Payment Cost Reduction: A Chargeback Prevention Guide

How eCommerce managers can cut processing fees and dispute losses with transparent pricing and digital wallet strategies

Learn how to audit your effective processing rate, eliminate hidden fees, and implement chargeback prevention methods that protect margins. This guide covers processor statement analysis, digital wallet payment optimization, and building a prevention-first cost reduction system.

TL;DR

- Transparency is the foundation – You cannot reduce payment costs or prevent chargebacks without interchange-plus pricing that separates every fee line.

- Pricing and chargebacks are connected – Dispute ratios affect interchange qualification, and opaque pricing hides the true cost of every chargeback.

- Digital wallet payments do double duty – Properly configured wallets lower interchange costs and reduce chargebacks through biometric authentication.

- Real-time alerts prevent up to 91% of chargebacks – Combine alerts with optimized billing descriptors and strong evidence documentation for maximum impact.

- Start with an effective rate audit – Pull three months of statements, calculate total fees divided by volume, and identify every fee line before changing anything.

Guide Orientation: What This Covers

This guide shows eCommerce managers how transparent pricing and chargeback prevention methods work together to drive real payment cost reduction. You’ll learn how to decode processor statements, spot hidden fees, structure digital wallet payments for lower dispute rates, and build a defense system that protects margin.

This is written for eCommerce managers running 10-50 person operations who already process meaningful volume and want tighter control over fees and funding timelines. It does not cover basic payment terminology, crypto gateways, or enterprise payment orchestration.

By the end, you’ll be able to audit your current effective rate, identify where fees are leaking, and implement a prevention-first approach that reduces both transaction costs and chargeback losses.

Why Transparent Pricing Matters Right Now

Processing fees and chargeback losses are climbing, and opaque pricing makes both worse. When your statement bundles interchange, assessments, and processor markup into a single number, you lose the ability to negotiate, compare, or audit. That opacity directly inflates the cost of every transaction and every dispute.

The chargeback problem compounds the pricing problem. According to Visa, disputes introduce additional operational costs beyond the transaction itself, including administrative handling and lost revenue.

Meanwhile, digital wallet adoption is accelerating. Apple Pay, Google Pay, and Shop Pay now handle a growing share of eCommerce checkout. According to the Federal Reserve, payment method structure directly impacts overall transaction cost efficiency. These methods carry different fee structures and fraud profiles than card-not-present transactions, which means your pricing model and prevention stack need to account for them. Businesses that ignore this shift overpay on every wallet transaction and miss the lower chargeback rates these methods can deliver when configured correctly. Transparency is the foundation. Without it, every optimization effort is guesswork.

