7 Ways to Boost Authorization Rates in eCommerce

Actionable strategies for eCommerce managers to recover declined payments and capture lost revenue

Learn the specific tactics that separate high-performing payment stacks from the rest. This guide covers network tokenization, smart retry logic, and data optimization techniques that can recover 2-5% of previously lost transactions.

TL;DR

- Smart routing recovers 5% of declines by directing transactions to optimal processors based on card type and geography

- Network tokenization adds up to 6% approval lift because issuers trust tokenized transactions more than raw card numbers

- Digital wallets boost approvals 2-5% through built-in biometric authentication that reduces fraud flags

- Data enrichment increases approvals by 3% by giving issuers the context they need to confidently approve transactions

- Start with 2-3 strategies based on your specific decline patterns rather than implementing everything at once

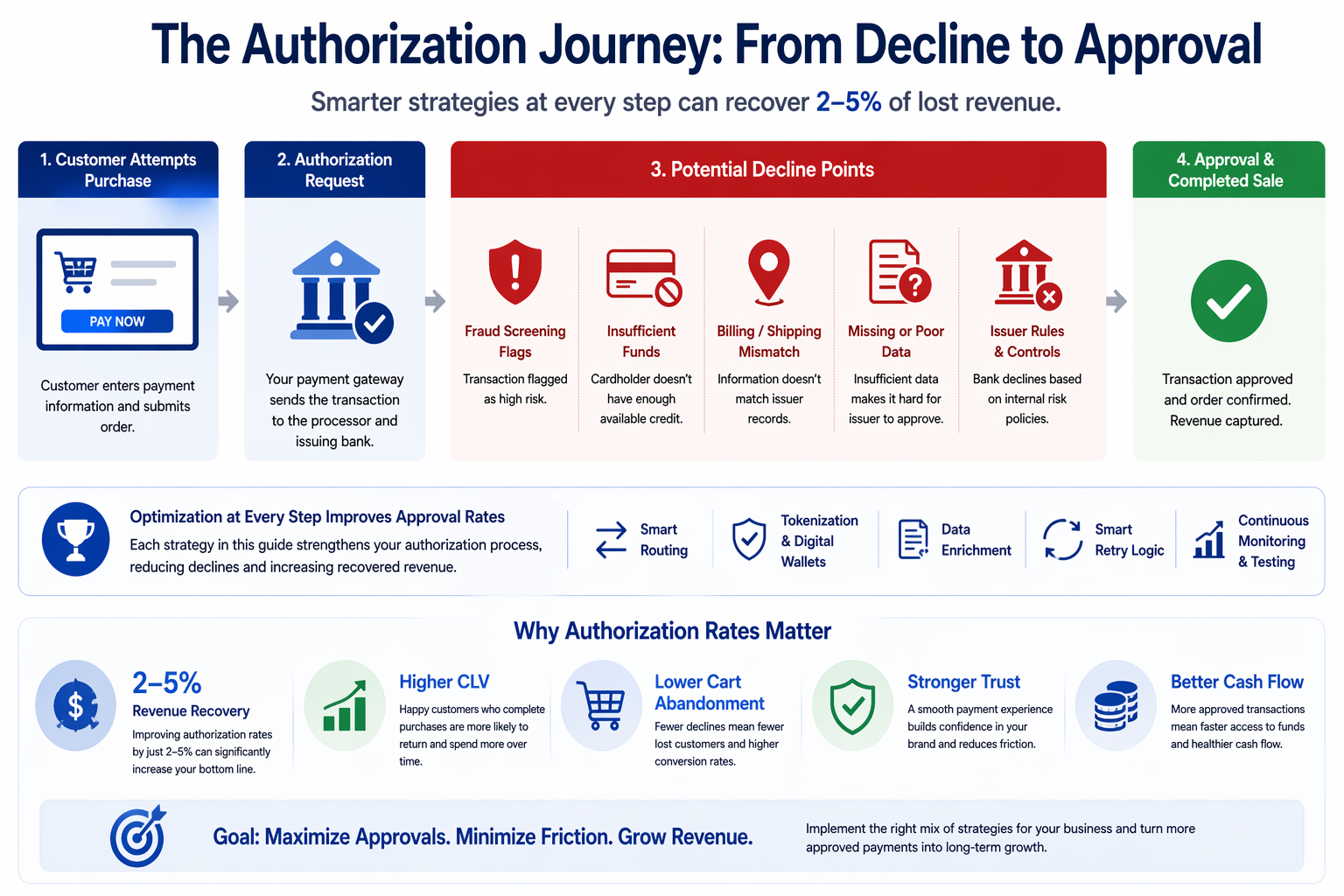

The Hidden Cost of Declined Transactions in 2025

Understanding where and why transactions fail helps businesses apply targeted strategies to recover lost revenue and improve approval rates.

