How Transaction Reporting Cuts Payment Processing Costs

Use level 3 data and cost-plus pricing to lower interchange rates and speed up deposits

Learn how strategic transaction reporting reduces payment processing fees and accelerates cash flow. This guide covers level 3 processing requirements and cost-plus pricing for eCommerce businesses.

TL;DR

- Transaction reporting quality directly affects your costs – More detailed data means lower interchange rates, potentially saving 0.5% to 1.5% per transaction through Level 2 and Level 3 processing.

- Cost-plus pricing is essential before optimizing – On tiered pricing, interchange savings go to your processor. Switch to cost-plus pricing first so data optimization benefits your bottom line.

- Next-day funding should be standard – Waiting 3 to 5 days for deposits is a processor limitation, not an industry requirement. Modern eCommerce processors offer next-day funding as standard.

- Monitor your effective rate monthly – Track total fees divided by total volume over time. Catch qualification problems and rate creep before they accumulate into significant losses.

- Start with a pricing audit – Request your last three statements, identify your pricing structure, and calculate your effective rate before investing in any other optimization efforts.

What This Guide Covers and Who It’s For

This guide helps eCommerce managers solve a specific problem: delayed deposits eating into your cash flow while high processing fees chip away at margins. You’ll learn how better transaction reporting connects directly to lower costs and faster access to your money.

By the end, you’ll understand how level 3 processing works, why cost-plus pricing saves you money, and exactly which data fields unlock the lowest interchange rates. This guide is for established online businesses processing $50,000 or more monthly who want predictable cash flow without overpaying for payment processing.

We won’t cover basic payment setup or gateway selection. This is about optimization, specifically using transaction data strategically to reduce what you pay per sale.

Why Transaction Reporting Matters for Your Bottom Line

Better transaction reporting reduces risk, lowers interchange fees, and accelerates deposits, improving overall cash flow.

eCommerce businesses lose money in two predictable ways: waiting too long for deposits and paying more per transaction than necessary. Both problems trace back to how your transactions are reported to card networks.

