5 Payment Gateways for Small Business Cash Flow

Fast deposits, predictable fees, and built-in support for digital wallets and recurring billing

Discover which payment gateways actually speed up fund access for growing eCommerce businesses. We compare features that matter: deposit timing, fee transparency, and modern payment support.

TL;DR

- Funding speed matters as much as fees – Standard 3-5 day deposit windows lock up working capital. Prioritize gateways offering next-day funding if cash flow timing creates operational stress.

- Digital wallet support is now expected – Apple Pay and Google Pay reduce checkout friction. Ensure your gateway supports these natively rather than through workarounds.

- Platform-native gateways save money – Shopify Payments eliminates additional transaction fees for Shopify merchants. Using third-party gateways on integrated platforms often means paying double fees.

- Recurring billing needs specialized features – If subscriptions exceed 20% of revenue, prioritize gateways with automatic card updaters, smart retry logic, and dunning management.

- Evaluate total cost, not just transaction rates – Factor in deposit timing, integration complexity, support quality, and fraud prevention when comparing gateways. The lowest per-transaction fee rarely delivers the lowest total cost.

The Deposit Delay Problem Draining Your eCommerce Cash Flow

Your customers click “buy” on Monday. The payment processes Tuesday. The funds clear… sometime next week. Maybe. For eCommerce managers running established online businesses, this timeline creates a cash flow gap that ripples through every operational decision.

The challenge intensifies as your business scales. Many businesses still operate on payment systems designed for a slower era, watching funds sit in limbo while inventory needs restocking and payroll deadlines approach.

Finding the right payment gateway for small businesses means looking beyond basic transaction processing. You need infrastructure that matches your operational tempo: faster fund access, predictable fees, and support for how customers actually want to pay in 2025.

What This List Delivers (And What It Doesn’t)

This guide targets eCommerce managers at businesses with 10-50 employees who need to solve specific problems: delayed deposits eating into working capital, transaction fees that fluctuate unpredictably, and payment systems that can’t keep pace with customer expectations for digital wallet payments and recurring billing solutions.

You won’t find every payment processor on the market here. We’ve excluded enterprise-only solutions requiring dedicated integration teams, processors with opaque pricing structures, and platforms lacking robust digital payment capabilities. Each gateway earned its place by demonstrating clear value for established eCommerce operations prioritizing cash flow velocity and operational efficiency.

How We Evaluated These Payment Gateways

Comparing payment gateways side by side reveals how funding speed, pricing structure, and features directly impact small business cash flow.

Selection criteria prioritized three factors: funding speed (how quickly you access your money), fee transparency (predictable costs without hidden charges), and modern payment support (digital wallets, recurring billing, multi-currency capabilities). We weighted practical implementation requirements alongside feature sets, recognizing that the best gateway is one your team can actually deploy and manage.

