Convenience Fee vs Surcharge for eCommerce Merchants

How to evaluate fee-passing strategies without triggering compliance violations or alienating customers

Learn the legal and practical differences between convenience fees and surcharges. This guide helps you evaluate whether passing processing costs to customers makes sense for your margins and relationships.

TL;DR

- Surcharges and convenience fees are legally distinct – Surcharges apply to credit card payments specifically, while convenience fees apply to alternative payment channels. Mislabeling them triggers fines.

- Surcharging often backfires financially – Merchants typically see a 10% drop in sales after implementing surcharges, which often exceeds the fees recovered.

- Customer satisfaction takes a measurable hit – Satisfaction scores drop 24 points for merchants that surcharge, and nearly one-third of customers report being surprised by fees.

- Alternative strategies may work better – Negotiating processor rates, optimizing interchange categories, and encouraging lower-cost payment methods reduce costs without risking customer relationships.

- Model the impact before implementing – Build scenarios accounting for sales decline, then track actual results against projections with clear thresholds for reversing course.

What This Guide Covers

This guide explains the critical differences between convenience fees and surcharges, two fee structures that can shift credit card processing costs from your business to your customers. You’ll learn how each works, when each is legal, and whether either strategy actually saves you money.

By the end, you’ll understand how to evaluate these options for your eCommerce operation, avoid compliance violations that trigger fines, and identify which approach (if any) aligns with your customer relationships and margins.

This guide is for established online businesses processing significant card volume who want to reduce processing fees strategically, not reactively. We won’t cover cash discount programs or B2B-specific payment structures here.

Why Processing Fee Strategy Matters Now

Credit card processing fees have climbed steadily. This pressure has pushed more merchants toward passing costs to customers.

Card acceptance costs are driven primarily by interchange and network fees, which make up the largest portion of merchant processing expenses as outlined by the Federal Reserve.

Here’s the uncomfortable truth: understanding payment processing fee structures isn’t optional anymore. The difference between a convenience fee vs surcharge isn’t semantic. It determines your legal exposure, customer perception, and whether you actually reduce costs or just create new problems. Getting this wrong can mean fines from card networks, lost sales, and damaged trust with customers who feel blindsided at checkout.

