Merchant Services Optimization to Cut Hidden Fees

A line-by-line guide to reading processor statements, calculating effective rates, and eliminating costly surprises

Learn how to audit your payment processing statements, identify negotiable fees, and choose the right pricing model. This guide gives eCommerce managers a repeatable system for merchant services optimization that delivers predictable costs.

TL;DR

- Know your effective rate – Total fees divided by total volume is the only honest measure of what you pay. Anything above 2.5% card-present or 3% card-not-present leaves room to optimize.

- Choose interchange-plus pricing – It exposes processor markup as a separate line item, making hidden fees visible and rate creep easier to catch.

- Eliminate junk fees at renewal – PCI non-compliance, batch, statement, and gateway access fees are often negotiable or removable. Bring audit data to the conversation.

- Optimize transaction routing – Pass full data (AVS, CVV, level 2/3), enable PINless debit routing, and batch daily to reduce downgrades and improve authorization rates.

- Audit monthly – Track effective rate, downgrade percentage, and chargeback ratio every month. Rate creep is preventable when you catch it within 30 days.

Guide Orientation

This guide shows eCommerce managers how to find, eliminate, and prevent hidden payment processing fees through merchant services optimization. It’s written for operators at established online businesses (10-50 employees) who already process meaningful volume and want predictable costs, faster deposits, and cleaner statements.

By the end, you’ll be able to read a processor statement line by line, calculate your effective rate, identify which fees are negotiable, choose between pricing models, and build a monthly audit habit. This guide does not cover tax compliance, international FX hedging, or cryptocurrency settlement. It focuses on card-present and card-not-present processing in the U.S. market.

Why Payment Processing Transparency Matters Now

Payment costs are no longer a back-office line item. Every basis point of markup compounds against your margin.

The problem isn’t the interchange rate itself. It’s the layers stacked on top: PCI non-compliance fees, batch fees, statement fees, cross-border assessments, monthly minimums, and downgrade surcharges that appear only when you read footnotes. Opaque fee structures make it harder to forecast cash flow, compare processor proposals, and spot preventable margin leakage.

Meanwhile, fraud controls, compliance requirements, and changing network rules continue to add operational complexity. Transparent pricing is now a cash flow strategy, not a finance-team preference.

Core Concepts: What You’re Actually Paying For

Every card transaction carries three cost layers. Understanding them is the foundation of any serious audit.

Interchange

Set by the card networks (Visa, Mastercard, Discover, Amex) and paid to the issuing bank. This is non-negotiable. It varies by card type, transaction method, and merchant category. A rewards card costs more than a basic debit card. A keyed-in transaction costs more than a chip read. According to the Federal Reserve, interchange varies significantly by card type and transaction method.

Assessments

Also set by the networks, paid to the networks themselves. Small, fixed, and non-negotiable.

Processor Markup

This is the only layer you can actually negotiate. It’s what your processor charges on top of interchange and assessments. It shows up as a percentage, a per-transaction fee, or both, and it’s where hidden fees hide.

Common Misconceptions

- “Flat rate means no hidden fees.” Flat-rate pricing (2.9% + $0.30) bundles everything into one number, which hides the markup by blending it with interchange. Simple does not mean cheap.

- “A lower rate is a better deal.” A teaser qualified rate can mask steep downgrade fees on rewards or corporate cards. Your effective rate, total fees divided by total volume, is what matters.

- “All processors follow the same rules.” Contract terms, early termination fees, and reserve holds vary widely. Vendor lock-in is a real cost.

