eCommerce Profitability: The Data Your Processor Ignores

Your platform already captures line-item detail — but flat-rate processors pocket the margin when they don’t pass it along

Learn how enriched transaction data already built into your eCommerce platform can unlock lower interchange rates. Discover why flat-rate processors have no incentive to submit it — and how that silence erodes your margins on every sale.

TL;DR

- Your platform already captures the data that unlocks lower rates – Tax amounts, freight charges, and product codes from your checkout can qualify transactions at cheaper interchange tiers, but most processors never submit them.

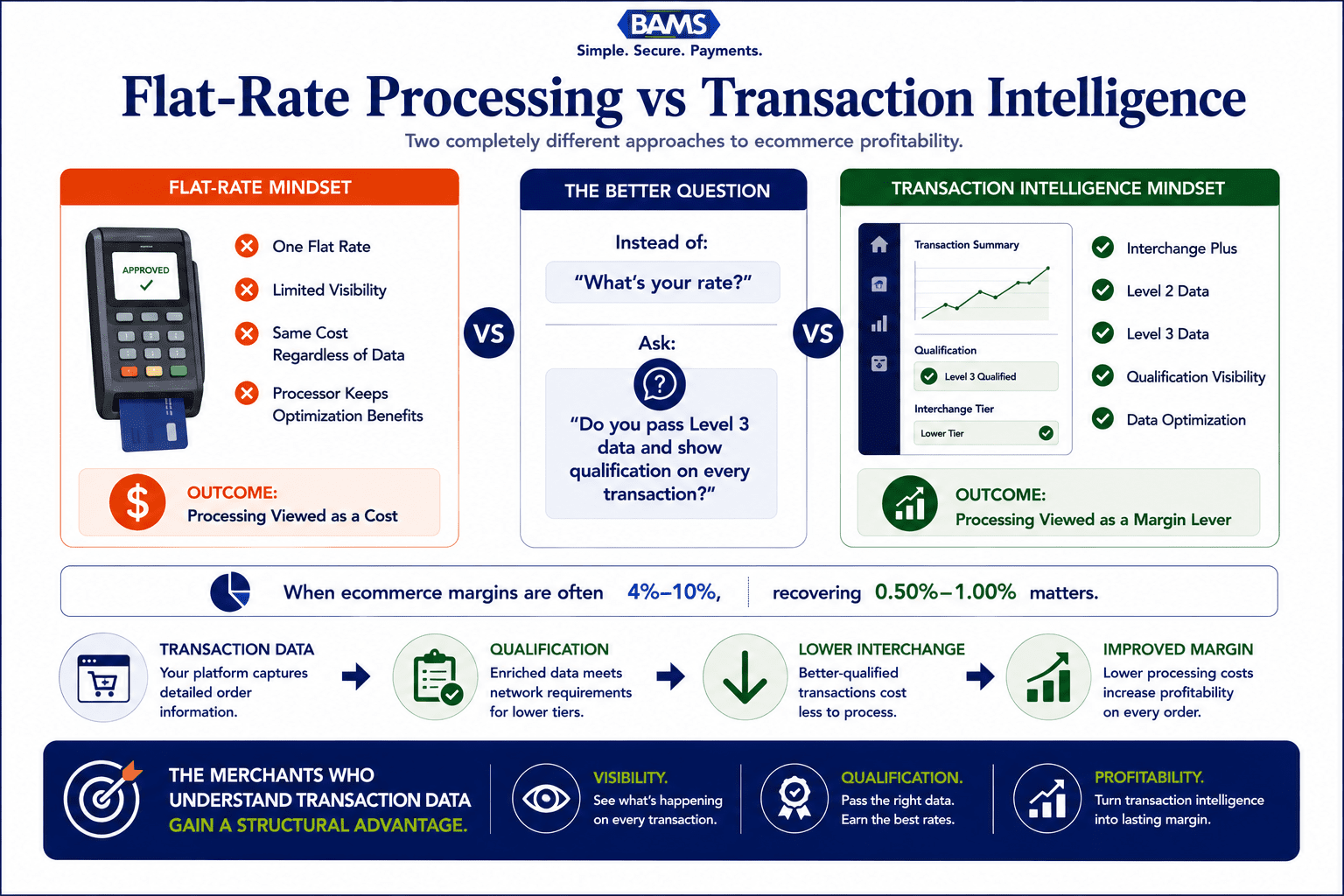

- Flat-rate pricing hides the savings from you – When your processor bundles interchange into one flat fee, they pocket the difference between what you pay and what the network actually charges. Interchange-plus pricing makes this visible.

- L3 data optimization is a structural margin advantage – With eCommerce profit margins averaging 4% to 10%, reducing processing costs by 0.50% or more per transaction through proper field mapping compounds into meaningful annual savings.

- The right processor question isn’t “what’s your rate?” – It’s “do you pass Level 3 data for my platform, and can I see interchange qualification on every transaction?”

Your Ecommerce Platform Already Knows Your Tax and Freight Data. Your Processor Probably Ignores It.

Every time a customer checks out on your store, your platform captures line-item detail: tax amounts, freight charges, product codes, quantities. That data exists. It’s sitting right there in the transaction record. But for the vast majority of eCommerce merchants, none of it ever reaches the card networks. And that silence is costing you real money on every single sale. The gap between what your platform knows and what your processor submits is one of the most overlooked drags on eCommerce profitability today.

Your checkout already collects the data. The real question is whether your processor submits it.

The Flat-Rate Comfort Zone

Most online merchants sign up with a payment processor, accept the quoted rate, and never look back. Flat-rate pricing made this easy. One number, no surprises, no homework. It became the default because it removed complexity, and for businesses doing a few thousand a month, the simplicity was worth the premium.