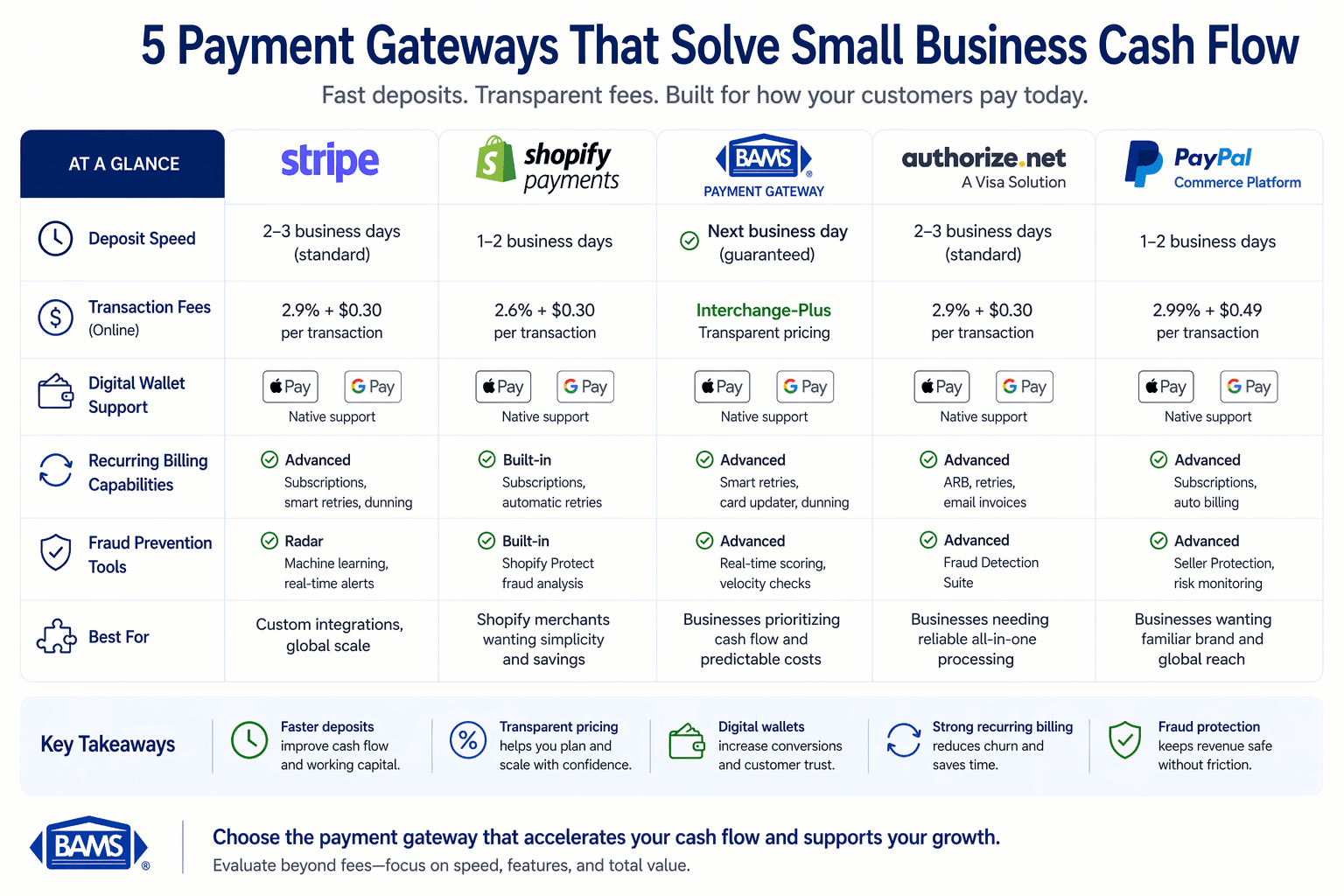

Top Five Payment Gateways That Empower Small Businesses to Thrive

1. Stripe: The Integration-First Platform for Scaling Operations

Why it matters: eCommerce managers often inherit payment systems that work “well enough” until they don’t. Stripe addresses the scaling problem directly, offering infrastructure that grows without requiring platform migrations or painful reconfigurations.

What it looks like today: Modern payment infrastructure continues to evolve. According to Visa, optimized payment systems are designed to process transactions securely while maintaining speed and efficiency. The platform supports all major cards, Apple Pay, Google Pay, and processes international payments in 135 currencies. Its API-first approach means your development team can customize checkout flows without vendor lock-in.

How to apply it: Stripe works best for businesses with some technical capacity or access to developers. If your eCommerce platform already offers Stripe integration (most do), implementation requires minimal custom work. Evaluate whether your international sales volume justifies the multi-currency capabilities, as domestic-only businesses may find simpler alternatives sufficient.

2. Square: Mobile-Ready Processing With Predictable Economics

Why it matters: Many eCommerce businesses also operate physical touchpoints: pop-up shops, trade shows, or local pickup options. Square bridges the gap between online and in-person sales without requiring separate payment systems.

What it looks like today:Square charges 2.6% + $0.10 per card-present transaction and up to 3.5% + $0.15 for card-not-present transactions. The platform handles PCI compliance automatically and includes fraud detection tools. Vendors at farmers’ markets and food trucks rely on Square’s integrated gateway and mobile terminals for exactly this reason.

How to apply it: Square delivers maximum value when you need unified reporting across sales channels. The flat-rate pricing simplifies forecasting, though high-volume businesses may find interchange-plus models more economical. Start with Square’s free tier to test integration with your existing eCommerce platform before committing to hardware purchases.

3. Shopify Payments: Native Integration for Shopify Merchants

Why it matters: Third-party payment gateways on Shopify incur additional transaction fees on top of processor charges. Shopify Payments eliminates this friction for merchants already invested in the Shopify ecosystem.

What it looks like today:Shopify Payments charges 2.9% + $0.30 per U.S. transaction with no additional gateway fees for Shopify users. Payouts arrive in 2-3 business days, faster than many competitors’ standard timelines. The platform supports Shop Pay, Apple Pay, Google Pay, and major credit cards natively.

How to apply it: This gateway makes sense only if you’re already on Shopify or planning to migrate. The economics favor Shopify merchants specifically since using external gateways means paying both processor fees and Shopify’s transaction percentage. If you’re evaluating platforms, factor this into total cost of ownership calculations.

According to the Federal Reserve, interchange structures play a major role in total payment processing costs, making transparency critical when evaluating providers.

4. Merchant Service Partners With Next-Day Funding

Why it matters: Standard 3-5 day deposit windows create operational drag. For businesses managing tight inventory cycles or variable demand, waiting nearly a week to access revenue means missed opportunities and unnecessary credit line usage.

