Payment Optimization for eCommerce and Faster Deposits

How to stop lending your revenue to payment processors and build predictable cash flow

Learn why your deposits get delayed and which payment optimization strategies actually accelerate fund access. This guide covers processor selection, funding timelines, and cost reduction tactics for e-commerce managers.

TL;DR

- Audit your current funding timeline first – Document actual deposit delays by pulling three months of transaction data before making any changes

- Next-day funding often pays for itself – The cost of delayed deposits (credit line interest, missed discounts) frequently exceeds any premium for faster funding

- Authorization rate improvements recover real revenue – A 2% improvement on $3 million volume equals $60,000 in previously lost sales

- Batch timing matters more than most realize – A 9 PM cutoff captures significantly more same-day transactions than a 5 PM cutoff, accelerating deposits

- Chargeback prevention protects funding speed – High chargeback ratios trigger reserves and holds that negate any faster funding benefits

What This Guide Covers

This guide is for eCommerce managers at established online businesses who are tired of watching cash sit in limbo while bills pile up. You’ll learn exactly why deposits get delayed, which payment optimization strategies actually accelerate fund access, and how to build a payment infrastructure that delivers predictable cash flow.

We cover processor selection, funding timelines, authorization rate improvements, and cost reduction tactics. We don’t cover payment gateway development, PCI compliance audits, or international tax implications. By the end, you’ll have a clear framework for evaluating your current setup and a step-by-step path to faster deposits.

Why Payment Optimization Matters Now

eCommerce operates on thin margins and tight timelines. When your processor holds funds for 3 to 5 business days, you’re essentially extending an interest-free loan to your payment provider while your suppliers expect payment, your ad spend compounds, and your inventory needs replenishing.

The gap between transaction and deposit creates a cash flow blind spot that forces reactive decision-making. AI-driven payment automation can reduce processing costs, yet most mid-size eCommerce operations still run on legacy systems designed for a slower era.

Real-time payment infrastructure is expanding globally. The infrastructure for faster deposits exists. The question is whether your merchant services setup takes advantage of it.

Core Concepts You Need to Understand

Settlement vs. Funding

Settlement is when the card network confirms the transaction. Funding is when money hits your bank account. These are separate processes, and the gap between them is where your cash flow problems live. Many processors batch settlements once daily, then release funds on their own schedule.

Authorization Rates and Their Hidden Cost

Every declined transaction is lost revenue. Payment orchestration can improve authorization rates through dynamic routing. On $5 million in annual transactions, that’s $100,000 to $150,000 in recovered sales. Authorization failures also create customer friction that damages lifetime value.

The True Cost of Processing

Interchange fees, assessment fees, processor markup, and incidental charges stack up. Most eCommerce managers focus on the headline rate while ignoring the total cost of acceptance. Cost-plus pricing models reveal the actual interchange cost, making optimization possible. Tiered pricing obscures these details and often costs more.

Funding Speed Tiers

Standard funding takes 2 to 3 business days. Guaranteed next-day funding gets deposits to you within 24 hours of batch close. Same-day funding exists but typically carries premium fees. The right tier depends on your cash conversion cycle and margin structure.

