How Delayed Funding Hurts Your eCommerce Business

Why your payment gateway’s deposit timing matters more than processing fees for cash flow

Learn how 3-5 day payment holds drain your working capital and what to look for in an eCommerce payment gateway that offers next-day funding. Built for established businesses managing real volume.

TL;DR

- Delayed deposits are a growing problem – 58% of digital media payments were late in H1 2025, and businesses with payment delays are 1.4x more likely to face cash flow issues

- Your actual funding timeline may differ from advertised – Audit 30 days of transactions to measure real elapsed time from sale to deposit, not what your processor claims

- Chargeback rates directly affect funding speed – Processors delay funds for higher-risk accounts, so proactive chargeback defense can unlock faster funding

- Batch timing matters – Setting your batch time before your processor’s cutoff can shave a full day off your funding timeline

- Calculate total cost, not just rates – A slightly higher transaction fee with next-day funding may cost less than a lower rate with 4-day delays when you factor in credit line interest and opportunity cost

What This Guide Covers

This guide is for eCommerce managers at established online businesses who are tired of waiting 3-5 days (or longer) to access their own revenue. You manage a team, handle real volume, and understand that cash flow timing directly impacts your ability to operate and grow.

By the end, you’ll understand exactly how delayed deposits hurt your business, what to look for in an eCommerce payment gateway that offers next-day funding, and how to evaluate whether your current payment processing solutions are costing you more than you realize.

We won’t cover basic payment gateway setup or beginner eCommerce concepts. This is about solving a specific operational problem: getting your money faster so you can run your business better.

