Checkout Transparency Chargebacks: Reduce Upsell Risk

How Transparent Checkout Upsells Reduce Chargebacks

A practical guide to implementing order bumps that boost revenue without triggering disputes

Learn how to structure checkout upsells that customers trust and rarely dispute. This guide covers pricing transparency tactics that protect revenue while adding incremental sales through order bumps.

TL;DR

- Chargebacks are surging – Global disputes projected to hit 337 million by 2026, with eCommerce rates up 222% since 2023. Unclear upsells are a primary driver.

- Friendly fraud dominates – 75% of chargebacks come from customers who forgot or misunderstood purchases, not criminals. Transparency eliminates the “I did not know” defense.

- Prevention beats representation – Merchants win only 45% of disputed chargebacks. Automated prevention tools resolve 73.6% of disputes before they escalate.

- Every touchpoint matters – Clear checkout displays, recognizable billing descriptors, detailed confirmation emails, and pre-charge reminders work together to prevent disputes.

- Measure net revenue, not just conversion – A high-converting upsell with high chargebacks can be net negative. Track 60-day dispute rates alongside conversion rates for true profitability.

Guide Orientation: What This Guide Covers

This guide shows you how transparent pricing in your checkout process directly reduces chargebacks and boosts conversion rates. You will learn to implement order bumps and upsells that customers trust, not dispute.

This is for eCommerce managers at established online businesses who want to add revenue through checkout upsells without triggering the chargeback surge that often follows. By the end, you will understand how to structure offers, communicate pricing, and manage disputes before they escalate.

We cover the relationship between checkout transparency and chargeback management. We do not cover general conversion optimization tactics unrelated to pricing clarity or dispute prevention.

Why Transparent Pricing Matters Now

Chargebacks are growing faster than eCommerce itself. Chargebacks continue to rise globally as eCommerce volume increases, with customer disputes often tied to unclear transactions and misunderstood purchases, as outlined by Visa. Your checkout upsells are increasingly in the crosshairs.

Chargeback rates in eCommerce rose 222% from Q1 2023 to Q1 2024. The primary driver? Friendly fraud, which accounts for 75% of disputes. Customers claim they did not authorize charges they actually made, often because they forgot about an upsell or did not understand what they purchased.

The cost of inaction is concrete. Add processing fees, chargeback fees, and potential account termination, and unclear checkout pricing becomes an existential risk.

The online travel sector learned this the hard way, facing an 816% chargeback surge from Q1 2023 to Q1 2024. High-ticket upsells and add-ons drove $25 billion in disputes in 2023 alone. Your eCommerce checkout faces identical dynamics when transparency fails.

Core Concepts: Understanding the Transparency-Chargeback Connection

What Chargeback Management Actually Means

Chargeback management is the systematic process of preventing, responding to, and recovering from payment disputes. It includes prevention (stopping disputes before they happen), representation (fighting invalid chargebacks), and analysis (identifying patterns to fix root causes).

Effective chargeback defense starts before a customer ever contacts their bank. As Chargeflow experts note, “Effective prevention creates a foundation for strong chargeback management by addressing the root causes of disputes.”

Order Bumps and Upsells: The Risk Zone

Order bumps are additional offers presented at checkout, typically with a single click to add. Upsells are higher-value alternatives or add-ons offered during or after the initial purchase. Both increase average order value but create dispute risk when customers do not clearly understand what they bought.

The distinction matters: a transparent order bump converts and sticks. A confusing one converts, then triggers a chargeback 30 days later when the customer reviews their statement.

Why “Friendly Fraud” Is Your Real Enemy

79% of merchants experienced chargebacks in 2024, up from 34% in 2023. Most of these are not criminal fraud. They are customers who forgot, misunderstood, or regretted a purchase. Transparent pricing eliminates the “I did not know” defense that makes friendly fraud so hard to fight.

