Understanding Convenience Fees vs Surcharges for eCommerce Success

Rethink fee structures to enhance customer experience and protect trust.

Convenience Fees vs Surcharges in eCommerce: What’s the Difference? Learn how confusing convenience fees with surcharges can harm your business. Discover strategies to manage fees while maintaining customer trust.

TL;DR

- Convenience fees and surcharges serve different purposes – One adds value for a price; the other punishes a payment choice. Customers know the difference.

- Surcharges can cost you more than they save – Merchants using surcharges saw 10% drops in card sales. That’s real revenue walking away.

- The real fix is reducing fees at the source – Better payment processor relationships and transparent pricing beat passing costs to customers.

- Reframe the question – Ask “How do I reduce this cost?” not “How do I recover it?” That shift changes your entire approach to payment strategy.

What Is a Convenience Fee?

A convenience fee is a charge added when a customer chooses an optional payment method or receives an additional service benefit.

What Is a Surcharge?

A surcharge is an added fee for paying with a credit card, typically used to offset processing costs.

The Fee You’re Adding Might Be Costing You More Than You Think

Here’s a pattern I see constantly: an eCommerce manager watches credit card processing fees climb past 2.3%, panics, and slaps a surcharge on every transaction. Problem solved, right?

Except three months later, cart abandonment is up, customer complaints are flooding in, and that “solution” has quietly eroded something harder to rebuild than margin: trust.

The conversation around convenience fee vs surcharge has become muddied. Most businesses treat them as interchangeable tools for the same job. They’re not. And confusing them is costing you customers.

Why Everyone Reached for the Surcharge Button

The logic seemed airtight. Swipe fees hit $187.2 billion in 2024, up 70% since the pandemic. Average Visa and Mastercard fees climbed to 2.35%, squeezing margins that were already thin.

Small businesses watched this happen with limited options. As Andy Ellen, president of the North Carolina Retail Merchants Association, puts it: “There isn’t much room for negotiation, especially for a smaller seller. The interchange fees are pretty much fixed.”

So 34% of U.S. small businesses added credit card surcharges in 2024. The math was simple: pass the cost to customers, protect your margins, move on.

Except the math wasn’t that simple at all.

The Real Difference Isn’t Legal. It’s Psychological.

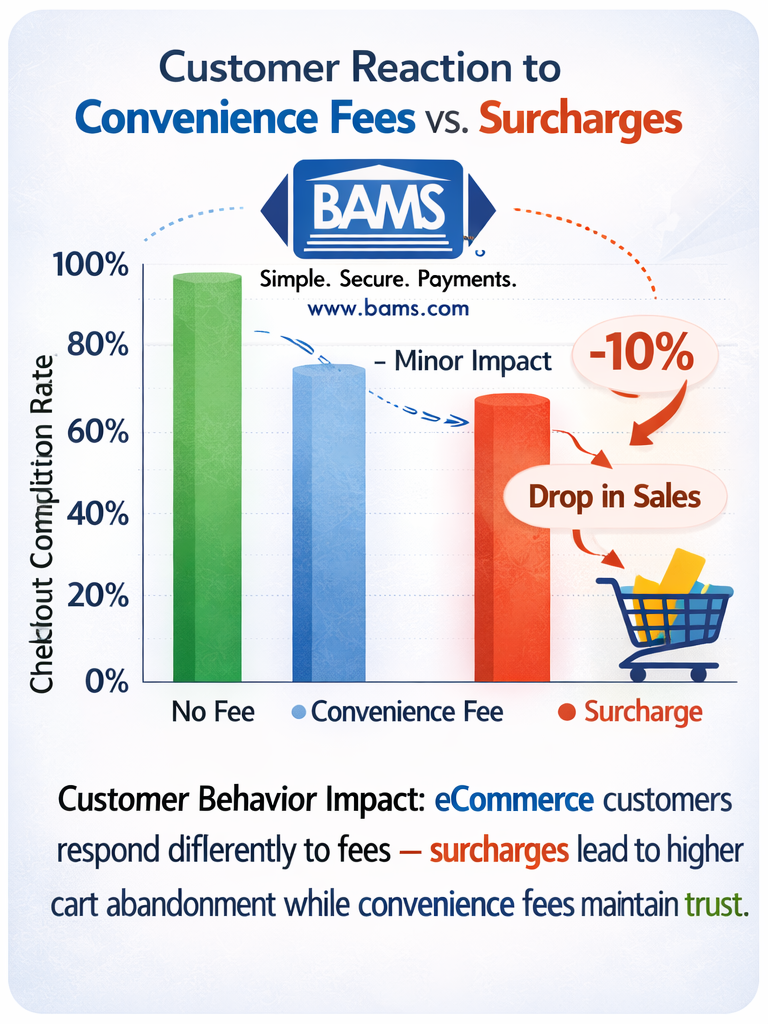

Convenience Fees vs. Surcharges : A visual comparison of how eCommerce customers perceive added value fees versus penalty-based payment surcharges.