Why Delayed Funding Is a Business Risk, Not Just an Inconvenience

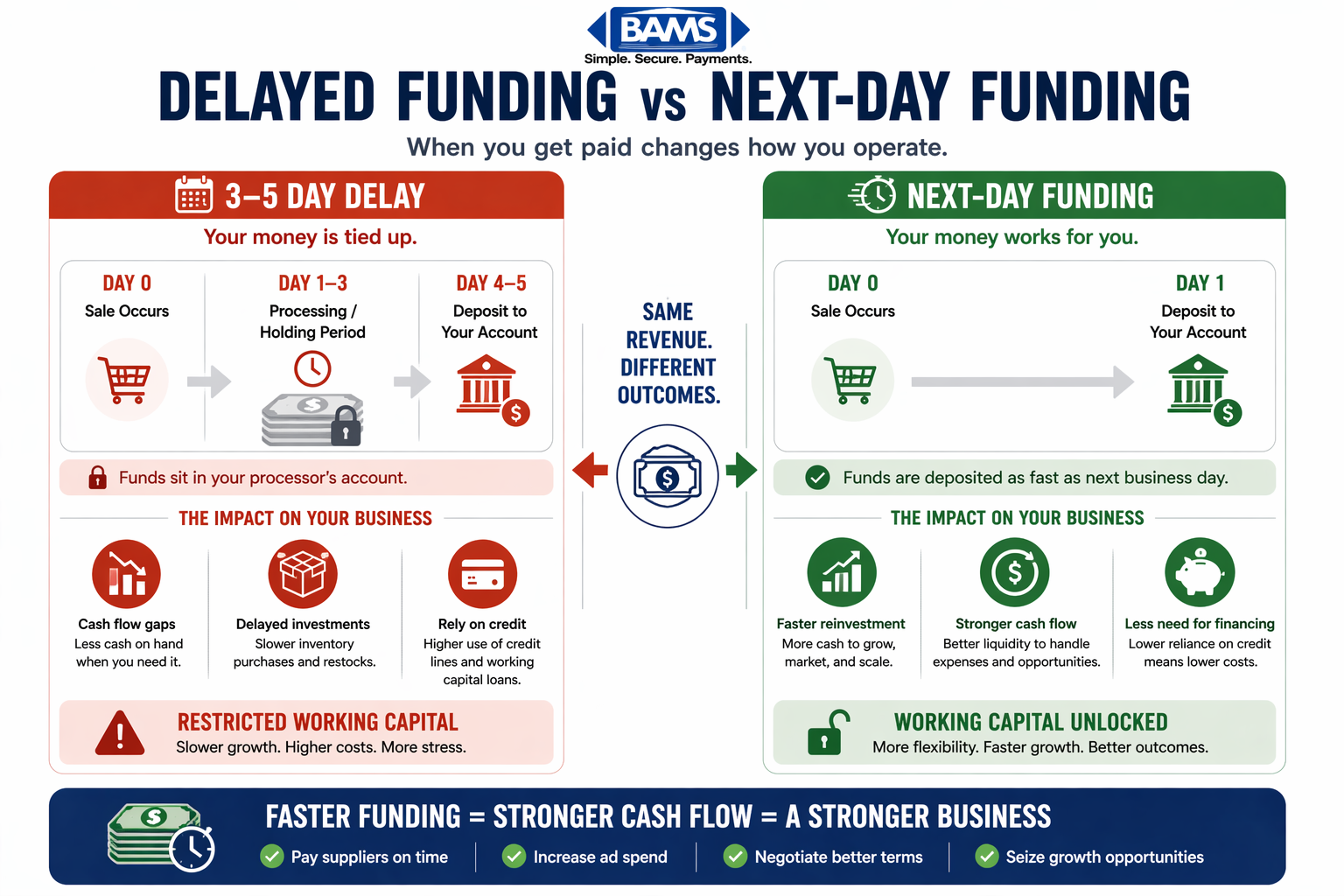

A comparison of delayed funding versus next-day funding, illustrating how slower deposits tie up cash and limit business operations.

Late payments have reached crisis levels. This isn’t a minor trend; it’s a structural shift in how money moves through digital commerce.

The downstream effects are severe. When your eCommerce payment gateway holds funds for 3-5 business days, you’re essentially extending an interest-free loan to your processor. Meanwhile, your suppliers want payment, your ad spend needs funding, and your team expects payroll. The gap between earning revenue and accessing it creates operational drag that compounds over time.

Payment processing timelines depend on how transactions move between banks, networks, and processors, with settlement and funding delays influenced by risk controls and processing infrastructure as outlined by Visa.

Core Concepts: Understanding the Funding Timeline

Settlement vs. Funding

Settlement is when the transaction clears between banks. Funding is when the money actually hits your account. Many processors conflate these terms, but they’re distinct. A transaction can settle in 24 hours while your funds sit in a holding account for days.

Reserve Requirements

Some processors hold a percentage of your transactions in reserve to cover potential chargebacks. This is standard for high-risk merchants, but many eCommerce businesses are classified as higher risk than necessary, resulting in unnecessary cash flow restrictions.

Batch Processing Windows

Your transactions are grouped into batches, typically once daily. When you batch (end of business day vs. midnight) affects when your funds begin their journey to your account. A 4 PM batch processes faster than an 11 PM batch.

The Real Cost of Delayed Deposits

Calculate this: take your average daily revenue, multiply by the number of days your processor holds funds, then consider what that capital could do if deployed immediately. For a business processing $50,000 monthly, a 4-day funding delay means roughly $6,500 is perpetually inaccessible. That’s working capital you’ve earned but cannot use.

A slightly higher rate with faster funding can outperform a cheaper option with delays, especially when using transparent interchange plus pricing that clearly shows your true processing costs.

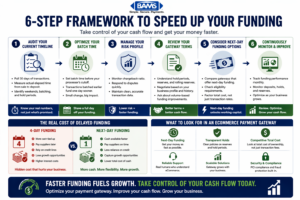

The Funding Optimization Framework

A step-by-step framework to optimize your funding timeline, reduce delays, and unlock faster access to your revenue.

Solving delayed deposits requires addressing four interconnected elements: processor selection, account configuration, operational timing, and risk profile management.

These aren’t sequential steps you complete once. They form a system that requires ongoing attention. Your processor determines baseline funding speed. Your account configuration affects whether you qualify for faster options. Your operational timing (when you batch, when you submit transactions) influences daily outcomes. And your risk profile, shaped by chargeback rates and transaction patterns, determines whether your processor sees you as a candidate for accelerated funding.

Most eCommerce managers focus only on processor selection and ignore the other three elements. That’s why businesses with identical processors can have dramatically different funding experiences.

Modern payment infrastructure emphasizes faster settlement visibility and improved control over transaction timing, helping businesses better manage cash flow according to Modern Treasury.

Step 1: Audit Your Current Funding Reality

Objective: Establish a factual baseline of how long your money actually takes to reach your account.

Pull your last 30 days of transactions and map each one from authorization to deposit. Don’t rely on your processor’s stated funding timeline; measure the actual elapsed time. You’ll likely find variation you didn’t expect.

Document the following for each transaction: authorization timestamp, batch timestamp, settlement date, and deposit date. Calculate the average, but also note outliers. A single delayed deposit during a cash-tight week can cause cascading problems.

What to avoid: Don’t accept “2-3 business days” as a sufficient answer. Push for specifics. Does that include weekends? What about holidays? What happens if you batch after a certain time?

Success indicators: You have a spreadsheet showing actual funding timelines for at least 30 transactions. You can identify patterns (Friday batches take longer, certain card types settle slower). You know your true average funding time, not your processor’s marketing claim.