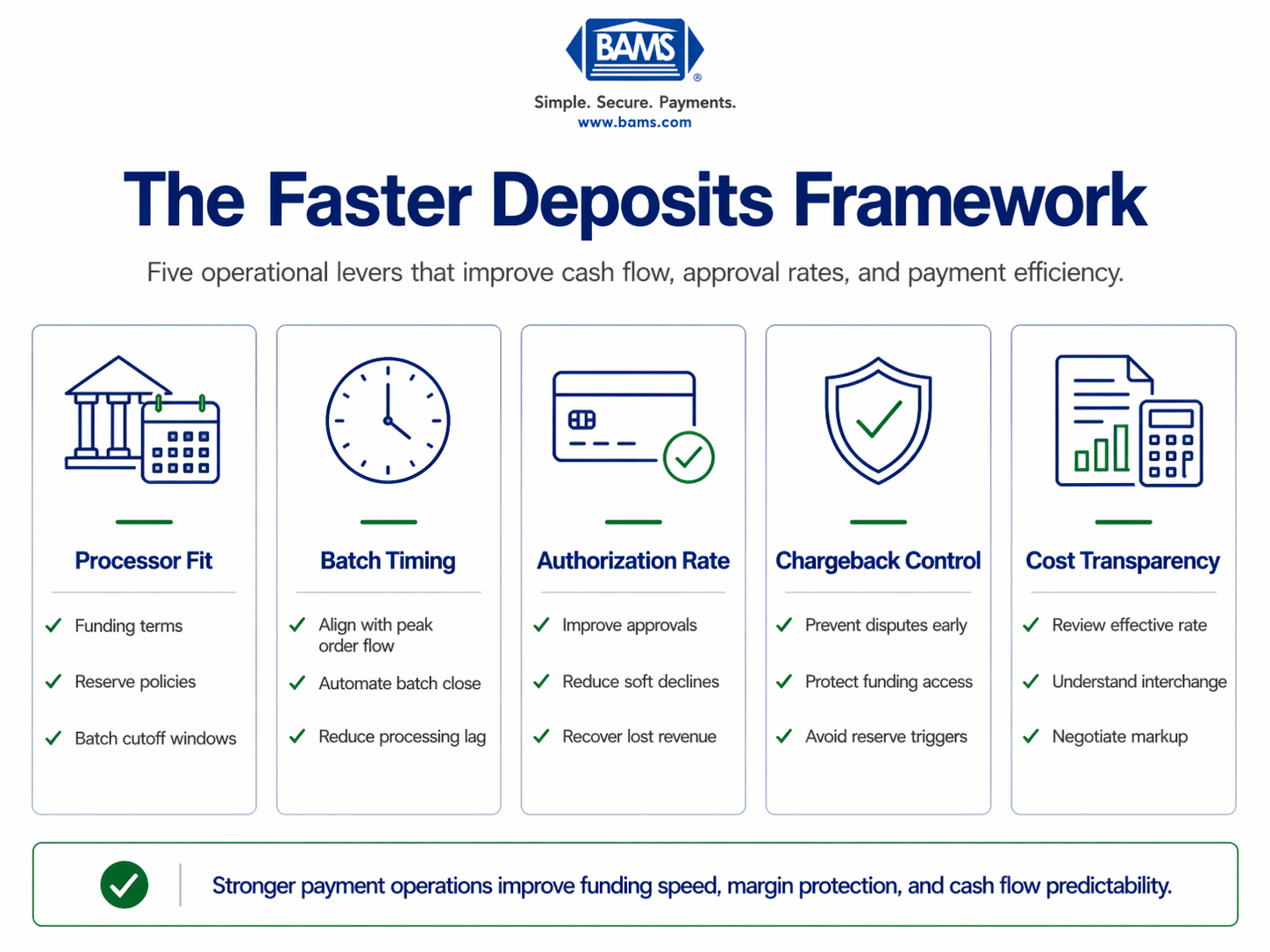

The Faster Deposits Framework

Overcoming delayed deposits requires addressing four interconnected areas: processor selection, operational timing, authorization optimization, and cost structure alignment. These aren’t isolated fixes. They form a system where improvements in one area amplify results in others.

The sequence matters. Start with processor evaluation, since everything else depends on your provider’s capabilities. Then optimize batch timing to maximize funding speed within your processor’s parameters. Next, improve authorization rates to increase the volume of successful transactions reaching settlement. Finally, align your cost structure to ensure faster funding doesn’t erode margins.

Each stage builds on the previous one. Rushing to optimize authorization rates while stuck with a processor that holds funds for 72 hours addresses symptoms, not causes.

Step 1: Audit Your Current Processor’s Funding Timeline

A structured framework showing the core levers eCommerce businesses can use to improve deposit speed and payment performance.

Objective

Establish a clear baseline of how long your money actually takes to reach your account, including all holds and exceptions.

Execution Guidance

Pull three months of transaction data and map each batch close time to the corresponding deposit date. Calculate the average, median, and longest funding delays. Identify patterns: Do certain transaction types trigger holds? Are weekends and holidays creating predictable gaps?

Review your merchant agreement for reserve requirements, rolling reserves, and hold policies. Many processors bury these details in addenda. Document the specific conditions that trigger extended holds, such as high-ticket items, new customer transactions, or international cards.

What to Avoid

Don’t accept “2 to 3 business days” as a complete answer. Dig into the actual deposit timestamps. Avoid comparing your current timeline to industry averages without understanding your specific transaction profile. A business processing $500 average tickets has different risk profiles than one processing $50 tickets.

Success Indicators

- You have a documented funding timeline with variance ranges.

- You understand which transaction types experience delays.

- You can identify the specific contractual terms governing your funding speed.

Step 2: Evaluate Next-Day Funding Options

Objective

Determine whether next-day funding makes financial sense for your operation and identify providers who offer it without prohibitive costs.

Execution Guidance

Calculate the cost of delayed deposits. If you’re paying 18% APR on a credit line to cover cash flow gaps, every day of deposit delay costs roughly 0.05% of the transaction value. On $500,000 monthly volume, 3-day delays cost approximately $750 monthly in financing costs alone.