Core Concepts: What You Need to Understand First

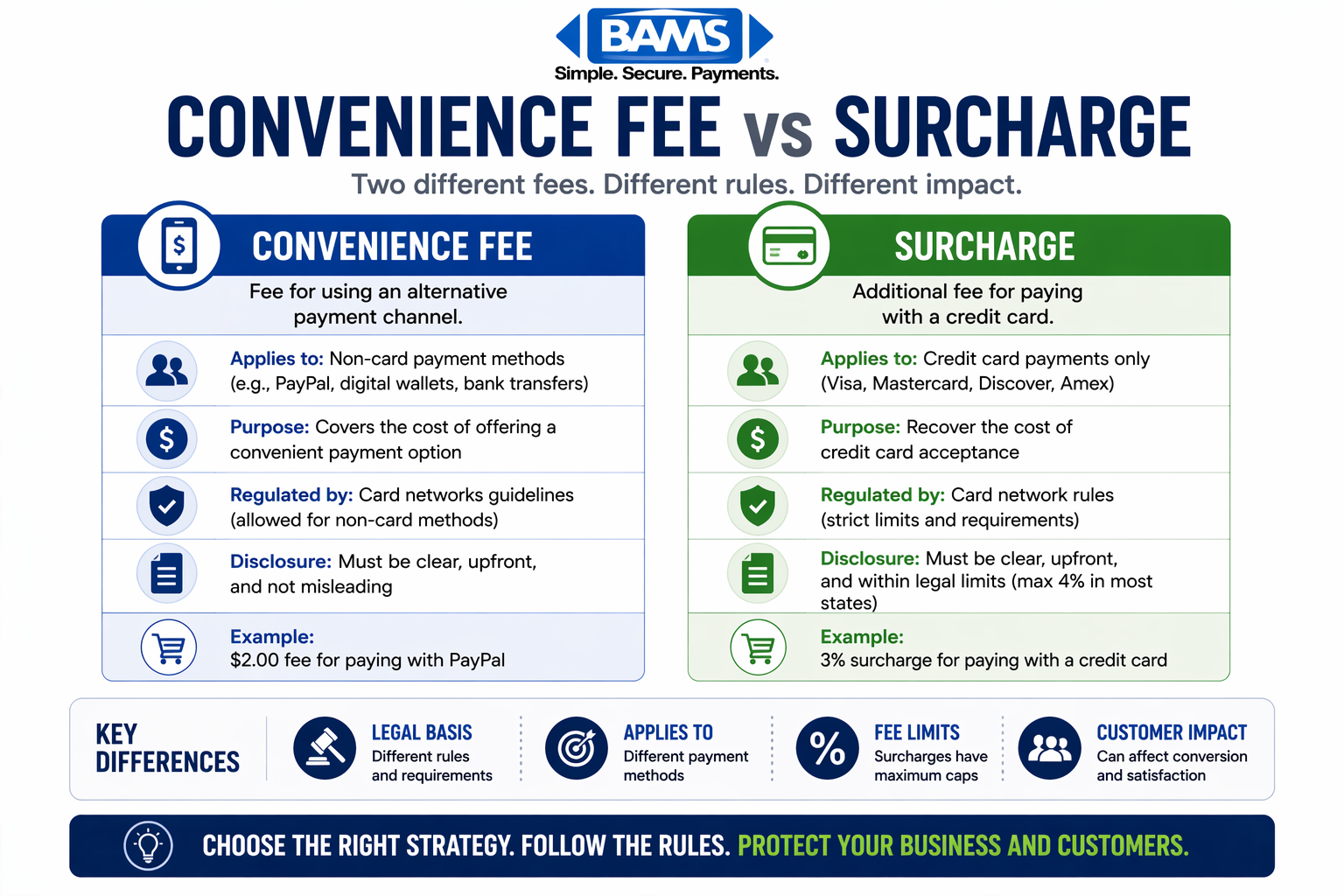

A side-by-side comparison of convenience fees and surcharges, highlighting key differences in rules, application, and business impact.

Processing Fees Explained

Every credit card transaction involves multiple parties taking a cut. Your total processing cost typically includes three components: interchange fees (paid to the card-issuing bank), assessment fees (paid to card networks like Visa and Mastercard), and your payment processor’s markup.

Interchange fees represent the largest portion, typically 1.5% to 2.5% of the transaction. These rates vary by card type, industry, and how the transaction is processed. Rewards cards cost more. Card-not-present transactions (standard for eCommerce) cost more than in-person swipes.

Surcharges vs. Convenience Fees: The Critical Distinction

A surcharge is an additional fee applied to credit card payments specifically. It’s meant to offset the cost of accepting credit cards and applies to all credit card transactions regardless of payment channel.

A convenience fee is charged for offering an alternative payment channel. The key requirement: there must be a standard payment method available, and the customer chooses a more convenient option. For example, paying a utility bill online instead of by mail, or buying event tickets by phone instead of at the box office.

The confusion between these terms costs merchants money through compliance violations and customer disputes. Many businesses incorrectly label surcharges as convenience fees, which triggers card network penalties and potential legal issues.

Common Misconceptions

“Surcharges and convenience fees are the same thing.” They’re not. Card networks treat them differently, with distinct rules and compliance requirements.

“I can add any fee I want to cover my costs.” You can’t. Both fee types have caps (typically 4% or your actual processing cost, whichever is lower), disclosure requirements, and state-level legal restrictions.

“Customers don’t care about small fees.” They do. Research shows consumer satisfaction drops 24 points (on a 1,000-point scale) for merchants that add surcharges compared to those that don’t.

The Strategic Framework: Evaluating Fee Pass-Through Options

Before implementing any fee strategy, you need a structured approach. This framework moves through four phases: Assessment, Compliance, Implementation, and Monitoring.

In the Assessment phase, you analyze your current processing costs, customer payment preferences, and competitive landscape. The Compliance phase ensures you understand legal requirements and card network rules. Implementation covers the technical and communication aspects. Monitoring tracks the actual impact on sales, customer satisfaction, and net savings.

Each phase builds on the previous one.

- Skipping Assessment leads to implementing solutions that don’t fit your business.

- Skipping Compliance leads to fines and forced reversals.

- Skipping Monitoring means you won’t know if your strategy is actually working.

Step-by-Step: Implementing a Strategic Fee Approach

Step 1: Audit Your Current Processing Costs

Objective: Establish your true cost baseline before making any changes.

Pull three to six months of processing statements. Identify your effective rate (total fees divided by total volume). Break down costs by interchange, assessments, and processor markup. Note which card types cost you most, as rewards and corporate cards typically carry higher interchange fees.

Look for hidden fees: PCI compliance fees, monthly minimums, batch fees, and statement fees. These add up and affect your calculation of whether surcharging makes financial sense.

