transactions for manual review, extending deposit timelines. Conversely, inadequate fraud protection leads to chargebacks that trigger reserve holds on future deposits. The optimal approach balances protection with approval speed, using machine learning tools that improve accuracy over time rather than blanket rules that create friction.

Sources