5 Hidden Payment Processing Costs Draining Profits

Beyond interchange fees: the overlooked charges silently eroding your margins each month

Discover five specific cost categories your payment processor may be hiding or downplaying. Learn which line items to audit and how to calculate your true processing costs.

TL;DR

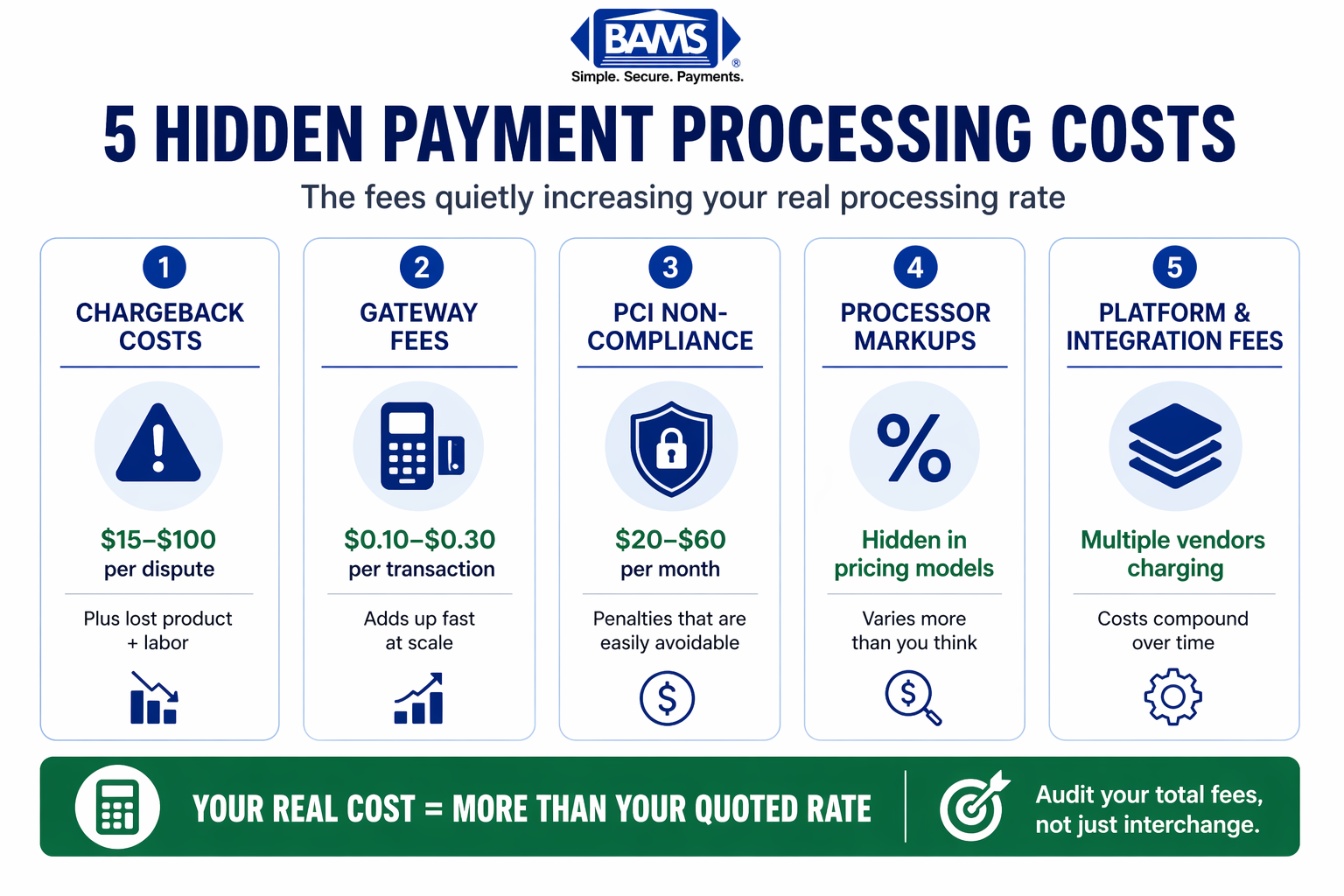

- Chargeback fees multiply fast – Direct costs of $15 to $100 per dispute plus $50 to $150 in operational expenses make each chargeback far more expensive than the fee line item suggests.

- Gateway fees distort your real rate – That $0.10 to $0.30 per-transaction charge can add 0.5% to 1.25% to your effective processing cost, especially on lower-value orders.

- PCI non-compliance costs $240 to $720 yearly – Complete your self-assessment questionnaire to eliminate this avoidable monthly penalty.

- Interchange-plus pricing reveals hidden markups – If your processor uses tiered pricing, you likely overpay on many transaction types without knowing it.

- Calculate your effective rate monthly – Divide total fees by total volume to find your true cost, then compare it to your quoted rate to identify hidden charges.

The Silent Drain on Your Payment Processing Budget

Five hidden payment processing costs that quietly increase your effective rate and reduce your overall profitability.