Step 2: Evaluate Your Processor’s Funding Options

Objective: Determine whether faster funding is available with your current processor or requires switching.

Contact your processor directly and ask specific questions. Do they offer next-day funding? What are the requirements? Is there an additional fee? What percentage of their merchants actually receive next-day deposits?

Many processors advertise next-day funding but bury the requirements. You might need to maintain a certain volume, keep chargebacks below a threshold, or pay a premium. Get these details in writing.

Compare what you learn against criteria for selecting eCommerce merchant services. The right payment processing solutions should offer transparent funding timelines without hidden conditions.

What to avoid: Don’t assume your current processor is your only option. Switching costs are real but often overestimated. Don’t let inertia keep you with a processor that’s holding your cash longer than necessary.

Success indicators: You have written documentation of your processor’s funding options, requirements, and fees. You’ve compared this against at least two alternatives. You can calculate the actual cost difference between your current setup and faster funding options.

Step 3: Optimize Your Risk Profile

Objective: Reduce the factors that cause processors to delay your funds.

Processors delay funding primarily because of perceived risk. High chargeback rates, irregular transaction patterns, and poor documentation all signal risk. Reducing these signals can unlock faster funding without changing processors.

Implement proactive chargeback defense. Use clear billing descriptors so customers recognize charges. Respond to disputes quickly with documentation. Consider chargeback defense programs that intercept disputes before they become chargebacks.

What to avoid: Don’t ignore chargebacks hoping they’ll resolve themselves. Don’t use vague billing descriptors that confuse customers. Don’t assume your chargeback rate is “normal” without benchmarking.

Success indicators: Your chargeback rate is below 1% (ideally below 0.5%). You have documentation ready for common dispute types. You’re tracking dispute reasons to identify and fix root causes.

Step 4: Configure Optimal Batch Timing

Objective: Align your operational timing with your processor’s funding windows.

Most processors have cutoff times for same-day batch processing. Transactions batched after the cutoff don’t begin processing until the next business day. If your cutoff is 4 PM Eastern and you batch at 5 PM, you’ve added a full day to your funding timeline.

Review your current batch settings. Many eCommerce platforms default to end-of-day batching, which might be midnight in your server’s timezone. Adjust this to batch before your processor’s cutoff.

Consider multiple daily batches if your volume supports it. Some processors allow this, and it can accelerate funding for morning transactions.

What to avoid: Don’t batch during weekends or holidays expecting next-day funding. Most processors don’t process on non-business days. Don’t set batch times without confirming your processor’s actual cutoff time (not the one in their marketing materials).

Success indicators: Your batch time is set at least 2 hours before your processor’s cutoff. You’ve tested this by tracking funding times before and after the adjustment. Weekend transactions are batched for Monday processing, not left pending.

Step 5: Select a Funding-Optimized Payment Gateway

Objective: Choose an eCommerce payment gateway specifically designed for fast, reliable funding.

If your current processor can’t deliver next-day funding, or charges excessive fees for it, switching may be the right move. The key is selecting a processor where fast funding is standard, not a premium add-on.

Evaluate potential processors on these criteria: standard funding timeline (not “up to” or “as fast as”), requirements for next-day funding, transaction fee structure (interchange-plus is typically more transparent than tiered pricing), chargeback support, and integration with your eCommerce platform.

When opening a new merchant account, ask specifically about funding timelines during underwriting. Get commitments in writing before signing.

What to avoid: Don’t choose based on the lowest advertised rate without understanding the funding timeline. A processor charging 0.1% less but holding funds 3 days longer may cost you more in operational impact. Don’t overlook integration complexity; a gateway that doesn’t work smoothly with your platform creates ongoing friction.

Success indicators: You’ve received written confirmation of funding timelines from at least two potential processors. You’ve calculated the total cost including fees and opportunity cost of delayed funding. You’ve verified integration compatibility with your eCommerce platform.

Selecting the right processor starts with choosing an integrated payment gateway that offers reliable next-day funding, clear settlement timelines, and minimal processing delays.

Step 6: Implement and Monitor

Objective: Execute your chosen strategy and verify results.

Whether you’re optimizing with your current processor or switching to a new one, implementation requires careful execution. If switching, plan for a transition period where you may be processing through two systems.

Set up tracking from day one. Create a simple spreadsheet that logs each day’s batch total, batch time, and actual deposit date. Review this weekly for the first month, then monthly thereafter.

Establish alerts for funding delays. If your processor commits to next-day funding and you don’t receive a deposit by a certain time, that’s a conversation to have immediately, not something to notice weeks later.

