OptBlue American Express Explained: Fees, Benefits & Setup

OptBlue American Express Explained: Fees, Benefits, Costs, and Merchant Strategy

The OptBlue American Express program has significantly reshaped how small and mid-sized businesses accept American Express payments. Historically, many merchants avoided Amex due to higher fees, separate agreements, and slower settlement timelines. However, OptBlue changed that model by integrating American Express into standard merchant processing environments.

Today, businesses can accept Amex alongside Visa, Mastercard, and Discover through a single provider. As a result, merchants gain operational efficiency, faster funding, and broader customer reach. However, while OptBlue simplifies acceptance, it also introduces new pricing structures and strategic considerations.

Understanding how OptBlue works—and how it impacts your cost structure—is essential for making informed decisions about your payment infrastructure.

Key Takeaways

- OptBlue allows merchants to accept American Express through their existing processor.

- It simplifies operations by combining settlement, reporting, and billing.

- Processors control pricing, which creates both flexibility and variability.

- Best suited for businesses processing under $1M annually in Amex volume.

- Requires evaluation of long-term costs, not just initial convenience.

What Is OptBlue American Express?

OptBlue American Express is a payment processing program that allows merchants to accept American Express cards without signing a direct agreement with Amex. Instead, merchants work through a payment processor that handles onboarding, pricing, and settlement.

Previously, businesses needed a separate contract with American Express. This created operational complexity and discouraged smaller merchants from accepting Amex. OptBlue eliminates that barrier by bundling Amex into a unified payment system.

According to Visa’s payment processing framework, modern payment systems rely on seamless integration between authorization, settlement, and reporting. OptBlue aligns with this model by streamlining all card types into one workflow.

