7 Payment Strategies to Reduce Cart Abandonment

How expanding payment options and digital wallets keeps customers at checkout instead of clicking away

Learn proven strategies to reduce cart abandonment by expanding your payment options. This guide covers digital wallet integration, B2B payment terms, and balancing customer preferences with processing costs.

TL;DR

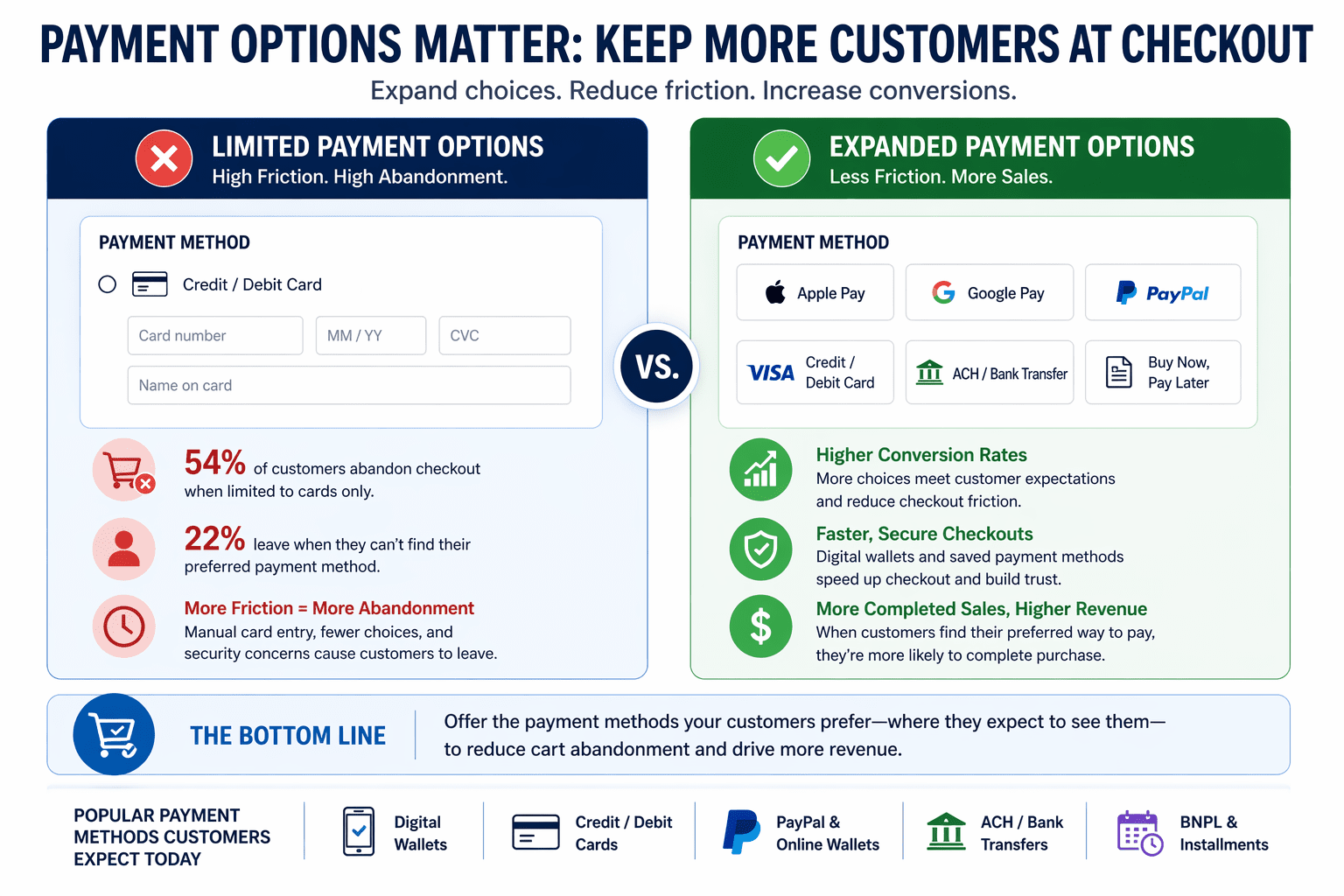

- Digital wallets are now baseline expectations – 54% of customers abandon checkout when limited to cards only, and 22% leave when they cannot find their preferred payment method

- Payment option placement matters as much as availability – Display express checkout buttons above the fold so customers see their preferred method before abandonment impulses kick in

- B2B requires different payment strategies – Over 48% of B2B buyers abandon due to insufficient options, with half preferring ACH or net-terms over credit cards

- Authorization rate optimization recovers hidden revenue – The difference between 90% and 95% authorization represents significant sales you are currently losing to technical failures

- Start with one or two strategies this quarter – Match payment expansion to your actual customer base, measure results, then expand incrementally rather than implementing everything at once

Why Payment Limitations Cost You Sales in 2025

Offering more payment options reduces checkout friction and significantly improves conversion rates compared to limited payment methods.

Offering more payment options reduces checkout friction and significantly improves conversion rates compared to limited payment methods.

