Chargeback Risk Management: The Hidden Cash Flow Lever

Why your processor’s default risk settings are designed to protect them, not your deposit timeline

Learn how chargeback risk management settings quietly control when you actually get paid. This piece reframes compliance defaults as negotiable cash flow variables that processors pre-set in their favor.

TL;DR

- Default risk settings control your cash flow – Processors assign conservative fraud filters, chargeback thresholds, and rolling reserves at onboarding that delay deposits, and most merchants never realize these are negotiable.

- Internal thresholds are stricter than network rules – Your processor may flag your account at a 0.3-0.5% chargeback rate, well below Visa’s 0.9% threshold, triggering holds you didn’t see coming.

- Chargeback risk management is a funding speed strategy – Keeping dispute rates low isn’t just about avoiding penalties. It’s about preventing your processor from ever having a reason to tighten reserves or delay settlements.

- Treat onboarding as financial negotiation – Batch timing, risk tiers, and reserve percentages are all adjustable variables. The merchants who get next-day funding are the ones who configure these deliberately instead of accepting defaults.

Your Processor Already Decided When You Get Paid

Before you processed your first transaction, your payment processor made a series of decisions about your money. Risk review thresholds, chargeback monitoring tiers, fraud filter sensitivity, reserve requirements. None of these showed up in your sales pitch. All of them showed up in your cash flow. For eCommerce managers running established businesses, chargeback risk management isn’t an afterthought. It’s the invisible architecture that determines whether your deposits land tomorrow or get frozen for weeks.

The Compliance Checkbox Myth

The standard advice around merchant services setup treats risk and compliance configuration as administrative housekeeping. Get your PCI attestation filed. Accept the default fraud filters. Sign the chargeback policy acknowledgment. Move on to the important stuff, like integration and design.

This framing made sense when processors operated with more uniform underwriting. But the economics of payment processing have shifted. The standard advice around merchant services setup treats risk and compliance configuration as administrative housekeeping. But the economics of payment processing have shifted. Visa chargeback resources continue to highlight the importance of dispute prevention and proactive risk management for merchants processing card payments. The result: what looks like a compliance checkbox is actually a cash flow lever, pre-set to protect the processor, not you.

Most eCommerce managers never question these defaults because they were never told the defaults were negotiable.

Risk Settings Are Cash Flow Settings

Here’s what we actually believe: the risk configuration your processor assigns at onboarding is the single biggest determinant of how fast you get paid, and most merchants never realize it’s adjustable.

This isn’t about compliance. It’s about control. Every threshold, every filter, every reserve percentage is a variable that directly shapes your deposit timing, your hold frequency, and your operating capital.

Most merchants think deposits are controlled by funding schedules. In reality, risk settings often determine whether funds arrive tomorrow or get delayed.

