7 Signals Slowing Your Deposits: A Cash Flow Management Guide

Diagnose the hidden bottlenecks in your payment pipeline — from batch timing to bank routing mismatches

Learn seven specific signals that quietly delay your merchant funding and what each one reveals about your payment setup. This guide helps eCommerce operators treat cash flow management as an optimizable system rather than a mystery.

TL;DR

- Batch timing is the most common culprit – If your batch closes after your processor’s cut-off window, you lose a full business day on every deposit. Check and adjust this first.

- Funding speed is a chain, not a feature – Your platform, gateway, processor, and bank each have their own timing. The slowest link determines when you get paid.

- Weekend and peak-event sales expose hidden gaps – ACH doesn’t settle on weekends, so your busiest sales periods often produce the longest deposit delays.

- Your bank might be the bottleneck – Not all banks participate in Same-Day ACH or process incoming deposits multiple times per day. Ask yours directly.

- You may be on a slow funding tier without knowing it – Many processors default merchants to 2 to 3 day settlement. Upgrading to next-day funding often requires nothing more than a request.

Why Your Deposits Are Late (and What Each Delay Actually Tells You)

You ran a strong sales day. Transactions cleared. Customers got confirmation emails. But when you check your bank account the next morning, the deposit isn’t there. For eCommerce managers juggling inventory restocks, ad spend, and payroll, delayed merchant funding isn’t just annoying. It’s a drag on every downstream decision your business makes.

Most content about fast funding treats deposit speed as a simple toggle: you either have it or you don’t. That framing misses the real picture. Funding delays are diagnostic. Each one points to a specific bottleneck in your payment pipeline, from batch timing to bank routing to platform configuration. And until you identify which bottleneck is yours, switching processors won’t necessarily fix anything.

This guide surfaces seven signals that quietly slow your deposits and explains what each one reveals about your current setup, so you can treat cash flow management as an optimizable system rather than a mystery.

