Business Capital Access: Why Your Processor Profits from Delay

Faster funding isn’t a premium feature — it’s what happens when processors stop earning interest on your float

Learn why standard two-to-three-day funding timelines persist despite modern payment infrastructure. This piece examines how processors profit from holding merchant revenue and why fast funding is a design decision, not a tier.

TL;DR

- Delayed deposits aren’t a technical necessity – Modern payment rails (same-day ACH, FedNow) make next-day and same-day funding possible. Most delays exist because processors profit from holding your money.

- Funding speed is an architecture issue, not a feature – Processors built around transparency (interchange-plus pricing, real-time risk assessment) deliver faster deposits by default, not as a paid upgrade.

- eCommerce operators feel this more than anyone – With 100% card-based revenue, every day of delay compounds into real cash flow pressure, affecting payroll, inventory, and ad spend.

- Ask better questions when evaluating processors – Forget “do you offer fast funding?” Ask about batch cut-off times, weekend handling, hold triggers, and whether next-day funding costs extra.

Your Processor Is Earning Interest on Your Revenue

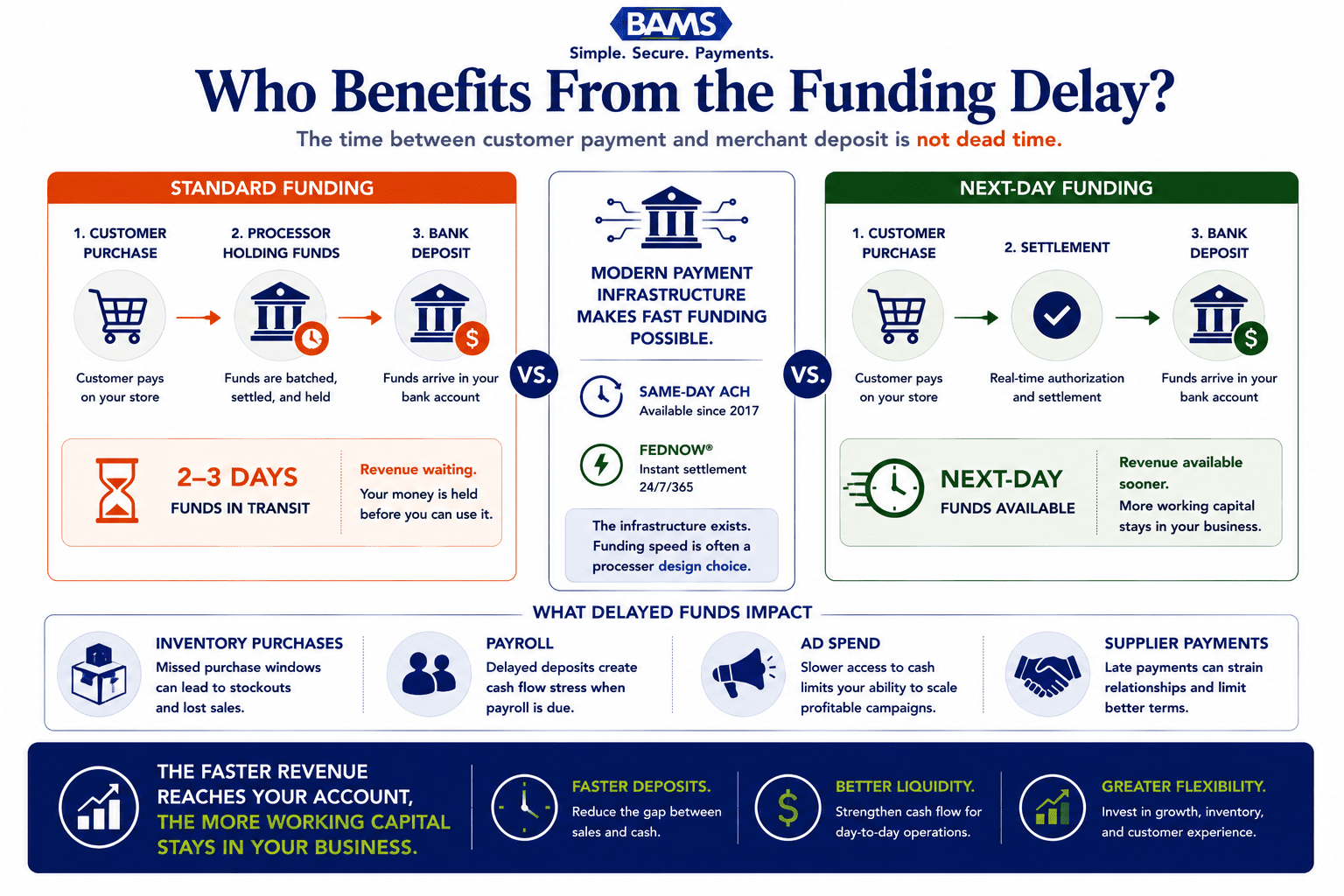

Here’s something eCommerce operators rarely think about: the two or three days between a customer swiping their card and the money landing in your bank account isn’t dead time. That gap is productive. Just not for you. Your credit card processing partner is holding your revenue, and in many cases, earning overnight interest on the float. Faster business capital access isn’t a perk they’re generously offering. It’s something they’ve been withholding by design.

Modern payment rails can move money faster. The real question is who benefits when deposits are delayed

Why “Standard” Funding Timelines Became the Norm

To be fair, delayed settlement made sense in an earlier era. Payment rails were slower. Fraud detection required manual review. Batch processing happened once a day, and banks needed time to reconcile. The two-to-three-day funding window became an industry default because the infrastructure genuinely demanded it.

But that was before same-day ACH. Before FedNow. Before processors had real-time transaction data, machine-learning fraud models, and automated underwriting that can assess merchant risk in seconds. The infrastructure has changed. The timelines haven’t, at least not at most processors. And there’s a reason for that: holding your money is profitable.