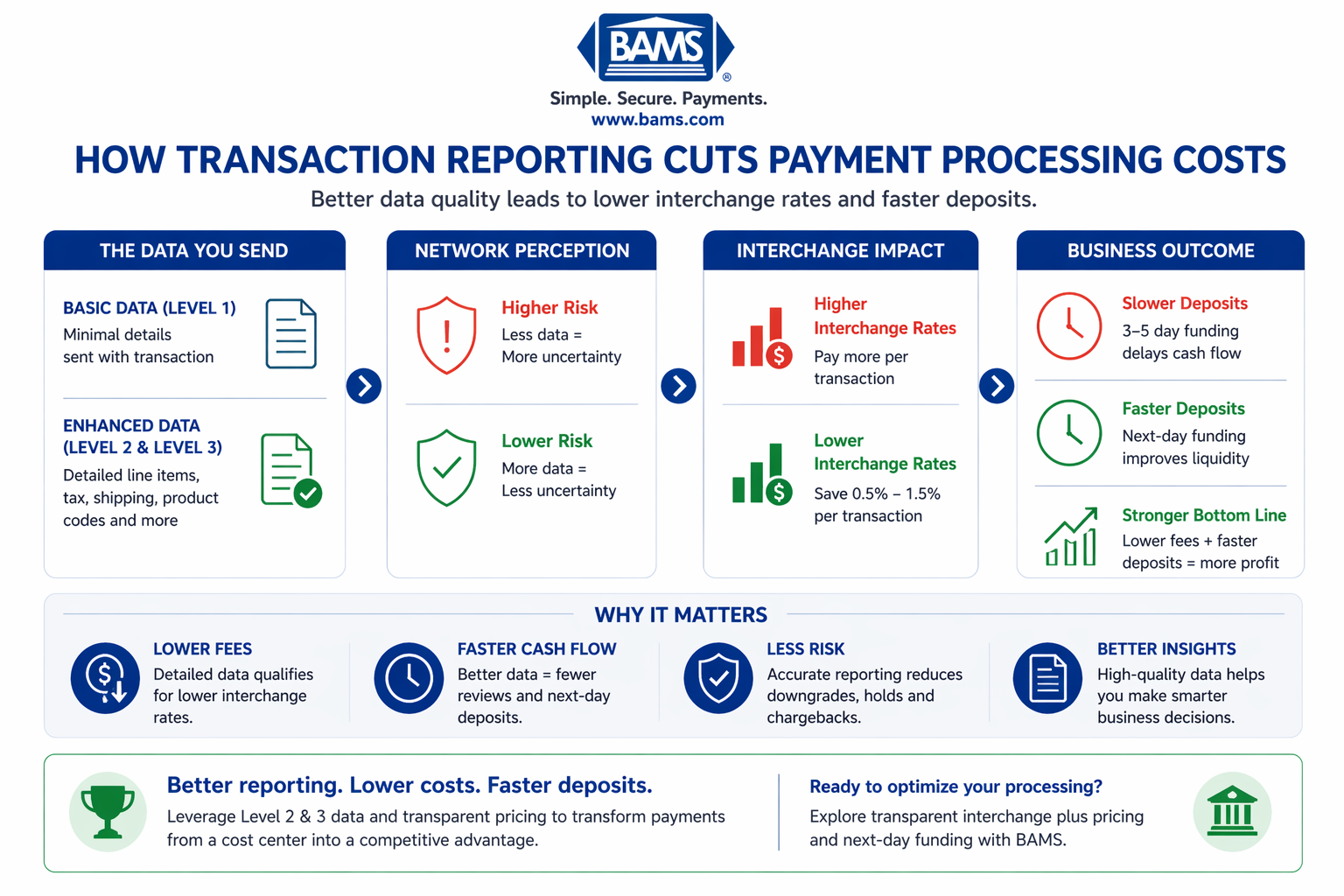

Card networks like Visa and Mastercard set interchange rates based on risk. The more data you provide about a transaction, the lower the perceived risk, and the lower your rate. Most eCommerce platforms send only basic data (card number, amount, date), which means you’re automatically paying higher rates. Interchange fees are structured based on risk and transaction data quality, as outlined by the Federal Reserve.

Delayed deposits compound this problem. When you wait 3 to 5 days for funds, you’re essentially providing interest-free loans to your processor. That delay affects inventory purchases, payroll timing, and your ability to respond to opportunities.

The connection between these issues is transaction reporting. Better data means lower rates. Better processing partners mean faster deposits. Together, they transform payments from a cost center into a competitive advantage.

Core Concepts: Understanding the Data-to-Savings Connection

What Level 3 Processing Actually Means

- Level 3 processing refers to the depth of transaction data you submit with each sale.

- Level 1 includes basic information (merchant name, transaction amount).

- Level 2 adds tax amount and customer code. Level 3 includes line-item details: product descriptions, quantities, unit costs, and shipping information.

Card networks reward this detail with lower interchange rates because detailed data reduces fraud risk and simplifies reconciliation for corporate cardholders. The savings range from 0.5% to 1.5% per transaction, depending on card type and transaction size.

Cost-Plus Pricing Explained

Cost-plus pricing (also called interchange-plus) separates your processing costs into two transparent parts: the actual interchange rate set by card networks, plus a fixed markup from your processor. This differs from transparent interchange plus pricing, which bundles everything into opaque categories.

With cost-plus pricing, when you reduce interchange through better data, you keep the savings. With tiered pricing, those savings often disappear into your processor’s margin.

The Reporting-Funding Connection

Transaction reporting quality affects funding speed. Clean, complete data processes faster through authorization networks. Processors with robust reporting systems can batch and settle transactions more efficiently, enabling next-day funding instead of the standard 2 to 5 day wait.

The Framework: From Delayed Deposits to Optimized Cash Flow

A practical framework for lowering payment processing costs through better data, pricing optimization, and reporting strategy.

Solving delayed deposits and high fees requires a systematic approach across four connected areas: pricing structure, data optimization, processor capabilities, and ongoing monitoring.

First, you need transparent pricing that lets you benefit from optimization efforts. Second, you need systems that capture and transmit detailed transaction data. Third, you need a processor equipped to handle that data and fund you quickly. Fourth, you need reporting tools to verify you’re actually getting the rates you deserve.

These elements work together. Level 3 processing without cost-plus pricing wastes your optimization effort. Cost-plus pricing without good reporting leaves you unable to verify savings. Each component depends on the others.

Modern payment infrastructure enables faster settlement and better reporting capabilities, improving both cost efficiency and cash flow according to Modern Treasury.

Step 1: Audit Your Current Pricing Structure

Objective

Determine whether your current pricing model allows you to benefit from transaction reporting improvements.

What to Do

Request your complete processing statement from the past three months. Look for how rates are presented. If you see categories like “qualified,” “mid-qualified,” and “non-qualified,” you’re on tiered pricing. If you see individual interchange categories (like “Visa CPS Retail” or “MC Data Rate II”) plus a consistent markup, you’re on cost-plus pricing.

Calculate your effective rate by dividing total fees by total volume. Compare this to published interchange rates for your transaction types. A gap larger than 0.3% to 0.5% suggests room for improvement.

