Payment Processing Fees: Why Your Rate Is Higher Than You Think

Key Takeaways

- Most merchants underestimate their true payment processing fees.

- Assessment fees, PCI costs, and card-not-present rates increase total cost.

- Effective rate calculation provides a more accurate cost picture.

- Understanding fees improves pricing, forecasting, and profitability.

Why Most Payment Processing Fee Estimates Are Incorrect

Merchants often rely on simplified estimates when evaluating payment costs. These estimates are usually based on quoted interchange rates or a general percentage provided by the processor.

However, payment processing involves multiple cost components beyond interchange. As a result, the commonly quoted percentage rarely represents the true effective rate.

Industry data shows that card payment costs continue to rise as transaction volumes grow. According to the Merchant Payments Coalition, total card fees in the United States exceeded $236 billion in 2024, reflecting the growing financial impact on merchants.

The Structure of Payment Processing Fees

To understand true costs, merchants must break payment processing fees into their core components.

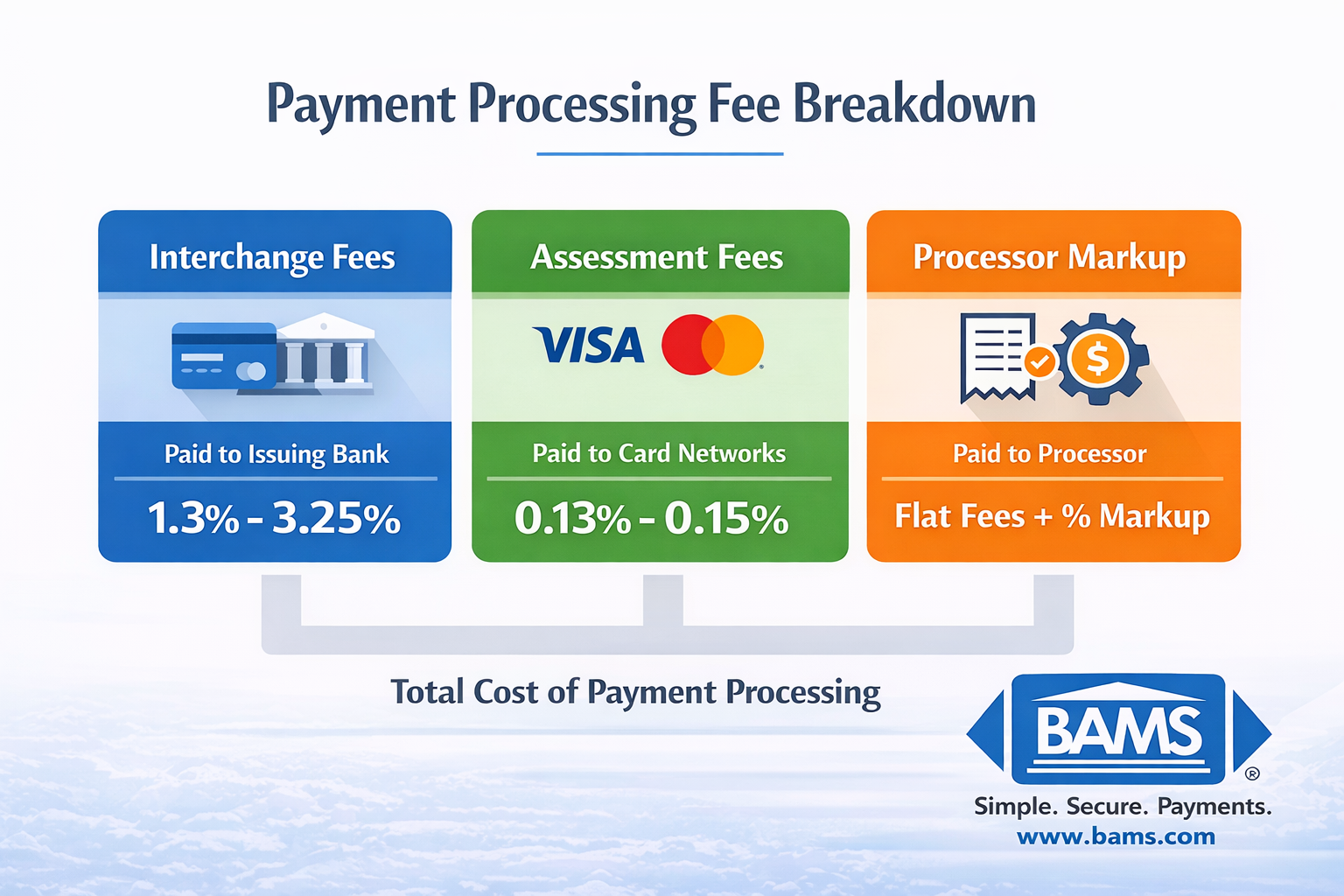

Payment processing fees consist of interchange, card network assessments, and processor markup that together determine your true effective rate.

1. Interchange Fees

Interchange fees are paid to the issuing bank and represent the largest portion of processing costs. These fees vary depending on card type, transaction method, and risk level.

2. Assessment Fees

Assessment fees are charged by card networks such as Visa and Mastercard. These fees are typically a small percentage of each transaction but apply to total volume, making their cumulative impact significant.

Card network rules and fee structures are outlined in official guidance from Visa merchant resources, which explain how transactions move across the payment ecosystem.

3. Processor Markup

Processors add their own markup on top of interchange and assessment fees. This may include per-transaction fees, monthly fees, or bundled pricing structures.

4. PCI Compliance and Additional Fees

Merchants are also responsible for maintaining payment security standards. The PCI Security Standards Council provides guidelines for protecting cardholder data. Failure to comply may result in additional fees or penalties.

Why Your Effective Rate Is Higher Than Expected

The effective rate represents the total fees paid divided by total transaction volume. This metric provides a more accurate picture of actual payment processing costs.

Several factors increase effective rates beyond initial estimates:

