Payment Gateway for WooCommerce: Faster Deposits

How multi-currency payment processing and faster deposits unlock international revenue growth

Learn how delayed deposits and limited currency support silently erode your profits. This guide covers evaluating and implementing a payment gateway for WooCommerce that accelerates fund access and expands international reach.

TL;DR

- Delayed deposits drain your working capital – A 3 to 5 day settlement window on $150K/month in sales means $30K to $50K is perpetually inaccessible. Switching to next-day funding frees that capital immediately for inventory, marketing, and operations.

- Multi-currency processing drives international conversions – Displaying local currency pricing removes checkout friction. WooCommerce supports 200+ countries and 118 languages, but your payment gateway must actually process and settle in those currencies to capture the full benefit.

- Your effective processing rate is likely higher than you think – Hidden fees (PCI compliance, batch fees, currency conversion markups, reserve holds) typically add 0.3% to 0.8% on top of advertised rates. Audit your last three months of statements to find your true cost.

- Chargebacks threaten more than revenue – A rising dispute ratio triggers slower settlements, reserve holds, and potential account termination. Proactive defense (clear descriptors, alert services, fast response) is far cheaper than reactive damage control.

- Start with a statement audit – Calculate your true effective rate and float cost. This two-hour exercise gives you the data to evaluate whether switching processors could save you thousands annually and unlock faster access to your own money.

Guide Orientation: What This Guide Covers and Who It’s For

This guide is for eCommerce managers running established online businesses on WooCommerce who are losing money and momentum to delayed deposits, high transaction fees, and limited currency support. If your current payment gateway for WooCommerce holds your funds for days, charges opaque fees, or can’t handle international transactions smoothly, this guide is written for you.

By the end, you’ll understand exactly how delayed deposits erode your cash flow, why multi-currency payment processing is now a competitive necessity (not a luxury), and how to evaluate and implement an integrated payment gateway that accelerates your access to funds while expanding your international reach.

This guide covers the financial mechanics of deposit delays, the decision framework for choosing a payment gateway, and a step-by-step process for transitioning to faster, more transparent payment processing. It does not cover platform migration (Shopify vs. WooCommerce), shipping logistics, or tax compliance for international sales.

Why Delayed Deposits and Limited Currency Support Cost You More Than You Think

comparison infographic showing delayed payment settlement versus next day funding for WooCommerce stores and the impact on ecommerce cash flow and working capital

Delayed deposits are one of the most underestimated drains on eCommerce profitability. When your payment processor holds funds for 3 to 7 business days, you’re effectively extending an interest-free loan to your gateway provider. For a store processing $200,000 per month, a five-day delay means roughly $50,000 is perpetually inaccessible, money that could cover inventory restocks, ad spend, or payroll.

Payment timelines depend on how transactions move between banks, card networks, and processors, with settlement speed influenced by batching schedules, risk controls, and payment infrastructure as outlined by Visa.

The problem compounds when you layer in international sales. WooCommerce powers eCommerce stores globally, with strong adoption across the US, UK, EU, India, and Australia. If your store sells to any of these markets but forces customers to pay in a single currency, you’re creating friction that kills conversions. Shoppers who see prices in an unfamiliar currency are significantly more likely to abandon their carts.

The cost of inaction is twofold. First, you lose the operational agility that comes with predictable cash flow. Second, you forfeit international revenue to competitors whose checkout experience feels local. The global payment gateway market growth is driven by merchants demanding faster settlements, multi-currency support, and transparent fee structures. If your current setup doesn’t deliver those three things, you’re operating at a structural disadvantage.

Core Concepts: Deposits, Multi-Currency Processing, and B2B Payment Gateways

Settlement Timing vs. Authorization

When a customer completes a purchase, authorization happens in seconds. But authorization isn’t money in your account. Settlement (the actual transfer of funds to your bank) can take anywhere from one to seven business days depending on your processor, your risk profile, and your contract terms. Many eCommerce managers conflate these two events, which leads to cash flow planning based on sales volume rather than actual fund availability.

Multi-Currency Payment Processing

Multi-currency payment processing allows your store to display prices, accept payments, and settle transactions in multiple currencies. This is distinct from simple currency conversion at checkout, where the customer sees a converted price but you still settle in a single base currency (often at an unfavorable exchange rate with hidden markups). True multi-currency processing reduces conversion friction and can improve your margins on international sales by giving you more control over exchange rate management.