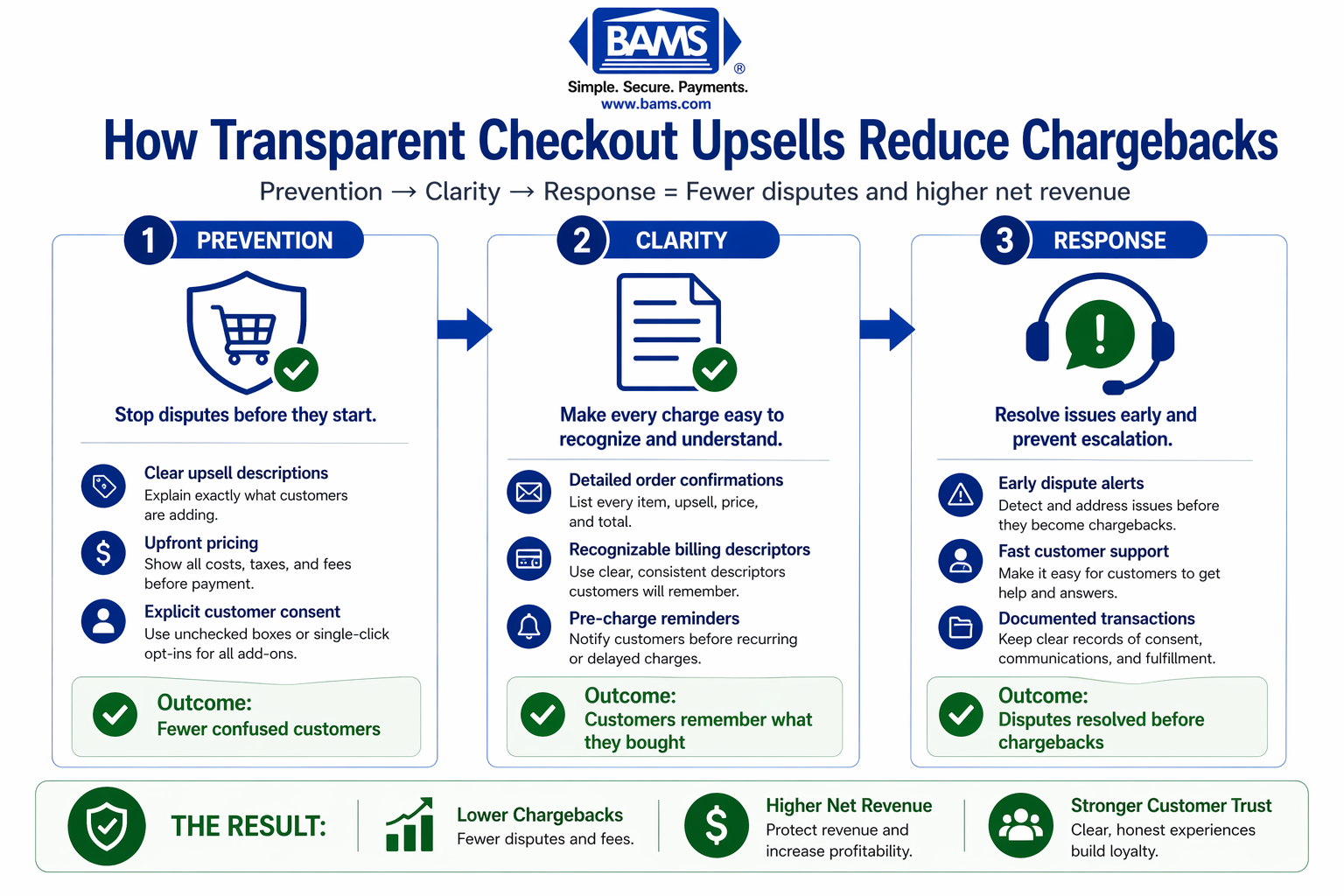

The Framework: Prevention-Clarity-Response

This guide follows a three-phase approach to connecting transparent pricing with chargeback reduction.

A 3-phase framework demonstrating how transparent checkout upsells prevent disputes, improve customer understanding, and reduce chargebacks.

Phase 1: Prevention focuses on checkout process analysis and designing upsells that communicate clearly. You build trust signals directly into your offers.

Phase 2: Clarity addresses post-purchase communication. Order confirmations, billing descriptors, and follow-up emails reinforce what customers bought and why.

Phase 3: Response covers what happens when disputes occur despite prevention. You will learn to document transparency for successful representation and identify patterns that reveal systemic issues.

These phases interconnect. Strong prevention reduces response workload. Clear documentation in the clarity phase provides evidence for the response phase. Analysis from response feeds back into prevention improvements.

