Interchange Fees vs Merchant Discount Rate Explained

Understanding interchange fees vs merchant discount rate is critical for eCommerce merchants who want to control payment processing costs. Most businesses focus only on the total percentage they pay. However, that number includes multiple components with very different levels of control. By understanding the difference, merchants can identify where negotiation is possible and where optimization delivers better results. As a result, finance teams can improve margins, pricing strategy, and long-term payment efficiency.

Key Takeaways

- Interchange fees are set by card networks and cannot be negotiated directly.

- Merchant discount rate includes processor markup, which is negotiable.

- Interchange typically represents 70–80% of total processing costs.

- Interchange optimization improves efficiency, while MDR negotiation reduces costs faster.

- Transparent pricing models help merchants identify savings opportunities.

What Is the Difference Between Interchange Fees and Merchant Discount Rate?

Interchange fees are the wholesale cost of accepting card payments. These fees are set by card networks such as Visa and Mastercard and are paid to the issuing bank for each transaction.

The merchant discount rate (MDR) is the total cost merchants pay. It includes interchange fees, card network assessments, and the processor’s markup. While interchange is fixed, MDR is where pricing structures and negotiations take place.

According to the Federal Reserve’s interchange fee data, these fees are designed to compensate issuing banks for transaction risk, fraud management, and credit services.

How Payment Costs Are Structured

Merchants often see only one rate on their statement. However, that rate combines three separate cost components. Therefore, focusing only on the total percentage can hide meaningful savings opportunities.

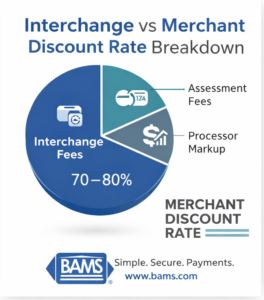

A visual breakdown of the merchant discount rate, showing how interchange fees, assessment fees, and processor markup contribute to total payment processing costs.

- Interchange fees (paid to issuing banks)

- Assessment fees (paid to card networks)

- Processor markup (paid to your payment provider)

When merchants break these components apart, they gain better visibility into where costs originate and where improvements are possible.

This structure explains why focusing only on the total percentage can lead to missed savings opportunities.

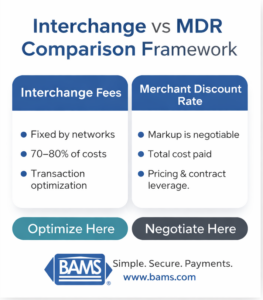

Interchange Fees vs Merchant Discount Rate: Comparison Framework

A side-by-side comparison showing where merchants can optimize interchange costs and where they can negotiate merchant discount rates.

| Criteria | Interchange Fees | Merchant Discount Rate | Merchant Focus |

|---|---|---|---|

| Negotiability | Fixed by networks | Markup is negotiable | MDR |

| Transparency | Published by networks | Depends on pricing model | Both |

| Cost Impact | 70–80% of fees | Total cost paid | Both |

| Optimization | Transaction-level | Pricing & contract | MDR first |

Where Merchants Actually Have Leverage

Card networks set interchange fees, so merchants cannot negotiate them directly. However, merchants can influence how transactions qualify. For example, better data quality, AVS verification, and faster settlement can move transactions into lower-cost categories.

In contrast, the merchant discount rate includes processor markup. Therefore, this is where merchants have real negotiating power. By negotiating markup, switching pricing models, or selecting transparent providers, businesses can reduce total processing costs more effectively.

Merchants operating online should also ensure their payment setup aligns with their business model through optimized eCommerce merchant account solutions.

Interchange Optimization Strategies

Although merchants cannot negotiate interchange, they can improve how transactions qualify. As a result, small operational changes can reduce costs over time.

- Use AVS and CVV verification for card-not-present transactions

- Settle transactions within 24 hours to avoid downgrades

- Submit Level 2 and Level 3 data for B2B payments

- Reduce manual or keyed transactions

Visa explains that secure transaction data and proper authorization practices improve approval rates while reducing fraud exposure. Consequently, these improvements can influence interchange qualification outcomes.

Merchant Discount Rate Optimization Strategies

Reducing MDR is often faster and more impactful for merchants. Key strategies include:

- Switching to interchange-plus pricing for transparency

- Negotiating processor markup based on volume

- Eliminating unnecessary fees

- Improving settlement timing to support cash flow

Faster funding options can also improve working capital. Merchants should evaluate how settlement timing aligns with operations using solutions like next-day funding.

Common Mistakes Merchants Make

- Focusing only on the total rate: Merchants often ignore the underlying cost structure.

- Accepting tiered pricing: This model frequently reduces transparency and increases costs.

- Ignoring interchange qualification: Poor data handling can trigger higher fees.

- Failing to renegotiate: As volume grows, merchants should revisit pricing terms.

Over time, these mistakes can significantly increase processing costs. Therefore, merchants should review their payment structure regularly.

Business Impact: Why This Distinction Matters

For merchants processing significant volume, small changes in MDR can produce meaningful savings. A 0.3% reduction on $500,000 in annual volume results in $1,500 in savings.

At scale, understanding interchange categories can further improve margins by reducing unnecessary downgrades and improving authorization performance.

The PCI Security Standards Council merchant resources emphasize that proper handling of transaction data is essential for maintaining secure and efficient payment systems.

Conclusion

Interchange fees vs merchant discount rate is not just a technical distinction. Instead, it directly affects merchant profitability and operational efficiency. Interchange explains why transactions cost what they do. However, merchant discount rate determines what merchants actually pay.

Therefore, merchants should focus on negotiating processor markup while improving transaction quality. By doing so, they can reduce costs, improve payment performance, and build a more efficient payment infrastructure over time.

Frequently Asked Questions

Can merchants negotiate interchange fees?

No. Interchange fees are set by card networks and are non-negotiable.

What part of payment processing can be negotiated?

The processor markup within the merchant discount rate is negotiable.

Why do some transactions cost more than others?

Costs vary based on card type, transaction method, and data quality.

What is the best pricing model for transparency?

Interchange-plus pricing provides the most visibility into actual costs.

Does PCI compliance affect processing costs?

Indirectly. Strong compliance reduces risk, potential fines, and operational issues.