Here’s what I actually believe: the distinction between a convenience fee and a surcharge isn’t about compliance. It’s about whether your customer feels punished or empowered.

A surcharge says: “You’re costing me money by paying this way.” A convenience fee says: “I’m offering you something extra, and here’s the cost.”

Same dollars. Completely different relationship.

What the Numbers Actually Tell Us

Let’s look at what happens when businesses treat these fees as identical.

Surcharging merchants saw a 10% drop in same-store debit and credit sales due to changed consumer behavior.

Customer Behavior Impact: eCommerce businesses using credit card surcharges experienced a measurable drop in checkout completion and card sales.

That’s not a rounding error. That’s one in ten transactions walking out the door.

Meanwhile, 69% of cardholders encountered surcharges in 2023. They noticed. They remembered. And many of them started shopping elsewhere.

John Cabell, managing director of payments intelligence at J.D. Power, has tracked this shift: “Merchants increasingly are passing on costs to consumers in a more explicit fashion.” The keyword is “explicit.” Visibility without context creates friction.

When Convenience Fees Actually Work

A convenience fee makes sense when you’re genuinely providing additional value. Think expedited processing, after-hours service, or a payment channel that costs you more to offer but saves your customer time or hassle.

The key question: Would your customer pay this fee even if they understood exactly what they were getting? If yes, you have a convenience fee. If no, you have a surcharge dressed up in better language.

Ecommerce managers often miss this distinction. They add a “convenience fee” for using a credit card online, but there’s nothing convenient about it. It’s just the standard way to pay. Customers see through this immediately.

When Surcharges Make Sense (and When They Don’t)

Surcharges can work in specific contexts. High-ticket B2B transactions where relationships are established. Industries where credit card payments are genuinely optional. Situations where your margins are transparent and your value proposition is strong enough to absorb the friction.

They rarely work in competitive ecommerce. When your customer is three clicks away from a competitor who doesn’t charge extra, that 2-3% fee becomes a conversion killer.

The businesses succeeding with surcharges aren’t just compliant. They’re strategic. They offer clear alternatives, communicate the “why” upfront, and make sure the surcharge never surprises anyone at checkout.

What This Means for Your Business

If surcharges are costing you 10% of transactions, and your average order value is $150, you’re not saving money. You’re hemorrhaging it.

The real opportunity isn’t in passing costs to customers. It’s in reducing credit card processing fees at the source through better payment processor relationships, smarter transaction routing, and pricing structures that actually align with your volume.

Most ecommerce managers don’t realize how much flexibility exists. They accept their current rates as fixed because they’ve never had a partner show them otherwise.

This is where transparency matters. A payment processor that shows you exactly where your fees go (interchange, assessment, markup) gives you leverage. One that bundles everything into a single rate is betting you won’t ask questions.

A Better Way to Think About Payment Costs

Stop thinking about fees as something to recover. Start thinking about them as a cost of conversion.

Your payment processor isn’t just a vendor. It’s infrastructure. The right partner reduces your effective rate, gets cash in your account faster, and handles disputes before they become chargebacks. The wrong one costs you in ways that never show up on a statement.

The question isn’t “How do I pass this cost to my customer?” It’s “How do I reduce this cost while improving my customer’s experience?”

That reframe changes everything. It shifts you from defensive fee recovery to proactive margin optimization.

The Bottom Line

Convenience fees and surcharges are not the same tool. One can strengthen customer relationships when applied correctly. The other almost always weakens them.

Before you add any fee to your checkout, ask: Am I solving my problem or creating my customer’s problem? The answer determines whether you’re building a business or just protecting a margin that’s already slipping away.

Want to reduce credit card processing fees without hurting conversion rates?

BAMS helps eCommerce businesses lower effective rates through transparent pricing and optimized transaction routing.

Frequently Asked Questions

What are credit card processing fees?

Credit card processing fees are charges merchants pay each time a customer uses a card. They typically include interchange fees (paid to the card-issuing bank), assessment fees (paid to card networks), and processor markup.

How can businesses minimize their credit card processing fees?

Start by understanding your current rate breakdown and negotiating with your payment processor. Consider transaction routing optimization, encouraging lower-cost payment methods, and partnering with processors who offer transparent, volume-based pricing.

Which types of transactions incur higher processing fees?

Card-not-present transactions (online purchases), rewards cards, and corporate cards typically carry higher interchange rates. Debit cards and transactions with PIN verification generally cost less to process.

Sources

- https://merchantspaymentscoalition.com/credit-card-swipe-fees-could-cost-consumers-20-billion-or-more-during-2025-holiday-season

- https://www.paymentsdive.com/news/third-of-us-small-businesses-add-credit-card-surcharges/739018/

- https://thefinancialbrand.com/news/payments-trends/credit-card-surcharges-cut-volume-but-love-for-rewards-is-strong-181562