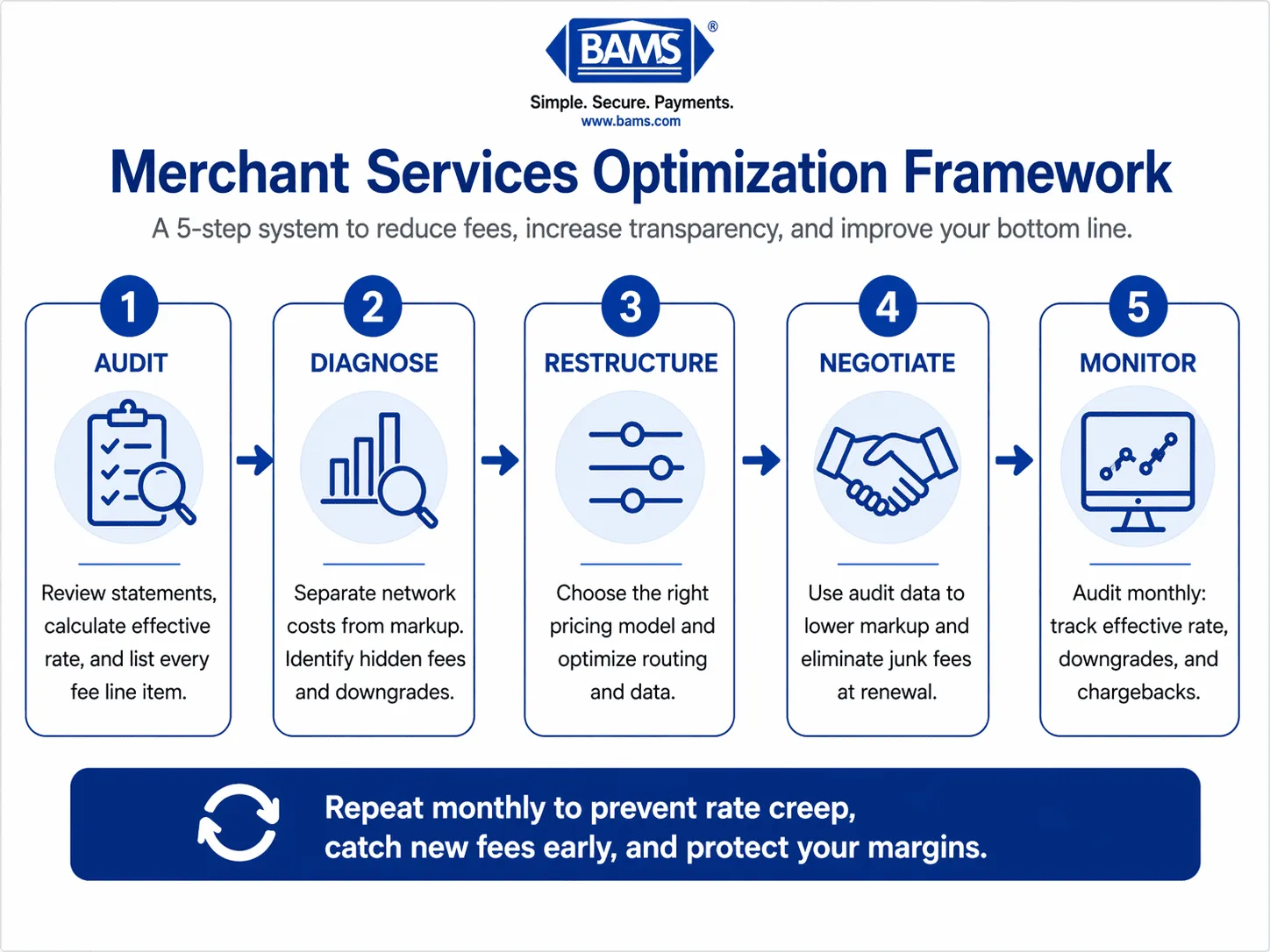

The Framework for Reducing Merchant Fees

A simple framework to audit, reduce, and monitor payment processing costs.

Use this five-stage loop to move from opaque billing to predictable cost. Each stage feeds the next, and the cycle repeats monthly.

- Audit. Establish your baseline effective rate and catalog every line item on your statement.

- Diagnose. Separate fixed network costs from negotiable markup. Identify hidden fees and downgrades.

- Restructure. Choose the pricing model that matches your volume and ticket profile. Interchange-plus for most, flat-rate only for very low volume.

