5 Hidden Payment Processing Costs Draining Profits

Hidden payment processing costs can significantly impact profitability for eCommerce merchants. While most businesses focus on interchange and headline rates, additional fees often accumulate unnoticed. As a result, merchants may pay more than expected without understanding why. By identifying these hidden costs, businesses can improve pricing accuracy, strengthen margins, and gain better control over payment operations.

Key Takeaways

- Hidden fees can increase your effective processing rate beyond quoted pricing.

- Chargebacks, gateway fees, and compliance penalties are common cost drivers.

- Processor markup transparency is essential for accurate cost control.

- Regular audits help merchants identify and eliminate unnecessary charges.

- Understanding total payment costs improves long-term profitability.

The Silent Drain on Payment Processing Costs

Most merchants review their monthly statement and focus on the total amount. However, that number often includes multiple hidden fees that are not immediately obvious. Therefore, relying only on headline rates can lead to inaccurate cost assumptions.

According to the Merchant Payments Coalition, U.S. merchants paid over $236 billion in card processing fees in 2024. As payment volume increases, these hidden costs scale alongside revenue.

In addition, the Federal Reserve highlights how interchange structures contribute to overall payment costs, reinforcing why merchants must evaluate total processing expenses beyond headline rates.

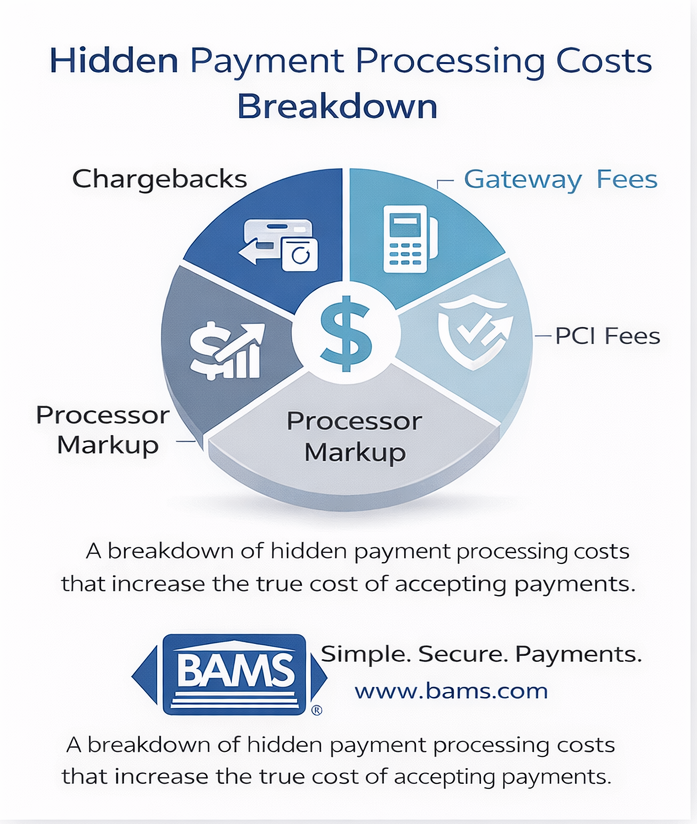

Hidden Payment Processing Costs: What to Look For

The diagram below highlights the most common hidden payment processing costs that merchants overlook.

1. Chargeback Costs Beyond the Fee

Chargebacks create more than a single fee. While processors may charge $15 to $100 per dispute, the total cost includes operational time, lost revenue, and potential penalties.

In addition, high dispute rates can trigger monitoring programs from card networks. The PCI Security Standards Council emphasizes the importance of secure payment practices to reduce fraud and disputes.

Merchants can reduce exposure by implementing strong dispute management processes and working with providers that offer proactive chargeback defense solutions.

2. Gateway Fees That Increase Your Effective Rate

Gateway fees typically apply per transaction and may not appear in quoted processing rates. Therefore, these fees can increase your effective rate, especially for lower-value transactions.

For example, a $0.25 fee on a $25 order adds 1% to the total cost. As transaction volume grows, this impact becomes more significant.

3. PCI Compliance and Non-Compliance Fees

Many processors charge monthly fees related to PCI compliance. If merchants fail to complete required assessments, they may incur additional non-compliance penalties.

Therefore, maintaining compliance not only reduces risk but also eliminates avoidable costs. Proper compliance management ensures secure handling of payment data and supports long-term operational stability.

4. Processor Markups That Lack Transparency

Processor markup represents the portion of fees retained by your payment provider. However, some pricing models obscure this markup, making it difficult to understand true costs.

For example, tiered pricing bundles transactions into categories without clearly showing actual interchange rates. In contrast, interchange-plus pricing provides full transparency.

Merchants evaluating providers should consider working with established partners such as BAMS merchant services to improve cost visibility and pricing structure.

5. Platform and Integration Fees

Modern payment systems often involve multiple vendors, including ecommerce platforms, gateways, and fraud tools. Each provider may charge separate fees.

As a result, total costs can increase without clear visibility. Therefore, merchants should map all vendors and associated fees to identify redundancies and optimization opportunities.

Framework: How Hidden Costs Impact Your Business

| Cost Type | Impact Area | Business Effect |

|---|---|---|

| Chargebacks | Risk & Operations | Higher labor costs and penalties |

| Gateway Fees | Transaction Costs | Higher effective processing rate |

| PCI Fees | Compliance | Recurring penalties if unmanaged |

| Processor Markup | Pricing | Reduced margin visibility |

| Platform Fees | Technology Stack | Compounding vendor costs |

How to Reduce Hidden Payment Processing Costs

Merchants can take several steps to reduce unnecessary fees and improve cost control.

- Calculate your effective rate monthly (total fees ÷ total volume)

- Request a full fee breakdown from your processor

- Switch to transparent pricing models such as interchange-plus

- Monitor chargeback ratios and implement prevention tools

- Complete PCI compliance requirements to avoid penalties

By taking these steps, merchants can improve cost visibility and make more informed decisions about payment strategy.

Conclusion

Hidden payment processing costs often have a greater impact than visible fees. While interchange and base rates receive the most attention, additional charges can quietly reduce profitability.

Therefore, merchants should review their payment structure regularly, identify hidden costs, and work with transparent providers. A proactive approach to payment cost management leads to better margins, improved operational control, and long-term financial stability.

Frequently Asked Questions

What are hidden payment processing costs?

They are additional fees beyond standard processing rates, including chargebacks, gateway fees, compliance penalties, and platform costs.

How do I calculate my true processing cost?

Divide total fees by total processed volume to determine your effective rate.

Can hidden fees be eliminated?

Some can be reduced or eliminated through better pricing models and operational improvements.

Why do processors include hidden fees?

Some pricing models bundle or separate fees in ways that reduce transparency and increase revenue.

How often should I review my payment costs?

Merchants should review their statements monthly to identify changes and unexpected charges.