How to Reduce Processing Fees: 7 Proven Tactics

Actionable strategies to cut your effective rate and reclaim thousands in annual overhead

Learn seven specific tactics to lower your payment processing costs, from choosing transparent pricing models to optimizing transaction routing. These strategies help eCommerce managers reduce effective rates and eliminate hidden charges.

TL;DR

- Switch to interchange-plus pricing to see exactly what you pay and eliminate overpayment on debit transactions

- Optimize transaction data by including complete billing information to qualify for lower interchange categories

- Audit your statements for hidden fees like PCI non-compliance charges, statement fees, and unnecessary monthly minimums

- Encourage debit and ACH payments to shift your payment mix toward methods costing 0.3% versus 1.8%

- Negotiate annually using your volume growth and clean processing history as leverage for better rates

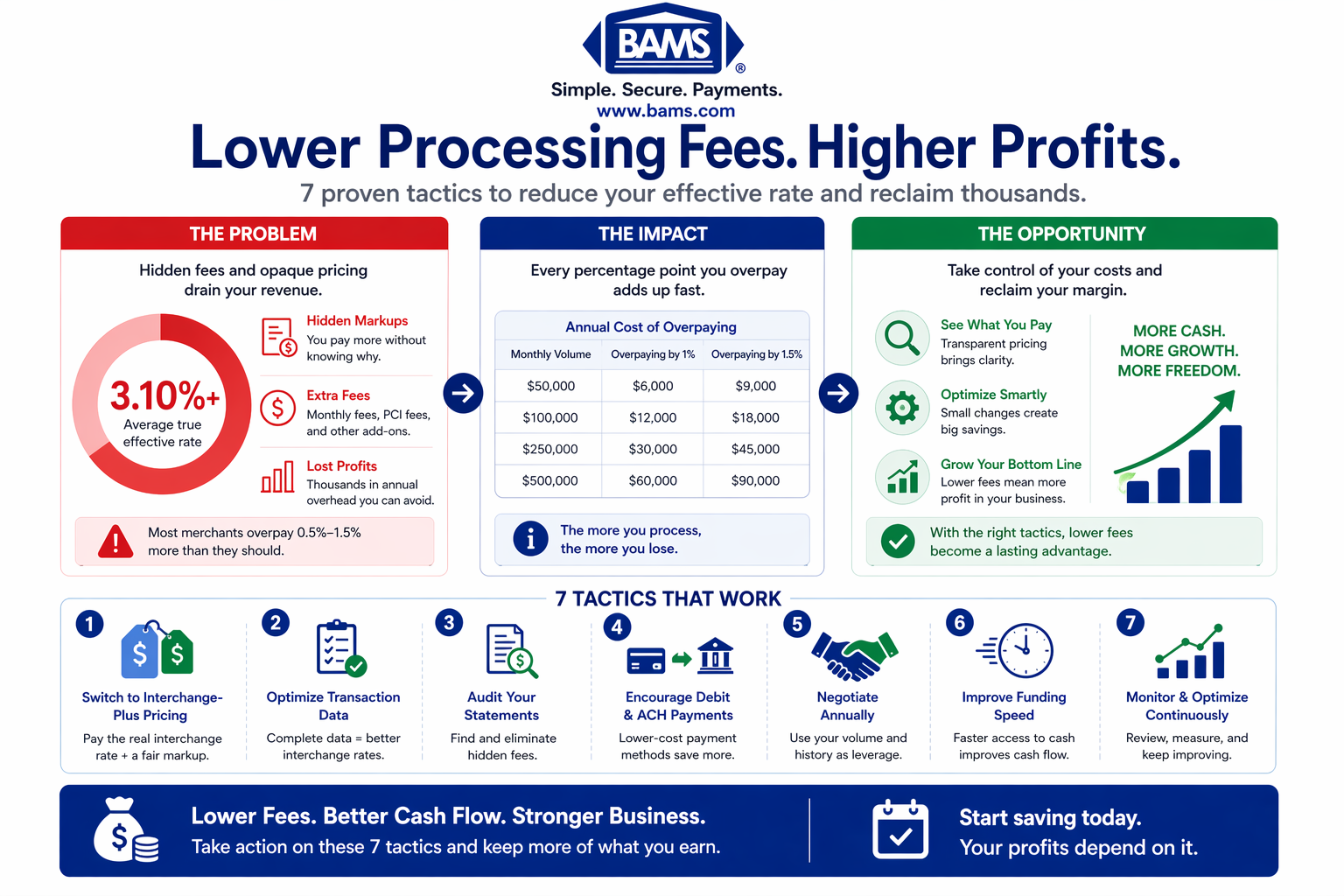

The Hidden Drain on Your Cash Flow

Processing fees quietly consume a significant portion of your revenue. According to the Federal Reserve, interchange structures significantly influence the total cost merchants pay per transaction, making fee optimization essential for profitability. For eCommerce managers processing substantial monthly volume, these fees compound into tens of thousands in annual overhead.