- Negotiate. Use your baseline data to renegotiate markup, eliminate junk fees, and lock in contract terms.

- Monitor. Run a monthly audit to catch rate creep, re-price drift, and new fees before they compound.

This framework works because it treats payments as an operational system, not a vendor relationship. Transparency is the output, not the input.

Step-by-Step Breakdown

Step 1: Run a Full Statement Audit

Objective: Know your true effective rate and every fee you pay.

Pull your last three months of processing statements. Calculate your effective rate: total fees divided by total card volume. If it’s above 2.5% for card-present or 3% for card-not-present, you have room to move.

List every line item. Flag anything labeled “monthly,” “PCI,” “regulatory,” “network access,” “batch,” “statement,” or “non-qualified.” These are where markup hides. Note which fees are percentage-based and which are flat.

Anti-patterns: Don’t rely on the summary page. The detail pages are where the real story lives. Don’t compare advertised rates to your effective rate because they measure different things.

Success indicators: You can state your effective rate to two decimal places and explain every fee category on your statement. A modern payment gateway with itemized reporting makes this process much easier.

Step 2: Choose the Right Pricing Model

Objective: Match your pricing structure to your transaction profile.

Interchange-plus pricing shows interchange, assessments, and markup as separate line items. You see exactly what the processor earns. Flat-rate pricing bundles everything into one number, convenient for very small merchants but expensive at scale. Tiered pricing (qualified, mid-qualified, non-qualified) is the least transparent and almost always the most expensive.

For most eCommerce businesses processing more than $25,000 per month, interchange-plus pricing is the clear choice. It exposes markup and makes rate creep visible.

Anti-patterns: Don’t accept tiered pricing. Don’t stay on flat-rate past $25K monthly volume unless your average ticket is under $15.

Success indicators: Your statement separates interchange, assessments, and markup clearly. You can answer the question “what did my processor earn on this transaction?” without guessing.

Step 3: Eliminate Junk Fees and Renegotiate

Identify and eliminate common hidden fees that increase processing costs.

Objective: Remove non-essential fees and lower markup.

Bring your audit data to a renegotiation conversation. Target these fees first: annual fees, PCI non-compliance fees (fix the underlying issue instead), batch fees over $0.10, statement fees, and IRS reporting fees duplicated elsewhere. Ask for them to be waived or removed. Many are pure margin.

On markup, anchor to your effective rate and request a specific basis-point reduction. Processors expect this conversation at renewal, and they have room to move. Transparent interchange-plus pricing with itemized statements removes the guesswork from this step entirely.

Anti-patterns: Don’t accept “that’s just our standard fee” as an answer. Don’t sign a new multi-year contract without an early termination clause capped at a reasonable amount.

Success indicators: Junk fees are removed, markup is in writing, and your contract terms are documented.

Step 4: Optimize Transaction Routing and Acceptance

Objective: Reduce downgrades and improve authorization rates.

Downgrades happen when transactions miss interchange qualification criteria, often due to missing data (AVS, CVV, level 2/3 data for B2B). Every downgrade moves a transaction to a more expensive interchange category. Enable address verification, pass full data on every transaction, and batch daily.

For debit, enable PINless routing where possible. For B2B, pass level 2 and level 3 data to unlock commercial card interchange rates. Improving data quality and routing logic can lower costs while also improving approval rates.

Anti-patterns: Don’t batch weekly. Don’t ignore soft declines. Don’t run card-not-present transactions without AVS and CVV.

Success indicators: Downgrade rate below 15%, authorization rate above 92%, and settlement within one business day.

Step 5: Build a Monthly Audit Habit

Objective: Catch rate creep and new fees within 30 days.

Rate creep is real. Processors adjust pricing between statements, add new fees tied to “network changes,” and re-price based on mix shifts. A monthly 20-minute audit catches this early.