Core Concepts You Need to Understand

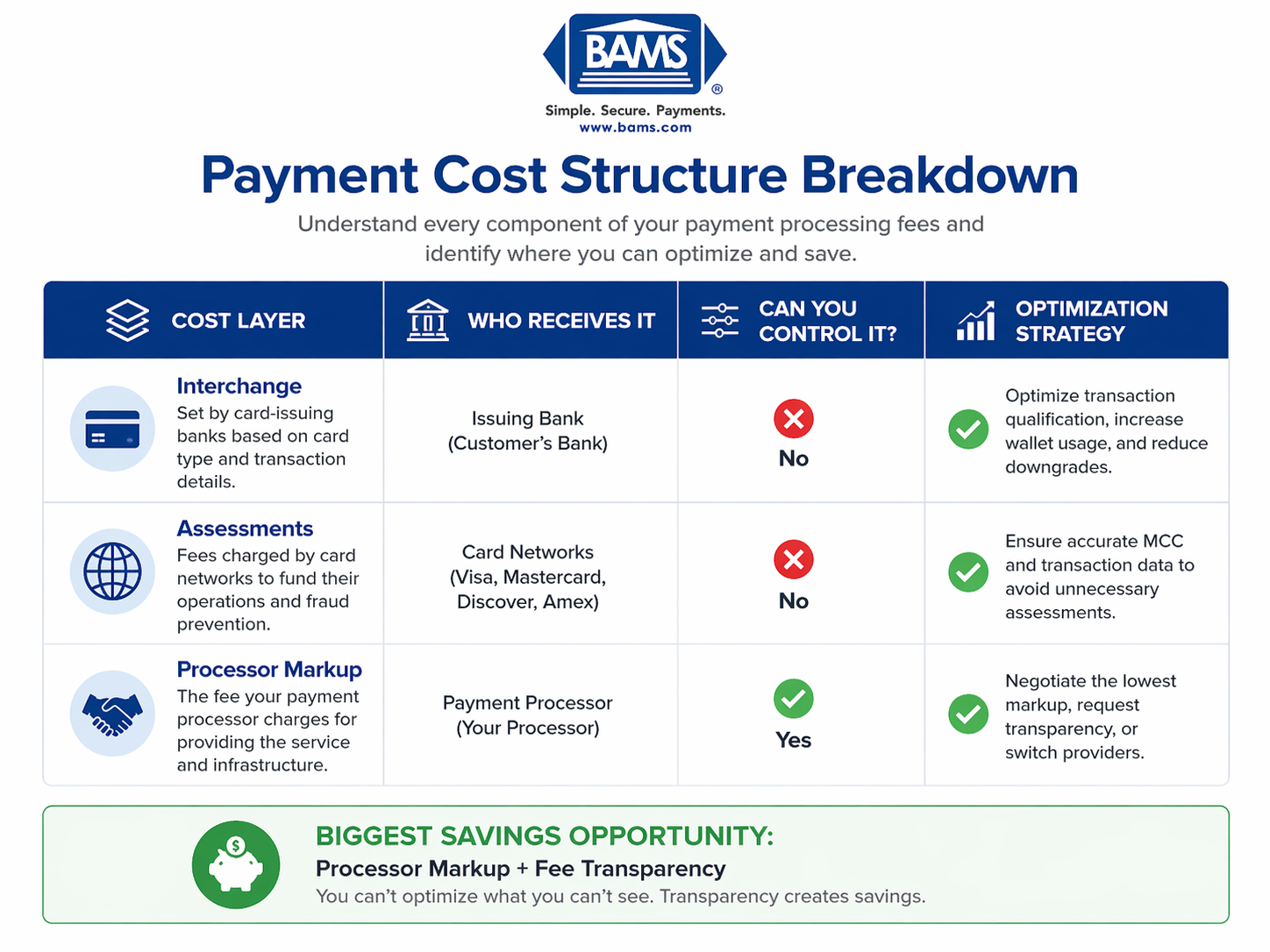

The Three Layers of Every Transaction Fee

Understanding the three layers of payment costs helps merchants identify where savings opportunities exist.

Every card transaction has three cost components: interchange (paid to the card-issuing bank), assessments (paid to Visa, Mastercard, etc.), and the processor markup. Interchange and assessments are fixed by the networks. Only the markup is negotiable. Flat-rate pricing hides all three inside one number. Interchange-plus pricing separates them, so you can see exactly what your processor earns.

Hidden Fees vs. Disclosed Fees

Hidden fees are not illegal, they are just not highlighted. Common ones include PCI non-compliance fees, batch fees, monthly minimums, statement fees, IRS reporting fees, and tiered downgrade charges when transactions fall into non-qualified buckets.

Chargebacks Are a Pricing Problem

Most merchants treat chargebacks as a fraud issue. They are actually a pricing issue too. Every dispute carries a fee, and high chargeback ratios push you into monitoring programs that carry even higher fees. Your pricing transparency and your dispute ratio are connected line items on the same P&L.

The Framework: Transparency Plus Prevention

The framework has two tracks that run in parallel.

Track 1: Pricing Transparency. Move to interchange-plus pricing, audit your statement monthly, and eliminate fees that do not tie to a real service. This gives you a clean effective rate and a baseline to measure against.

Track 2: Chargeback Prevention. Deploy real-time alerts, optimize billing descriptors, push customers toward digital wallet payments with strong authentication, and document every transaction for dispute response.

These tracks reinforce each other. Transparent pricing reveals the true cost of each chargeback. Prevention lowers your dispute ratio, which qualifies you for better interchange categories and keeps you out of penalty programs. Skip either track and you leave money on the table.

Step-by-Step Breakdown

Step 1: Audit Your Current Effective Rate

Objective: Know exactly what you pay, per transaction, across every fee line.

Pull three months of processor statements. Calculate your effective rate by dividing total fees by total processed volume. Most eCommerce merchants on flat-rate pricing run 2.9% to 3.5%. On interchange-plus, the all-in rate typically lands between 2.2% and 2.7% depending on card mix.

List every fee on the statement. Categorize each as interchange pass-through, network assessment, processor markup, or ancillary (PCI, gateway, batch, statement, monthly minimum). Ancillary fees are where hidden costs hide.