Your payment processor sends you a statement every month. You glance at the total, wince, and move on. But that number at the bottom? It only tells part of the story.

eCommerce managers like you absorbed much of that increase, often without understanding exactly where the money went.

The visible costs (interchange fees, assessment fees, your merchant discount rate) get most of the attention. But the charges buried in fine print or disguised as “standard” line items can quietly erode margins month after month. Payment processing costs continue to rise as card usage increases, with interchange and related fees forming a significant portion of merchant expenses, as outlined by the Federal Reserve.

This guide exposes five specific cost categories that many payment processors either downplay or fail to explain. These are not theoretical risks. They are active drains on your cash flow right now.

What This Guide Covers (And Who It Serves)

This breakdown targets eCommerce managers at established online businesses processing consistent transaction volume. If you handle payments daily and have felt the sting of unexplained fee increases, this is for you.

We are not covering basic credit card processing fees or rehashing interchange 101. You already know those costs exist. Instead, we focus on the secondary and tertiary charges that compound your true cost of accepting credit cards.

By the end, you will know exactly which line items to audit, which questions to ask your payment processor, and how to calculate whether your current setup is costing more than it should.

How These Costs Were Selected

Each item on this list meets three criteria. First, it appears frequently on merchant statements but rarely gets explained. Second, it scales with transaction volume, meaning it grows as your business grows. Third, it can be reduced or eliminated with the right processor relationship and proactive management.

1. Chargeback Fees That Multiply Beyond the Dispute

Why It Matters

Most eCommerce managers know chargebacks cost money. Few realize how much. PayPal and Stripe typically charge $15 to $20. Visa and Mastercard assessments can push that to $100. Customer disputes often stem from unclear transactions or unrecognized charges, making chargebacks a significant cost driver for merchants as outlined by Visa.

But the direct fee is just the start. Add $50 to $150 in operational expenses per case for investigation, documentation, and response time. Your team spends hours fighting disputes instead of growing revenue.

What It Looks Like Today

Chargebacks will drain $33.79 billion from eCommerce in 2025, climbing to $41.69 billion by 2028. Excessive dispute rates trigger Visa and Mastercard monitoring programs, which impose $5,000 to $25,000 in monthly penalties. Banks processing 10,000 chargebacks monthly face $150,000 to $1 million in direct fees alone.

How to Apply It

Audit your chargeback rate monthly, not quarterly. Request a processor that offers proactive chargeback defense rather than reactive notification. Calculate your true cost per dispute by adding staff time, lost merchandise, and processor fees. If your current provider profits from your chargebacks without helping prevent them, that misalignment costs you money every month.

2. Gateway Transaction Fees That Hide in Plain Sight

Why It Matters

Your payment gateway charges a fee every time a transaction passes through. This seems obvious until you realize these fees often appear separately from your processing rate, making your quoted percentage misleading.

Understanding gateway fees becomes easier when using an integrated payment gateway that consolidates processing, reduces fragmentation, and provides clearer transaction-level cost visibility.

What It Looks Like Today

Many processors bundle gateway fees into a single rate. Others list them separately, creating the illusion of a lower processing percentage. The difference matters most for businesses with high transaction counts and moderate average order values.

How to Apply It

Request a complete fee breakdown from your processor that separates interchange, assessment, gateway, and markup components. Calculate your effective rate by dividing total fees by total processed volume. Compare this number (not the quoted rate) when evaluating payment processor options.

3. PCI Compliance Fees That Penalize Inaction

Why It Matters

Payment Card Industry compliance is mandatory. But many processors charge you whether you comply or not, just in different ways. PCI non-compliance fees run $20 to $60 per month. That is $240 to $720 annually for simply not completing your self-assessment questionnaire.

Some processors also charge PCI compliance fees on top of your compliance efforts, essentially billing you for the privilege of following the rules.

What It Looks Like Today

Compliance requirements have not simplified. Annual questionnaires, quarterly scans, and documentation requirements remain standard. Processors vary widely in how they support (or profit from) your compliance journey.

How to Apply It

Complete your PCI SAQ immediately if you have not already. Ask your processor whether they charge compliance fees, non-compliance fees, or both. Request a processor that includes compliance support in their service rather than treating it as an additional revenue stream.

4. Processor Markups That Compound Invisibly

Why It Matters

Interchange fees go to card-issuing banks. Assessment fees go to card networks. Your processor’s markup is what they keep. This markup determines whether your payment processing is a fair exchange or an ongoing extraction.

Processor markups average around 0.20%, but they vary significantly. Some processors use tiered pricing that obscures their actual margin. Others use interchange-plus pricing that makes their markup transparent.

What It Looks Like Today

Standard payment processing fees range from 1.5% to 3.5% per transaction. Small businesses processing $100,000 to $250,000 annually often pay 2.9% to 4.2%. Medium businesses ($250,000 to $1 million) pay 2.5% to 3.5%. Large businesses ($1 million or more) pay 1.8% to 2.8%. Your processing volume creates leverage. Use it.