The challenge extends beyond the headline rate. Hidden markups, statement fees, and PCI non-compliance charges push true effective rates to 3.10% or higher for businesses that assume their advertised 2.9% + $0.30 rate tells the whole story. Meanwhile, larger merchants negotiate rates nearly half that amount through strategic pricing models and volume leverage.

This gap represents an opportunity. Understanding how to reduce processing fees starts with recognizing that your current costs likely include unnecessary markup, and that transparency pricing for processing exists as a viable alternative to opaque fee structures.

Hidden fees and opaque pricing increase your effective rate, but small optimizations can significantly reduce costs and improve profit margins.

What This Guide Delivers

This listicle targets eCommerce managers at established online businesses who process enough volume to make fee optimization worthwhile. You will find seven specific strategies that reduce your effective rate, improve cash flow predictability, and eliminate surprise charges.

This is not a guide to switching payment gateways or negotiating with card networks directly. Instead, these tactics focus on decisions within your control: pricing model selection, transaction optimization, and proactive fee management. Each strategy includes current implementation methods and realistic constraints.

How These Strategies Were Selected

Each tactic meets three criteria: it produces measurable savings, it applies to businesses processing $50,000+ monthly, and it requires no specialized technical infrastructure. Strategies that only benefit enterprise-level merchants or demand significant capital investment were excluded.

1. Switch to Interchange-Plus Pricing

Why It Matters

Flat-rate pricing models charge the same percentage regardless of card type, meaning you overpay on debit transactions and lower-risk purchases. Interchange-plus pricing separates the actual interchange cost from your processor’s markup, giving you visibility into exactly what you pay and why.

What It Looks Like Today

Small merchants under $1M annual volume often pay effective rates of 3.2% to 4.0% on flat-rate plans. Merchants who switch to interchange-plus typically see rates drop to 2.0% to 2.5%, with the savings increasing as volume grows. A payment processing fee calculator can model your specific savings based on transaction mix.

How to Apply It

Request a detailed statement analysis from a processor offering transparency pricing for processing. Compare your current effective rate (total fees divided by total volume) against quoted interchange-plus rates. Prioritize processors who disclose their markup separately from interchange costs.

2. Optimize for Lower Interchange Categories

Why It Matters

Interchange fees vary significantly based on how transactions are processed. Card-present transactions cost less than card-not-present. Providing complete transaction data (address verification, CVV, invoice numbers) qualifies purchases for lower-cost categories.

What It Looks Like Today

Ecommerce transactions that fail to include AVS matching or complete billing data often “downgrade” to higher interchange tiers. B2B merchants who submit Level II or Level III data (tax amounts, customer codes, line-item details) access interchange rates 0.5% to 1.0% lower than standard eCommerce rates.

How to Apply It

Audit your transaction data completeness. Ensure your checkout captures billing address, CVV, and customer email for every order. If you sell to businesses, ask your processor about Level II/III data submission. The technical lift is modest; the savings compound monthly.

3. Reduce Chargebacks Before They Happen

Why It Matters

Each chargeback costs $20 to $100 in fees, plus the lost transaction amount, plus potential rate increases if your chargeback ratio exceeds 1%. Proactive defense costs far less than reactive dispute management.

What It Looks Like Today

Modern chargeback prevention combines clear billing descriptors, automated delivery confirmation, and real-time fraud scoring. Processors with dedicated chargeback defense teams intervene before disputes escalate, often resolving issues through representment or pre-dispute alerts.

How to Apply It

Review your billing descriptor (the name appearing on customer statements) for clarity. Implement order confirmation emails with tracking information. Partner with a processor that offers proactive chargeback support rather than charging fees after disputes occur.

4. Negotiate Based on Volume and History

Why It Matters

Your processing history, chargeback ratio, and average ticket size all provide leverage, but only if you ask.

What It Looks Like Today

Processors evaluate risk based on historical data. A clean processing record with low chargebacks and consistent volume justifies lower rates. Many merchants never request rate reviews, leaving savings on the table as their businesses grow.

How to Apply It

Schedule annual rate reviews with your processor. Prepare documentation showing volume growth, low chargeback ratios, and consistent processing patterns. If your current processor refuses to negotiate, use their quote as leverage with alternatives offering transparency pricing for processing.

5. Eliminate Hidden Fees Through Statement Audits

Why It Matters

Statement fees, batch fees, PCI non-compliance fees, and monthly minimums add 0.2% to 0.5% to your effective rate. Many merchants pay these charges for years without questioning their necessity.

What It Looks Like Today

A typical merchant statement includes 15 to 25 line items beyond interchange and processor markup. PCI non-compliance fees ($19 to $99 monthly) often persist even after compliance is achieved. Statement fees ($5 to $15) charge for paper statements you may not receive.