Anti-patterns: Comparing only the advertised rate. Ignoring monthly fixed fees because they seem small. Assuming your processor applies interchange optimization automatically.

Success indicators: You can state your effective rate to two decimal places, list every line-item fee, and identify at least two charges you cannot justify.

Step 2: Switch to Interchange-Plus Pricing

Objective: Make every component of your cost visible and negotiable.

Interchange-plus quotes the processor markup as a fixed number above interchange, for example “interchange + 0.25% + $0.10.” You see exactly what the networks charge and exactly what your processor earns. Flat-rate pricing feels simpler but typically costs 40 to 80 basis points more on qualified transactions.

Request interchange-plus pricing in writing. Ask for a side-by-side comparison using your last 90 days of transaction data. If your current processor will not provide one, that is a signal. To better understand how pricing impacts your overall processing strategy, explore payment gateway solutions.

Anti-patterns: Accepting “we’ll match your current rate” without a full line-item breakdown. Signing multi-year contracts with early termination fees. Overlooking PCI fees, gateway fees, and batch fees in the comparison.

Success indicators: Your new statement shows interchange, assessments, and markup as separate lines. Your effective rate drops by at least 15 to 40 basis points.

Step 3: Configure Digital Wallet Payments for Lower Costs and Fewer Disputes

Objective: Route more transactions through wallets that carry lower fraud risk and better authentication.

Digital wallet payments like Apple Pay and Google Pay use tokenization and device-level biometric authentication. This qualifies many transactions for lower interchange categories and significantly reduces chargeback exposure because “I didn’t authorize this” claims are much harder to sustain against biometric proof.

Enable wallet options at checkout with equal visual weight to card entry. Test one-click flows. Confirm your gateway passes the correct indicators to the network so you earn the better interchange rate. Many merchants enable wallets but lose the rate benefit because the gateway is misconfigured.

Anti-patterns: Burying wallet buttons below card fields. Running wallets through a gateway that flattens them into standard card-not-present transactions. Ignoring wallet-specific dispute evidence when responding to chargebacks.

Success indicators: Wallet transactions make up 25%+ of checkout volume. Your chargeback ratio on wallet transactions is meaningfully lower than on keyed card transactions.

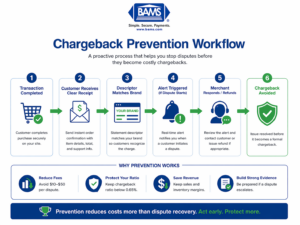

Step 4: Deploy Real-Time Chargeback Alerts

A structured prevention workflow reduces disputes before they become costly chargebacks.

Objective: Stop disputes before they become chargebacks.

Real-time alert networks notify you when a customer initiates a dispute with their bank, giving you a narrow window to refund the transaction and avoid a formal chargeback. According to Visa, early intervention in the payment lifecycle plays a critical role in reducing dispute escalation.

BAMS includes proactive chargeback defense and alert integration as part of its merchant services package, so you get prevention tooling without assembling vendors yourself. Learn more about chargeback defense solutions.

Anti-patterns: Refunding every alert without checking for friendly fraud patterns. Letting alerts sit unprocessed past the response window. Treating alerts as a substitute for good billing descriptors and order confirmations.

Success indicators: Alert response time under 12 hours. Chargeback ratio trending below 0.65%. Dispute win rate above 40% on cases you choose to fight.

Step 5: Optimize Descriptors, Receipts, and Evidence

Objective: Eliminate the friendly fraud and customer confusion that drive disputes.

Your billing descriptor is the single most overlooked prevention tool. If customers see a charge they don’t recognize on their statement, they dispute. Use a descriptor that matches your storefront name and includes a support phone number. Send order confirmation emails with itemized details, shipping tracking, and clear refund instructions.

Document delivery proof, IP address, AVS/CVV match results, and device fingerprints for every transaction. When a dispute comes in, this evidence is the difference between winning and losing.

Anti-patterns: Using your LLC’s legal name as the descriptor. Generic “thank you for your order” emails with no item detail. Failing to retain evidence past 60 days.

Success indicators: Non-fraud disputes drop by 30%+ within 90 days. Dispute response packages assemble in under 15 minutes.

Step 6: Run Monthly Statement Audits

Objective: Catch pricing drift, surprise fees, and category downgrades before they compound.