Switching to transparent interchange plus pricing allows you to clearly separate network fees from processor markup, eliminating hidden pricing layers and improving cost visibility.

How to Apply It

Request interchange-plus pricing from your processor. This model shows you exactly what the card networks charge and exactly what your processor adds. If your current provider uses tiered or flat-rate pricing, you likely pay more than necessary on many transaction types.

5. Platform and Integration Fees That Scale Against You

Why It Matters

Your eCommerce platform, shopping cart, and payment integrations each take a cut. These fees seem small individually but compound at scale.

The hidden cost here is not just the fee itself. It is the lack of transparency about who charges what and why.

What It Looks Like Today

Modern eCommerce stacks involve multiple vendors.

- Your platform charges a percentage.

- Your payment gateway charges per transaction.

- Your processor charges their markup.

- Your fraud prevention tool charges per scan.

Each vendor optimizes for their revenue, not your total cost.

How to Apply It

Map every fee in your payment stack. Create a simple spreadsheet listing each vendor, their fee structure, and your monthly cost. Look for redundancies (multiple fraud tools, overlapping services) and negotiate with vendors who have competition. Consider processors that bundle services to reduce total vendor count.

The Pattern Across These Costs

These five cost categories share common traits. They all scale with transaction volume, meaning they grow as your business succeeds. They all benefit from opacity, meaning processors profit when you do not understand them. And they all respond to active management, meaning you can reduce them with attention and the right partnerships.

The tradeoff is time versus savings. Auditing your payment stack takes hours. Negotiating with processors takes effort. But the return compounds monthly. A 0.25% reduction on $1 million in annual processing saves $2,500 every year, indefinitely.

These costs also interact. High chargeback rates increase your risk profile, which can increase your processor markup. Poor PCI compliance creates vulnerability, which increases chargeback likelihood. Addressing one category often improves others.

Modern payment infrastructure emphasizes transparency and cost visibility, enabling businesses to better understand and manage their true transaction costs according to Modern Treasury.

Where to Start Without Overwhelming Your Team

A practical checklist to audit your payment processing fees, uncover hidden costs, and reduce your true processing rate.

You cannot fix everything at once. Start with the highest-impact, lowest-effort items.

First, calculate your effective processing rate by dividing last month’s total fees by total processed volume. Compare this to your quoted rate. The gap reveals hidden costs.

Second, audit your chargeback fees specifically. Request a breakdown from your processor showing dispute costs, penalties, and operational expenses. If this number surprises you, prioritize chargeback prevention.

Third, request interchange-plus pricing if you currently use tiered or flat-rate structures. This single change often reduces costs immediately while increasing transparency permanently.

Your payment processor should help you understand and reduce these costs, not profit from your confusion. If your current provider cannot explain every line item on your statement, that gap is costing you money.

Frequently Asked Questions

What are credit card processing fees and why do merchants pay them?

Credit card processing fees cover the cost of moving money from your customer’s bank to yours. They include interchange fees (paid to the card-issuing bank), assessment fees (paid to card networks like Visa and Mastercard), and processor markups (your payment processor’s profit). Merchants pay these fees because card networks require compensation for fraud protection, transaction processing, and the convenience they provide to customers.

How are credit card processing fees determined?

Fees depend on several factors: card type (rewards cards cost more), transaction method (card-present versus online), your industry risk category, and your processing volume. Interchange fees are set by card networks and change twice yearly. Your processor’s markup is negotiable based on your volume and risk profile.

Which types of transactions incur higher processing fees?

Card-not-present transactions (online purchases) cost more than in-person swipes due to higher fraud risk. Rewards cards and corporate cards carry higher interchange rates than basic debit cards. International transactions add cross-border fees. Keyed-in transactions (manually entered card numbers) cost more than chip or contactless payments.

How can businesses minimize their credit card processing fees?

Request interchange-plus pricing for transparency. Negotiate your processor markup based on volume. Reduce chargebacks through better fraud prevention and customer service. Ensure PCI compliance to avoid penalty fees. Encourage debit card or ACH payments when possible. Review statements monthly to catch unexpected fee increases.

What is the difference between interchange-plus and tiered pricing?

Interchange-plus pricing shows you the exact interchange fee plus a fixed processor markup. You see what the card networks charge and what your processor adds. Tiered pricing bundles transactions into categories (qualified, mid-qualified, non-qualified) with different rates. Tiered pricing obscures true costs and typically results in higher fees for most transaction types.

How do chargeback fees impact small and medium businesses?

Beyond the direct fee ($15 to $100 per dispute), chargebacks trigger operational costs ($50 to $150 in staff time per case), lost merchandise value, and potential monitoring program penalties. Excessive chargeback rates can result in $5,000 to $25,000 monthly fines from card networks, account termination, or placement on industry blacklists that prevent you from accepting cards entirely.