Credit Card Fees Transparency: Why Hiding Costs More

Why Hiding Credit Card Fees Costs More Than Showing Them

The case for transparent surcharges: how honest pricing builds trust and protects your margins

Discover why absorbing credit card processing fees silently may be hurting your business more than helping it. Learn how transparent surcharging can build customer trust while protecting your bottom line.

TL;DR

- Processing fees hit record highs – Credit card companies collected $148.5 billion in swipe fees in 2024, up 70% since the pandemic, and you’re absorbing that cost silently.

- Surcharges build trust, not friction – Transparent pricing gives customers agency and stops cash buyers from subsidizing card rewards programs.

- Frame it as choice, not penalty – The difference between “we charge extra” and “here’s what it costs, you decide” changes how customers perceive your business.

- Your margins become predictable – When processing costs are visible and passed through appropriately, your pricing stops fluctuating based on payment mix.

The Fee You’re Hiding Is Costing You More Than the Fee Itself

Every eCommerce manager knows the sting. You close a $200 sale, feel that brief hit of dopamine, then watch $5 to $7 vanish into processing fees before the money even hits your account. Most businesses absorb this cost silently, baking it into prices and hoping customers don’t notice.

But here’s the thing: your customers aren’t stupid. They know someone’s paying those fees. The only question is whether you’re being honest about it.

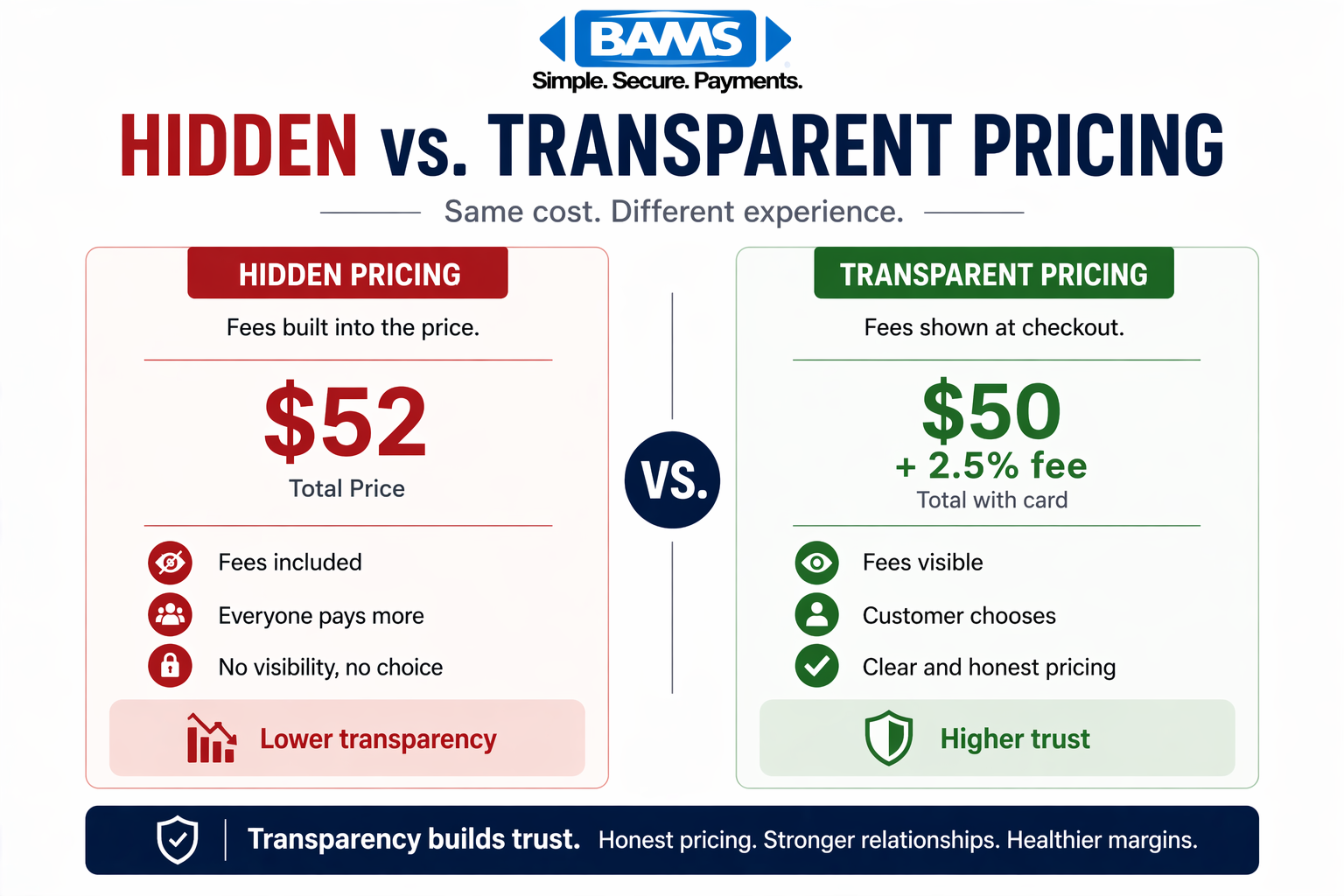

A simplified comparison showing how hidden pricing inflates costs for everyone, while transparent pricing clearly shows credit card fees.