What it looks like today: Dedicated merchant services partners now offer guaranteed next-day funding as a standard feature rather than a premium add-on. These providers typically combine faster fund access with interchange-plus pricing, where you pay actual card network costs plus a fixed markup rather than flat rates that obscure true processing costs.

How to apply it: Next-day funding matters most when your cash conversion cycle is tight. Calculate your average daily sales and multiply by your current deposit delay. That number represents working capital locked in transit. If that figure exceeds your comfort threshold, prioritize funding speed in your gateway evaluation. Consider whether your current processor’s fund access timeline actually serves your operational needs.

5. Gateways With Built-In Recurring Billing Solutions

Why it matters: Subscription revenue provides predictable cash flow, but only if your payment infrastructure handles recurring billing gracefully. Failed payments, expired cards, and manual retry processes erode the efficiency gains subscriptions promise.

What it looks like today: Modern recurring billing solutions include automatic card updater services, smart retry logic for failed payments, and customer self-service portals for payment method management.

How to apply it: If recurring revenue exceeds 20% of your total sales, prioritize gateways with native subscription management. Evaluate dunning capabilities (how the system handles failed payments) and churn reduction features. The cost of involuntary churn from payment failures often exceeds the premium for better subscription tooling.

Patterns Across These Payment Gateway Options

Three themes emerge from this analysis. First, SMEs prefer reduced security responsibilities over maximum customization. Second, digital wallet payments have shifted from nice-to-have to expected. Customers increasingly prefer Apple Pay and Google Pay over manual card entry.

Third, the real cost of a payment gateway extends beyond transaction fees. Deposit timing affects working capital. Integration complexity affects team capacity. Support quality affects problem resolution speed. The cheapest per-transaction rate rarely delivers the lowest total cost of ownership.

Where to Start: Prioritizing Your Gateway Evaluation

Choosing the right payment gateway starts with understanding your business needs, then evaluating funding speed, costs, features, and support.

Don’t attempt to optimize every payment variable simultaneously. Start with your most pressing constraint. If cash flow timing creates operational stress, prioritize funding speed over feature breadth. If international sales represent growth potential, prioritize multi-currency support.

For most established eCommerce operations, we recommend evaluating no more than three gateways seriously. Request actual pricing based on your transaction volume and average ticket size. Test customer support responsiveness before signing contracts. And verify PCI compliance and fraud prevention capabilities meet your risk tolerance. The PCI Security Standards Council emphasizes that strong security standards are essential to protect transactions while maintaining seamless checkout experiences.

The right payment gateway transforms a cost center into operational infrastructure that actively supports growth. Choose based on your specific constraints, not industry rankings.

Frequently Asked Questions

What is a payment gateway and why is it important for eCommerce?

A payment gateway securely transmits transaction data between your online store, the customer’s bank, and your merchant account. It authorizes payments in real-time, encrypts sensitive card information, and determines whether transactions succeed or fail. For eCommerce operations, the gateway directly impacts checkout conversion rates, fraud exposure, and how quickly you access your revenue.

How do I choose the best payment gateway for my business?

Start by identifying your primary constraint: funding speed, transaction costs, integration requirements, or international capabilities. Request volume-based pricing from 2-3 providers using your actual sales data. Evaluate support responsiveness, test the checkout experience from a customer perspective, and verify compatibility with your eCommerce platform before committing.

When should I consider switching my payment gateway?

Consider switching when deposit delays create cash flow problems, when fees have increased without corresponding service improvements, when your current gateway lacks support for digital wallets or recurring billing, or when customer complaints about checkout friction increase. The switching cost is typically lower than businesses assume, especially with hosted gateway solutions.

Which payment gateways support international transactions?

Stripe supports 135 currencies and is often the default choice for international eCommerce. PayPal offers broad international acceptance with localized checkout experiences. Evaluate currency conversion fees carefully, as these can significantly impact margins on cross-border sales. Some gateways offer multi-currency merchant accounts that reduce conversion costs.

How do payment gateways ensure the security of online transactions?

Reputable gateways maintain PCI DSS compliance, encrypt transaction data during transmission, and offer fraud detection tools including address verification (AVS), card verification codes (CVV), and velocity checks. Hosted gateways reduce your PCI compliance burden by handling card data on their secure servers rather than yours.

What’s the difference between flat-rate and interchange-plus pricing?

Flat-rate pricing (like Square’s 2.6% + $0.10) charges the same percentage regardless of card type. Interchange-plus pricing passes through actual card network costs plus a fixed markup. Flat-rate simplifies forecasting but typically costs more at higher volumes. Interchange-plus offers transparency and usually lower costs for established businesses processing over $10,000 monthly.