Monthly Payment Processor Audits: 2025 Checklist

The specific statement checkpoints that catch hidden fee discrepancies before they drain your margins

Learn the exact line items and fee categories to inspect each month so your merchant fee comparison reflects what you actually pay. Built for eCommerce teams processing $50K+ monthly.

TL;DR

- Monthly audits beat annual reviews – A 30-minute monthly check of effective rate, downgrades, and new line items catches 70% of fee discrepancies before they compound.

- Effective rate is the only number that matters – Total fees divided by total volume. Compare this against your quoted markup plus published interchange to spot padding.

- Downgrades and PCI fees are the biggest leaks – Non-qualified transaction tiers and duplicate PCI compliance and non-compliance charges quietly inflate costs by 40-80 basis points.

- New line items require written justification – Unannounced “network access” or “technology” fees are refundable if the processor cannot produce the disclosure notice.

- Interchange-plus pricing eliminates most ambiguity – For eCommerce merchants above $50K monthly volume, transparent pricing models paired with next-day funding produce measurable cash flow and margin gains.

1. The Hidden Cost Problem in 2025 Payment Processing

Payment processing statements have become intentionally complex. Line items shift month to month, new assessment fees appear without notice, and the effective rate you negotiated rarely matches what you actually pay. For eCommerce managers running 10-50 person operations, this opacity quietly erodes margins, sometimes by 40-80 basis points per transaction.

The shift toward transparent pricing is accelerating. According to the PCI Security Standards Council, compliance remains a critical part of payment operations for merchants handling card data, and billing clarity matters more as statements grow more complex. Monthly payment processor audits are the practical response: a repeatable process that catches discrepancies before they compound into five-figure annual leaks. This list gives you the specific audit checkpoints that drive accurate merchant fee comparisons.

2. Who This Is For and What It Skips

This guide is for eCommerce managers, finance leads, and owner-operators processing at least $50K per month who want to verify what they are actually paying versus what they were quoted. It skips general “shop around” advice, vendor rankings, and marketing copy about saving 30%. Instead, you get the audit checkpoints, the specific statement fields to inspect, and the fee categories most likely to drift. Use it as a monthly review template, not a one-time exercise.

3. Selection Criteria

Each item made the list based on three filters: frequency of discrepancy in real statements, financial impact when left unchecked, and ability for a non-specialist to verify in under 30 minutes. Items requiring a forensic accountant were excluded. Items that depend on a specific processor’s proprietary tooling were also excluded in favor of universal audit methods.