Every declined transaction represents more than a lost sale. It signals potential customer frustration, abandoned carts, and revenue that quietly disappears from your bottom line. For eCommerce managers handling thousands of monthly transactions, even a 2% improvement in authorization rates can translate to significant recovered revenue.

The payment landscape continues to evolve. According to Visa, modern payment systems are designed to improve approval rates while maintaining security and efficiency.

Issuers now use sophisticated fraud detection that sometimes flags legitimate purchases. Cross-border transactions face additional scrutiny. And the gap between merchants who optimize their payment stack and those who accept default settings continues to widen.

Authorization rate improvement isn’t about a single fix. It requires understanding why transactions fail, how modern payment infrastructure addresses those failures, and which interventions deliver measurable results for your specific business model.

What This Guide Covers (And What It Doesn’t)

This guide targets eCommerce managers at established online businesses processing consistent transaction volume who want actionable strategies for customer payment recovery and faster access to funds. You’re past the startup phase and ready to optimize rather than simply survive.

We won’t cover basic payment setup or entry-level fraud prevention. Instead, we focus on intermediate-to-advanced tactics that require some existing payment infrastructure to implement effectively. Each strategy assumes you already have a functioning eCommerce payment gateway and baseline transaction reporting in place.

How We Selected These Strategies

Each strategy meets three criteria: documented impact on authorization rates from industry research, practical implementation for mid-size eCommerce operations, and compatibility with maintaining strong fraud protection. We prioritized approaches that balance recovery rates with security rather than sacrificing one for the other.

Combining multiple optimization strategies creates a compounding effect that increases approval rates and recovers lost revenue.

1. Implement Smart Transaction Routing

Why It Matters

Not all payment processors handle every transaction type equally well. A processor excellent for domestic debit cards might underperform on international credit transactions. Smart routing directs each transaction to the processor most likely to approve it based on card type, geography, and historical performance data.

What It Looks Like Today

Modern routing technology analyzes transaction characteristics in real-time and selects optimal pathways. According to Nuvei’s 2024 research, smart routing converts up to 5% of declined transactions into approvals. This isn’t theoretical. It’s measurable recovery happening at the infrastructure level.

How to Apply It

Start by auditing your current decline patterns. Identify whether failures cluster around specific card types, regions, or transaction amounts. Then evaluate whether your payment gateway insights reveal routing options you’re not using. Many established processors offer routing capabilities that merchants never activate.

2. Deploy Network Tokenization

Why It Matters

Card-on-file transactions using traditional card numbers (PANs) face higher decline rates than tokenized transactions. Issuers trust network tokens more because they’re harder to compromise and easier to verify. This trust translates directly into approvals.

What It Looks Like Today

For eligible merchants in 2025, this improvement has grown to approximately 6%. That’s a substantial lift from a single technical implementation.

How to Apply It

Review your stored credential handling. If you’re still storing raw card numbers (even encrypted), you’re leaving authorization rate improvement on the table. Prioritize tokenization for subscription billing and repeat customers where the impact compounds over time.

3. Expand Digital Wallet Acceptance

Why It Matters

Digital wallets like Apple Pay and Google Pay include built-in authentication that issuers recognize and trust. The biometric verification (fingerprint, face recognition) that customers perform before completing payment reduces fraud risk, which increases issuer confidence in approving transactions.

The PCI Security Standards Council emphasizes that strong fraud detection and compliance frameworks are essential to balance transaction approvals with security.

What It Looks Like Today

Beyond approval rates, digital wallet payments typically process faster and reduce cart abandonment by streamlining checkout. For guidance on implementing fraud protection measures alongside digital wallets, consider how biometric authentication shifts risk away from your business.

How to Apply It

Audit your checkout flow for digital wallet visibility. If Apple Pay and Google Pay buttons appear below the fold or require extra clicks, you’re suppressing adoption. Place them prominently and test whether mobile customers convert at higher rates when wallets are the default option.

4. Enrich Transaction Data Before Authorization

Why It Matters

Issuers decline transactions they can’t confidently evaluate. Incomplete or inconsistent data triggers caution. By enriching each transaction with cleaner formatting, additional context, and pre-authorization screening, you give issuers the information they need to say yes.

What It Looks Like Today

Enriching orders with cleaner data and richer context can increase authorization rates by up to 3% on average. This includes standardizing address formats, validating email domains, and providing device fingerprinting data that helps issuers distinguish legitimate customers from fraudsters.

How to Apply It

Examine what data you’re currently sending with each authorization request. Many merchants transmit only required fields. Adding optional fields (customer tenure, order history indicators, device consistency signals) often improves approval rates without requiring new integrations.

5. Implement Automated Decline Recovery

Why It Matters

Some declines are temporary. The customer’s bank flagged an unusual purchase, the card was briefly over-limit, or network congestion caused a timeout. Automated retry logic can recover these transactions without customer intervention, turning potential losses into completed sales.