But as your volume grows, that simplicity becomes expensive. Flat-rate processors charge the same markup whether a transaction qualifies for the lowest interchange tier or the highest. They have no incentive to help you qualify for better rates. In fact, the less data they pass along, the wider the spread they pocket. Federal Reserve Small Business Survey data continues to show that margin management, cost control, and cash flow optimization remain critical priorities for growing businesses.

The Real Game Is Data, Not Negotiation

Here’s what we actually believe: the merchants who capture and pass enriched transaction data (Level 2 and Level 3) don’t just save on processing. They unlock a structural margin advantage that compounds with every order. This isn’t about haggling for ten basis points. It’s about understanding that interchange itself rewards better data, and building your payment stack to collect it.

How Interchange Actually Rewards Enriched Data

Visa and Mastercard built their interchange tables with data quality in mind. When a transaction includes only basic authorization data (card number, amount, approval code), it qualifies at the highest interchange tier. The card networks treat it as higher risk and charge accordingly.

But when a transaction includes Level 2 data (tax amount, merchant tax ID, customer code) and Level 3 data (line-item detail, product codes, freight amount, unit cost), the networks reduce the interchange rate. The logic is straightforward: more data means more transparency, which means lower fraud risk and easier reconciliation for the issuing bank. Lower risk, lower cost. Visa interchange reimbursement fee schedules demonstrate how enhanced transaction data and commercial card qualification can influence interchange categories and processing costs.

The savings are not trivial.

For B2B and government card transactions, Level 3 qualification can reduce interchange by 0.50% to 1.00% or more per transaction. For a merchant processing $500,000 a year in qualifying volume, that’s $2,500 to $5,000 back in margin, annually, without changing a single product price or acquiring a single new customer.

And here’s the part nobody talks about: your eCommerce platform already collects most of this data. Shopify, WooCommerce, BigCommerce, Magento (all of them) capture tax calculations, shipping costs, SKU-level detail, and quantity fields at checkout. The data exists in your order record. The question is whether your processor maps those fields and submits them downstream.

Most don’t. Flat-rate processors batch transactions with minimal data because it’s cheaper for them to operate that way. They absorb the interchange cost into their flat fee and keep the difference. When your transaction could have qualified at a lower tier but didn’t, you subsidize that gap. You just never see it on your statement because flat-rate pricing obscures the underlying interchange entirely.

This is where transparent pricing models like interchange-plus change the equation. On interchange-plus, you see the actual interchange rate for every transaction, plus a fixed markup. If your processor passes Level 3 data and your transaction qualifies at a lower tier, you pay less. The incentives align: your processor benefits from helping you qualify, not from hiding the details.

BAMS structures its merchant accounts on interchange-plus pricing with this exact philosophy, giving eCommerce merchants visibility into what they’re actually paying at the interchange level, so optimizations like L3 data capture translate directly into lower costs on their statements.

What Changes If You Start Thinking This Way

If enriched transaction data is the lever, then your payment processing strategy stops being a vendor decision and starts being an operational one. It means your checkout configuration, your gateway settings, and your field-mapping choices all affect your effective processing rate. Every tax field left blank, every freight amount omitted, every missing product code is margin you’re leaving on the table.

It also means the processor comparison conversation changes. The right question isn’t “what’s your rate?” It’s “do you pass Level 3 data for my platform, and can I see the interchange qualification on every transaction?” If your processor can’t answer that clearly, they’re probably profiting from the ambiguity. Opaque billing practices thrive when merchants don’t know what to ask.

With U.S. retail eCommerce hitting $326.7 billion in Q1 2026, the volume flowing through online checkouts is enormous. Small percentage improvements in processing cost, applied across that volume, represent serious money. The merchants who treat transaction data optimization as a core competency will outperform those who treat processing as a fixed cost.

Stop Thinking “Payment Processing.” Start Thinking “Transaction Intelligence.”

The biggest processing savings often come from better transaction data, not tougher rate negotiations.

The old mental model says payment processing is a utility. You plug it in, it works, you pay the bill. The new mental model says every transaction is a data packet, and the completeness of that packet determines what you pay to move money.

Think of it like shipping. You wouldn’t send every package via overnight express when ground delivery works for most orders. But that’s exactly what happens when your processor submits bare-minimum transaction data: every sale gets routed to the most expensive interchange tier by default. Mapping your tax and freight fields is the equivalent of choosing the right shipping method for each package. Same destination, dramatically different cost.

The Margin Is Already There

You don’t need to raise prices. You don’t need to cut headcount. You don’t need a new product line. The margin improvement from proper L3 data capture is already built into how the card networks price interchange. It’s been there the whole time. The only question is whether your payment stack is configured to claim it, or whether you’re subsidizing someone else’s spread.

Frequently Asked Questions

How does optimizing transaction data affect processing fees?

When your processor submits enriched data (tax amounts, freight charges, line-item detail) with each transaction, card networks like Visa and Mastercard qualify that transaction at a lower interchange tier. This can reduce your per-transaction cost by 0.50% to 1.00% on qualifying volume, directly improving your effective processing rate.

Why is interchange-plus pricing more beneficial than flat-rate pricing?

Interchange-plus shows you the actual network cost for each transaction plus a fixed markup, so any data optimization savings flow directly to you. Flat-rate pricing bundles everything into one number, meaning your processor keeps the savings when transactions qualify at lower tiers.

What are the best strategies to reduce payment processing fees?

Start by switching to interchange-plus pricing so you can see what you’re actually paying. Then ensure your gateway is mapping Level 2 and Level 3 fields (tax, freight, product codes) from your eCommerce platform to your processor, and audit your statements monthly to verify transactions are qualifying at the correct interchange tiers.

Sources