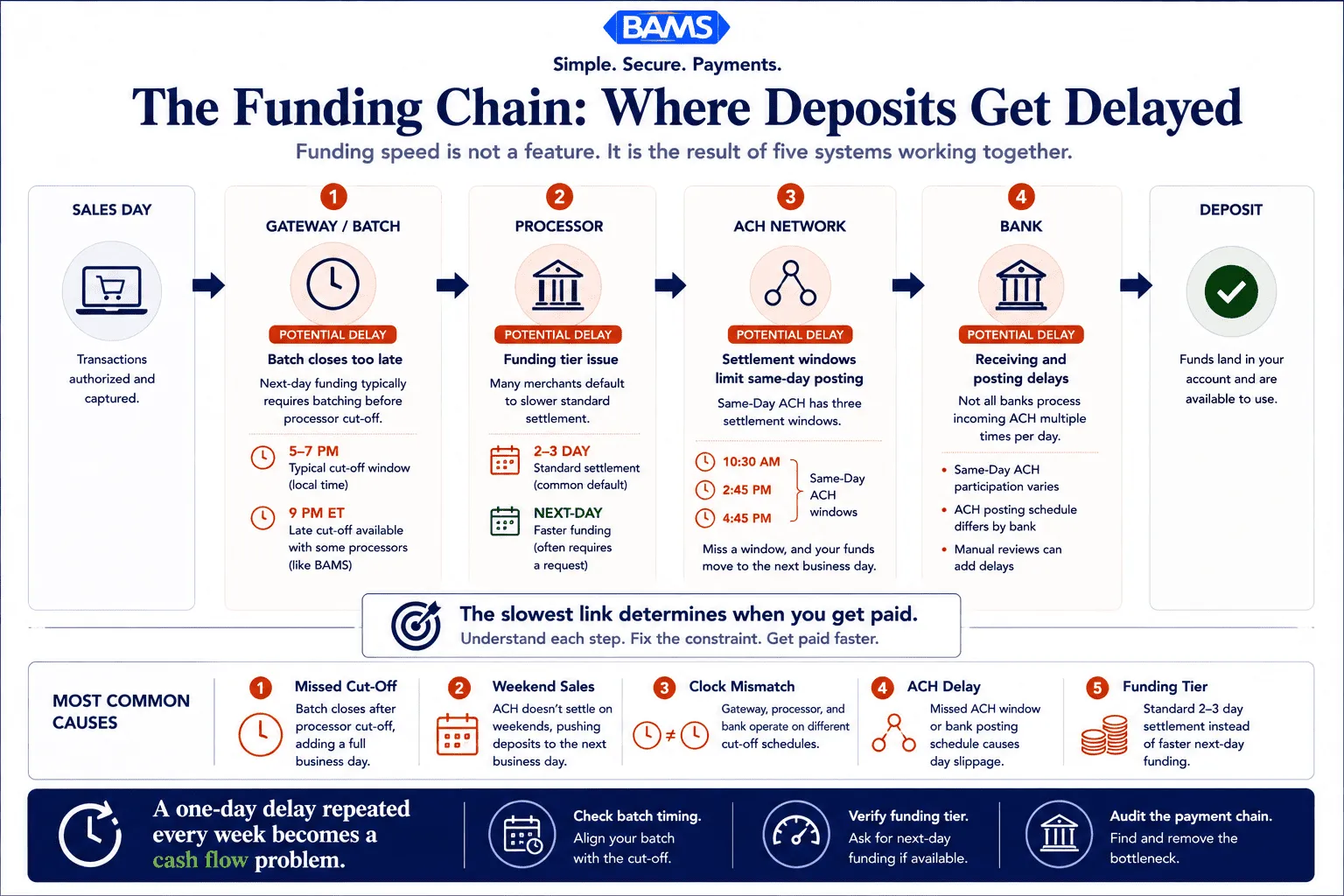

Most businesses blame their processor when deposits are late. In reality, funding speed depends on every link in the payment chain.

Who This Is For (and What We’re Skipping)

This is for eCommerce operators at established businesses processing enough volume that a one-day funding delay has real financial consequences: missed vendor discounts, stalled ad budgets, or manual cash-bridging workarounds. If you’re running 10 to 50 employees and your payment stack touches a gateway, a processor, and a business bank account, these signals apply to you.

We’re not covering basic definitions of ACH or card networks. We’re also not building a generic “benefits of faster funding” list. Instead, every item below isolates a specific mechanical cause of deposit delay and gives you a concrete way to diagnose or resolve it.

How We Selected These Seven Signals

Each signal was chosen because it meets three criteria: it’s common enough to affect a meaningful share of eCommerce merchants, it’s frequently misattributed to “the processor being slow,” and it’s actionable without requiring a full platform migration. The order moves from the most straightforward fixes to the more structural ones.

7 Signals That Quietly Delay Your Merchant Funding

Every funding delay leaves clues. These seven signals help identify where the bottleneck exists.

1. Your Batch Closes After the Processor’s Cut-Off Window

Why it matters: Every processor has a daily cut-off time for batching transactions. If your batch closes after that window, your sales from today don’t enter the settlement queue until tomorrow. That single timing mismatch can add a full business day to every deposit, and most merchants never realize their batch schedule is the cause.

What it looks like today:Next-day funding typically requires batching before a processor cut-off around 5 to 7 PM local time. Some processors offer later windows (BAMS, for instance, provides a 9 PM ET cut-off for next-day funding), but many eCommerce platforms default to midnight batch closings that miss every cut-off. FedNow Service resources continue to demonstrate how faster payment infrastructure and settlement capabilities are reshaping expectations around funding speed and liquidity access for merchants.

How to apply it: Log into your gateway or processor dashboard and find your batch settlement time. Compare it to your processor’s published cut-off. If your batch closes after the cut-off, adjust it to close 30 to 60 minutes before. This single change often eliminates a full day of delay with zero cost.

2. Weekend and Holiday Sales Pile Up Without a Settlement Path

Why it matters: Ecommerce doesn’t pause on weekends, but ACH settlement does. If your peak sales volume lands on Friday evening through Sunday (common for DTC brands running weekend promotions), those transactions sit in limbo until the next business day. For high-volume events, that can mean three days of revenue stacked into a single deposit, distorting your cash flow visibility.

What it looks like today:ACH payments typically clear in 1 to 3 business days, and “business days” excludes weekends and federal holidays. Merchants who run flash sales on Fridays often see deposits arrive Tuesday or Wednesday. NACHA ACH Network resources explain how ACH settlement schedules and business-day processing windows directly affect when merchants receive funds.