B2B Payment Gateways vs. B2C Gateways

B2B payment gateways handle larger transaction sizes, support net terms or invoicing, and often include Level II/III data processing for lower interchange rates on commercial cards. If your WooCommerce store serves both retail and wholesale customers, your gateway needs to handle both transaction profiles without forcing you into two separate systems. Many conventional gateways are optimized for small B2C transactions and charge premium rates on the larger B2B orders that actually drive your revenue.

The Real Cost of “Free” Gateways

Several popular payment gateways advertise no monthly fees but compensate through higher per-transaction rates, delayed settlement windows, and aggressive reserve holds. For a store doing $50,000 or more per month, the total cost of a “free” gateway frequently exceeds what you’d pay for a dedicated merchant account with transparent pricing and faster funding.

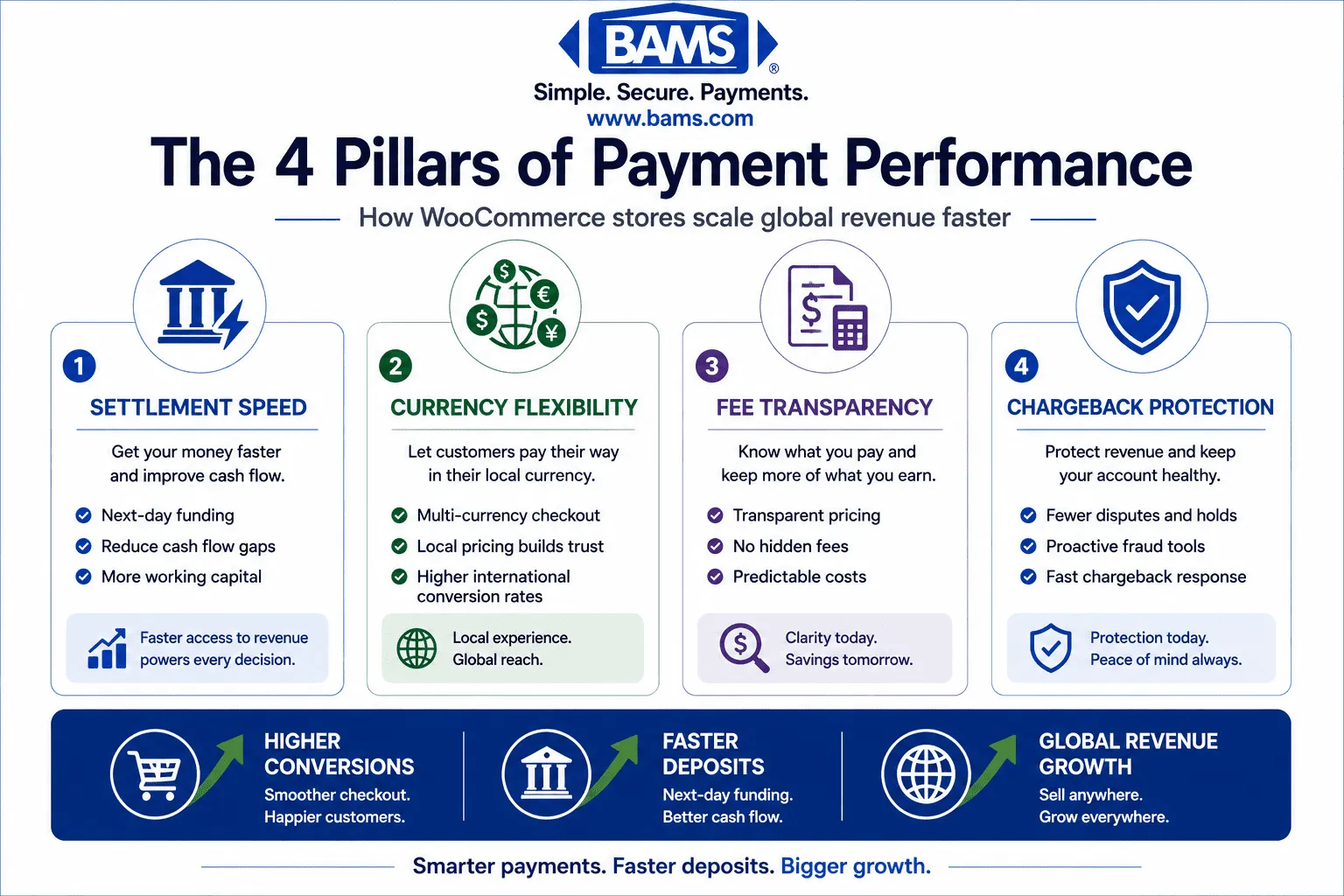

The Framework: Four Pillars of Payment Performance for WooCommerce

The four pillars of payment performance that help WooCommerce stores accelerate deposits, reduce friction, and scale international sales.