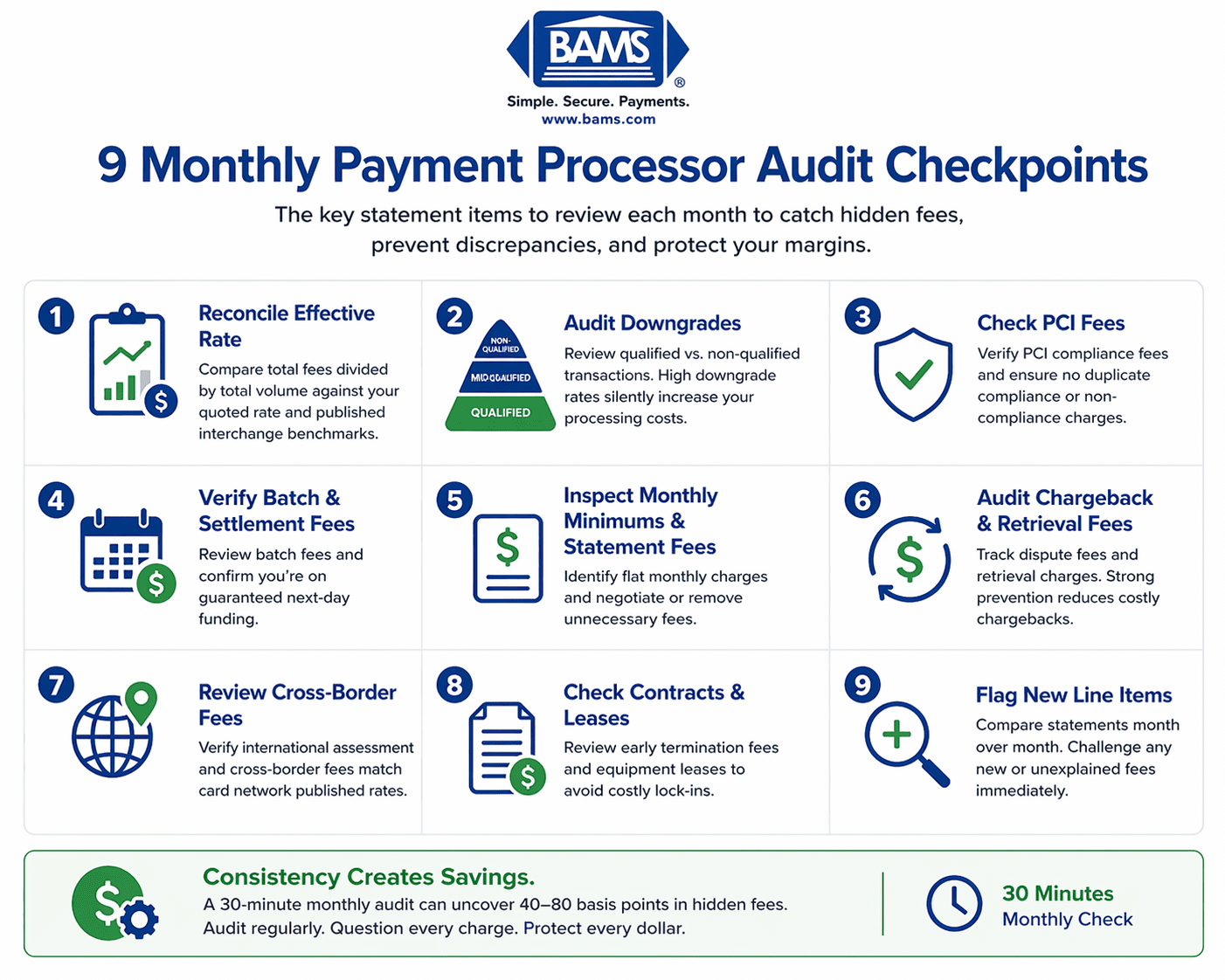

4. Nine Audit Checkpoints for Payment Processing Transparency

A complete monthly audit checklist that helps merchants identify hidden fees, prevent discrepancies, and protect margins.

1. Reconcile the Effective Rate Against Your Quoted Rate

Why it matters: Your effective rate (total fees divided by total volume) is the only number that matters for merchant fee comparison. Processors rarely volunteer it because it exposes padding in assessment and “network” categories.

What it looks like today: Most statements bury the data across three to five pages. Interchange-plus statements itemize clearly; tiered and flat-rate statements obscure the underlying interchange cost.

How to apply it: Each month, divide total fees charged by total processed volume. Compare against your contracted markup plus published guidance from the Federal Reserve. A variance above 15 basis points warrants a formal dispute with your provider.

2. Audit Non-Qualified and Downgrade Categories

Why it matters: Tiered pricing processors classify transactions as qualified, mid-qualified, or non-qualified, often moving transactions into expensive buckets without explanation. This is the single largest source of unexpected fee inflation.

What it looks like today: Keyed-in transactions, rewards cards, and corporate cards frequently get downgraded. Some processors downgrade cards that should qualify at the standard rate.

How to apply it: Pull a monthly downgrade report. If more than 20% of volume sits in non-qualified tiers, you are either mispriced or misconfigured. Consider switching to payment gateway solutions, which support more transparent payment operations.

3. Check for PCI Compliance and Non-Compliance Fees

Why it matters: PCI fees appear in two forms: a monthly or annual compliance charge, and a non-compliance penalty that can become a major recurring cost if your attestation lapses silently.

What it looks like today: Some processors auto-enroll merchants in “PCI programs” that charge $15-$35 monthly plus a non-compliance fee if you miss the annual self-assessment.

How to apply it: Confirm your PCI self-assessment is current. If you see both a compliance fee and a non-compliance fee on the same statement, dispute immediately.

4. Verify Batch and Settlement Fees

Why it matters: Batch fees ($0.10-$0.25 per batch) add up when settled daily across multiple MIDs. More importantly, delayed settlement schedules cost you working capital.

What it looks like today: Processors increasingly offer next-day funding, but not always by default. Funding delays of two to three business days are still common on legacy contracts.

How to apply it: Count your batches. Confirm your funding timeline. Providers offering guaranteed next-day funding can materially improve cash flow for volume-heavy eCommerce operations.

5. Inspect Monthly Minimum and Statement Fees

Why it matters: Monthly minimums penalize seasonal businesses. Statement fees (often $10-$25) are pure profit for the processor and frequently negotiable or waivable.

What it looks like today: These fees rarely appear in initial quotes. They surface on month two or three and persist until someone notices.

How to apply it: List every flat monthly charge on your statement. Request a written justification for each. Any charge without a clear service attached is a candidate for removal at renewal.

6. Audit Chargeback and Retrieval Fees

Why it matters: Chargeback fees range from $15 to $100 per dispute. Retrieval fees (before a formal chargeback) add another $5-$25. High-volume eCommerce brands can absorb thousands monthly without a defense strategy.

What it looks like today: Friendly fraud and “item not received” disputes dominate. Most processors charge the fee whether you win or lose the dispute.