Track three numbers: effective rate, downgrade percentage, and total fees as a percentage of volume. Compare month-over-month. Any change of more than five basis points deserves a phone call. Also track chargeback ratio, since dispute activity can quietly add cost and complexity.

Anti-patterns: Don’t skip months. Don’t delegate this to someone who can’t read interchange categories.

Success indicators: You have a rolling 12-month record of effective rate and fee composition, and rate changes never surprise you.

Practical Example: A Mid-Sized eCommerce Brand

A home goods brand processing $450,000 monthly on flat-rate pricing at 2.9% + $0.30 was paying roughly $13,050 in monthly fees. Their effective rate was 2.9%, but they had no visibility into markup.

After moving to interchange-plus with a 25 basis point markup plus $0.10 per transaction, their effective rate dropped to 2.35%. That’s $2,475 saved per month, $29,700 annually, with no change to customer experience. They also caught a duplicated $99 monthly “gateway access” fee that had been billed for 18 months.

The next operational gain often comes from better cash flow visibility and faster deposits through guaranteed next-day funding.

Common Mistakes and Pitfalls

- Chasing the lowest advertised rate. Teaser rates rarely reflect what you’ll actually pay. Effective rate is the only honest metric.

- Ignoring contract terms. Early termination fees, auto-renewal clauses, and equipment leases can lock you into bad economics for years.

- Treating PCI compliance as optional. Non-compliance fees are avoidable. Complete the self-assessment questionnaire annually.

- Skipping the monthly audit. Rate creep is the most common source of margin erosion, and it’s fully preventable.

- Confusing simplicity with transparency. One blended rate is simple. Interchange-plus with itemized line items is transparent. They are not the same.

These mistakes are normal. Processing is deliberately complex, and most operators learn the system only after it has cost them. The goal is not perfection, it’s visibility.

Card network fees and rules change regularly. Always verify updates against Visa’s published fee schedule.

What to Do Next

Start with one action: pull your last statement and calculate your effective rate. That single number tells you whether the rest of this guide is urgent or routine for your business.

From there, work the framework one stage at a time. Audit this month, restructure next quarter, renegotiate at renewal. Treat this guide as a reference you return to when your volume changes, your processor raises fees, or your contract comes up for renewal. Transparent pricing isn’t a one-time project. It’s a habit that compounds, quietly, in your favor.

Frequently Asked Questions

What are merchant fees and how do they work?

Merchant fees are the total cost of accepting card payments. They include interchange (paid to the card-issuing bank), assessments (paid to card networks like Visa and Mastercard), and processor markup (paid to your payment processor). Only the markup is negotiable. Your effective rate, total fees divided by total card volume, is the clearest measure of what you actually pay.

Which pricing model is better: interchange-plus or flat rate?

Interchange-plus is almost always better once you’re processing more than $25,000 per month. It separates interchange, assessments, and markup into clear line items, so you can see exactly what your processor earns. Flat rate is simpler but hides the markup inside a single blended number, which usually costs more at scale.

What are some common hidden fees in merchant services?

The most common hidden fees include PCI non-compliance fees, monthly minimums, batch fees, statement fees, network access fees, IRS reporting fees, gateway access fees, and downgrade surcharges on rewards or corporate cards. Many appear as small line items that add up to hundreds or thousands per month.

How can I negotiate lower merchant processing rates?

Start with your effective rate and a full list of line items from your last three statements. Anchor the conversation to specific basis-point reductions on markup, not on interchange. Ask for junk fees to be waived, request removal of annual and statement fees, and make sure any agreement is in writing with a clear end date.

When should I consider switching payment processors?

Consider switching when your effective rate has crept up over two or more quarters, when your processor refuses to move to interchange-plus pricing, when deposits consistently take more than two business days, or when you’re paying fees you can’t explain. A contract renewal is the natural trigger point.

How often should I audit my payment processing statements?

Monthly. A 20-minute review of effective rate, downgrade percentage, and total fees as a share of volume catches rate creep early. Any change greater than five basis points month-over-month deserves a phone call to your processor.