The industry built a business model around the float, then dressed it up as risk management.

Fast Funding Is a Design Decision, Not a Feature Tier

We believe that funding speed is a structural outcome of how a processor is built, not a premium add-on to be unlocked at a higher price. When a processor is designed around transparency, next-day funding isn’t a luxury. It’s the natural result.

That single distinction changes everything about how you should evaluate your payment stack.

What’s Actually Happening Between the Swipe and Your Bank Account

Most eCommerce managers understand the basics: customer pays, processor processes, money arrives. But the middle step is where the story gets interesting, and where the delays hide.

When a customer completes a transaction on your site, the payment travels through a chain: your gateway captures it, your processor routes it through the card network (Visa, Mastercard), the issuing bank authorizes it, and the acquiring bank settles it into your merchant account. From there, an ACH transfer moves the funds to your business bank account.

Each of those handoffs introduces potential delay. But here’s the thing: most of those delays are now optional. Same-day ACH has been available since 2017, and the Federal Reserve’s FedNow Service enables instant settlement around the clock. The rails exist. The question is whether your processor chooses to use them.

The Hidden Variables eCommerce Operators Miss

Your funding speed isn’t just about your processor’s policy. It’s about your specific configuration. Cut-off times matter: if your processor batches transactions at 4 PM ET but your biggest sales window is 8 PM to midnight, an entire day of revenue misses the batch and sits idle. Weekend sales surges (common in eCommerce) can mean Friday night revenue doesn’t arrive until Tuesday or Wednesday.

Cross-border transactions add another layer. International card settlements involve additional intermediary banks and currency conversion windows. High-volume sale events like flash sales or holiday promotions can trigger risk holds that freeze funds for days, even when the transactions are perfectly legitimate.

None of this is explained in the “we offer next-day funding” marketing copy. But it’s what actually determines when you get paid.

The Cash Flow Math That Matters

Consider what delayed deposits actually cost. Federal Reserve data shows that 33% of employer firms delayed payments to owners, suppliers, or payroll at least once in 2023. That’s not a minor inconvenience. That’s missed supplier discounts, strained vendor relationships, and payroll anxiety.