How Default Chargeback Risk Management Quietly Freezes Your Revenue

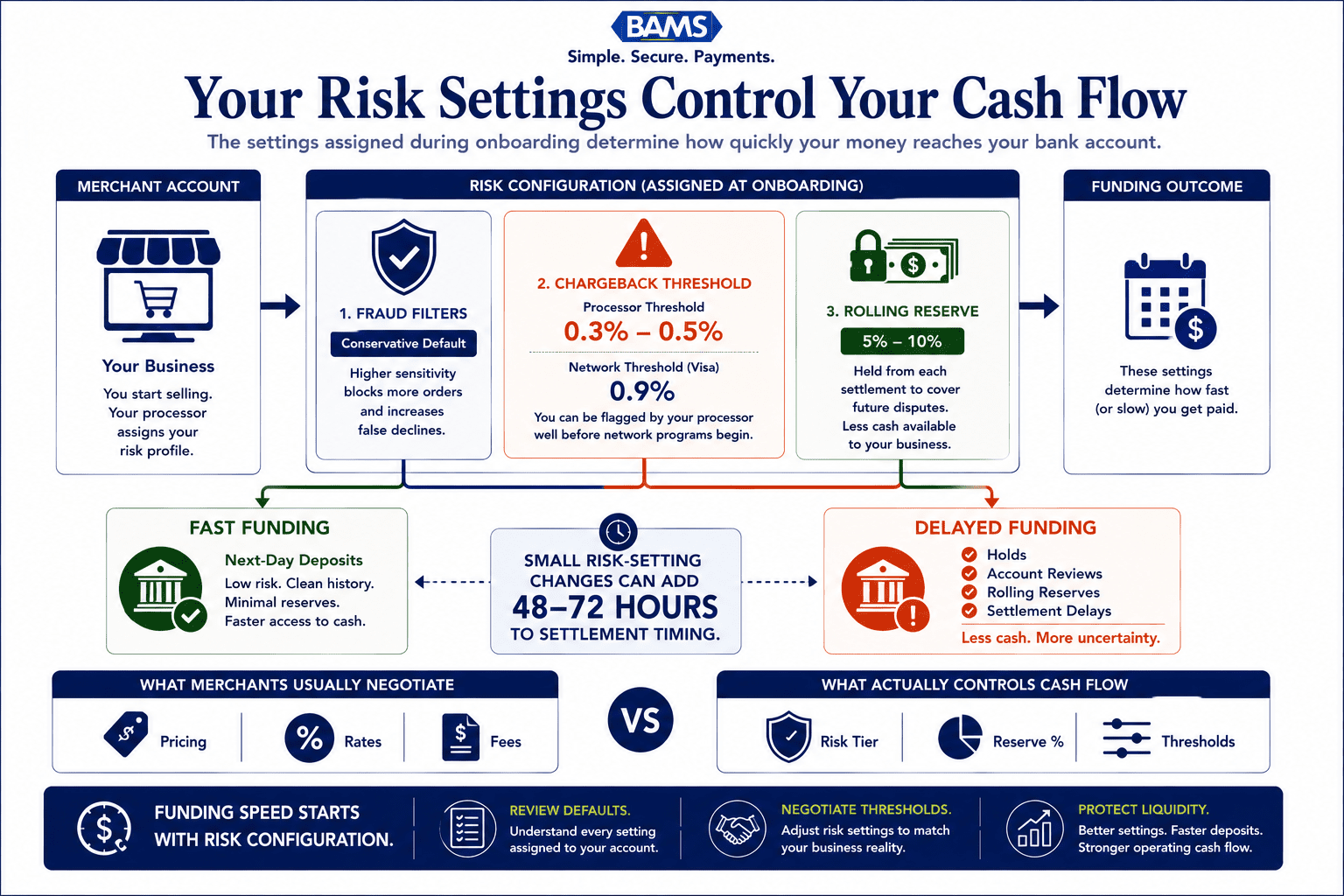

Let’s trace the mechanics. When a processor onboards a new merchant account, their underwriting team assigns a risk profile. That profile determines your fraud filter sensitivity, your chargeback ratio monitoring threshold, and whether a rolling reserve gets applied to your deposits. For most mid-market eCommerce businesses, these settings land on conservative defaults.

Conservative means: tighter fraud filters that decline more legitimate transactions. Lower chargeback ratio triggers that flag your account faster. And sometimes a 5-10% rolling reserve held against future disputes, quietly siphoning cash from every batch settlement.

The processor’s logic is straightforward. Mastercard chargeback guidance emphasizes the importance of monitoring dispute activity and maintaining effective prevention practices before chargebacks become an operational or financial issue. Processors aren’t being malicious. They’re managing portfolio-level exposure. But their risk tolerance isn’t calibrated to your business. It’s calibrated to their worst-case scenario across thousands of merchants.

We’ve seen the pattern repeatedly. An established eCommerce brand with clean transaction history and low dispute rates gets the same conservative defaults as a brand-new dropshipper with no track record. The result? Deposits that should arrive next day get held for review. Batch settlements that should clear overnight get delayed by 48 to 72 hours. And nobody explains why, because the settings were buried in onboarding paperwork nobody reads closely.

The Chargeback Ratio Trap

Here’s where it gets particularly costly. The average chargeback rate hit 0.26% in Q3 2025, according to recent industry data. Card networks like Visa and Mastercard set their monitoring thresholds at 0.9% to 1.0%. But many processors set internal thresholds far lower, sometimes at 0.5% or even 0.3%, to give themselves an early warning buffer.