Step-by-Step Breakdown

Step 1: Audit Your Current Checkout for Transparency Gaps

Objective: Identify every point where customers might misunderstand what they are buying or how much they will pay.

Start with checkout process analysis from your customer’s perspective. Go through your own checkout as a first-time buyer. Note every upsell, order bump, and additional charge. Ask yourself: would I remember agreeing to this in 30 days?

Document each add-on offer with screenshots. Record the exact language used, the price display, and how the “add to order” action works. Check your billing descriptor, which is what appears on customer bank statements. If it says “ACME LLC” instead of your brand name, customers will not recognize the charge.

Review your last 90 days of chargebacks. Categorize them by reason code. Look for patterns: are disputes concentrated on specific products, upsells, or order values? This data reveals where transparency is failing.

Anti-patterns to avoid: Do not assume your checkout is clear because you understand it. Do not skip the billing descriptor check. Do not ignore “low-value” chargebacks, as they indicate systemic issues.

Success indicators: You have a complete map of every charge point in your checkout. You know exactly what customers see on their bank statements. You have categorized recent chargebacks by root cause.

Step 2: Redesign Upsells for Unmistakable Clarity

Objective: Structure order bumps and upsells so customers cannot misunderstand what they are adding or what it costs.

Apply the “statement test” to every offer. Write the upsell description as it would appear on a bank statement. If a customer would not recognize it, rewrite the offer. “Premium Shipping Protection, $4.99” is clear. “Add-on #3” is not.

Use explicit price displays. Show the additional cost separately from the order total, then show the new total with the upsell included. Avoid percentage discounts without showing the actual dollar amount. “Save 20%” means nothing if customers do not know the base price.

Require deliberate action for high-value adds. Single-click additions work for low-cost items. For anything over $20, add a confirmation step. This friction reduces conversions slightly but eliminates “I did not mean to add that” disputes entirely.

Include clear cancellation and refund terms directly on the upsell offer. Do not bury them in terms of service. If the add-on is a subscription, state the billing frequency in the offer itself.

Anti-patterns to avoid: Pre-checked boxes for upsells (illegal in some jurisdictions and dispute magnets everywhere). Vague descriptions like “protection plan” without specifics. Hiding the upsell price until after checkout.

Success indicators: Every upsell clearly states what it is, what it costs, and how to cancel. High-value adds require confirmation. You can explain any charge to a customer in one sentence.

Step 3: Build Trust Signals Into Your Checkout Experience

Objective: Reduce the psychological distance between purchase and payment, making customers confident they understand their transaction. Clear payment security standards help protect customer data and build confidence during checkout, reducing post-purchase disputes, as defined by the PCI Security Standards Council.

Display running totals prominently throughout checkout. Every time an item is added or an upsell is accepted, update the visible total immediately. Customers should never be surprised by the final amount.

Display security badges and use an integrated payment gateway that ensures fast, secure, and transparent transactions. This reduces uncertainty at the moment of payment and helps prevent disputes caused by unclear or delayed processing.

Implement order summary review before final submission. This single-page checkout best practice forces customers to see everything they are buying. Make the summary scannable with clear line items, quantities, and prices.

Add a “questions about your order?” link with immediate access to support. Customers who can get answers before buying do not file chargebacks after. Live chat or a visible phone number reduces disputes more than any fraud tool.

Anti-patterns to avoid: Hiding totals until the final step. Using generic security badges without actual security. Making support contact information hard to find.

Success indicators: Customers see their complete order total at every checkout stage. Support is accessible before purchase completion. Your checkout passes the “would my parent understand this?” test.

Step 4: Optimize Post-Purchase Communication

Objective: Reinforce purchase details immediately and repeatedly so customers remember what they bought when they see their statement.

Send order confirmation emails within minutes, not hours. Include every line item with descriptions matching what customers saw at checkout. Show the exact amount charged and the billing descriptor that will appear on their statement.

For orders with upsells, call out the add-ons specifically. “Your order includes Premium Shipping Protection ($4.99)” reminds customers what they added. This simple line prevents the “I do not recognize this charge” dispute.

Set up shipping notifications with order details repeated. Each touchpoint reinforces the purchase. By the time customers see their bank statement, they have seen the charge details three or four times.

