Faster eCommerce Deposits: Payment Optimization Guide

How to Optimize Payments for Faster eCommerce Deposits

Actionable strategies to accelerate cash flow without compromising transaction security

Learn why your deposits get delayed and which factors you can control. This guide helps eCommerce managers identify bottlenecks and implement changes that accelerate cash flow.

TL;DR

- Audit your current setup first – Request settlement reports, check batch cutoff times, and verify your merchant category code to identify exactly where delays occur in your specific configuration.

- Improve transaction data quality – Complete billing information, AVS/CVV matching, and Level 2/3 data reduce holds and fraud flags that slow down legitimate transactions.

- Customize risk rules to your business – Generic fraud settings create generic delays. Adjust thresholds based on your actual transaction patterns and build whitelists for repeat customers.

- Optimize operational timing – Align batch submissions with processor clearing cycles. Missing a cutoff by minutes can add a full day to settlement time.

- Negotiate faster funding terms – Next-day funding is available for businesses with stable histories. Businesses can unlock guaranteed next-day funding to reduce delays.

What This Guide Covers

This guide addresses a specific problem: your e-commerce business makes sales, but the money takes too long to reach your bank account. You will learn why deposits get delayed, which factors you can control, and how to implement faster deposit strategies without compromising transaction security.

By the end, you will be able to evaluate your current payment setup, identify bottlenecks causing delays, and implement changes that accelerate cash flow. This guide is for e-commerce managers at established businesses who process enough volume that even small delays create operational friction.

We focus on actionable optimizations, not theoretical frameworks. We will not cover payment gateway selection from scratch or international compliance requirements in depth.

Why Payment Optimization Matters Now

The gap between when you make a sale and when you can use that money creates real business constraints. According to Visa, payment processing involves multiple stages that can introduce delays if not optimized.

The cost of inaction is real. Delayed funds reduce flexibility, slow growth, and create operational friction.

Core Concepts You Need to Understand

The Deposit Timeline

When a customer pays, the money does not move directly to you. It passes through authorization, capture, batching, clearing, and settlement. Each stage introduces potential delays. Understanding where your specific delays occur determines which optimizations matter.

Authorization vs Settlement

Authorization confirms the customer can pay. Settlement moves the actual funds. Many merchants confuse these, assuming an approved transaction means money is coming quickly. The authorization-to-settlement gap is where most delays hide.

Batch Processing Windows

Most processors batch transactions daily. Miss the cutoff time, and your sales wait an extra day before processing even begins. This is controllable but often overlooked.

Risk Scoring and Holds

Processors hold funds when transactions are flagged as risky. According to the PCI Security Standards Council, strong payment environments reduce unnecessary friction and risk exposure.

Common Misconceptions

Faster deposits do not require accepting more risk. The assumption that speed and security trade off against each other is outdated. Modern payment infrastructure allows both when configured correctly.

