7 Cash Flow Challenges Ecommerce Brands Can’t Ignore

Why deposit timing gaps — not slow sales — quietly strangle growing online stores

Discover the liquidity pressure points unique to eCommerce operators, from payment processor holds to restock timing gaps. Learn how deposit delays create cash flow challenges that generic forecasting advice completely misses.

TL;DR

- Deposit timing, not revenue, drives eCommerce cash flow problems – The two-to-five-day gap between when you earn money and when it hits your bank account is the root cause of most liquidity crunches for online sellers.

- Forecast from deposit dates, not order dates – Rebuild your cash flow model using actual bank settlement data instead of platform revenue dashboards to avoid overstating available cash.

- Shortening your funding cycle is the fastest liquidity lever – Switching from three-day to next-day funding frees up trapped working capital equal to two days of revenue, without cutting costs or increasing sales.

- Model promotions and peak season as liquidity events – Flash sales and Q4 ramp-ups create cash gaps because outflows (inventory, ads, fulfillment) spike before deposit inflows catch up. Plan for the timing gap, not just the revenue target.

- Start with three changes – Map your real deposit timeline, create a “spendable cash” metric, and calculate your trapped working capital. These take less than a week and improve every cash decision immediately.

The Real Cash Flow Challenges in eCommerce Aren’t About Slow Sales

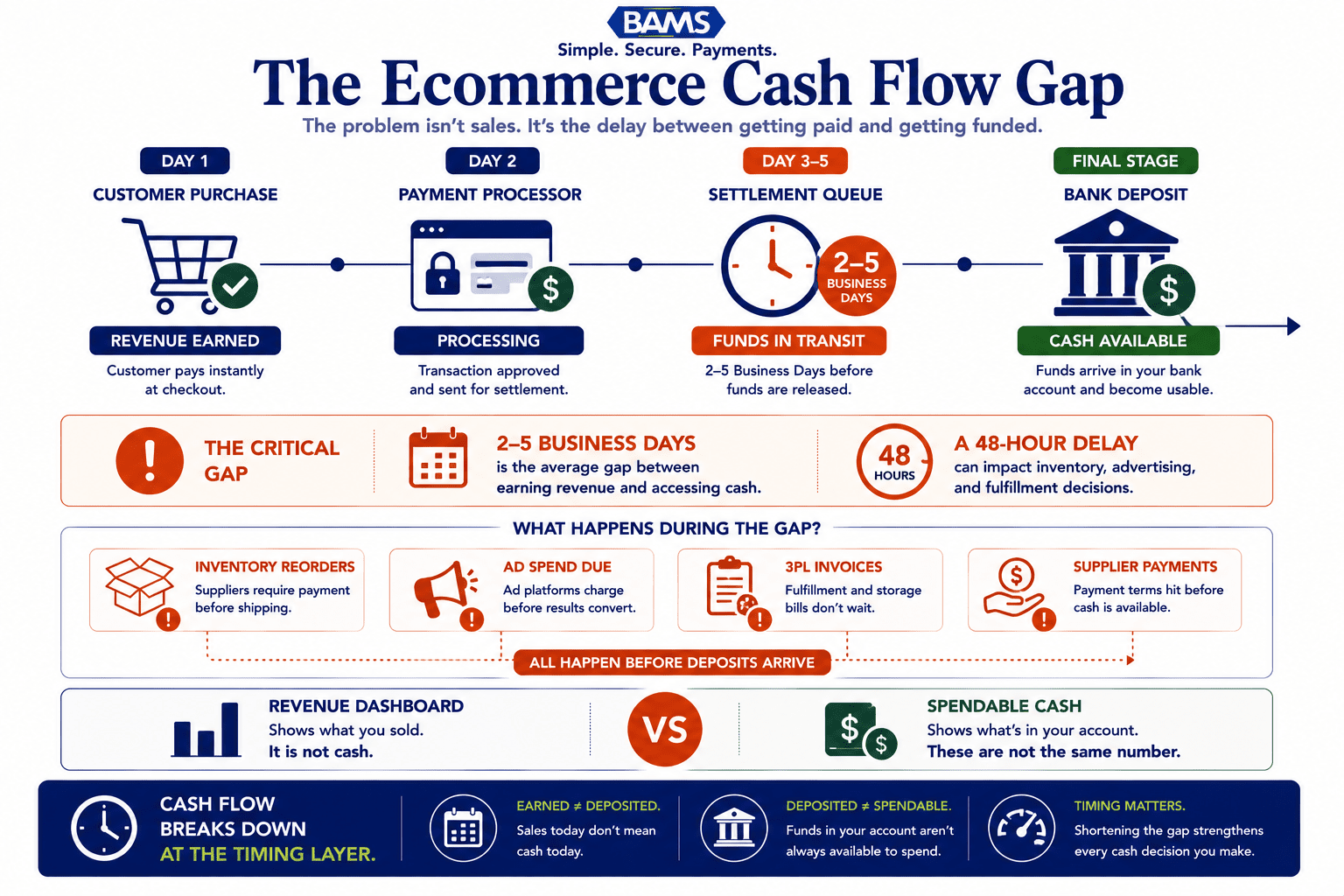

Your store had a record Tuesday. Orders flooded in, margins held, and your ad spend converted at twice the benchmark. By Friday, you need to restock your top SKU and pay your 3PL invoice. But the cash from Tuesday’s sales? It’s still sitting in a processing queue somewhere between your payment gateway and your bank account.

This is the liquidity problem that quietly strangles growing eCommerce brands. Federal Reserve Small Business Survey data continues to show that cash flow management and operational liquidity remain among the top concerns for growing businesses. For online sellers, the root cause is often the lag between earning revenue and being able to spend it.

Most cash flow forecasting advice assumes you’re chasing invoices or negotiating payment terms with clients. That’s a B2B problem. Ecommerce operators face a different beast: you collect payment instantly from customers, but your processor holds those funds for two to five business days. The gap between “sold” and “funded” is where cash flow forecasts break down.

Revenue is earned immediately. Cash arrives days later. That gap drives most ecommerce liquidity problems.

What This Guide Covers (and What It Doesn’t)

This guide is for eCommerce managers at established online businesses who already have revenue flowing but struggle to forecast available cash accurately. If you’re running a store doing $500K or more annually and your forecasting model treats “revenue” and “cash in bank” as the same thing, these tactics are for you.