Create a post-purchase email for subscription upsells that clearly states when the next charge will occur. Send reminder emails before recurring charges. Mastercard’s 2025 Global Chargebacks Outlook emphasizes that “businesses willing to embrace new tools” for proactive communication see significantly lower dispute rates.

Anti-patterns to avoid: Generic confirmation emails without itemization. Failing to mention the billing descriptor. Surprising customers with recurring charges.

Success indicators: Confirmation emails include complete order details and billing descriptor. Subscription customers receive advance notice of charges. Your email open rates indicate customers are seeing these communications.

Step 5: Implement Pre-Chargeback Intervention

Objective: Catch and resolve disputes before they become chargebacks through alert systems and rapid response.

Enroll in card network alert programs. Visa and Mastercard offer merchant notification when customers initiate disputes. These alerts give you hours to resolve issues before they become formal chargebacks.

Modern payment infrastructure enables faster transaction visibility and proactive issue resolution, helping businesses reduce disputes before they escalate according to Modern Treasury.

Create a rapid response protocol for dispute alerts. When you receive notification, contact the customer immediately with their order details. Often, a simple reminder of what they purchased resolves the issue. Offer refunds proactively for legitimate confusion.

Track customer service inquiries about charges. A customer asking “what is this charge?” is a pre-chargeback signal. Train support staff to treat these inquiries as urgent and to document the resolution.

Work with a payment processor that offers proactive chargeback defense. Integrated alert systems and rapid response tools built into your merchant services reduce the manual work of intervention.

Anti-patterns to avoid: Waiting for formal chargebacks to respond. Treating customer confusion as a support ticket rather than a dispute risk. Using processors without alert integration.

Success indicators: You receive and respond to dispute alerts within hours. Customer inquiries about charges are flagged and prioritized. Your pre-chargeback resolution rate exceeds 50%.

Step 6: Document Everything for Successful Representation

Objective: Build an evidence system that proves customer awareness and consent for every upsell transaction.

Capture checkout screenshots at the time of purchase. Automated systems can record exactly what the customer saw, including upsell offers, price displays, and confirmation screens. This evidence is crucial for representation.

Log customer interactions tied to order IDs. If a customer contacted support, clicked a confirmation email, or engaged with shipping notifications, document it. This proves they were aware of and engaged with their purchase.

Store IP addresses, device information, and session data. For friendly fraud disputes, proving the legitimate customer made the purchase is half the battle. Detailed transaction records support your case.

Create representation templates for common dispute types. When a chargeback arrives, you should be able to compile evidence within hours, not days.

Understand pre-arbitration fees and processes before deciding to fight every dispute. For small transactions, accepting the chargeback may cost less than the arbitration risk.

Anti-patterns to avoid: Relying on memory instead of documentation. Fighting every chargeback regardless of evidence strength. Missing representation deadlines.

Success indicators: You can compile complete evidence packages within 24 hours. Your representation win rate exceeds the 45% industry average. You make informed decisions about which disputes to fight.

Step 7: Analyze and Iterate Based on Dispute Data

Objective: Use chargeback patterns to continuously improve checkout transparency and reduce future disputes.

Review dispute data monthly. Categorize by reason code, product, upsell type, and customer segment. Look for concentrations that indicate specific transparency failures.

Calculate the true cost of each upsell. Revenue from an order bump minus chargebacks, fees, and support costs equals actual value. Some high-converting upsells are net negative when dispute costs are included.

A/B test transparency improvements. Try different price display formats, confirmation flows, and post-purchase communications. Measure both conversion rates and 60-day chargeback rates. A slight conversion decrease with a significant chargeback reduction often improves net revenue.

Share dispute insights with your product and marketing teams. If a specific product or offer generates disproportionate disputes, the issue may be product quality or marketing claims, not checkout transparency.

Anti-patterns to avoid: Treating chargebacks as a cost of doing business without analysis. Optimizing only for conversion without tracking disputes. Siloing dispute data from other business functions.

Success indicators: Monthly dispute reports identify specific improvement opportunities. You know the net profitability of each upsell including dispute costs. Transparency changes are tested and measured.