How to apply it: Map your weekly sales volume by day. If weekends account for a disproportionate share, factor the settlement gap into your cash flow projections. Consider processors that offer weekend or holiday deposit support, and time your largest ad spend or inventory purchases to align with mid-week deposit arrivals rather than assuming daily consistency.

3. Your Gateway and Processor Are on Different Clocks

Why it matters: Many eCommerce businesses use a third-party gateway (Stripe, Authorize.net, etc.) that connects to a separate acquiring processor. Each system has its own batch timing, reconciliation cycle, and time zone configuration. When these clocks don’t align, a transaction captured at 6 PM in your gateway might not reach the processor’s queue until the following morning.

What it looks like today: This is especially common in businesses that migrated platforms or added a new gateway without reconfiguring settlement schedules. The delay appears intermittent because it only affects transactions processed in the gap between the two systems’ cut-offs.

How to apply it: Document the batch close time and time zone for both your gateway and your processor. If there’s a mismatch, adjust the gateway’s batch schedule to close at least one hour before the processor’s cut-off. If your gateway doesn’t allow custom batch timing, escalate with their support team or evaluate whether a more tightly integrated stack would remove the gap.

4. Your Bank’s Receiving Window Doesn’t Match the Payment Rail

Why it matters: Even after your processor releases funds, your bank has to receive and post them. Not all banks process incoming ACH at the same speed. Some smaller banks or credit unions only process ACH files once per day, meaning a deposit that arrives at 3 PM might not post until the next morning’s processing run.

What it looks like today:Same-Day ACH operates across three processing windows with cut-offs at 10:30 AM, 2:45 PM, and 4:45 PM ET. If your processor sends funds via the third window but your bank doesn’t participate in same-day ACH receiving, the deposit rolls to the next standard cycle. FedNow participating organizations provide visibility into which financial institutions have adopted faster payment capabilities, helping merchants evaluate whether their banking partner may be contributing to funding delays.

How to apply it: Contact your business bank and ask two specific questions: Do you participate in Same-Day ACH receiving? How many ACH processing runs do you execute per day? If the answers reveal a bottleneck, consider whether your banking relationship is costing you a day of float on every deposit.

5. High-Ticket or Unusual Transactions Trigger Funding Holds

Why it matters: Processors use risk algorithms that can flag individual transactions or entire batches for manual review. A single high-ticket order, a spike in volume during a sale event, or a sudden increase in international cards can trigger a temporary hold on your entire batch. You won’t always get notified, and the delay can look identical to a normal settlement lag.

What it looks like today: This is particularly common during product launches, seasonal sales, or any event that deviates from your “normal” processing pattern. Merchants often blame the bank or the payment network when the hold originates at the processor level. Understanding how your processor handles funding holds is critical to avoiding surprise delays.

How to apply it: Before any major sale event, notify your processor in advance with expected volume and average ticket size. Ask whether your account has auto-hold thresholds and what triggers them. Processors with dedicated account management (like BAMS) can often pre-authorize higher volumes so your deposits flow without interruption during peak periods.

6. Your Reconciliation Data Has Mismatches That Stall Settlements

Why it matters: Settlement isn’t just about moving money. It requires matching transaction data across your platform, gateway, processor, and bank. Mismatched merchant IDs, inconsistent descriptor names, or incorrect routing numbers can cause a batch to fail validation, sending it back for correction. Experts recommend validating routing and account numbers before approval to prevent exactly this kind of silent delay.

What it looks like today: Data mismatches often surface after a platform migration, a bank account change, or when a business adds a new sales channel. The deposit doesn’t fail visibly. It just takes an extra day while the system resolves the discrepancy.

How to apply it: Audit your settlement chain quarterly. Verify that the bank account and routing number on file with your processor match your current business account exactly. Confirm that your merchant ID and business descriptor are consistent across all channels. One mismatched digit can add 24 hours to every deposit cycle.

7. You’re on a Standard Funding Tier Without Knowing It

Why it matters: Many processors default new merchants to a standard 2 to 3 day funding cycle. Upgrading to next-day or same-day funding is often available but requires an explicit request, a different pricing tier, or meeting specific volume thresholds. Merchants who never ask stay on the slow track indefinitely, paying the same rates but receiving funds later.