We’re not covering basic budgeting, invoice management, or B2B receivables optimization. Instead, we focus on the operational pressure points unique to eCommerce: deposit timing, inventory purchasing cycles, promotional surges, and the compounding effect of processing delays on working capital. Every item below addresses a specific gap between when you earn money and when you can deploy it.

How We Selected These Strategies

Each item was evaluated on three criteria: does it address a timing-specific liquidity problem (not a general expense problem)? Can it be implemented within existing eCommerce infrastructure? And does it produce measurable improvement in short-term cash buffer availability within 30 days? Items that only apply to brick-and-mortar or B2B invoice cycles were excluded.

7 Ways to Improve Liquidity When You Get Paid Daily

1. Map Your Actual Deposit Timeline, Not Your Revenue Timeline

Why it matters: Most eCommerce forecasts treat the sale date as the cash date. They’re not the same. If your processor batches at midnight and funds in two business days, a Thursday sale doesn’t land until Monday. A Friday sale might not arrive until Tuesday or Wednesday. This misalignment compounds during high-volume periods and creates phantom cash in your forecast.

What it looks like today: Processors vary widely. Standard merchant account holds range from two to five business days. Some processors offer next-day or same-day funding, which compresses the gap but doesn’t eliminate it entirely. Your forecast needs to reflect your actual funding schedule, not an average.

How to apply it: Pull 60 days of bank deposit data and match each deposit to its corresponding batch date. Calculate your real average funding delay. Then rebuild your cash flow forecast to project available cash based on deposit dates, not order dates. If your cash flow forecast is overstating available cash, this is almost always the reason.

2. Shorten Your Cash Conversion Cycle at the Processor Level

Why it matters: FedNow Service resources continue to demonstrate how faster payment infrastructure and accelerated settlement can improve liquidity access and working capital efficiency for businesses.For eCommerce, the fastest lever isn’t negotiating supplier terms or chasing receivables. It’s reducing the time between customer payment and bank deposit. A shift from three-day funding to next-day funding effectively frees up two days of revenue at any given time.

What it looks like today: Many eCommerce brands accept their processor’s default funding schedule without questioning it. Meanwhile, processors like BAMS offer next-day funding with a 9 PM EST cutoff, which means sales processed by evening hit your account the following business day. That’s a structural improvement to your cash position, not a one-time fix.