Overcoming delayed deposits and scaling international sales requires a payment infrastructure built on four interconnected pillars. Each one addresses a specific failure mode that eCommerce managers encounter as they grow.

- Settlement Speed: How quickly authorized funds reach your bank account. This is the foundation of operational cash flow.

- Currency Flexibility: The ability to accept, display, and settle in multiple currencies without hidden conversion markups.

- Fee Transparency: A pricing structure where you can predict your monthly processing costs within a narrow margin, with no surprise deductions.

- Risk and Chargeback Management: Proactive tools and support that prevent disputes from escalating into fund holds or account freezes.

These four pillars are sequential in priority but operate simultaneously. You can’t benefit from multi-currency processing if chargebacks are triggering reserve holds that delay your deposits. And transparent fees mean nothing if your settlement window is a week long. The step-by-step breakdown that follows addresses each pillar in the order you should tackle them.

Step-by-Step: How to Overcome Delayed Deposits and Scale International Sales

Step 1: Audit Your Current Settlement Timeline and True Processing Costs

Objective: Establish a factual baseline of how long your funds take to arrive and what you’re actually paying per transaction, including all hidden fees. Card payment costs include interchange fees, network assessments, and processor charges, which together determine the true cost structure and cash flow impact of eCommerce transactions as outlined by the Federal Reserve.

Start by pulling three months of your payment processor statements. For each month, record: total sales volume, total fees deducted (including per-transaction fees, monthly fees, PCI compliance fees, and any reserve holds), and the average number of business days between a completed sale and the funds appearing in your bank account. Most eCommerce managers discover that their effective processing rate is 0.3% to 0.8% higher than the advertised rate once all ancillary fees are included.

Next, calculate your “float cost,” the opportunity cost of delayed funds. If your average settlement delay is four business days and your monthly volume is $150,000, roughly $30,000 is perpetually unavailable. That’s $30,000 you can’t use to buy inventory at early-payment discounts, fund marketing campaigns during peak periods, or cover payroll without dipping into a credit line.

Anti-patterns: Don’t rely on your gateway dashboard alone for cost analysis. Many dashboards exclude reserve deductions, currency conversion fees, and chargeback fees from the headline rate. Pull actual bank deposits and reconcile against reported payouts. Also avoid averaging across months without accounting for seasonal volume spikes, which often trigger higher reserve requirements.

Success indicators: You have a spreadsheet showing your true effective rate (total fees divided by total volume), your average settlement delay in business days, and your monthly float cost. This becomes your benchmark for evaluating alternatives.

Step 2: Define Your International Sales Requirements

Objective: Map your current and target international markets to specific currency, language, and payment method requirements.

WooCommerce operates in 200+ countries and supports 118 languages, which means your platform can technically reach almost any market. But your payment gateway may not support the currencies or local payment methods your customers prefer. Start by analyzing your existing traffic and sales data by country. Google Analytics and your WooCommerce reports will show you where your international visitors are coming from and where they’re dropping off in the checkout flow.

For each target market, identify: the preferred local currency, the dominant payment methods (credit cards, bank transfers, digital wallets), and any regulatory requirements for processing payments in that region. For example, stores targeting India need UPI and local card network support, not just Visa and Mastercard.

Anti-patterns: Don’t assume that accepting USD globally is “good enough.” Customers in the UK, EU, and Asia expect to see and pay in their local currency. Forcing a currency conversion at checkout adds friction and often triggers a bank-imposed foreign transaction fee on the customer’s end, which they’ll associate with your store, not their bank. Also avoid selecting a gateway based solely on the number of currencies it lists. What matters is whether it supports settlement in those currencies or merely converts them back to your base currency at a markup.

Success indicators: You have a prioritized list of 3 to 5 target markets with specific currency, payment method, and settlement requirements for each.

Step 3: Evaluate Payment Gateways Against Your Specific Requirements

Objective: Build a shortlist of payment gateways that meet your settlement speed, currency, fee transparency, and risk management criteria.

Using your audit data from Step 1 and your market requirements from Step 2, create an evaluation matrix. The columns should include: settlement speed (next-day vs. 2-day vs. 3+ day), supported currencies with settlement options, effective processing rate for your average transaction size, chargeback management tools, WooCommerce integration quality, and contract terms (month-to-month vs. annual lock-in).