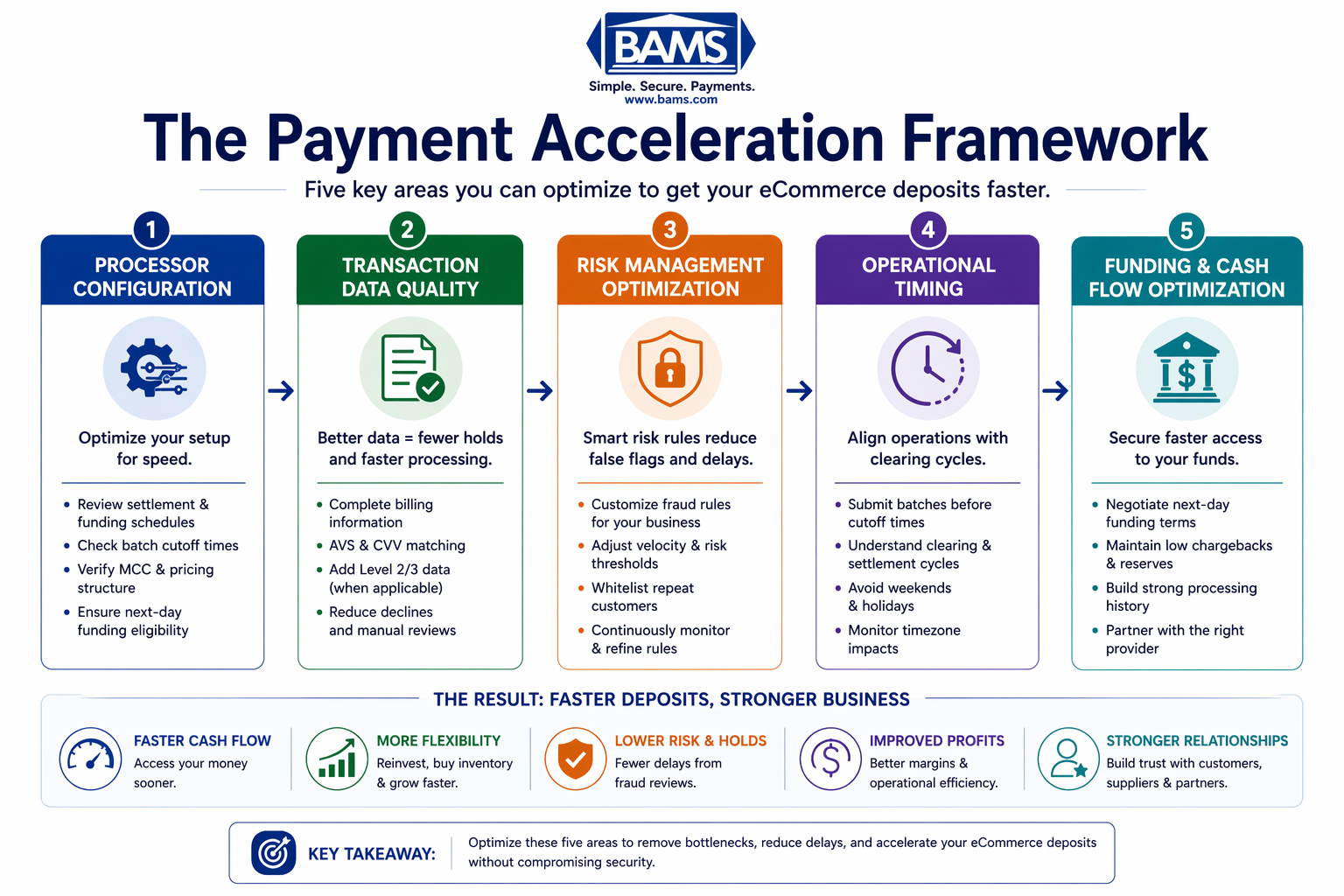

The Payment Acceleration Framework

A structured framework showing how businesses optimize payments across five key areas to achieve faster and more predictable deposit timing.

Optimizing deposit speed requires working across five interconnected areas: processor configuration, transaction quality, risk management, operational timing, and funding arrangements. Weakness in any area limits gains from the others.

The sequence matters. Start with processor configuration (the foundation), then improve transaction quality (reduces holds), implement smart risk management (prevents unnecessary delays), optimize operational timing (captures available speed), and finally negotiate better funding terms (the payoff).

Each stage builds on the previous. Negotiating next-day funding means little if poor transaction quality triggers constant holds. This guide walks through each stage with specific actions.

Step 1: Audit Your Current Processor Configuration

Objective

Identify exactly where delays occur in your current setup and establish a baseline for improvement.

Execution Guidance

Request a detailed settlement report from your processor covering the last 90 days. Map the time from transaction authorization to funds appearing in your bank account for a representative sample of transactions. Look for patterns: do certain transaction types, amounts, or customer profiles consistently take longer?

Check your batch processing cutoff time. If your business peaks in evening hours but your batch closes at 3 PM, you are losing a full day on significant transaction volume. Many processors allow cutoff time adjustments, but you must ask.

Review your merchant category code (MCC). Incorrect classification can trigger additional scrutiny and delays. E-commerce businesses sometimes get miscategorized, adding unnecessary friction.

Anti-Patterns to Avoid

Do not assume your current configuration is optimal because it was set up by professionals. Default settings favor processor convenience, not merchant speed. Do not skip this audit assuming the problem is elsewhere.