How to apply it: Calculate your average daily revenue. Multiply it by the number of days your current processor holds funds. That number is your trapped working capital. Compare it against next-day funding options and weigh the difference against any fee changes. For most brands doing $1M or more annually, the freed capital outweighs incremental costs significantly.

3. Build a Flash Sale Liquidity Model Before You Launch the Promotion

Why it matters: Flash sales and promotional surges create a paradox: revenue spikes, but so do immediate costs. You need to restock faster, your ad spend scales up, and your fulfillment partner invoices sooner. If your deposit timeline doesn’t match the speed of those outflows, a successful sale can actually create a short-term cash crisis.

What it looks like today: Most brands plan promotions around revenue targets and inventory levels. Very few model the cash flow timing of a promotion, specifically when the revenue from the surge will actually be depositable versus when the associated costs come due.

How to apply it: Before any promotion, build a simple three-column model: expected daily revenue (by deposit date, not order date), expected daily outflows (ad spend, fulfillment, restock deposits), and net daily cash position. If the net position goes negative on any day, you need either a short-term cash buffer or a faster deposit schedule to cover the gap. Run this model for every promotion over $10K in projected revenue.

4. Separate “Spendable Cash” from “Booked Revenue” in Your Dashboard

Why it matters: Ecommerce platforms report gross revenue in real time. Your bank account tells a different story. The gap between these two numbers is where poor purchasing decisions, missed supplier discounts, and unnecessary credit line draws originate. As one CFO at a multichannel consumer brand put it: “The business can be profitable on paper and still run out of cash if inventory buys, ad spend, and processor payouts are out of sync.”

What it looks like today:46% of small businesses report insufficient cash reserves to cover three months of expenses. For eCommerce brands, the problem often isn’t low reserves. It’s that managers make spending decisions based on Shopify or Amazon dashboards showing revenue that hasn’t settled yet.

How to apply it: Create a daily “spendable cash” metric that equals your bank balance plus confirmed pending deposits (based on your mapped deposit timeline from item 1) minus committed outflows for the next 72 hours. Use this number for all purchasing and ad budget decisions, not your platform’s revenue figure.

5. Align Inventory Reorder Points with Deposit Cycles, Not Sales Velocity Alone

Why it matters: Inventory as one of the two largest cash traps for retailers. Ecommerce brands typically set reorder points based on sales velocity and lead times. But if your reorder trigger fires on a Monday and your supplier requires a deposit by Wednesday, you need to know whether Monday and Tuesday’s deposits will actually clear in time.

What it looks like today: Inventory management tools (Cin7, TradeGecko successors, NetSuite) calculate reorder points based on demand forecasting. Almost none factor in your actual deposit schedule or available cash position at the time a reorder is triggered. This creates a blind spot that forces reactive scrambling.

How to apply it: Add a cash availability check to your reorder workflow. When your system flags a reorder, cross-reference it against your spendable cash projection for the next five business days. If the cash won’t be available in time, you have three options: negotiate extended supplier payment terms, shift to a processor with faster funding, or adjust your reorder point to trigger earlier when cash is available.

6. Forecast Peak Season as a Liquidity Event, Not Just a Revenue Event

Why it matters: Peak season (Q4 for most eCommerce brands) requires front-loaded spending: inventory pre-buys, increased ad budgets, seasonal staffing, and higher fulfillment costs. Revenue comes later, and even then, deposit delays mean the cash arrives days after the sales. Brands that forecast peak season only by revenue projections often find themselves cash-constrained during their most profitable period.

What it looks like today: Experienced operators pre-buy inventory 60 to 90 days before peak. But many don’t model the cash flow gap between those pre-buys and when peak-season deposits actually start landing. The result is reliance on credit lines or, worse, throttling ad spend during the highest-ROI window of the year.

How to apply it: Start your peak season cash flow model 90 days before the season begins. Plot every known outflow (inventory deposits, ad budget ramp, seasonal labor) against projected deposit inflows on their actual settlement dates. Identify the week where the gap between outflows and available cash is widest. That’s your maximum liquidity exposure. Secure your short-term cash buffer (credit line, faster funding terms, or retained cash reserve) to cover that specific window.