What to Avoid

Don’t assume your current rate is competitive because you negotiated it recently. Pricing structures matter more than rate promises. A “low” tiered rate can cost more than a “higher” interchange-plus rate because of how transactions get categorized.

Success Indicators

You can identify exactly what you pay per transaction type. You understand whether your pricing structure rewards or ignores optimization efforts.

Step 2: Map Your Transaction Data Capabilities

Objective

Identify what data your eCommerce platform currently sends and what additional fields you could capture.

What to Do

Review your payment gateway settings and integration documentation. Most platforms can send Level 2 data (tax amount, customer code) with minimal configuration. Level 3 data requires more setup but delivers bigger savings, especially for B2B merchant account.

Create an inventory of data you already capture: product SKUs, descriptions, quantities, unit prices, tax amounts, shipping costs, and customer purchase order numbers. Compare this against Level 3 data requirements to identify gaps.

What to Avoid

Don’t assume your platform automatically sends all available data. Many eCommerce systems capture detailed information but only transmit basic fields to payment processors. The data exists; it’s just not being used.

Success Indicators

You have a documented list of data fields you capture versus data fields you transmit. You’ve identified specific gaps that, if closed, would qualify transactions for lower interchange categories.

Step 3: Configure Level 2 and Level 3 Data Transmission

Objective

Enable your systems to send enhanced transaction data that qualifies for lower interchange rates.

What to Do

Work with your payment gateway provider to enable Level 2 and Level 3 data fields. For Level 2, ensure tax amount and customer code fields are populated and transmitted. For Level 3, configure line-item detail transmission including product codes, descriptions, quantities, and unit costs.

If you process significant B2B volume, prioritize Level 3 configuration. Corporate and purchasing cards offer the largest rate reductions for detailed data. A B2B-focused merchant account can help ensure your systems are properly configured.

Test transactions after configuration changes. Verify that enhanced data appears in your gateway reports and that transactions are qualifying for lower interchange categories. Detailed transaction data improves processing efficiency and reduces risk, helping qualify transactions for better rates as supported by Visa.

What to Avoid

Don’t enable Level 3 processing without verifying your pricing structure supports it. On tiered pricing, your processor may pocket the interchange savings rather than passing them to you. Ensure you’re on cost-plus pricing first.

Success Indicators

Test transactions show Level 2 or Level 3 qualification in your processing reports. You see lower interchange rates on transactions with enhanced data compared to basic transactions.

Step 4: Establish Next-Day Funding

Objective

Reduce the gap between sale and deposit to improve cash flow predictability.

What to Do

Confirm your processor offers next-day funding and understand any requirements. Some processors require specific batch times, minimum processing history, or reserve accounts. Know the cutoff times for same-day batching.

Review your batch settlement schedule. Transactions batched before the cutoff fund next day; transactions after the cutoff add another day. Adjust your batch timing to maximize next-day funding.

Consider whether your current processor can deliver on funding speed. Many traditional processors treat next-day funding as a premium feature. Partners focused on eCommerce payment processing often include it as standard.

What to Avoid

Don’t accept “2 to 3 business days” as normal. Modern payment infrastructure supports next-day funding for most transaction types. If your processor can’t deliver, the limitation is their system, not industry standard.

Success Indicators

Deposits arrive consistently the next business day. You can predict cash availability with confidence for operational planning.

Step 5: Implement Transaction Reporting Monitoring

Objective

Create visibility into whether your optimization efforts are delivering expected results.

What to Do

Set up regular review of your processing statements, at minimum monthly. Track your effective rate over time and by transaction type. Look for transactions that should qualify for lower rates but aren’t.

Create a simple tracking spreadsheet with columns for total volume, total fees, effective rate, and Level 2/Level 3 qualification percentage. Trend this data monthly to spot problems early.

Request detailed interchange qualification reports from your processor. These show exactly which interchange category each transaction qualified for and why. Use this data to identify systematic issues.

What to Avoid

Don’t rely solely on summary statements. The overall effective rate can hide problems. A few high-rate transactions can offset savings from many optimized transactions. Dig into the details.

Success Indicators

You can explain your effective rate and identify which transaction types contribute most to costs. You catch qualification problems within one billing cycle.

Step 6: Address Common Qualification Failures

Objective

Fix systematic issues that prevent transactions from qualifying for optimal interchange rates.

What to Do

Review transactions that downgraded from expected interchange categories. Common causes include missing data fields, authorization-to-settlement time exceeding limits, and mismatched transaction amounts.

For eCommerce, ensure Address Verification Service (AVS) data is collected and transmitted. Missing AVS data causes automatic downgrades on many card types. Similarly, ensure CVV is collected for card-not-present transactions.