- Card-not-present transaction premiums

- Higher-cost rewards or business cards

- Monthly and compliance fees

- Batch and statement charges

For eCommerce businesses, card-not-present transactions significantly increase costs due to higher fraud risk and stricter verification requirements.

Merchants using modern payment gateways can better track transaction data and identify cost drivers across payment types.

The Cost of Inaccurate Fee Assumptions

Underestimating payment processing fees leads to inaccurate pricing models and reduced profitability. Businesses may assume margins that do not exist, affecting growth decisions and operational planning.

For example, a business processing $500,000 monthly may believe it pays 2.5%, or $12,500. However, if the true effective rate is 3.1%, actual costs rise to $15,500—an additional $36,000 annually.

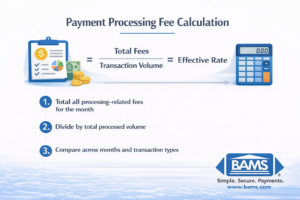

How to Calculate Your True Payment Processing Fees

To determine your real cost, merchants should calculate their effective rate using actual statement data.

- Total all processing-related fees for the month

- Divide by total processed volume

- Compare across months and transaction types

Calculating your effective rate reveals the true cost of payment processing beyond quoted percentages.

This process reveals the true cost of accepting payments and provides a foundation for cost optimization strategies. Merchants who fully understand their fee structure are better positioned to negotiate competitive credit card processing pricing and improve long-term profitability.

Conclusion

Payment processing fees are more complex than they appear. While quoted rates provide a baseline, they rarely reflect the full cost structure.

Merchants that calculate their effective rate gain a clearer understanding of their financial position. This insight supports better pricing decisions, improved cost control, and stronger long-term profitability.

Accurate cost visibility is not optional—it is essential for managing payment infrastructure effectively.

Frequently Asked Questions

What are payment processing fees?

Payment processing fees are the total costs merchants pay to accept card payments, including interchange, assessment fees, and processor markup.

Why are my fees higher than quoted rates?

Quoted rates often exclude additional costs such as PCI compliance, assessment fees, and card-not-present premiums.

How do I calculate my effective rate?

Divide total monthly processing fees by total transaction volume to determine your true effective rate.

What is a typical effective rate?

Most businesses experience effective rates between 2.5% and 3.5%, depending on transaction mix and industry.