What it looks like today:NACHA raised the Same-Day ACH per-payment cap to $1 million in 2022, expanding the range of transactions eligible for faster rails. Yet many processors haven’t proactively migrated existing merchants to faster tiers. The capability exists, but it’s opt-in.

How to apply it: Call your processor and ask what funding tier your account is on. Ask what’s required to move to next-day funding. Compare the cost (if any) against the value of accessing your revenue one to two days sooner. For many established eCommerce businesses, the math strongly favors the upgrade. Some providers, like BAMS, include next-day funding at no additional fee, which eliminates the cost question entirely.

The Pattern Behind These Delays

Look across all seven signals and a clear theme emerges: funding speed is not a single feature. It’s the output of a chain with at least four links (platform, gateway, processor, bank), and the weakest link sets the pace. Most merchants optimize only one link (usually by choosing a processor that advertises fast funding) while ignoring the others.

The second pattern is that delays compound during the moments that matter most. Weekend surges, sale events, and seasonal peaks are exactly when cash flow management is most critical, and exactly when these bottlenecks hit hardest. A system that works fine on a normal Tuesday can fall apart during Black Friday weekend.

The third insight is that many of these delays are invisible by design. You don’t get an error message when your batch misses a cut-off. Your bank doesn’t alert you that it only processes ACH once daily. The absence of a notification is itself a problem worth solving.

Where to Start: Prioritizing Your Fixes

You don’t need to address all seven signals at once. Start with the two that require the least effort and yield the most immediate results: check your batch close time (Signal 1) and confirm your funding tier (Signal 7). Both can be resolved with a single phone call or dashboard adjustment.

Next, audit your bank’s ACH receiving capabilities (Signal 4) and your gateway-processor timing alignment (Signal 3). These require slightly more investigation but often reveal the root cause of “random” one-day delays that have persisted for months.

Save the structural items (Signals 5 and 6) for your next quarterly review or before your next major sale event. The goal isn’t perfection. It’s turning your funding pipeline from a black box into a system you understand and can tune as your business grows.

Frequently Asked Questions

What is next-day funding in merchant services?

Next-day funding means your processor deposits the proceeds from your card transactions into your business bank account by the next business day. Instead of waiting 2 to 3 days for settlement, you access your revenue roughly 24 hours after the batch closes. Eligibility often depends on batch timing, account history, and your processor’s specific cut-off windows.

Why is next-day funding important for small businesses?

Faster access to revenue lets you cover payroll, restock inventory, and fund marketing without bridging gaps with credit lines or personal capital. For businesses operating on tight margins, even a one-day improvement in deposit timing can reduce reliance on short-term borrowing and improve overall cash flow predictability.

How can a business qualify for next-day funding?

Requirements vary by processor, but common qualifications include a minimum processing history (typically 3 to 6 months), consistent transaction volume, low chargeback rates, and batching before the processor’s daily cut-off time. Some processors require a specific pricing tier, while others include next-day funding as a standard feature for qualifying merchants.

What are the differences between same-day funding and next-day funding?

Same-day funding deposits your transaction proceeds on the same business day the batch is submitted, provided it’s processed before an earlier cut-off (often mid-afternoon ET). Next-day funding deposits arrive the following business day, with later cut-off windows (often 5 to 9 PM). Same-day funding typically costs more and has stricter timing requirements, while next-day funding offers a practical balance of speed and flexibility for most eCommerce businesses.

Which factors affect the speed of merchant funding?

Several factors interact: your batch settlement time, your processor’s cut-off window, the payment rail used (standard ACH vs. Same-Day ACH), your bank’s ACH receiving schedule, risk holds triggered by unusual transaction patterns, and data accuracy across your gateway and processor. A delay at any single point in this chain adds time to your deposit.

Do weekend sales affect when I receive my deposits?

Yes. ACH settlement does not occur on weekends or federal holidays. Transactions processed Friday evening through Sunday typically don’t enter the settlement queue until Monday, with deposits arriving Tuesday or later. For eCommerce businesses with strong weekend sales, this creates a recurring cash flow gap that should be factored into weekly financial planning.