Merchant Services: Why Your Processor Stays Silent

Transaction-level visibility without proactive guidance isn’t transparency — it’s a support gap costing you money

Learn why detailed processing statements don’t equal transparency and what real merchant services accountability looks like. Discover how transaction-level evaluation can uncover savings your processor already sees but never flags.

TL;DR

- Your processor already has the data – Authorization, clearing, and settlement give processors transaction-level visibility long before your monthly statement is generated.

- Statements summarize; they don’t diagnose – Interchange downgrades, card-type mismatches, and missing Level 2/3 data opportunities are invisible in bundled monthly summaries.

- Transaction-level evaluation is an accountability standard – If your processor isn’t proactively flagging savings from the data they already see, that’s a support gap, not a technology limitation.

- Ask better questions – Demand specifics about which transactions downgraded, which card types are driving fees, and whether commercial card volume qualifies for lower rates.

The Statement Arrived. The Answers Didn’t.

Every month, your processing statement lands. Pages of line items, totals, and abbreviations that look like they mean something. You scan the bottom line, compare it to last month, and move on. Most eCommerce managers do exactly the same thing.

But here’s the friction: your processor saw every single transaction before that statement was generated. They watched each authorization, each clearing, each settlement. They had the data. The question is whether they did anything useful with it.

The Myth of the Transparent Statement

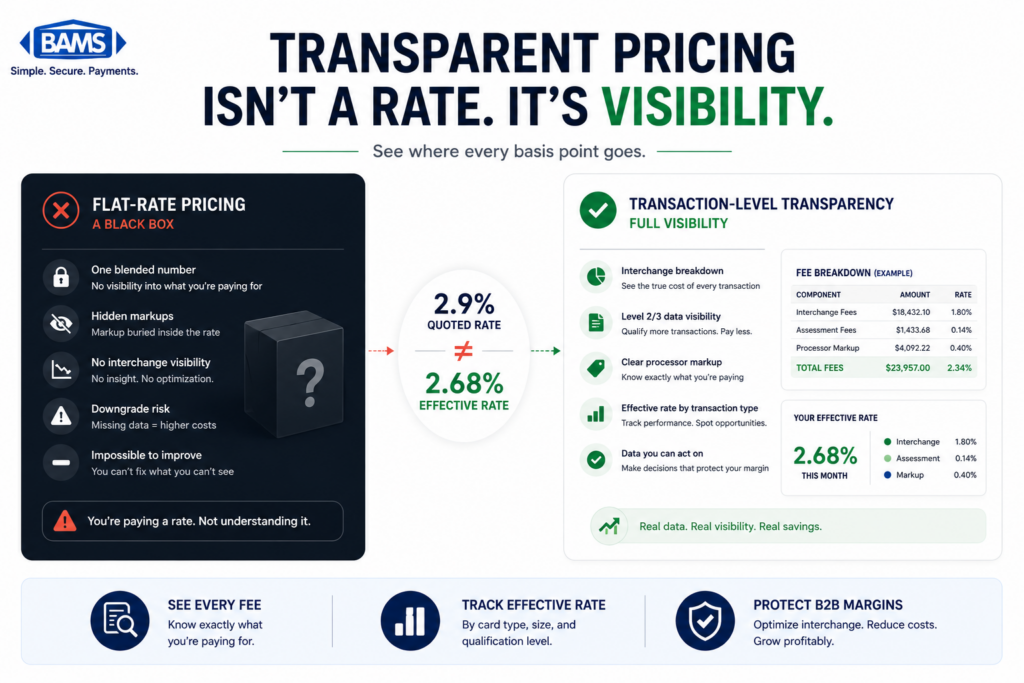

The payments industry has trained merchants to believe that a detailed monthly statement equals transparency. More line items, more columns, more pages. It feels comprehensive. And for a long time, that was enough.

Processors leaned into this. They shipped statements with dozens of interchange categories, batch summaries, and fee breakdowns. The implicit message: “We’re showing you everything.” Merchants accepted it because the alternative (calling and asking) felt worse than squinting at a PDF.

But a summary is not an analysis. A receipt is not a recommendation. The statement tells you what happened. It almost never tells you what should have happened, or what’s costing you money that doesn’t need to.

The Real Problem Is Not Data. It’s Silence.

Here’s what we actually believe: if your processor has transaction-level visibility and isn’t using it to flag savings opportunities, that’s a support gap, not a data gap. The information exists. Someone is choosing not to act on it.