Compare this against the premium (if any) for next-day funding in merchant services. Some providers, like BAMS, include next-day funding as a standard feature rather than an upcharge. Factor in batch cutoff times, since a 9:00 PM cutoff captures more same-day transactions than a 5:00 PM cutoff.

What to Avoid

Don’t switch processors solely for funding speed without evaluating total cost of acceptance. A processor offering next-day funding with inflated interchange markups may cost more overall. Avoid providers who require minimum volume commitments you can’t consistently meet.

Success Indicators

You have a clear cost-benefit analysis comparing your current setup to next-day funding alternatives. You’ve identified at least two providers whose terms align with your transaction profile and volume.

Step 3: Optimize Batch Timing and Processing Windows

Objective

Maximize the transactions captured in each batch while ensuring batches close early enough to qualify for fastest available funding.

Execution Guidance

Analyze your hourly transaction distribution. If 40% of your orders arrive between 7 PM and midnight, a 5 PM batch cutoff leaves significant volume for next-day processing, adding 24 hours to those deposits. Negotiate or configure batch close times that capture peak transaction periods.

Implement automatic batch closing rather than manual processes. Manual batching introduces human error and inconsistent timing. Your batch management should approach similar consistency.

What to Avoid

Don’t set batch times based on convenience rather than transaction patterns. Avoid running multiple batches daily unless your processor offers faster funding for each batch. Multiple batches with standard funding just fragments your deposits without accelerating them.

Success Indicators

Your batch cutoff captures at least 90% of daily transactions. Batches close automatically at consistent times. You’ve documented the relationship between batch timing and deposit timing.

Step 4: Improve Authorization Rates Through Smart Routing

Objective

Reduce declined transactions by routing payments through optimal processors based on card type, geography, and historical performance.

Execution Guidance

Segment your decline data by card network, issuing bank, and transaction characteristics. Identify patterns: Are international cards declining at higher rates? Do certain BIN ranges show consistent failures? This data informs routing decisions.

Consider payment orchestration platforms that dynamically route transactions to the processor most likely to approve them. These platforms maintain connections to multiple processors and use real-time performance data to optimize routing. Merchants using orchestration solutions reduce integration complexity while improving approval rates.

Implement retry logic for soft declines. A transaction that fails due to temporary issuer issues may succeed seconds later. Automated retry with appropriate delays recovers revenue without customer friction.

What to Avoid

Don’t treat all declines identically. Hard declines (stolen card, closed account) should not be retried. Soft declines (insufficient funds, temporary hold) warrant different handling. Avoid aggressive retry patterns that trigger fraud flags at issuing banks.

Success Indicators

Your authorization rate improves by at least 1 to 2 percentage points. You have visibility into decline reasons by category. Retry logic recovers measurable revenue without increasing chargeback rates.

Step 5: Reduce Cart Abandonment With Payment Flexibility

Objective

Capture more completed transactions by offering payment methods that match customer preferences and reduce checkout friction.

Execution Guidance

Customers using one-click checkout increase spending and purchase frequency. Implement saved payment credentials for returning customers. The reduction in checkout friction directly increases completed transactions.

Add digital wallet options (Apple Pay, Google Pay, PayPal) that let customers pay without entering card details. If you sell internationally, display prices and process payments in local currencies.

Evaluate buy-now-pay-later options for higher-ticket items. These services pay you immediately while extending credit to customers, accelerating your cash flow while increasing average order value.

What to Avoid

Don’t add payment options without understanding their cost structure. Some alternative payment methods carry higher fees that erode margins on low-ticket items. Avoid cluttering checkout with options your specific customer base doesn’t use.

Success Indicators

Cart abandonment rate decreases. Payment method distribution shows adoption of newly added options. Average order value remains stable or increases.

Step 6: Implement Proactive Chargeback Prevention

Objective

Reduce chargebacks that trigger processor holds, increased reserves, and potential account termination.

Execution Guidance

Deploy fraud detection tools that flag suspicious transactions before fulfillment. Machine learning models analyze transaction patterns, device fingerprints, and behavioral signals to identify fraud without blocking legitimate customers.

Implement clear billing descriptors that customers recognize. “Friendly fraud” chargebacks often occur when customers don’t recognize a charge. Your descriptor should include your brand name and a contact method.

Enroll in card network alert programs (Visa’s Verifi, Mastercard’s Ethoca) that notify you of disputes before they become chargebacks. These alerts give you the opportunity to issue refunds proactively, avoiding the chargeback entirely.