For B2B payment gateways specifically, evaluate whether the provider supports Level II and Level III data processing. Commercial card transactions that include enhanced data (purchase order numbers, tax amounts, line-item details) qualify for lower interchange rates, which can save 0.5% to 1.0% per transaction on B2B orders. If a significant portion of your revenue comes from wholesale or business customers, this single feature can offset your entire monthly gateway cost.

Providers like BAMS offer next-day funding and transparent pricing structures specifically designed for small-to-midsize eCommerce operations, which directly addresses the settlement delay problem. When evaluating any provider, request a statement analysis rather than relying on quoted rates. A statement analysis compares your current processing costs line-by-line against what the new provider would charge on the same transaction mix.

Anti-patterns: Avoid choosing a gateway based on brand recognition alone. The most popular options often have the longest settlement windows and the least transparent fee structures because they can afford to. Also don’t skip the contract review. Look for early termination fees, rate increase clauses, and reserve hold policies that could negate the benefits of switching.

Success indicators: You have a shortlist of 2 to 3 gateways with completed evaluation matrices, and you’ve requested statement analyses from each.

Step 4: Implement Multi-Currency Checkout Without Breaking Your Store

Objective: Deploy multi-currency payment processing on your WooCommerce store with minimal disruption and accurate pricing.

WooCommerce’s flexibility is both its strength and its risk here. Multi-currency implementation typically involves three components: a currency switcher plugin (for frontend display), your payment gateway’s multi-currency processing capability (for actual transaction handling), and your accounting system’s ability to reconcile settlements in multiple currencies.

Start with your highest-value target market from Step 2. Configure pricing in that market’s currency using either fixed prices (you set the price manually in each currency) or dynamic conversion (prices auto-convert based on exchange rates). Fixed pricing gives you margin control but requires regular updates. Dynamic conversion is lower maintenance but can create margin compression during exchange rate fluctuations.

Test the complete checkout flow from the customer’s perspective before going live. Place test orders in each supported currency and verify that: the correct currency symbol and amount display throughout the checkout, the payment gateway processes the transaction in the displayed currency (not converting silently), and the settlement arrives in your account at the expected rate. Understanding how payment processing works end-to-end is critical here because multi-currency adds complexity at every stage.

Anti-patterns: Don’t launch all target currencies simultaneously. Roll out one at a time, verify reconciliation accuracy, and then add the next. Also avoid using a separate plugin for currency conversion that doesn’t communicate with your gateway. Mismatches between displayed prices and charged amounts are a leading cause of chargebacks on international orders.

Success indicators: Test orders in your first target currency complete successfully, settle in the expected timeframe, and reconcile accurately in your accounting system.

Step 5: Accelerate Settlement with Next-Day Funding

Objective: Reduce your average settlement window to one business day, freeing up working capital for growth.

Next-day funding means transactions processed today land in your bank account tomorrow. This sounds simple, but the operational impact is significant. For a store processing $10,000 per day, moving from a 3-day settlement to next-day funding frees up $20,000 in working capital permanently. Over a year, that’s $20,000 you can deploy into inventory, marketing, or debt reduction instead of waiting for it to clear.

To qualify for next-day funding, most processors require: a US-based business bank account, transaction batching before a daily cutoff time (typically 8 PM or 10 PM ET), and a chargeback ratio below the card network thresholds (under 1% of transactions). If your chargeback ratio is above 0.65%, address that first (see Step 6) because a high dispute rate is the most common reason processors deny or revoke next-day funding eligibility.

Configure your WooCommerce store to auto-batch transactions daily.

Most gateway plugins support automatic batching, but some default to manual batch submission, which means your funds don’t start the settlement process until you (or someone on your team) remembers to close the batch. Automate this immediately.

Anti-patterns: Don’t assume next-day funding applies to all transaction types. Some processors exclude international transactions, transactions above a certain dollar amount, or transactions flagged for review. Clarify these exclusions before committing. Also avoid processors that offer next-day funding as a paid add-on with a per-transaction surcharge. The math often doesn’t work out for stores with high transaction counts and lower average order values.

Success indicators: Your first batch under the new processor settles in your bank account the next business day, and subsequent batches arrive consistently without exceptions. Implementing guaranteed next day funding reduces settlement delays and gives eCommerce businesses faster access to working capital for inventory, payroll, and advertising.

Step 6: Build Proactive Chargeback Defense to Protect Your Settlement Speed

Objective: Keep your chargeback ratio below card network thresholds to maintain next-day funding eligibility and avoid reserve holds.