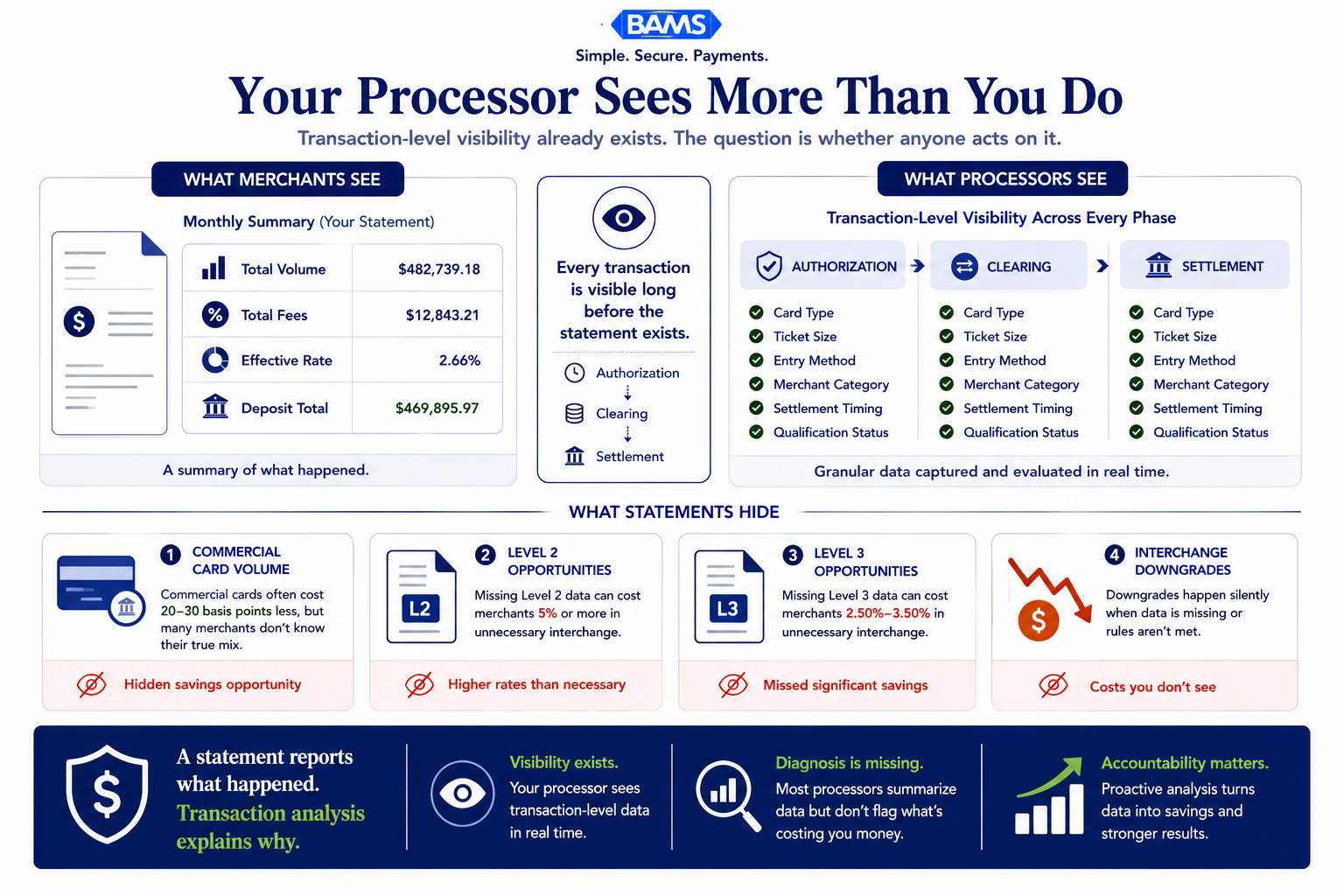

Your monthly statement is a summary. Your processor has already seen every transaction in detail.

What Transaction-Level Evaluation Actually Reveals

To understand why this matters, you need to know what your processor already sees. Visa payment processing resources explain the authorization, clearing, and settlement stages that processors monitor before transactions ever appear on a monthly statement. The credit card payment process has three distinct phases: authorization, clearing, and settlement. At every phase, your processor handles granular transaction data, card type, entry method, ticket size, merchant category, and more. All of this happens before a single line appears on your monthly statement.

That visibility is powerful. The OCC Comptroller’s Handbook identifies exception reporting (comparing merchants against parameters like average ticket size, chargeback activity, and authorization mismatches) as the primary tool for detecting merchant-level anomalies. In other words, regulators already expect processors to use transaction-level data for operational insight. The infrastructure for proactive review exists. It’s standard practice for risk. The question is why it isn’t standard practice for savings.