For an eCommerce business processing $500,000 annually, a two-day funding delay means roughly $2,700 in revenue is perpetually in transit. That’s money you can’t use for ad spend, inventory, or payroll. Scale that up during Q4 when daily volume doubles or triples, and the float becomes a real operational constraint.

Meanwhile, small businesses account for 94% of employer firms in the U.S. and employ 61.6 million people. The aggregate impact of processors sitting on merchant revenue is enormous. And it’s largely invisible.

Why Some Processors Move Faster (and Others Don’t Want To)

Processors that offer same-day or next-day funding as a default tend to share a few traits. They use interchange-plus pricing, which means their revenue comes from a transparent margin on each transaction rather than from opaque bundled rates that obscure the true cost. They invest in real-time risk assessment so they don’t need to hold funds for manual review. And they maintain direct banking relationships that eliminate intermediary delays.

Processors that keep you waiting tend to share different traits. Tiered pricing that hides their margins. Batch processing schedules optimized for their operations, not yours. And “premium” funding tiers that charge you extra to access your own money faster.

This is where BAMS takes a different approach. Their next-day funding isn’t a premium tier; it’s part of how the system works. Combined with interchange-plus pricing and dedicated account management, the model is built so that standard holds don’t eat into your cash flow the way they do with legacy processors.

If This Is Right, You’re Paying Twice for Slow Money

If funding speed really is a design choice rather than a technical limitation, the implications are uncomfortable. It means every day your revenue sits in someone else’s account is a day you’re subsidizing their business model. You’re paying processing fees and giving them free use of your capital.

It also means the “same-day funding” upsell that some processors offer for an additional fee is, bluntly, charging you to stop doing something they didn’t need to do in the first place. That’s not a feature. That’s a toll.

For eCommerce operators specifically, this matters more than for brick-and-mortar businesses. Your revenue is 100% card-based. Every dollar flows through your processor. There’s no cash register to fall back on. Meanwhile, U.S. Small Business Administration resources continue to highlight the critical role small businesses play in the U.S. economy and why access to working capital remains essential for growth and stability.

Stop Comparing Features. Start Comparing Architectures.

Most processors advertise fast funding. The important question is whether fast funding is built into the system or sold as an upgrade.

The useful reframe here isn’t “same-day vs. next-day.” It’s this: does your processor’s architecture treat your revenue as yours, or as theirs until they release it?

When you evaluate payment processors, don’t ask “do you offer fast funding?” Every processor will say yes. Instead, ask: What’s your batch cut-off time? What happens to weekend transactions? Is next-day funding the default, or does it cost extra? What triggers a hold on my funds, and who decides when to release them?

The answers to those questions reveal whether speed is baked into the system or bolted on top of a slow one. That’s the difference between a processor built for you and one built around you. When you’re choosing a payment processor, the architecture tells you more than the feature list ever will.

Your Revenue Shouldn’t Need Permission to Reach You

We don’t think faster deposits are something merchants should have to negotiate for, pay extra for, or feel grateful to receive. The technology exists. The rails are live. The data to underwrite risk in real time is abundant.

The only thing standing between you and your money is a business model that profits from the delay. Once you see that clearly, you can’t unsee it.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your card transaction revenue is deposited into your bank account by the next business day after the sale. It eliminates the standard two-to-three-day hold that most legacy processors impose.

Why does funding speed vary so much between processors?

Funding speed depends on a processor’s batch schedule, banking relationships, risk assessment methods, and whether they use modern payment rails like same-day ACH. Processors built around transparency tend to settle faster because they don’t rely on float revenue.

How do weekend sales and high-volume events affect deposit timing?

Weekend transactions typically don’t batch until Monday, which means Friday and Saturday revenue may not arrive until Tuesday or Wednesday. High-volume events can also trigger risk holds that delay funds further, depending on your processor’s policies.