Chargebacks are the silent killer of fast settlement. When your dispute ratio climbs, processors respond by slowing your settlement, imposing reserve holds (where they withhold 5% to 10% of your volume), or terminating your account entirely. Visa’s dispute monitoring threshold is 0.9% of transactions, and Mastercard’s is 1.0%. But most processors start tightening terms well before you hit those numbers.

Build a three-layer defense.

First, prevent disputes at the source by using clear billing descriptors (the name that appears on customer bank statements should match your store name), sending immediate order confirmation and shipping notification emails, and making your refund policy visible and easy to use. Second, use chargeback alerts (services like Ethoca and Verifi) that notify you of disputes before they become formal chargebacks, giving you a window to issue a refund and avoid the dispute entirely. Third, when chargebacks do occur, respond with compelling evidence within the deadline (typically 7 to 20 days depending on the card network).

BAMS includes a proactive chargeback defense program with dedicated account management, which is particularly valuable for eCommerce managers who don’t have a full-time payments specialist on staff. Having someone who understands the dispute process and can help you compile evidence quickly makes the difference between winning and losing representments.

Anti-patterns: Don’t ignore chargebacks because they’re a small percentage of your volume. Even a handful of disputes per month can push a mid-volume store over the monitoring threshold. Also don’t treat chargebacks as purely a payments problem. Most disputes originate from fulfillment issues (late shipments, incorrect items) or unclear product descriptions, which are operational problems that require cross-team solutions.

Success indicators: Your monthly chargeback ratio stays below 0.5%, you’re enrolled in chargeback alert services, and you have a documented response process with templates for common dispute reason codes.

Step 7: Monitor, Optimize, and Scale

Objective: Establish ongoing monitoring to ensure your payment infrastructure continues to perform as you grow into new markets.

Set up a monthly payment operations review. Track five metrics: effective processing rate (total fees / total volume), average settlement time, chargeback ratio, international conversion rate by currency, and gateway uptime/decline rate. Any significant movement in these metrics signals a problem that needs attention before it impacts your cash flow or customer experience.

As your international volume grows, revisit your currency strategy quarterly. WooCommerce powers 30-35% of all online stores worldwide, and the platform’s market share in regions like Asia and Europe continues to expand. Markets that weren’t worth dedicated currency support six months ago may now represent meaningful revenue opportunities. Add currencies based on actual sales data, not assumptions about where your customers might be.

Also review your gateway contract annually. Payment processing is a competitive industry, and rates, features, and settlement terms improve regularly. Use your monthly metrics as leverage in negotiations. A processor that sees consistent volume growth, low chargebacks, and clean transaction history has every incentive to offer you better terms to retain your business.

Anti-patterns: Don’t set up your payment infrastructure and forget about it. Processing rates creep up through small fee adjustments that compound over time. If you’re not reviewing statements monthly, you’re likely paying more than you were six months ago. Also avoid scaling into new markets without confirming that your gateway supports the local payment methods and settlement currencies first. Modern payment infrastructure improves transaction visibility and settlement timing, enabling eCommerce businesses to manage international payments and cash flow more predictably according to Modern Treasury.

Success indicators: You have a recurring calendar event for monthly payment reviews, a dashboard tracking the five key metrics, and a documented process for adding new currencies.

Practical Example: From 5-Day Settlement to Next-Day Funding

Consider a WooCommerce store selling specialty kitchen equipment to both retail consumers and restaurant supply businesses across the US, UK, and Germany. Monthly volume: $180,000 ($120,000 domestic, $60,000 international). Their existing gateway settled domestic transactions in 3 business days and international transactions in 5 to 7 days. Their effective processing rate, after accounting for currency conversion markups and monthly fees, was 3.4%.

After completing the audit in Step 1, they discovered $12,000 in annual fees they hadn’t accounted for (PCI non-compliance fees, batch fees, and statement fees buried in monthly deductions). Their float cost was approximately $36,000 perpetually tied up in transit.

By switching to a processor with next-day domestic funding and 2-day international settlement, and implementing true multi-currency processing in GBP and EUR, they achieved three outcomes. First, their float dropped from $36,000 to under $10,000, freeing $26,000 in working capital. Second, their international conversion rate improved by 18% in the first quarter after displaying local currency pricing. Third, their effective processing rate dropped to 2.7% through transparent interchange-plus pricing and Level III data processing on their B2B restaurant supply orders.