How to apply it: Track chargebacks as a percentage of transactions. According to Visa, dispute management directly affects merchant costs and operational efficiency. Implement delivery confirmation, clear billing descriptors, and proactive refund policies. Review your processor’s chargeback defense support; passive processors cost you both the fee and the transaction value.

7. Review Cross-Border and International Assessment Fees

Why it matters: International transactions carry a 0.4%-1% assessment on top of interchange. If your eCommerce traffic includes international buyers, this line can be significant and is often misreported.

What it looks like today: Card brands charge separate ISA (International Service Assessment) and cross-border fees. Some processors bundle these opaquely into a single markup.

How to apply it: Segment your transaction report by issuing country. Verify the assessment matches the published Visa and Mastercard rates, not your processor’s bundled version.

8. Check for Early Termination and Equipment Lease Clauses

Why it matters: Early termination fees (ETFs) of $295-$995 and multi-year equipment leases are the two clauses that keep merchants locked into bad contracts. They do not appear on monthly statements but surface the moment you try to leave.

What it looks like today: Equipment leases for terminals can total $4,000-$8,000 over four years for hardware worth $300. Processor-agnostic POS systems let you switch without replacing hardware.

How to apply it: Re-read your contract annually. Document your ETF exposure and lease remaining term. When evaluating alternatives, factor buyout costs into your merchant services comparison.

9. Flag New Line Items Month Over Month

Why it matters: Processors introduce new fees through buried notifications. A line item appearing for the first time is your signal to investigate before it becomes permanent.

What it looks like today: “Network access fees,” “regulatory compliance fees,” and “technology fees” are common euphemisms for margin increases.

How to apply it: Keep a rolling 12-month statement comparison. Any new line item requires written justification. If the processor cannot produce the notice that disclosed the change, the fee is refundable.

5. Pattern Recognition: What These Checkpoints Share

Every item on this list exploits the same structural weakness: asymmetric information between processor and merchant. Processors know your rate structure line by line; most merchants review statements in aggregate. The audit process reverses this asymmetry.

A second pattern: fees tend to cluster. Merchants paying inflated downgrades usually also pay padded PCI fees and carry outdated ETF clauses. Contracts age poorly. What was competitive in 2021 is rarely competitive in 2025, particularly as next-day funding, interchange-plus pricing, and transparent chargeback support have become table stakes rather than premium features. Treat the audit as a system, not a checklist, and the compounding savings exceed any single line-item recovery.

6. Where to Start When Resources Are Limited

A simple 5-step audit workflow that helps merchants consistently detect and reduce hidden payment processing costs.

You do not need to tackle all nine checkpoints at once. If you have one hour this month, start with effective rate reconciliation (item 1), downgrade analysis (item 2), and new line item review (item 9). These three surface roughly 70% of typical discrepancies.

Build from there. Add chargeback tracking and PCI verification in month two. Tackle contract-level items (ETFs, equipment leases) at renewal. The goal is a repeatable 30-minute monthly process, not a perfect first audit.

Frequently Asked Questions

How often should I conduct a payment processor audit?

Monthly audits catch discrepancies before they compound. A 30-minute review of effective rate, downgrades, and new line items each month is enough for most eCommerce operations. Conduct a deeper annual audit that includes contract clauses, equipment leases, and vendor comparison.

What pricing model is better: interchange-plus or flat rate?

Interchange-plus is more transparent because it separates the true cost of the transaction (interchange) from your processor’s markup. Flat-rate pricing is simpler but typically costs more at volume above $25K per month. For established eCommerce operations, interchange-plus almost always produces a lower effective rate.

What are the most common hidden fees in merchant services?

The recurring offenders are non-qualified downgrade fees, PCI non-compliance penalties, monthly minimums, statement fees, “network access” surcharges, and early termination fees. Equipment lease payments also qualify as hidden when they extend years past the hardware’s useful life.

When should I consider switching payment processors?

Switch when your effective rate exceeds quoted markup by more than 15 basis points for two consecutive months, when new line items appear without written notice, when chargeback support is unresponsive, or when funding delays exceed one business day. Factor early termination fees and lease buyouts into the switching cost analysis.

How do I negotiate lower merchant processing rates?

Bring data. Present three months of statements, your calculated effective rate, and two competing quotes with the same pricing structure. Ask for specific concessions: markup reduction, waived monthly fees, shorter contract term, no ETF. Processors retain existing accounts at margins they would never offer new prospects if you ask directly.

What should a transparent processing statement include?

A transparent statement itemizes interchange by category, shows assessment fees separately, lists the processor markup as a distinct line, and discloses every flat monthly charge with a clear service name. If you cannot reconstruct your effective rate from the statement in under 10 minutes, the statement is not transparent.

Sources