Avoid: Using a single month’s data, which may not reflect seasonal variations. Ignoring chargebacks and their associated fees in your cost calculation.

Success indicator: You can state your exact effective processing rate and identify your highest-cost transaction types.

Step 2: Evaluate Legal and Compliance Requirements

Objective: Understand what you’re legally permitted to do in your operating states.

Surcharging is prohibited in some states, including Connecticut and Massachusetts. Other states have specific disclosure requirements. Your merchant services provider should help clarify which rules apply to your business.

Card network rules add another layer. Card networks impose strict rules on how surcharges and payment-related fees are applied, including disclosure, limits, and eligibility requirements as outlined in Visa’s official rules and guidelines Visa and Mastercard both allow surcharging but require advance registration (typically 30 days notice to the card network). You must disclose the surcharge at the point of entry, at the point of sale, and on the receipt. The surcharge cannot exceed 4% or your actual cost of acceptance, whichever is lower.

Convenience fees have stricter requirements. They’re generally only permitted for government agencies, educational institutions, and specific service providers where an alternative payment channel exists. Most eCommerce businesses don’t qualify for true convenience fees..

Avoid: Assuming your state allows surcharging without verification. Labeling a surcharge as a convenience fee to avoid negative perception (this violates card network rules).

Success indicator: You have documented confirmation of your legal ability to surcharge and understand the specific disclosure requirements.

Step 3: Model the Financial Impact

Objective: Project realistic savings after accounting for behavioral changes.

This is where most merchants miscalculate.

Build a model with three scenarios: optimistic (5% sales impact), realistic (10% impact), and pessimistic (15% impact). Factor in the surcharge revenue against lost margin from reduced sales. Include implementation costs like system updates, staff training, and signage.

For many eCommerce businesses, the math doesn’t work. If your margins are tight, a 10% sales drop often exceeds the processing fees you’d recover through surcharging.

Avoid: Assuming customers won’t change behavior. Ignoring the lifetime value impact of customers who leave permanently.

Success indicator: You have a spreadsheet model showing net impact across multiple scenarios, with clear break-even points.

Step 4: Consider Alternative Cost Reduction Strategies

Objective: Evaluate options that reduce costs without customer-facing fees.

Before passing costs to customers, businesses should evaluate options like transparent interchange plus pricing, which reduces processing expenses by separating network fees from processor markup and eliminating hidden costs.

Negotiate with your payment processor, as many merchants overpay due to outdated contracts or lack of competitive quotes. A merchant services provider focused on transparent pricing can often reduce your effective rate without surcharging.

Optimize for lower interchange categories. Ensure you’re capturing all required data fields for business and corporate cards (Level 2 and Level 3 processing). Use address verification to qualify for better rates. Settle batches daily to avoid downgrades.

Encourage lower-cost payment methods. Debit cards typically cost less than credit cards. ACH transfers cost even less. Some businesses offer small discounts for preferred payment methods rather than penalties for credit cards.

Avoid: Accepting the first quote from any processor. Assuming your current rates are competitive without benchmarking.

Success indicator: You’ve obtained at least two competitive processing quotes and identified specific interchange optimization opportunities.

Step 5: Design Your Implementation (If Proceeding)

Objective: Create a compliant, customer-friendly implementation plan.

If your analysis supports surcharging, design the implementation carefully. Transparency is non-negotiable. Clear payment flows and transparent transaction handling improve customer trust and reduce friction during checkout, as outlined by Visa.

Display the surcharge clearly before checkout begins, not at the final confirmation. State the exact percentage and dollar amount. Explain why the fee exists (covering payment processing costs) in plain language.

Update your payment systems to apply surcharges only to credit cards, not debit cards. This is a common compliance failure. Debit card surcharging is prohibited by card network rules, and violating this can result in fines or loss of card acceptance privileges.

Avoid: Burying disclosure in terms and conditions. Applying surcharges to debit transactions. Using aggressive or defensive language about the fee.

Success indicator: A customer can understand the surcharge policy within 10 seconds of arriving at checkout. A seamless checkout experience depends on the right infrastructure. Using an integrated payment gateway ensures accurate fee application, proper card-type handling, and a smoother customer payment experience.

Step 6: Monitor and Adjust

Objective: Track actual results against your projections and adjust accordingly.

Establish baseline metrics before implementation: conversion rate, average order value, customer satisfaction scores, and repeat purchase rate. Track these weekly for the first three months after implementing surcharges.

Watch for leading indicators of problems: increased cart abandonment at the payment stage, rise in customer service inquiries about fees, negative reviews mentioning fees, and decline in repeat purchases from existing customers.