Success Indicators

You have documented your average settlement time, identified your batch cutoff, confirmed your MCC is accurate, and created a list of specific configuration changes to request.

Step 2: Improve Transaction Data Quality

Objective

Reduce holds and delays caused by incomplete or suspicious-looking transaction data. Better data reduces fraud flags and improves processing efficiency. According to the Federal Reserve, transaction quality impacts processing cost and efficiency.

Execution Guidance

Implement Address Verification Service (AVS) and CVV matching on all transactions. These basic checks reduce fraud flags that trigger holds. Collect and submit complete billing information, not just the minimum required for authorization.

For B2B transactions, investigate Level 2 and Level 3 data submission. Providing detailed line-item information not only reduces interchange fees but signals legitimacy to processors, reducing scrutiny.

Anti-Patterns to Avoid

Do not collect excessive data that creates checkout friction. Focus on data that processors actually use for risk assessment. Do not assume more fields always mean better outcomes.

Success Indicators

Your authorization rate increases, holds decrease as a percentage of transactions, and you see fewer manual review flags from your processor.

Step 3: Implement Smart Risk Management

Objective

Reduce fraud-related holds without increasing actual fraud losses.

Execution Guidance

Review your processor’s risk rules and adjust thresholds based on your actual fraud patterns, not industry defaults. If you sell low-ticket items with minimal fraud history, aggressive holds on transactions over $100 waste time and money.

Implement velocity checks that match your business reality. A customer ordering five items in one session is normal for your business but might trigger generic fraud rules. Customize these thresholds.

Build a whitelist of repeat customers. Verified buyers should not face the same scrutiny as first-time purchasers. Most processors support customer-level risk scoring that you can influence.

Anti-Patterns to Avoid

Do not disable fraud protection to speed up processing. The goal is smarter protection, not less protection. Do not ignore processor recommendations entirely, as they have visibility into patterns you cannot see.

Success Indicators

Fraud-related holds decrease while actual fraud losses remain stable or decline. Manual review queue shrinks without corresponding increase in chargebacks.

Step 4: Optimize Operational Timing

Objective

Capture every available hour in the settlement cycle through operational adjustments.

Execution Guidance

Align your batch submission with your processor’s optimal windows. If your processor’s clearing cycle starts at 5 PM Eastern, submitting your batch at 4:55 PM gets you into that day’s cycle. Submitting at 5:05 PM pushes everything to tomorrow.

For businesses with significant transaction volume, consider multiple daily batch submissions. Some processors support this, allowing you to clear morning transactions before afternoon sales even complete.

Automate capture for digital goods and services where fulfillment is instant. Delayed capture (common in physical goods shipping) adds settlement time. Where appropriate, capture immediately at authorization.

Anti-Patterns to Avoid

Do not capture transactions before you can fulfill them. This creates chargeback risk and violates card network rules. Do not assume your developer’s default settings optimize for timing.

Success Indicators

Average settlement time decreases by hours or a full day. Weekend transaction settlements shift earlier in the following week.

Step 5: Negotiate Funding Arrangements

Objective

Secure the fastest possible funding terms your business profile supports.

Execution Guidance

With the previous optimizations in place, you have a stronger negotiating position. Your transaction quality is higher, your risk profile is cleaner, and your operational timing is optimized. Use this to negotiate better funding terms.

Guaranteed next-day funding is available from many processors for businesses with stable transaction histories and low chargeback rates. Faster access to funds improves cash flow predictability and enables better business decisions. BAMS offers next-day funding as a standard feature for qualifying merchants, eliminating the typical 2-3 day wait that creates cash flow gaps.

Understand what disqualifies you from faster funding. High chargeback ratios, inconsistent volume patterns, or certain product categories may require additional documentation or gradual qualification.

Anti-Patterns to Avoid

Do not accept faster funding with significantly higher fees without calculating the actual ROI. Do not assume your current processor cannot offer better terms, as many will match competitor offers to retain volume.

Success Indicators

You have documented funding terms, understand qualification requirements, and have a clear path to faster settlement, whether with your current processor or a better alternative.

Step 6: Monitor and Iterate

Objective

Build ongoing visibility into payment performance and continuously optimize.