Your checkout page is bleeding revenue. Not from poor product descriptions or weak calls-to-action, but from something far more fixable: the payment options you offer.

eCommerce managers at established businesses face a frustrating paradox. You have invested in acquisition, optimized product pages, and built trust with customers.The math is brutal: more than half your potential conversions disappear at the final step.

The landscape has shifted. Digital wallet payments now represent a baseline expectation, not a competitive advantage. Customers who grew up with Apple Pay and Google Pay view manual card entry as friction. B2B buyers increasingly demand net-terms and ACH options. Your payment stack either meets these expectations or watches customers leave.

Modern payment behavior continues to shift toward faster, frictionless checkout experiences, as improvements in payment infrastructure and digital acceptance expand across eCommerce according to Modern Treasury

This guide moves beyond surface-level advice about adding a PayPal button. We examine the strategic approaches that reduce cart abandonment through payment option expansion, addressing the specific challenges eCommerce managers face when balancing customer preferences against processing costs and operational complexity.

What This Guide Delivers

This listicle targets eCommerce managers at businesses with 10-50 employees who need actionable strategies, not theoretical frameworks. You already understand that cart abandonment matters. You need specific approaches that work within real-world constraints: limited development resources, existing payment processor relationships, and the need to maintain profitability.

We exclude enterprise-only solutions requiring dedicated payment teams. We skip the obvious suggestions you have already implemented. Instead, each strategy addresses the specific moment when payment friction causes abandonment, with clear implementation paths and measurable outcomes.

The value proposition is direct: reduce cart abandonment by expanding payment options strategically, without adding operational complexity that erodes your margins.

How We Selected These Strategies

Each strategy meets three criteria. First, it addresses documented abandonment causes backed by research data. Second, it can be implemented by mid-size eCommerce teams without enterprise resources. Third, it delivers measurable impact on conversion rates within 90 days of implementation.

We prioritized approaches that balance customer convenience against processing costs, recognizing that payment option expansion only works when it improves your bottom line, not just your conversion metrics.

Seven Strategies to Reduce Cart Abandonment Through Payment Expansion

Seven proven payment strategies that help eCommerce businesses reduce cart abandonment, improve conversions, and increase revenue.

1. Prioritize Digital Wallet Integration

Why it matters: Digital wallets use tokenization and secure authentication to reduce friction and improve transaction success rates, as outlined by Visa. Digital wallets eliminate the friction of manual card entry, address security concerns through tokenization, and reduce checkout time from minutes to seconds.

What it looks like today: Apple Pay, Google Pay, and Shop Pay have moved from nice-to-have features to expected options. Mobile commerce now exceeds 60% of eCommerce traffic, and customers on phones expect one-tap checkout experiences. The days of typing 16-digit card numbers on mobile keyboards are ending.

How to apply it: Start with Apple Pay and Google Pay, which cover the largest user bases. Ensure your payment gateway supports both. Test the mobile checkout flow yourself, measuring time-to-completion before and after implementation. Track conversion rate changes by device type for 30 days post-launch.

2. Implement Buy Now, Pay Later Options

Why it matters: BNPL addresses a specific abandonment trigger: customers who want your product but face cash flow timing issues. This is not about customers who cannot afford your products. It is about customers who prefer to spread payments across paychecks.

What it looks like today: Klarna, Afterpay, and Affirm have normalized installment payments for purchases as small as $50. Live Sell Academy research shows that advertising BNPL options in marketing emails increases conversion rates by giving customers permission to buy now rather than waiting.

How to apply it: Choose a BNPL provider whose fee structure works with your margins. Display BNPL messaging on product pages, not just at checkout. This plants the seed earlier in the purchase journey. Monitor average order value changes, as BNPL typically increases AOV by 20-30%.

3. Add Express Checkout Buttons Above the Fold

Why it matters: Checkout page design determines whether customers see their preferred payment option before abandonment impulses kick in. Placement matters as much as availability.

What it looks like today: Leading eCommerce sites display PayPal, Apple Pay, and Google Pay buttons prominently at the top of checkout, before the traditional card entry form. This signals to customers that their preferred method is available before they start the mental calculation of whether to proceed.

How to apply it: Audit your checkout page. If customers must scroll to see digital wallet options, you are losing conversions. Implement express checkout buttons above the fold on both desktop and mobile. A/B test button order to determine which placement drives highest completion rates for your specific audience.

4. Expand B2B Payment Options Beyond Credit Cards

Why it matters: If you sell to businesses, credit card limitations hit harder. ACH and account-to-account payments continue to grow as businesses seek lower-cost and more efficient alternatives to card payments, supported by data from NACHA.

What it looks like today: B2B eCommerce has adopted consumer-style checkout experiences while ignoring B2B payment preferences. Businesses expect invoicing options, net-30 terms, and ACH transfers. Forcing credit card payment creates friction and often violates corporate purchasing policies.

How to apply it: If B2B represents significant revenue, add ACH payment options and explore net-terms solutions. Work with your merchant services provider to understand cost differences between payment methods. ACH typically costs less than credit card processing, improving your margins while meeting customer preferences.