Check your authorization-to-settlement timing. Most card networks require settlement within 24 to 48 hours of authorization. Delayed shipments with delayed capture can cause downgrades. Consider authorizing at shipment rather than checkout for high-value orders.

What to Avoid

Don’t assume all downgrades are unavoidable. Many result from configuration issues or process gaps that are fixable. Investigate before accepting higher rates as normal.

Success Indicators

Downgrade rate decreases month over month. You can identify and explain remaining downgrades as genuinely unavoidable (specific card types, customer data issues).

Step 7: Integrate Chargeback Prevention with Reporting

Objective

Use transaction data to reduce chargebacks, which affect both direct costs and long-term processing rates.

What to Do

Connect your transaction reporting to chargeback prevention strategies. Detailed transaction data helps dispute illegitimate chargebacks by providing evidence of what was ordered, shipped, and delivered.

Implement clear billing descriptors that customers recognize. Confusion about charges is a leading cause of “friendly fraud” chargebacks. Your descriptor should clearly identify your business name and ideally include a customer service number.

Monitor chargeback ratios by card type and transaction characteristic. High chargebacks trigger rate increases and can threaten your merchant account. Early detection through good reporting prevents escalation.

What to Avoid

Don’t treat chargebacks as purely a customer service problem. They directly affect your processing costs. A chargeback ratio above 1% puts you in monitoring programs with higher rates and potential account termination.

Success Indicators

Chargeback ratio stays below 0.5%. You successfully dispute a higher percentage of chargebacks using transaction documentation.

Common Mistakes That Undermine Optimization Efforts

The most common mistake is optimizing data without fixing pricing structure. eCommerce managers invest time configuring Level 3 processing while on tiered pricing, then wonder why their rates don’t improve. Always establish cost-plus pricing before investing in data optimization.

Another frequent error is inconsistent monitoring. Businesses implement improvements, see initial results, then stop tracking. Rates creep up through card network changes, processor fee adjustments, or system configuration drift. Ongoing monitoring catches these issues before they accumulate.

Finally, many businesses underestimate the cash flow impact of delayed deposits. They focus entirely on rate optimization while ignoring funding speed. A 0.2% rate reduction means little if you’re waiting five days for funds you need to buy inventory or make payroll.

What to Do Next

Start with your pricing structure. Request your last three processing statements and determine whether you’re on cost-plus or tiered pricing. If you’re on tiered pricing, addressing that unlocks everything else.

If you’re already on cost-plus pricing, audit your Level 2 and Level 3 data transmission. Most eCommerce platforms have this capability; it’s often just not enabled. One configuration change can reduce your effective rate on every transaction going forward.

Use this guide as a reference rather than a one-time checklist. Transaction reporting optimization is ongoing. Card networks update interchange categories, your product mix changes, and new payment methods emerge. Revisit these steps quarterly to ensure your systems stay optimized.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposits depend on three factors: your processor’s capabilities, your batch settlement timing, and your transaction data quality. Next-day funding is achievable with processors who prioritize eCommerce and with clean transaction data that processes efficiently. Batch your transactions before your processor’s daily cutoff time to ensure same-day processing and next-day funding.

How can I improve my payment authorization rates?

Authorization rates improve with accurate customer data, proper AVS configuration, and retry logic for soft declines. Ensure your checkout captures complete billing address information and transmits it with authorization requests. For subscription or recurring payments, implement account updater services that automatically refresh expired card details.

Which payment processing fees can I reduce to optimize costs?

The largest reducible fee is interchange, which typically represents 70% to 80% of total processing costs. Interchange rates drop when you provide detailed transaction data through Level 2 and Level 3 processing. Additionally, ensure you’re on cost-plus pricing so interchange reductions flow to your bottom line rather than your processor’s margin.

What role does fraud protection play in payment optimization?

Fraud protection directly affects your processing costs in two ways. First, chargebacks from fraud increase your direct costs and can push you into high-risk pricing tiers. Second, good fraud prevention allows you to accept more transactions confidently, improving authorization rates without increasing losses. Balance fraud screening strictness to avoid rejecting legitimate customers.

When should I consider expanding my payment options?

Expand payment options when you see cart abandonment at checkout or when customer feedback indicates preferred methods aren’t available. Digital wallet payments often have lower fraud rates and can reduce cart abandonment. However, each new payment method adds complexity, so prioritize options your specific customers request rather than adding everything available.

How does Level 3 processing differ from standard transaction processing?

Standard processing sends minimal data: card number, amount, and date. Level 3 processing adds detailed line-item information including product descriptions, quantities, unit costs, tax amounts, and shipping details. This additional data reduces perceived risk for card networks, qualifying transactions for lower interchange rates, particularly on corporate and purchasing cards used in B2B transactions.

Sources