7. Treat Processing Fees as a Variable Cost in Your Cash Flow Model

Why it matters: Processing fees reduce the amount that actually deposits into your account, but many forecasts use gross revenue figures without deducting them. At a 2.5% to 3.5% effective rate, a brand doing $100K per month is losing $2,500 to $3,500 in cash that never arrives. During high-volume months, this gap widens and can throw off your cash projections by thousands of dollars.

What it looks like today: Interchange-plus pricing models make fees somewhat predictable, but card mix (credit vs. debit, rewards cards, international cards) causes variation. Flat-rate processors simplify the math but often charge more overall. Neither model is inherently better for forecasting. What matters is that you model net deposits, not gross.

How to apply it: Pull your last six months of processing statements and calculate your effective rate by month. Use the average as your baseline deduction in cash flow projections. If your rate varies by more than 0.3% month to month, investigate whether a transparent interchange-plus processor like BAMS would reduce both the cost and the variability, making your forecast more reliable. Also review invoicing tools that accelerate collection for any B2B or wholesale segments of your business.

The Pattern Across All Seven Strategies

The fastest way to improve liquidity isn’t always increasing sales. It’s reducing the delay between revenue and cash.

Every item on this list addresses the same underlying problem: eCommerce cash flow breaks down at the timing layer, not the revenue layer. Your business can be growing, profitable, and operationally sound while still running into liquidity walls because your cash arrives two to five days after you need it.

The shared theme is that improving liquidity for eCommerce doesn’t require cutting costs or increasing sales. It requires compressing the gap between earning and accessing your money, then building forecasts that reflect reality instead of platform dashboards. Faster deposits, better timing models, and net-cash thinking form an integrated system. Each reinforces the others. A faster deposit schedule makes your flash sale model more resilient. A net-deposit forecast makes your reorder workflow smarter. A spendable cash metric keeps your team from making decisions based on numbers that don’t exist in your bank account yet.

Where to Start (Without Overhauling Everything)

You don’t need to implement all seven at once. Start with three: map your actual deposit timeline (item 1), create a spendable cash metric (item 4), and calculate your trapped working capital (item 2). These three changes take less than a week and immediately improve the accuracy of every cash flow decision you make.

If your trapped capital number is significant, evaluate whether switching to a guaranteed next-day funding processor changes your operational flexibility. For most established eCommerce brands, this single infrastructure change has a larger impact on daily cash flow than any budgeting tactic or cost-cutting measure. Prioritize the timing layer first. The rest follows.

Frequently Asked Questions

What is a cash flow acceleration strategy for eCommerce?

A cash flow acceleration strategy focuses on reducing the time between when you earn revenue and when that cash is available to spend. For eCommerce, this primarily means shortening deposit timelines from your payment processor, aligning purchasing decisions with actual bank balances instead of reported revenue, and modeling outflows against net deposit dates rather than order dates.

How does next-day funding improve liquidity for online sellers?

Next-day funding compresses the gap between a customer’s purchase and when the funds hit your bank account. If your current processor holds funds for three to five days, switching to next-day funding frees up two to four days of revenue at any given time. For a brand doing $10K per day, that’s $20K to $40K in additional working capital available without borrowing.

Why do eCommerce cash flow forecasts overstate available cash?

Most forecasts use order dates or gross revenue figures from platforms like Shopify or Amazon. These numbers don’t account for processor deposit delays (typically two to five business days) or processing fee deductions. The result is a forecast that shows cash you technically earned but can’t actually access yet, leading to overspending or missed payment obligations.

How can businesses improve cash flow forecasting with real-time data?

Start by matching bank deposit records to batch processing dates to calculate your true funding delay. Then build a daily “spendable cash” metric: bank balance plus confirmed pending deposits minus committed outflows for the next 72 hours. This real-time view replaces the lagging, inaccurate picture that platform dashboards provide.

When should eCommerce brands build a short-term cash buffer?

Build a short-term cash buffer before any period where outflows will spike ahead of revenue: promotional events, inventory pre-buys for peak season, or major ad spend increases. Model the specific week where the gap between outflows and available deposits is widest, and size your buffer to cover that window. A general rule is to hold enough to cover five to seven days of operating expenses beyond your committed reserves.

Which payment solutions help reduce processing fees and improve forecasting?

Interchange-plus pricing models offer more transparency and predictability than flat-rate processors, which simplifies forecasting. Look for processors that provide detailed monthly statements breaking down your effective rate by card type. Consistent, transparent pricing reduces the variability in your net deposit projections, making your cash flow model more reliable month to month.