Set a decision threshold in advance. If sales drop exceeds your pessimistic scenario, have a plan to reverse course. Some businesses find that removing surcharges after a trial period actually increases customer loyalty due to the perceived responsiveness.

Avoid: Waiting too long to evaluate results. Ignoring qualitative feedback from customers and support staff.

Success indicator: You have a dashboard tracking key metrics with clear thresholds for action.

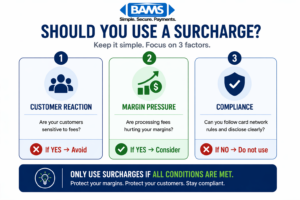

When Each Approach Makes Sense

A simplified framework to decide whether surcharging makes sense based on customer behavior, margins, and compliance.

Surcharging May Work If:

Your industry commonly surcharges (customers expect it). Your margins are high enough to absorb some sales loss. You operate in states where surcharging is legal. Your customer base is price-insensitive or has limited alternatives.

Surcharging Likely Backfires If:

You compete primarily on price or convenience. Your customers have easy alternatives. Your margins are thin. Customer lifetime value depends on repeat purchases and referrals.

Convenience Fees Are Appropriate If:

You’re a government agency, utility, or educational institution. You offer multiple payment channels with a clear “standard” option. The fee applies to the alternative channel, not to a specific card type.

Common Mistakes That Cost Merchants Money

Mislabeling fees is the most expensive error. Calling a surcharge a “convenience fee” or “service fee” doesn’t change what it is legally. Card networks audit for this, and violations result in fines up to $25,000 per month.

Implementing without modeling leads to surprises. About 20% of merchants now assess surcharges, but many discover the net impact is negative only after losing customers.

Forgetting state-specific rules creates legal exposure. Surcharging laws vary significantly, and what’s legal in Texas may be prohibited in Connecticut.

Neglecting the customer experience destroys trust. Customers who feel surprised or deceived rarely return, and they tell others. The short-term fee recovery rarely compensates for long-term relationship damage.

What to Do Next

Start with Step 1: audit your current processing costs. You can’t make an informed decision about surcharging without knowing your actual effective rate and cost breakdown.

If your effective rate seems high, get a competitive quote from a merchant services provider that offers transparent pricing before implementing customer-facing fees. Many businesses find they can reduce processing costs significantly through better rates and interchange optimization, without risking customer relationships.

Revisit this guide as your business grows. The calculus changes with volume, customer mix, and competitive dynamics. What doesn’t make sense today might work in two years, or vice versa.

Frequently Asked Questions

What are credit card processing fees and why do merchants pay them?

Credit card processing fees are the costs merchants pay to accept card payments. They include interchange fees (paid to the card-issuing bank), assessment fees (paid to card networks like Visa and Mastercard), and your payment processor’s markup. Merchants pay these fees because card networks and banks provide the infrastructure, fraud protection, and guarantee of payment that make card transactions possible.

How are credit card processing fees determined?

Interchange fees, the largest component, vary by card type (rewards cards cost more), transaction type (card-not-present costs more than card-present), merchant category, and data provided with the transaction. Assessment fees are set by card networks as flat percentages. Processor markups vary by provider, contract terms, and your negotiating leverage based on volume.

Can I add a surcharge to credit card transactions in any state?

No. Some states prohibit credit card surcharging, including Connecticut and Massachusetts. Other states have specific disclosure and registration requirements. Before implementing surcharges, verify the laws in every state where you do business. Your payment processor should help clarify which rules apply to your situation.

What’s the maximum surcharge I can charge customers?

Card network rules cap surcharges at 4% or your actual cost of card acceptance, whichever is lower. If your processing costs are 2.5%, you cannot surcharge 4%. You must also disclose the exact surcharge amount before the transaction and on the receipt.

Why do customers react negatively to surcharges?

Surcharges feel like a penalty for using a preferred payment method. Research shows consumer satisfaction drops significantly for merchants that surcharge. Many customers also report being surprised by fees at checkout, which damages trust. The perception of unfairness, especially when competitors don’t surcharge, drives customers to alternatives.

How can I reduce processing fees without surcharging customers?

Negotiate better rates with your payment processor or get competitive quotes. Optimize for lower interchange by capturing required data fields for business cards (Level 2 and Level 3 processing). Use address verification to qualify for better rates. Settle batches daily. Encourage lower-cost payment methods like debit cards or ACH transfers through small incentives rather than credit card penalties.

Sources