The Polite Fiction of “Free” Card Acceptance

The conventional wisdom says you should never show customers what credit card processing costs. The logic sounds reasonable: why introduce friction? Why give shoppers a reason to hesitate?

So businesses raise prices across the board. A $50 item becomes $52. Everyone pays more, whether they use a card, debit, or digital wallet. Cash customers subsidize rewards programs they’ll never benefit from. And the 1.5% to 3.5% processing fees small businesses pay? Buried in the price tag, invisible but very much present.

Card processing costs are primarily driven by interchange fees set by card networks and issuing banks, forming the largest component of merchant payment expenses as outlined by the Federal Reserve.

This approach worked when processing costs were stable and modest. Neither is true anymore.

What Changed Everything

Here’s what I actually believe: a surcharge for credit card fees isn’t a penalty you impose on customers. It’s a transparency tool that builds trust and protects your margins simultaneously.

The math has shifted dramatically. Card networks enforce strict requirements around surcharging, including disclosure rules, percentage limits, and restrictions on debit card usage as outlined in Visa’s official guidelines.

You’re not absorbing a minor cost anymore. You’re subsidizing a system designed to extract maximum value from every transaction you process.

Why Transparency Beats Absorption

Look at what’s happening on the ground. Across North Carolina, businesses from coffee shops to car dealerships started adding visible surcharges to credit card transactions in 2024 and 2025. They matched the actual swipe rates, typically around 2.35%, and showed them clearly on receipts.

The interesting part? Many customers appreciated the honesty. When you understand the difference between a convenience fee vs surcharge (convenience fees apply to alternative payment methods; surcharges offset the actual cost of card acceptance), you can communicate clearly with customers about what they’re paying and why.

The businesses that struggled were the ones who added fees without explanation. Transparency without communication is just a surprise charge. But transparency with context? That’s a different conversation entirely.

The Numbers Tell the Story

Consider your actual exposure. For eCommerce specifically, that percentage is dramatically higher. Most of your revenue likely flows through cards.

Meanwhile, interchange fees vary wildly by card type. Premium rewards cards cost even more to process.

When a customer uses their fancy travel rewards card, you’re paying for their free flights. That’s the system. The question is whether you want to keep pretending it doesn’t exist.

What Smart Operators Are Doing

A comparison showing how transparent pricing gives customers the choice between paying a card fee or using a no-fee payment option.

The most effective approach I’ve seen combines three elements. First, transparent pricing that shows customers exactly what card processing costs. Second, a cash or debit discount that rewards lower-cost payment methods. Third, clear communication at checkout explaining the options.

This isn’t about punishing card users. It’s about giving customers agency. Some will happily pay 2.5% extra for the convenience and rewards of their credit card. Others will choose debit or ACH and save money. Both groups appreciate having the choice.

Credit card processing for small businesses doesn’t have to be a fixed cost you simply endure. It can be a variable you actively manage. Executing this strategy requires the right infrastructure. An integrated payment gateway ensures accurate fee handling, proper routing, and a seamless checkout experience without hidden friction.

If This Is Right, Your Pricing Model Needs Work

Think about what changes if you stop hiding processing costs. Your base prices become more competitive. Cash and debit customers stop subsidizing card users. Your margins become predictable rather than variable based on payment mix.

More importantly, you start having honest conversations with customers about value. The businesses that thrive in the next decade won’t be the ones with the lowest prices. They’ll be the ones customers trust most. And trust starts with transparency.

Swipe fees on 2025 holiday spending alone are projected to hit $19.9 billion. That money comes from somewhere. Right now, it’s coming from your margins or your customers’ wallets, invisibly. Making it visible doesn’t create the cost. It just stops pretending the cost doesn’t exist.

If you want true cost control, start with transparent interchange plus pricing, which separates network fees from processor markup and removes hidden pricing layers across your transactions.

A Better Mental Model

Stop thinking of processing fees as a tax on doing business. Start thinking of them as a service you can choose to provide, subsidize, or pass through.

When you frame surcharges as “we’re charging you extra,” customers feel penalized. When you frame them as “here’s what card acceptance actually costs, and we’re giving you the choice,” the dynamic shifts entirely. One approach creates resentment. The other creates partnership.

The reframe that matters: surcharges aren’t about passing costs to customers. They’re about stopping the practice of hiding costs from customers.

The Honest Path Forward

Visa and Mastercard control 80% of the card market. They set the prices. You don’t have leverage over interchange rates. But you do have leverage over how you communicate with customers and structure your pricing.

The businesses winning on processing costs aren’t the ones with the best negotiating skills. They’re the ones who stopped treating fees as shameful secrets and started treating them as facts worth discussing openly.

Your customers already know someone pays for their rewards points. The only question is whether you’re going to keep pretending it’s not them.

Frequently Asked Questions

What’s the difference between a convenience fee and a surcharge?

A surcharge offsets the actual cost of accepting credit cards and applies only to credit transactions. A convenience fee covers the cost of offering an alternative payment channel, like paying a utility bill online instead of by mail.

Are credit card surcharges legal for eCommerce businesses?

Surcharges are legal in most U.S. states, but rules vary. You must disclose the surcharge clearly before checkout and cap it at your actual processing cost (typically no more than 3%).

How can I reduce credit card processing fees without adding surcharges?

Negotiate with your payment processor, encourage debit or ACH payments, and ensure you’re on the right pricing model for your transaction volume. Reviewing your merchant statement quarterly helps catch unnecessary fees.

Sources