What It Looks Like Today

Modern systems intelligently time retries, adjust routing on subsequent attempts, and distinguish between soft declines (worth retrying) and hard declines (permanent rejections).

How to Apply It

Configure your payment system to categorize decline codes and apply appropriate retry strategies. Soft declines (insufficient funds, temporary holds) warrant automatic retries with delays. Hard declines (lost/stolen cards, closed accounts) should trigger customer notification workflows instead.

6. Leverage Enhanced Issuer Networks

Why It Matters

Some payment platforms maintain direct relationships with issuing banks that allow them to share additional transaction context. These enhanced networks can flag legitimate transactions that might otherwise be declined, essentially vouching for your customers at the authorization moment.

What It Looks Like Today

Enhanced issuer network programs provide 1-2% authorization rate uplift on eligible volume. This happens through data sharing agreements between processors and issuers that reduce false positive fraud flags. Your transaction data helps train models that benefit all merchants on the network.

How to Apply It

Ask your payment processor whether they participate in enhanced issuer programs and whether your transactions qualify. According to the Federal Reserve, transaction structure and data quality influence both approval rates and processing efficiency.

Some programs require minimum volume thresholds or specific integration requirements. Understanding eligibility helps you prioritize which processor relationships to deepen.

7. Optimize Your Payment Platform Infrastructure

Why It Matters

Legacy payment infrastructure accumulates technical debt that manifests as declined transactions. Outdated API versions, deprecated authentication protocols, and suboptimal connection handling all contribute to preventable failures. Sometimes the biggest authorization rate improvement comes from modernizing your foundation.

What It Looks Like Today

Companies switching to modern payment platforms have seen North American approval rates increase by 2%. These gains come from better network connections, updated authentication flows, and optimized timeout handling rather than any single feature.

How to Apply It

Review your integration age and update status. If you implemented your payment integration more than three years ago without major updates, you’re likely missing optimization opportunities. Schedule a technical audit focused specifically on authorization-related configurations and transaction reporting capabilities.

Patterns Across These Strategies

Three themes connect these approaches. First, authorization rate improvement increasingly depends on data quality and context rather than just transaction mechanics. Issuers approve what they can confidently evaluate. Second, the best customer payment recovery happens invisibly. Customers shouldn’t know their transaction was initially declined and then recovered through smart retry logic.

Third, these strategies compound. Tokenization improves digital wallet performance. Data enrichment enhances the effectiveness of enhanced issuer networks. Smart routing works better when combined with decline recovery. Treating these as an integrated system rather than isolated tactics multiplies their impact.

Where to Start

Don’t attempt all seven strategies simultaneously. Most eCommerce operations should begin with two or three interventions based on their specific decline patterns. If international transactions drive most failures, prioritize smart routing and data enrichment. If subscription billing shows high churn from payment failures, focus on tokenization and automated decline recovery.

Review your payment gateway insights to identify your highest-impact opportunity. Then implement one strategy fully before adding the next. This approach lets you measure actual impact and build organizational knowledge about what moves your specific authorization rates. Payment optimization is a continuous process, not a one-time project.

Frequently Asked Questions

How can I improve my payment authorization rates?

Focus on data quality, modern infrastructure, and smart retry logic. Implement network tokenization for stored cards, expand digital wallet acceptance, and ensure you’re sending complete transaction data with each authorization request. Most merchants see 2-5% improvement by addressing these fundamentals before pursuing advanced optimizations.

What are faster deposit strategies in merchant services?

Guaranteed next-day funding programs, optimized settlement timing, and reducing holds on high-risk transaction types all accelerate access to funds. Work with your payment processor to understand which transactions qualify for expedited settlement and whether your business model supports faster funding options.

Why do legitimate transactions get declined?

Issuers use automated fraud detection that sometimes flags unusual purchase patterns, new customer relationships, or transactions that don’t match historical behavior. Incomplete transaction data, outdated card credentials, and temporary account issues also contribute to false declines on legitimate purchases.

What role does fraud protection play in payment optimization?

Effective fraud protection actually improves authorization rates by building issuer trust. When your fraud screening catches genuine threats, issuers become more confident approving your transactions. The goal is balancing security with approval rates rather than sacrificing one for the other.

Which payment processing fees can I reduce to optimize costs?

Interchange optimization through proper transaction categorization, Level 3 processing for B2B transactions, and cost-plus pricing models often reduce fees. Reducing chargebacks through proactive defense also eliminates penalty fees and preserves your processing rates over time.

When should I consider expanding my payment options?

Expand payment options when you see cart abandonment at checkout, when entering new geographic markets, or when your customer base shows preference for methods you don’t support. Digital wallets specifically warrant priority given their authorization rate benefits and growing consumer adoption.

Sources

- Visa – Payment Processing

- PCI Security Standards Council – Merchant Security

- Federal Reserve – Interchange Fees