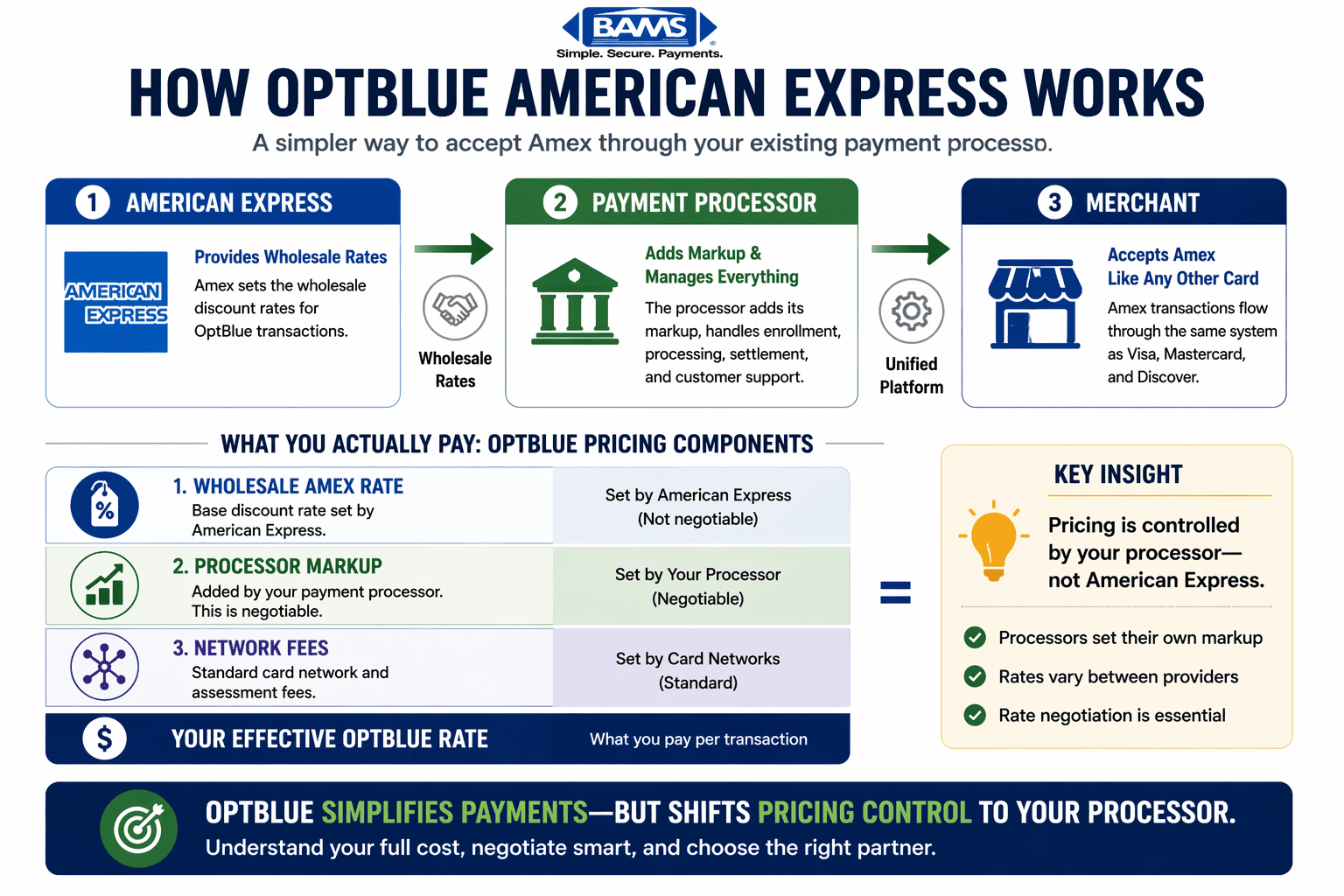

How OptBlue Works

A simplified breakdown of how OptBlue works, illustrating the relationship between American Express, payment processors, and merchants, along with key pricing layers.

1. Enrollment Through a Processor

Merchants enroll in OptBlue through a participating provider. This removes the need for direct negotiation with American Express.

2. Wholesale Pricing + Markup

American Express provides wholesale rates to processors. The processor then applies a markup, which becomes the merchant’s effective rate.

3. Unified Payment Flow

Transactions are authorized, settled, and reported alongside other card brands. This results in one statement, one deposit stream, and one support channel.

As a result, accounting becomes simpler and operational overhead is reduced.

Why OptBlue Was Introduced

American Express historically operated under a closed-loop model. While this structure provided control, it limited merchant adoption due to higher costs and complexity.

OptBlue was introduced to increase acceptance among small and mid-sized businesses. By allowing third-party processors to manage pricing and onboarding, Amex significantly expanded its footprint.

This shift reflects broader industry trends. According to Modern Treasury, payment systems are evolving toward integrated infrastructure that reduces friction and improves merchant accessibility.

Detailed Benefits of OptBlue

1. Operational Simplicity

OptBlue consolidates all payment activity into one platform. This reduces administrative work and simplifies reconciliation across multiple payment types.

2. Faster Funding Cycles

Traditional Amex processing often involved delayed settlement. With OptBlue, funding timelines align with other card brands, improving cash flow predictability.

3. Access to High-Value Customers

American Express cardholders typically have higher spending power. Accepting Amex can increase average transaction size and overall revenue.

4. Flexible Pricing Opportunities

Because processors set pricing, merchants can negotiate rates. This introduces competition that did not exist in traditional Amex models.

5. Scalable Infrastructure

OptBlue allows merchants to scale without adding additional systems or contracts. This is particularly beneficial for growing businesses.

Limitations and Risks

1. Pricing Variability

Processor markups vary widely. Therefore, two merchants using OptBlue may pay significantly different rates.

2. Reduced Transparency

Some processors bundle fees, making it difficult to identify the true cost of Amex acceptance.

3. Volume Restrictions

OptBlue is typically limited to businesses processing under $1 million annually in Amex transactions. Beyond that, merchants must transition to Amex Direct.