What to avoid: Don’t assume the switch solved everything and stop monitoring. Funding timelines can drift. Don’t ignore small delays; they often indicate larger problems developing.

Success indicators: You have a monitoring system in place. You’ve verified that actual funding times match commitments. You have a clear escalation path when delays occur.

What This Looks Like in Practice

Consider an eCommerce business processing $75,000 monthly with a 4-day average funding delay. That’s roughly $10,000 perpetually tied up in the payment pipeline. During a growth phase requiring inventory investment, this business had to use a credit line to bridge the gap, paying interest on money they’d already earned.

After switching to a processor offering genuine next-day funding and optimizing batch timing, their average funding delay dropped to 1.2 days. The $8,000+ freed up eliminated their need for the credit line. The annual savings in interest alone exceeded the slightly higher per-transaction fees of the new processor.

The calculation isn’t always this clear-cut. Some businesses have predictable cash flow and can absorb delays. Others operate on tight margins where every day of delay creates measurable strain. Know which category you’re in before deciding how aggressively to pursue faster funding.

Common Mistakes That Keep Your Money Stuck

Accepting stated timelines without verification. Processors advertise best-case scenarios. Your actual experience depends on your specific account configuration, risk profile, and operational timing. Measure, don’t assume.

Ignoring chargeback impact. Every chargeback affects your risk profile. Processors respond to elevated chargebacks by slowing funding, increasing reserves, or both. Proactive defense pays dividends beyond just avoiding the chargeback fees.

Optimizing for rate instead of total cost. A 0.2% lower rate means nothing if you’re paying interest on a credit line to cover the cash flow gap. Calculate the full cost of your payment processing solutions, including the opportunity cost of delayed access to funds.

Treating this as a one-time project. Funding optimization requires ongoing attention. Processors change policies, your transaction patterns evolve, and new options emerge. Review your setup quarterly.

What to Do Next

Rising card processing costs and payment friction continue to impact merchant cash flow, particularly for businesses operating on tight margins as highlighted by Merchant Payments Coalition. Start with the audit. Before making any changes, understand your current reality. Pull 30 days of transactions and calculate your actual funding timeline. This gives you the baseline to measure any improvements against.

If your audit reveals funding delays significantly longer than your processor’s stated timeline, that’s your first conversation. Sometimes a simple account review can unlock faster funding you were already eligible for.

If your processor can’t or won’t improve your funding timeline, use the criteria in this guide to evaluate alternatives. The right merchant account setup should deliver next-day funding as standard, not as a premium feature you have to negotiate for.

Your revenue belongs in your account, working for your business. Every day it sits in a processor’s pipeline is a day you’re subsidizing someone else’s cash flow instead of your own.

Frequently Asked Questions

What is a payment gateway and why is it important for eCommerce?

A payment gateway is the technology that securely transmits transaction data between your online store, the customer’s bank, and your merchant account. For eCommerce, it’s the critical infrastructure that enables you to accept credit cards, digital wallets, and other payment methods. The gateway you choose directly affects your funding speed, security compliance, and customer checkout experience.

How do I choose the best payment gateway for my business?

Focus on four factors: funding timeline (how quickly you actually receive deposits), fee transparency (interchange-plus pricing is typically clearer than tiered), integration compatibility with your eCommerce platform, and support quality. Request written commitments on funding timelines before signing, and verify claims by asking what percentage of merchants actually receive the advertised funding speed.

When should I consider switching my payment gateway?

Consider switching when your actual funding timeline exceeds 2-3 business days consistently, when your processor can’t provide transparent fee breakdowns, when chargeback support is reactive rather than proactive, or when you’re paying premium fees for features that should be standard (like next-day funding). Calculate the total cost including opportunity cost of delayed funds before deciding.

What causes payment processors to delay funding?

Processors delay funding based on perceived risk. High chargeback rates, irregular transaction patterns, new account status, and industry classification all affect funding speed. Reducing your chargeback rate, maintaining consistent transaction volumes, and building account history can all help accelerate your funding timeline with any processor.

How much does delayed funding actually cost my business?

Calculate your average daily revenue and multiply by the number of days your funds are delayed. This is capital you’ve earned but can’t deploy. For a business processing $50,000 monthly with a 4-day delay, roughly $6,500 is perpetually inaccessible. Add any interest you’re paying on credit lines to bridge cash flow gaps for a more complete picture.

What’s the difference between next-day funding and same-day funding?

Next-day funding means deposits arrive the business day after you batch your transactions. Same-day funding means deposits arrive the same day you batch (before a cutoff time). Same-day funding is rare and typically requires premium fees or specific account qualifications. For most eCommerce businesses, reliable next-day funding provides sufficient cash flow improvement without the added cost.