How to Apply It

Request a line-by-line explanation of every fee on your statement. Confirm PCI compliance status and demand removal of non-compliance fees if compliant. Opt into electronic statements to eliminate paper fees. Use a payment processing fee calculator to quantify the annual impact of each charge.

6. Encourage Debit and ACH Payments

Why It Matters

ACH transfers cost significantly less than card payments. The NACHA ACH Network supports low-cost electronic transfers, making ACH a powerful option for reducing overall processing fees.

Shifting payment mix toward lower-cost methods produces immediate savings.

What It Looks Like Today

Subscription businesses and B2B merchants increasingly offer ACH as the default payment method, with credit cards as a secondary option. Some merchants provide small discounts (1% to 2%) for ACH payments, passing a portion of savings to customers while retaining the rest.

How to Apply It

Add ACH payment options to your checkout for customers with recurring purchases or high-ticket orders. Consider cash discount programs that incentivize lower-cost payment methods. For B2B transactions, position ACH as the standard with credit cards available for convenience.

7. Accelerate Funding to Improve Cash Flow

Why It Matters

While not a direct fee reduction, faster access to funds reduces your reliance on credit lines and improves working capital efficiency. The effective cost of waiting 3 to 5 days for deposits compounds when you factor in interest on borrowed capital or missed inventory opportunities.

What It Looks Like Today

Standard processing deposits funds in 2 to 3 business days. Guaranteed next-day funding options exist without additional fees depending on your provider. Some processors include next-day funding as a standard feature, eliminating the tradeoff between speed and cost.

How to Apply It

Calculate your current cost of delayed deposits (interest on credit lines, missed early-payment discounts from suppliers). Compare processors offering next-day funding without additional fees. Factor funding speed into your total cost of processing, not just the per-transaction rate.

Patterns Across These Strategies

Applying these seven tactics consistently can lower your effective processing rate, improve cash flow, and increase long-term profitability.

Three themes connect these tactics. First, transparency compounds savings. Processors who hide fees in bundled rates have no incentive to reduce them. Interchange-plus pricing, detailed statements, and clear markup disclosure create accountability.

Second, prevention beats reaction. Optimizing transaction data, defending chargebacks proactively, and auditing statements regularly cost less than accepting default rates and disputing errors after the fact.

Third, leverage accumulates. Volume growth, clean processing history, and demonstrated knowledge of how to reduce processing fees all strengthen your negotiating position. Each improvement makes the next easier to achieve.

Where to Start

You do not need to implement all seven strategies simultaneously. Begin with the highest-impact, lowest-effort changes: request a statement audit, confirm your pricing model, and verify PCI compliance status. These three actions typically reveal 0.3% to 0.5% in immediate savings.

Next, evaluate your transaction data quality and chargeback prevention processes. These require modest operational changes but produce ongoing savings that compound monthly.

Finally, use your improved metrics to negotiate better rates or evaluate processors offering transparency pricing for processing as a standard feature. The goal is not perfection but consistent improvement, turning payment processing from a cost center into a predictable, optimized operation.

Frequently Asked Questions

How do I calculate my true effective processing rate?

Divide your total processing fees (all line items, not just the advertised rate) by your total processing volume for the same period. For example, if you processed $100,000 and paid $3,100 in total fees, your effective rate is 3.1%. Compare this to your advertised rate to identify hidden costs.

What is the difference between interchange-plus and flat-rate pricing?

Flat-rate pricing charges the same percentage regardless of card type (typically 2.9% + $0.30). Interchange-plus separates the actual interchange cost from the processor’s markup, so you pay less on debit cards and lower-risk transactions. Most businesses processing over $10,000 monthly save money with interchange-plus.

How much can I realistically save by switching pricing models?

Merchants switching from flat-rate to interchange-plus typically reduce effective rates by 0.5% to 1.0%. On $100,000 monthly volume, that translates to $500 to $1,000 in monthly savings. Savings increase with higher debit card usage and larger average transaction sizes.

What are the most common hidden fees on processing statements?

Common hidden fees include PCI non-compliance fees ($19 to $99 monthly), statement fees ($5 to $15), batch fees ($0.10 to $0.30 per batch), monthly minimums, and annual fees. These charges often persist even when they no longer apply, such as non-compliance fees after achieving compliance.

How often should I review my processing rates?

Conduct a comprehensive rate review annually, or whenever your monthly volume increases by 25% or more. Volume growth, improved chargeback ratios, and consistent processing history all provide leverage for negotiating better rates.

Does next-day funding cost extra?

Many processors charge 0.5% to 1.0% for next-day funding as an add-on service. However, some processors include next-day funding as a standard feature at no additional cost.

Factor funding speed into your total cost of processing, not just the per-transaction rate. As explained by Modern Treasury, improved payment operations and visibility help businesses manage liquidity more effectively.