4. Dependency on Processor

Merchants rely on their provider for pricing, support, and service quality. This makes provider selection critical.

Cost Breakdown: What You Are Really Paying

OptBlue pricing consists of multiple layers:

- Wholesale Discount Rate – Base rate set by American Express

- Processor Markup – Additional percentage or fee added by your provider

- Network Fees – Standard card network costs

A breakdown of OptBlue pricing components, highlighting where costs originate and where merchants can negotiate to reduce their effective rate. OptBlue pricing includes wholesale rates, processor markup, and network fees, all of which impact your effective cost.

According to the Federal Reserve, card processing costs are driven by interchange and network fees, which form the foundation of all transaction pricing.

Even small percentage differences can significantly impact annual costs. For example:

- $500,000 annual Amex volume

- 0.5% difference in processing rate

- = $2,500 additional cost per year

This highlights why rate negotiation is critical.

How to Negotiate Better OptBlue Rates

Many merchants assume pricing is fixed. However, OptBlue allows for negotiation.

1. Request Interchange-Plus Pricing

This structure provides transparency by separating wholesale costs from markup.

2. Compare Multiple Providers

Different processors offer different markups. Comparing quotes creates leverage.

3. Evaluate Effective Rate

Focus on total cost as a percentage of sales—not just headline rates.

4. Leverage Volume

Higher processing volume can often secure lower rates.

Real-World Merchant Scenarios

Restaurant

A mid-sized restaurant benefits from OptBlue by simplifying operations and increasing average ticket size. However, high transaction volume makes processing fees a critical factor.

eCommerce Business

An online store gains access to premium customers but must carefully manage fraud risk and chargebacks.

B2B Company

A B2B business may prioritize cost optimization over convenience. In this case, using a B2B merchant account can provide better control over interchange rates and overall processing costs.

Risk Management and Chargebacks

Accepting American Express can increase revenue—but it also introduces risk. Disputes and chargebacks must be managed effectively.

Implementing chargeback defense solutions helps merchants identify dispute patterns, respond effectively, and reduce long-term losses.

Strong dispute management is essential for maintaining healthy processor relationships and avoiding penalties.

Decision Framework: Is OptBlue Right for You?

| Business Type | Recommendation | Key Consideration |

|---|---|---|

| Startup | Consider OptBlue | Simplicity outweighs cost |

| Mid-sized business | Strong fit | Balance of efficiency and scalability |

| High-volume merchant | Evaluate Amex Direct | Potential cost savings |

| Cost-sensitive business | Proceed cautiously | Processing fees impact margins |

Strategic Insight: Payment Infrastructure Matters

Payment acceptance is not just a technical function—it is a financial strategy. OptBlue offers convenience, but merchants must evaluate long-term cost implications.

Choosing the right payment structure can significantly impact margins, scalability, and operational efficiency. Therefore, businesses should align their POS and payment systems with broader financial goals.

Conclusion

OptBlue American Express has made Amex acceptance more accessible, efficient, and scalable for small and mid-sized businesses. By simplifying onboarding, consolidating payments, and enabling competitive pricing, it provides clear operational advantages.

However, merchants must carefully evaluate processor markups, total cost of ownership, and long-term flexibility. A strategic approach ensures that payment systems support—not hinder—business growth.

Frequently Asked Questions

1. What is OptBlue American Express?

It is a program that allows merchants to accept American Express through their payment processor instead of a direct agreement.

2. Who qualifies for OptBlue?

Typically businesses processing under $1 million annually in Amex transactions.

3. Are OptBlue fees negotiable?

Yes. Processors set pricing, allowing merchants to negotiate rates.

4. Is OptBlue PCI compliant?

Yes. Merchants must comply with PCI DSS standards regardless of processor.

5. Does OptBlue reduce chargebacks?

No. Merchants must implement structured chargeback management strategies.