The total annual savings in processing fees alone was approximately $15,000. Combined with the improved conversion rate on international orders (adding roughly $40,000 in annual revenue), the payment infrastructure change generated over $55,000 in combined value in the first year.

Common Mistakes and Pitfalls

- Treating all gateways as interchangeable. The difference between a 2-day and a 5-day settlement window compounds dramatically at scale. A gateway is infrastructure, not a commodity.

- Ignoring B2B transaction optimization. If even 20% of your volume comes from business buyers, failing to process Level II/III data means you’re overpaying on interchange for your highest-value orders.

- Launching multi-currency without reconciliation planning. Accepting payments in five currencies is pointless if your accounting team can’t reconcile settlements accurately. Build the back-office process before you flip the switch.

- Waiting until chargebacks are a crisis. By the time your processor notifies you of a problem, you’re already in a monitoring program. Proactive defense costs far less than reactive remediation.

- Optimizing for the lowest advertised rate. The cheapest quoted rate almost never translates to the lowest total cost. Evaluate effective rates based on your actual transaction mix, not marketing materials.

What to Do Next

Start with Step 1. Pull your last three months of processor statements and calculate your true effective rate and float cost. This single exercise takes about two hours and gives you the concrete data you need to evaluate whether your current setup is costing you more than it should.

If the numbers confirm what you suspect, request a statement analysis from one or two alternative processors. Compare the results against your baseline. You don’t need to switch tomorrow, but you do need to know what better looks like for your specific volume and transaction profile.

Bookmark this guide and revisit it as your international sales grow. The framework scales with your business: each time you enter a new market or your volume crosses a new threshold, cycle back through the relevant steps to ensure your payment infrastructure is keeping pace with your ambitions rather than holding them back.

Frequently Asked Questions

What is a payment gateway and why is it important for eCommerce?

A payment gateway is the technology that securely transmits transaction data between your online store, the customer’s bank, and your merchant account. It handles authorization, encryption, and fraud screening in real time. For eCommerce, it’s the critical link that determines how quickly you get paid, what currencies you can accept, and how secure your customers’ data remains. A poorly chosen gateway creates checkout friction, delays your deposits, and can increase your vulnerability to chargebacks. Learn more about how payment gateways work in our detailed breakdown.

How do I choose the best payment gateway for my WooCommerce store?

Focus on four criteria specific to your business: settlement speed (next-day funding vs. multi-day delays), supported currencies and local payment methods for your target markets, total effective cost (not just the advertised per-transaction rate), and chargeback management tools. Request a statement analysis from prospective providers so you can compare apples-to-apples against your current costs. Avoid choosing based on popularity alone. The best gateway is the one that matches your transaction volume, customer geography, and growth trajectory.

When should I consider switching my payment gateway?

Switch when your current gateway consistently holds funds for more than two business days, when your effective processing rate exceeds 3% after accounting for all fees, when you’re losing international sales due to limited currency support, or when chargeback disputes escalate without adequate support from your provider. If you’re processing $50,000 or more per month, even a 0.3% reduction in your effective rate saves $1,800 annually. Which payment gateways support international transactions and multi-currency processing?

Many gateways advertise international support, but there’s a meaningful difference between currency conversion (where the gateway converts foreign payments to your base currency at a markup) and true multi-currency processing (where you can display, charge, and settle in multiple currencies). When evaluating options, confirm whether the gateway settles in local currencies or simply converts everything back to USD. Also verify support for region-specific payment methods like SEPA in Europe or UPI in India, which are essential for maximizing conversion in those markets.

How does next-day funding work, and can my store qualify?

Next-day funding means transactions batched before a daily cutoff time (usually 8 to 10 PM ET) are deposited in your bank account the following business day. To qualify, you typically need a US-based business bank account, a chargeback ratio below 1%, and automatic daily batch submission configured in your WooCommerce gateway plugin. Some processors exclude certain transaction types (high-value orders, international transactions) from next-day eligibility, so clarify these exclusions before committing.

How can I reduce chargebacks on my WooCommerce store?

Build a three-layer defense. First, prevent disputes by using clear billing descriptors, sending proactive shipping notifications, and making your refund policy easy to find and use. Second, enroll in chargeback alert services (Ethoca, Verifi) that notify you of disputes before they become formal chargebacks, giving you time to issue a preemptive refund. Third, when chargebacks do occur, respond within the deadline with organized evidence including order confirmations, delivery tracking, and customer communication logs. Keeping your ratio below 0.5% protects your next-day funding eligibility and prevents costly reserve holds.