Consider what a transaction-level evaluation can surface that a bundled statement hides:

- Card-type mix. You might process a meaningful share of commercial or corporate purchasing cards without knowing it. Those transactions are eligible for lower interchange rates through enhanced data programs (Level 2 and Level 3 processing), but only if the right data fields are submitted. If your processor isn’t flagging this, you’re paying consumer-card rates on B2B volume. Visa interchange reimbursement fee schedules show how transaction qualification and enhanced commercial card data can affect interchange costs across different card categories.

- Interchange misqualification. Transactions can “downgrade” to higher-cost interchange tiers for technical reasons: missing data fields, late settlement, or incorrect merchant category codes. These downgrades don’t show up as errors on your statement. They show up as slightly higher fees that compound month after month.

- Fee-type mismatches.Transaction-level payment analytics can detect overpayment drivers like interchange errors and fee-type mismatches that are invisible on a bundled monthly summary. Your effective rate might look reasonable in aggregate while individual transaction categories bleed margin.

The average U.S. merchant pays roughly 2.50% to 3.50% in card processing fees, with per-transaction rates reaching 5% in some cases. Even small shifts in interchange qualification across thousands of monthly transactions add up fast. A 20 or 30 basis point improvement on commercial card volume isn’t a rounding error. For a mid-size eCommerce operation, that’s real margin recovered.

This is where the gap between processor-agnostic gateways and human-first merchant services becomes concrete. A gateway aggregates your transactions and passes them through. A partner like BAMS uses dedicated account management to review that same transaction data and proactively identify where you’re overpaying on interchange, whether you’re missing Level 2 or Level 3 data opportunities, and where hidden fees in merchant services are quietly inflating your effective rate. The difference isn’t access to data. It’s whether anyone on the other end is accountable for doing something with it.

What Changes If You Expect More

If transaction-level evaluation is the standard (and we believe it should be), then several things shift. First, your monthly statement becomes a starting point for conversation, not the end of one. You stop accepting “that’s just what processing costs” because you can see exactly which card types, which interchange tiers, and which data gaps are driving that cost.

Second, you stop treating payment processing costs as fixed overhead. They become variable, improvable, and worth reviewing quarterly with someone who understands your transaction profile. Ecommerce managers who measure success by faster access to funds and reduced processing costs already think this way about logistics and ad spend. Payments deserve the same scrutiny.

Third, you start asking better questions of your processor. Not “can you send me my statement?” but “which of my transactions downgraded last month, and why?” If they can’t answer, that tells you everything about the relationship.

Transparency is not showing data. Transparency is helping merchants act on it.

A New Way to Think About Merchant Services

Stop thinking of your processor as a utility and start thinking of them as an analyst who happens to move money. The data flowing through their systems is a diagnostic tool. Every transaction carries information about how efficiently you’re paying to accept payments.

The reframe is simple: transaction-level evaluation is not a premium feature. It’s an accountability standard. Any processor with settlement-level visibility who doesn’t use it to surface savings is leaving your money on the table and hoping you won’t notice. That’s not a technology limitation. That’s a choice about what kind of support they think you deserve.

Your Statement Is a Receipt. Demand a Diagnosis.

The information to reduce your processing costs already exists inside your transaction data. It’s been there every month. The only variable is whether someone on the other side of that relationship is looking at it, interpreting it, and picking up the phone.

If your current processor has never once called you to say “we noticed something in your transactions that could save you money,” that’s not because there’s nothing to find. It’s because nobody’s looking.

Frequently Asked Questions

What is Level 3 data in merchant services?

Level 3 data refers to detailed, invoice-quality transaction information (line-item descriptions, quantities, tax amounts) submitted during card processing. When this data is included on eligible commercial card transactions, it can qualify for significantly lower interchange rates, reducing your overall payment processing costs.

How do I know if my processor is using my transaction data to find savings?

Ask them directly: “Which of my transactions downgraded last month, and what caused it?” If they can’t answer with specifics about interchange qualification, card-type mix, or data submission gaps, they’re not performing transaction-level evaluation on your behalf.

Do Level 3 data benefits apply to eCommerce businesses, not just large B2B companies?

Yes. Many eCommerce merchants unknowingly process commercial and corporate purchasing card orders from business buyers. Those transactions are eligible for lower interchange rates through enhanced data programs, but only if the right fields are submitted, something a proactive merchant services partner should flag for you.

Sources

- https://corporate.visa.com/en/solutions/acceptance/process-payments.html

- https://usa.visa.com/content/dam/VCOM/download/merchants/visa-usa-interchange-reimbursement-fees.pdf

- https://www.occ.treas.gov/publications-and-resources/publications/comptrollers-handbook/files/merchant-processing/pub-ch-merchant-processing.pdf