Practical Examples

Scenario: The Hidden Subscription Upsell

An eCommerce store offers a “VIP Membership” upsell at checkout for $9.99/month with the first month free. The offer converts at 12%, adding significant revenue. After 60 days, chargebacks spike. Customers forgot they signed up and do not recognize the recurring charge.

The fix: The store redesigns the offer to clearly state “$9.99/month starting [specific date]” with a checkbox customers must actively select. They add a confirmation email on signup and a reminder email three days before the first charge. Conversion drops to 8%, but chargebacks on the membership fall 70%. Net revenue increases.

Scenario: The Confusing Order Bump

A retailer adds a “Product Protection Plan” order bump. The offer says “Protect your purchase for just $3.99.” Customers add it without understanding it is a third-party warranty, not shipping insurance. Disputes follow when claims are denied or customers do not remember adding it.

The fix: The offer is rewritten to “Extended Warranty by [Provider Name], $3.99, covers defects for 2 years.” The billing descriptor is updated to include the provider name. A post-purchase email explains exactly what the warranty covers and how to file a claim. Disputes drop 60% while conversions remain stable.

Common Mistakes and Pitfalls

A side-by-side comparison of common checkout upsell mistakes that trigger chargebacks versus best practices that prevent disputes and build customer trust.

Optimizing for conversion alone. High-converting upsells with high dispute rates destroy profitability. Always measure the 60-day chargeback rate alongside conversion.

Assuming customers read everything. They do not. Critical information must be unmissable, not just present. If it can be skipped, it will be.

Blaming customers for disputes. Even when chargebacks are technically “friendly fraud,” they often result from genuine confusion. Fix the confusion instead of fighting every dispute.

Neglecting billing descriptors. Your checkout can be perfect, but if customers do not recognize the charge on their statement, they will dispute it. Check your descriptor monthly.

Treating chargeback management as a payment processor’s job. Your processor can help, but preventing legitimate chargebacks through transparency is your responsibility.

What to Do Next

Start with one action: go through your own checkout as a customer today. Note every upsell, every price display, and what appears on your test transaction’s bank statement. This single exercise reveals more transparency gaps than any audit report.

From there, prioritize fixes based on your chargeback data. If you do not have categorized dispute data, that is your second action: build a simple tracking system for the next 30 days.

Return to this guide as you implement changes. The framework is designed for iteration, not one-time execution. Each improvement in transparency compounds over time, reducing disputes while building the customer trust that drives sustainable conversion rates.

Frequently Asked Questions

What is checkout optimization and why is it important for reducing chargebacks?

Checkout optimization is the process of improving your payment flow to increase conversions while reducing friction and confusion. For chargeback prevention, it means designing upsells and pricing displays so customers clearly understand every charge. When customers know exactly what they bought, they do not dispute charges they do not recognize.

How can I reduce cart abandonment during the checkout process without increasing dispute risk?

Focus on clarity over speed. Show running totals at every step, use single-page checkout with clear order summaries, and make support accessible before purchase completion. Guest checkout options reduce friction without sacrificing transparency. The goal is confident buyers who complete purchases and remember them.

Which payment methods should I offer to optimize my checkout experience?

Offer the methods your customers prefer, typically credit cards, debit cards, and digital wallets like Apple Pay or Google Pay. More important than variety is consistency: ensure your billing descriptor is recognizable across all payment methods. A customer paying with PayPal should see the same clear charge description as one using a credit card.

How can I build trust with customers during the checkout process?

Display security badges near payment fields, show complete order summaries before final submission, and make support contact information visible. Include clear refund and cancellation terms directly on upsell offers. Trust signals reduce both abandonment and post-purchase anxiety that leads to disputes.

What is the difference between preventing chargebacks and fighting them?

Prevention stops disputes before they happen through clear pricing, good communication, and customer service. Fighting chargebacks (representation) happens after a dispute is filed, using evidence to prove the transaction was legitimate. Prevention is significantly more cost-effective. Merchants win only 45% of disputed chargebacks, and the process consumes time and resources regardless of outcome.

How do I know if my upsells are causing chargebacks?

Track chargebacks by product and offer type for 90 days. Look for patterns: are disputes concentrated on specific upsells or order values? Review the reason codes. “Transaction not recognized” and “merchandise not as described” often indicate transparency failures in upsell presentation or post-purchase communication.

Sources