Execution Guidance

Create a monthly payment performance review. Track authorization rates, settlement times, hold percentages, and funding speed. Look for degradation that signals configuration drift or changing processor behavior.

Compare your metrics against industry benchmarks. While your infrastructure differs, these benchmarks show what modern payment systems can achieve.

Document what works. Payment optimization is not a one-time project. As your business grows, transaction patterns change, and periodic re-optimization captures new opportunities.

Anti-Patterns to Avoid

Do not set and forget. Payment infrastructure changes, processor policies evolve, and your business profile shifts. Static configurations degrade over time.

Success Indicators

You have a recurring review process, documented baseline metrics, and a clear escalation path when performance degrades.

Practical Application: Before and After

Consider a mid-size e-commerce operation processing $500,000 monthly. With standard 2-3 day settlement, approximately $33,000-$50,000 is perpetually in transit. That capital cannot pay suppliers, fund advertising, or earn returns.

After implementing the optimizations above (batch timing adjustment, transaction data improvements, next-day funding negotiation), the same business reduces float to roughly $16,500. The $16,500-$33,500 freed up monthly compounds into significant annual advantage.

The security profile actually improved because better transaction data and smarter risk rules reduced both fraud losses and false positive holds. Speed and security moved together, not against each other.

Common Mistakes That Delay Deposits

Ignoring batch cutoff times. This is the most common and most fixable delay source. Check your cutoff, adjust if possible, and build operations around it.

Accepting default risk settings. Generic fraud rules create generic delays. Your business has specific patterns that warrant specific configurations.

Treating all transactions identically. Repeat customers, high-value orders, and first-time buyers have different risk profiles. Treating them the same leaves speed on the table.

Not asking for better terms. Processors rarely volunteer faster funding. Qualification requirements are often lower than merchants assume, but you must initiate the conversation.

Optimizing in isolation. Fixing batch timing while ignoring transaction quality yields limited results. The framework works as a system.

What to Do Next

Start with the audit. Request your settlement report, document your current batch cutoff, and verify your merchant category code. This takes an afternoon and reveals exactly where your specific delays originate.

From there, work through the framework sequentially. Each stage creates conditions for the next. Rushing to negotiate faster funding before improving transaction quality often fails.

Revisit this guide as your business scales. Transaction patterns that work at $100,000 monthly may need adjustment at $500,000. Cost-effective payment processing is an ongoing practice, not a one-time fix.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies include optimizing batch submission timing, improving transaction data quality to reduce holds, negotiating next-day funding terms, and implementing smart risk management that reduces false positive fraud flags. These strategies work together to minimize the time between customer payment and funds reaching your bank account.

Why is payment optimization important for businesses?

Payment optimization directly impacts cash flow, which affects every operational decision. Money stuck in processing cannot pay suppliers, fund inventory, or support growth initiatives. For e-commerce businesses with tight margins, even one-day improvements in settlement time free up working capital that compounds into significant annual advantage.

How can I improve my payment authorization rates?

Implement Address Verification Service (AVS) and CVV matching, submit complete billing information, and consider Level 2/3 data for B2B transactions. Payment orchestration platforms can dynamically route transactions to best-performing providers, improving authorization rates by 2-3% on average. Better authorization rates mean fewer declined sales and fewer customer recovery efforts.

What role does fraud protection play in payment optimization?

Fraud protection and payment speed are not opposites. Smart fraud protection uses customized risk rules based on your actual business patterns rather than generic industry defaults. This reduces false positive holds that delay legitimate transactions while maintaining or improving actual fraud prevention. The goal is precision, not volume of checks.

Which payment processing fees can I reduce to optimize costs?

Focus on interchange optimization through better transaction data (Level 2/3 processing), pricing model evaluation (interchange-plus often beats flat-rate for established businesses), and chargeback reduction. High chargeback ratios not only incur direct fees but can push you into higher-risk pricing tiers that increase all transaction costs.

When should I consider expanding my payment options?

Expand payment options when data shows cart abandonment at checkout or when entering markets with strong local payment preferences. Businesses offering PayPal see 25% higher conversion rates according to industry research. However, each new payment method adds complexity, so prioritize options your specific customers actually request or that demonstrably reduce abandonment.

Sources