When your account crosses your processor’s internal threshold (not the network threshold), they can impose holds, increase reserves, or delay funding. You’re technically in good standing with Visa. But your processor has already decided you’re a risk. And they made that decision based on a default setting you never negotiated.

Many merchants stay below network limits yet still trigger funding restrictions because processors use stricter internal thresholds.

What Actually Unlocks Faster Deposits

The eCommerce managers who get next-day funding consistently aren’t just picking the right processor. They’re configuring three specific variables at setup:

- Batch cutoff timing aligned to their sales patterns, not the processor’s default window

- Risk thresholds adjusted to reflect their actual dispute history, not a generic risk tier

- Reserve requirements negotiated based on transaction volume and chargeback data, not left at onboarding defaults

This is where a partner like BAMS changes the equation. Their approach treats onboarding configuration as infrastructure design, with dedicated account managers who adjust risk settings and batch timing to match your actual business profile rather than leaving you on processor defaults. The difference between a two-day hold and next-day funding often comes down to a single conversation that most processors never initiate.

Similarly, proactive chargeback defense (alerts, prevention tools, representment support) isn’t just about winning disputes. It’s about keeping your chargeback ratio low enough that your processor never triggers the internal thresholds that justify holds in the first place. BAMS builds this into their merchant services model specifically because they understand the upstream relationship between dispute rates and deposit speed.

The Cost of Not Knowing This

If this framing is correct, and risk configuration is the upstream cause of delayed deposits, then most eCommerce businesses are solving the wrong problem. They’re shopping for lower interchange rates while their real cash flow bottleneck sits in a risk settings panel they’ve never seen.

Consider the math. A business processing $500,000 per month with a 7% rolling reserve has $35,000 in limbo at any given time. That’s not a fee on your statement. It’s invisible capital you can’t use for inventory, payroll, or growth. And it was determined by a default setting, not a deliberate business decision. Federal Reserve Small Business Survey data continues to show that access to working capital and cash flow management remain among the most important operational concerns for growing businesses.

The merchants who win aren’t necessarily fighting fewer chargebacks. They’re managing their risk profile so aggressively that their processor never has a reason to tighten the screws. That’s a fundamentally different strategy than treating compliance as a checkbox.

A New Way to Think About Payment Processing Setup

Stop thinking of processor onboarding as “getting set up.” Start thinking of it as negotiating the terms of your own cash flow.

Every default is a decision someone else made about your money. Fraud filter sensitivity decides how many sales you lose to false declines. Chargeback thresholds decide when your deposits get held. Reserve percentages decide how much working capital you surrender without even knowing it. The online payment gateway setup process is where these variables get locked in, and it’s the last time most merchants think about them.

The merchants who get paid fastest are the ones who treat risk configuration as financial strategy, not administrative paperwork.

Your Defaults Are Not Your Destiny

The hidden fees in payment processing aren’t always line items. Sometimes they’re the opportunity cost of capital you can’t access because a risk threshold you never chose got triggered by a dispute pattern you could have prevented. Every one of those variables is adjustable. The question is whether anyone at your processor has ever offered to adjust them for you.

Frequently Asked Questions

Why are my deposits delayed even though my chargeback rate is below the card network threshold?

Most processors set internal risk thresholds well below the Visa or Mastercard monitoring limits. Your account can be flagged for holds or reserves at 0.3% to 0.5%, even though network programs don’t trigger until 0.9% or higher. Ask your processor what their internal threshold is and whether it’s negotiable based on your transaction history.

What documents do I need to gather before switching merchant service providers?

At minimum, prepare three to six months of processing statements, your current chargeback ratio data, bank verification documents, and your PCI compliance attestation. Having your dispute history ready gives a new provider the evidence to assign you a more favorable risk profile from day one rather than defaulting to conservative settings.

How do rolling reserves affect my cash flow if I have a low chargeback rate?

A rolling reserve holds a percentage of every batch settlement (typically 5-10%) for a set period, regardless of your current dispute performance. If your chargeback rate is consistently low, this reserve may be reducible or removable entirely, but only if you proactively request a review with your processor.