What to Avoid

Don’t set fraud rules so aggressively that you decline legitimate customers. False positives cost more than the fraud they prevent. Avoid ignoring chargeback patterns. Repeated chargebacks from specific products, traffic sources, or customer segments indicate systemic issues.

Success Indicators

Chargeback ratio stays below 0.5% (ideally below 0.3%). Fraud losses decrease without proportional increase in false declines. Processor removes or reduces reserve requirements based on improved performance.

Step 7: Negotiate Cost-Plus Pricing for Transparency

Objective

Gain visibility into actual processing costs and ensure you’re paying fair rates that support sustainable faster funding.

Execution Guidance

Request a cost-plus (interchange-plus) pricing structure that separates interchange fees, card network assessments, and processor markup. This transparency lets you identify optimization opportunities and verify you’re not overpaying.

Review your effective rate (total fees divided by total volume) monthly. Compare against benchmarks for your industry and average ticket size. E-commerce businesses typically see effective rates between 2.3% and 2.9%, depending on card mix and transaction characteristics.

Negotiate processor markup based on your volume, chargeback rate, and growth trajectory. Processors have flexibility on their margin even when interchange is fixed.

What to Avoid

Don’t accept tiered pricing models that obscure actual costs. Avoid long-term contracts with early termination fees that lock you into unfavorable terms. Don’t assume your current rate is competitive without market comparison.

Success Indicators

You can calculate your exact cost per transaction type. Your effective rate aligns with or beats industry benchmarks. Contract terms allow flexibility to renegotiate or switch providers.

Real-World Application: The Compound Effect

Consider a $3 million annual revenue eCommerce operation with 2.5-day average funding delays, 94% authorization rate, and 2.8% effective processing rate. Implementing this framework could yield the following results.

Switching to a processor with next-day funding and a 9 PM batch cutoff reduces average funding delay to under 24 hours. The business recovers approximately 1.5 days of cash flow, freeing roughly $12,300 in daily working capital.

Improving authorization rates by 2 percentage points (94% to 96%) on $3 million volume recovers $60,000 in previously declined transactions. Dynamic routing and retry logic capture most of this without additional customer acquisition cost.

Negotiating cost-plus pricing and optimizing card mix reduces effective rate from 2.8% to 2.5%. On $3 million volume, that’s $9,000 in annual savings that drops directly to bottom line.

These improvements compound. Faster deposits reduce financing costs. Higher authorization rates increase volume. Lower processing costs improve margins. The system works together.

Common Mistakes That Stall Progress

Focusing on funding speed while ignoring authorization rates leaves money on the table. A processor that funds quickly but declines 8% of transactions costs more than one with slightly slower funding and 97% approval rates.

Treating processor relationships as set-and-forget misses optimization opportunities. Your transaction profile changes as you grow. Quarterly reviews of funding timelines, approval rates, and effective rates catch drift before it compounds.

Underestimating the operational impact of chargeback prevention is common. Every chargeback costs $20 to $100 in fees beyond the transaction value. High chargeback ratios trigger reserves and holds that negate faster funding benefits.

Assuming all next-day funding offers are equivalent ignores critical details. Batch cutoff times, weekend handling, and holiday policies vary significantly. A “next-day” promise with a 3 PM cutoff and no weekend funding may deliver worse results than a 2-day promise with 9 PM cutoffs and Saturday deposits.