Processors periodically adjust fees, add line items, or reclassify transactions into higher-cost categories. Without a monthly audit, these changes go unnoticed for quarters. Set a recurring 30-minute review: compare effective rate month-over-month, flag any new fee lines, and confirm interchange categories match expected mix.

Anti-patterns: Only reviewing statements when something feels wrong. Accepting “network fee increase” explanations without verification. Skipping audits during busy seasons, which is when drift hides best.

Success indicators: Effective rate stays flat or declines. No unexplained fee lines persist across two consecutive statements.

Practical Example: A Mid-Size Apparel Brand

An apparel brand processing $450,000/month on flat-rate 2.9% + $0.30 pricing pays roughly $14,200 in fees. Chargeback ratio sits at 0.9%, generating around 40 disputes per month at $25 each, or $1,000 in fees plus lost revenue.

After switching to interchange-plus at roughly 2.45% all-in, monthly fees drop to about $11,000, saving $3,200/month. Adding real-time alerts and descriptor optimization cuts the chargeback ratio to 0.35%, reducing dispute fees by 60%. Enabling digital wallet payments shifts 30% of volume into lower interchange tiers, saving another $600/month.

Combined annual savings: roughly $50,000. The transparency was the unlock. Without seeing each cost line separately, none of these moves would have been visible.

Common Mistakes and Pitfalls

Chasing the lowest advertised rate. The teaser rate rarely reflects your effective rate. Ancillary fees and category downgrades make the difference.

Treating pricing and chargebacks as separate problems. They share a P&L line. Prevention lowers interchange qualification. Transparency reveals dispute costs.

Enabling digital wallets without configuring the gateway. You get the checkout convenience but miss the interchange benefit.

Signing long contracts with ETFs. Flexibility matters more than a 10-basis-point discount when your volume or risk profile changes.

Refunding every chargeback alert reflexively. This trains friendly fraud and erodes your dispute win rate. Build decision rules.

Ignoring PCI and compliance fees. These are often the largest hidden line items. Confirm you are actually receiving the service the fee names.

What to Do Next

Start with one action this week: pull your last three processor statements and calculate your effective rate. That single number tells you whether the rest of the framework is worth your time. If your effective rate is above 2.7% on eCommerce volume, the savings opportunity is almost certainly significant.

From there, work the framework at your own pace. Pricing transparency and chargeback prevention are not one-time projects. They are operational disciplines that compound over months. Use this guide as a reference when you review statements, evaluate processors, or investigate a spike in disputes. Progress comes from consistent small adjustments, not heroic overhauls.

Frequently Asked Questions

What are merchant fees and how do they work?

Merchant fees are the total costs charged to accept electronic payments. They include interchange (paid to the issuing bank), network assessments (paid to Visa, Mastercard, etc.), and your processor’s markup. Flat-rate pricing bundles all three into one number. Interchange-plus pricing separates them so you can see and negotiate the markup.

Which pricing model is better: interchange-plus or flat rate?

Interchange-plus is almost always better for eCommerce businesses processing more than $20,000/month. You see exactly what each component costs and can audit your processor’s markup. Flat rate is simpler but typically costs 40-80 basis points more on qualified transactions, which adds up quickly at volume.

What are common hidden fees in merchant services?

The most common hidden fees include PCI non-compliance penalties, monthly minimum fees, batch fees, statement fees, IRS reporting fees, gateway fees, and tiered downgrade charges when transactions fall into non-qualified categories. These often add 30-60 basis points to your effective rate beyond the advertised processing rate.

How can real-time chargeback alerts reduce my costs?

Real-time alerts notify you when a customer initiates a dispute, giving you a short window to refund before it becomes a formal chargeback. This avoids the $10-$50 dispute fee, protects your chargeback ratio, and keeps you out of card network monitoring programs that carry additional penalties.

Do digital wallet payments actually lower chargeback rates?

Yes, when configured correctly. Wallets like Apple Pay and Google Pay use tokenization and biometric authentication, which qualifies many transactions for lower interchange categories and makes “unauthorized transaction” disputes much harder to sustain. The key is ensuring your gateway passes the correct indicators to the network so you receive the rate benefit.

When should I consider switching payment processors?

Consider switching if your effective rate is above 2.7% on eCommerce volume, your processor cannot provide interchange-plus pricing, you see unexplained fees on statements, or your support experience is reactive rather than proactive. Also switch if your contract includes early termination fees that prevent normal business flexibility.