5. Streamline Payment Security Without Adding Friction

Why it matters: Security concerns drive abandonment, but excessive security measures create their own friction. The goal is visible security that builds trust without adding steps. Customers want to know their payment information is safe, but they do not want to jump through hoops to prove their identity.

What it looks like today: Digital wallets inherently provide security through biometric authentication and tokenization. eCommerce chargeback defense solutions now relies on behind-the-scenes verification rather than customer-facing challenges. The best security is invisible to legitimate customers.

How to apply it: Display security badges and SSL indicators prominently. Ensure your payment processor handles fraud detection without adding customer-facing friction. Review your 3D Secure settings to balance fraud protection against false declines. Track authorization rate improvement as you optimize security settings.

6. Optimize for Authorization Rate Improvement

Why it matters: Payment option expansion means nothing if transactions fail at the authorization stage. Declined transactions create abandonment even when customers have valid payment methods. Authorization failures often stem from technical issues, not customer problems.

What it looks like today: Modern payment processors offer retry logic, network tokenization, and intelligent routing to maximize authorization rates. The difference between a 90% and 95% authorization rate represents significant revenue recovery.

How to apply it: Review your authorization rate data with your payment processor. Ask about automatic retry capabilities for soft declines. Ensure your processor supports network tokenization, which improves authorization rates for returning customers. Set a baseline and track improvement monthly.

7. Implement Faster Deposit Strategies

Why it matters: This strategy addresses the merchant side of payment optimization. Delayed deposits create cash flow gaps that limit your ability to invest in inventory, marketing, and growth. Next-day funding transforms payment processing from a cash flow obstacle into a predictable advantage.

What it looks like today: Traditional 3-5 day deposit windows are no longer the only option. Next-day funding has become available to mid-size merchants without enterprise volume requirements. This shift allows eCommerce managers to operate with smaller cash reserves and respond faster to opportunities.

How to apply it: Evaluate your current deposit timeline and calculate the working capital impact. Compare processor options that offer next-day funding. Factor deposit speed into your total cost of payment processing, not just transaction fees. Faster access to funds often justifies slightly higher per-transaction costs.

The Pattern Behind These Strategies

These seven approaches share a common thread: they reduce friction at the moment of payment decision. Whether expanding digital wallet payments, adding BNPL options, or improving authorization rates, each strategy removes a specific barrier between customer intent and completed purchase.

The tradeoff across all strategies involves balancing customer convenience against operational complexity and processing costs. Adding payment options increases conversion rates but adds reconciliation work and potentially higher fees. The winning approach identifies which payment methods your specific customers prefer and prioritizes those, rather than implementing every option available.

Second-order effects matter here. Faster deposits improve cash flow, which enables inventory investments, which reduces stockouts, which prevents a different type of abandonment. Payment security improvements reduce chargebacks, which protects your processor relationship, which maintains access to competitive rates.

Where to Start

You cannot implement all seven strategies simultaneously without overwhelming your team. Start with the highest-impact, lowest-effort options based on your current situation.

If you lack digital wallet integration, begin there. If you already offer Apple Pay and Google Pay, audit your checkout page placement before adding new options.

To support wallets like Apple Pay and Google Pay, your checkout must run on an integrated payment gateway that enables fast, secure, and frictionless transactions.

For B2B-focused businesses, prioritize ACH and net-terms before consumer-focused BNPL. Match your payment expansion strategy to your actual customer base, not generic best practices.

Resource constraints are real. Choose one or two strategies for this quarter, measure results, then expand. Incremental improvement beats ambitious plans that stall in implementation.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies involve working with payment processors that offer next-day or same-day funding instead of traditional 3-5 day settlement windows. This improves cash flow predictability and reduces the working capital you need to maintain. Key factors include processor capabilities, transaction volume, and account history.

Why is payment optimization important for businesses?

Payment optimization directly impacts both revenue and costs. On the revenue side, it reduces cart abandonment by offering preferred payment methods. On the cost side, it improves authorization rates (reducing lost sales from declined transactions) and can lower processing fees through better pricing structures and reduced chargebacks.

How can I improve my payment authorization rates?

Authorization rate improvement comes from several factors: using network tokenization for returning customers, implementing intelligent retry logic for soft declines, ensuring accurate billing information collection, and working with processors that offer dynamic routing. Review your current rates with your processor and ask about specific optimization tools available.

When should I consider expanding my payment options?

Expand payment options when you see abandonment rates above industry benchmarks (typically 70% for eCommerce), when customer feedback mentions payment limitations, or when entering new markets with different payment preferences. Prioritize expansion based on actual customer demand rather than adding every option available.

Which payment processing fees can I reduce to optimize costs?

Focus on interchange optimization through proper transaction categorization, reducing chargebacks through fraud prevention, negotiating processing margins based on volume, and choosing appropriate payment methods for different transaction types. ACH payments typically cost less than credit cards for B2B transactions.

What role does fraud protection play in payment optimization?

Effective fraud protection reduces chargebacks (protecting revenue and processor relationships) while maintaining high authorization rates for legitimate customers. The goal is invisible security that stops fraud without adding friction. Modern solutions use machine learning and behavioral analysis rather than customer-facing challenges.