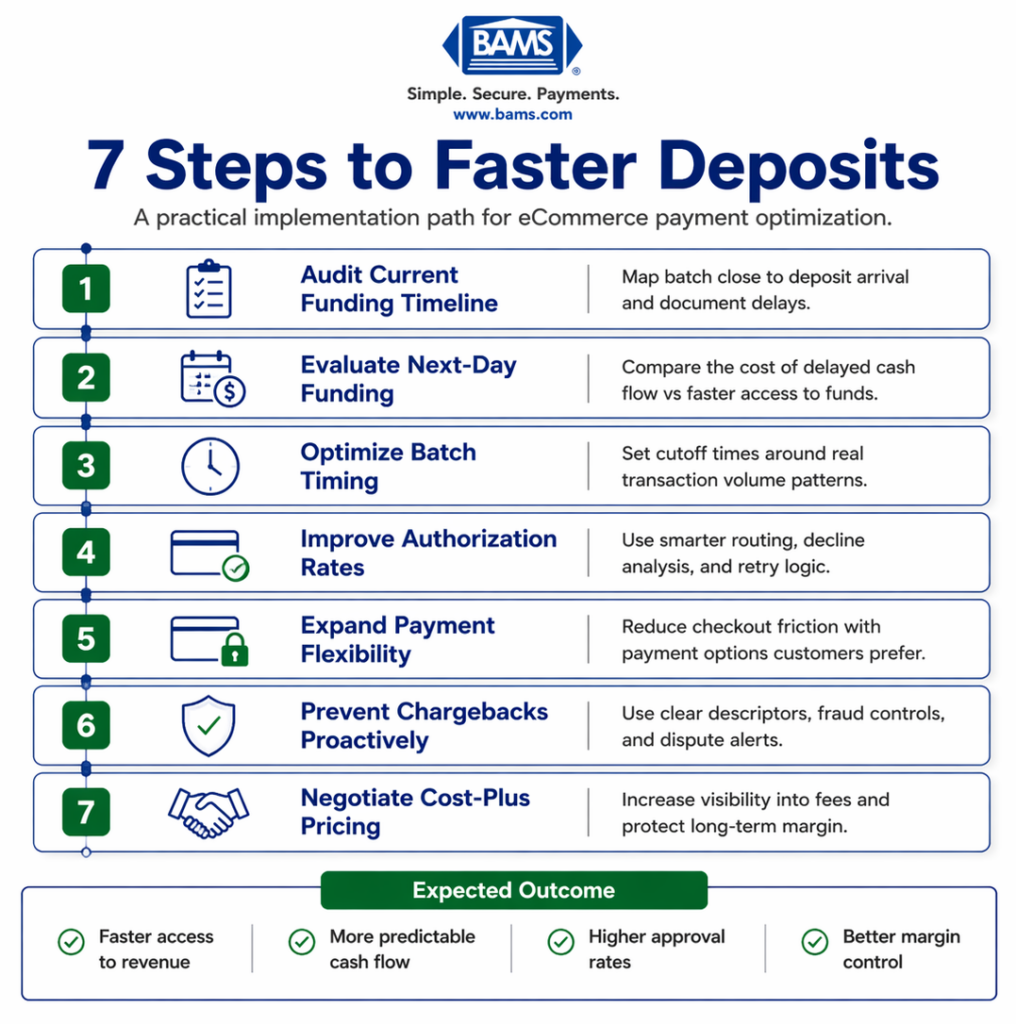

A step-by-step sequence for evaluating payment setup, improving approvals, and building faster, more predictable deposits.

What to Do Next

Start with Step 1: audit your current processor’s actual funding timeline. Pull three months of data and document the gap between batch close and deposit arrival. This baseline reveals whether your current setup is fixable or requires a provider change.

If your funding delays exceed 48 hours consistently, prioritize evaluating credit card processing merchants with next-day funding. The cash flow improvement from faster deposits typically justifies the switching costs within 3 to 6 months.

Use this guide as a reference rather than a checklist. Your specific transaction profile, customer base, and growth stage determine which optimizations deliver the highest return. Revisit quarterly as your business evolves and payment infrastructure options expand.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies include selecting processors that offer next-day funding, optimizing batch close times to capture more transactions before cutoff, and maintaining low chargeback ratios to avoid holds. The most effective approach combines processor selection with operational changes that maximize the volume of transactions qualifying for accelerated funding.

Why is payment optimization important for eCommerce businesses?

Payment optimization directly impacts cash flow, profit margins, and customer experience. Delayed deposits force businesses to use credit lines or delay supplier payments. Low authorization rates mean lost sales. High processing fees erode margins. Optimizing across all three areas compounds into significant financial improvement.

How can I improve my payment authorization rates?

Improve authorization rates by implementing dynamic routing that sends transactions to the processor most likely to approve them, adding retry logic for soft declines, ensuring billing information matches cardholder records, and using address verification services appropriately. Payment orchestration platforms automate much of this optimization.

What role does fraud protection play in payment optimization?

Fraud protection prevents chargebacks that trigger processor holds, increased reserves, and potential account termination. Effective fraud detection also reduces false declines that block legitimate customers. The goal is balancing fraud prevention with approval rate optimization rather than maximizing either in isolation.

When should I consider expanding my payment options?

Expand payment options when cart abandonment data shows customers dropping off at checkout, when you’re entering new geographic markets with different payment preferences, or when competitors offer options you don’t. Prioritize additions based on your specific customer demographics rather than adding every available option.

Which payment processing fees can I reduce to optimize costs?

Processor markup is the most negotiable fee component. Interchange fees are set by card networks but can be optimized through proper transaction categorization and Level 2/3 data submission for B2B transactions. Assessment fees are fixed. Focus negotiation on markup while optimizing transaction handling to qualify for lower interchange tiers.