7 Hidden Fees in Merchant Services Draining Margins

How to spot silent interchange downgrades your processor hopes you never notice

Learn the specific signals that reveal whether your processor is truly qualifying high-ticket transactions at the lowest interchange rate — or quietly passing through uninspected fees. Built for eCommerce businesses processing $100K+ in annual card volume.

TL;DR

- Your interchange-plus label may be cosmetic – If your processor isn’t submitting Level 2/3 data for B2B and corporate card transactions, you’re paying standard rates despite having a “transparent” pricing model.

- Calculate your effective processing rate monthly – Total fees divided by total volume is the single number that reveals hidden cost drift. If it’s above 2.5% on B2B orders, investigate downgrade surcharges and card mix changes.

- Small fixed fees compound fast – PCI fees, batch fees, statement fees, and network assessment markups can collectively add $1,500 to $2,400+ per year in costs that have no direct relationship to your transaction volume.

- Contract traps prevent switching – Early termination fees and auto-renewal clauses keep you locked into unfavorable pricing. Calendar your contract renewal dates now so you can renegotiate or exit on your terms.

- Audit quarterly, not annually – Hidden fees persist because they’re designed to avoid scrutiny. A simple quarterly review of your statement line items and effective rate removes their advantage.

The Silent Margin Leak Most eCommerce Businesses Miss

U.S. merchants continue to face rising card processing costs as interchange and swipe fee concerns remain a major issue for businesses processing high transaction volumes, according to the Merchant Payments Coalition. For eCommerce businesses processing B2B and high-ticket orders, hidden fees in merchant services are responsible for a disproportionate share of that total. Yet most mid-market operators (10 to 50 employees) have no reliable way to verify whether their processor is actually qualifying large transactions at the lowest available interchange rate, or just claiming to.

The problem isn’t always fraud or bad faith. It’s diagnostic invisibility. Your processor says you’re on interchange-plus pricing. Your statements show line items that look legitimate. But somewhere between the swipe and the settlement, silent downgrades, misclassified transactions, and opaque surcharges erode your margins on every large order.

This guide surfaces the specific signals that reveal whether your credit card processing fees reflect real qualification work or uninspected pass-through billing.

Who This Is For and What It Covers

This list is built for eCommerce managers at established businesses doing $100K to $1M+ in annual card volume, particularly those handling B2B orders, wholesale, or high average order values. If you’re processing consumer micro-transactions under $20, the economics here won’t apply the same way.

We’re not covering how to switch to ACH payment processing or account-to-account payments (those are separate strategies). Instead, we’re focused on the card-present and card-not-present fees you’re already paying, and the specific places where hidden costs accumulate undetected.

How We Selected These Items

Each item was chosen based on three criteria: how frequently it appears in real merchant statements without being questioned, how much margin it can silently consume over a 12-month period, and how actionable the diagnostic step is for a team without a dedicated payments analyst. If you can’t check for it within a billing cycle, it didn’t make the list.

7 Hidden Fees That Inflate Your B2B Processing Costs

The most common hidden merchant service fees quietly increasing B2B payment processing costs.

1. Interchange Downgrade Surcharges on Unqualified Transactions

Why it matters: When a transaction fails to meet the card network’s data requirements for a lower interchange tier, it gets “downgraded” to a higher rate. On a $5,000 B2B order, the difference between Level 3 qualification and a standard rate can be 0.5% to 1.0%, or $25 to $50 per transaction. Multiply that across hundreds of monthly orders, and you’re looking at thousands in silent margin loss.

What it looks like today: Most processors list downgrade fees as a separate line item buried in your monthly statement, sometimes labeled “non-qualified surcharge” or “EIRF” (Electronic Interchange Reimbursement Fee). Some don’t break them out at all, folding them into a blended rate that obscures the problem entirely.

How to apply it: Pull your last three monthly statements. Search for any line item referencing “downgrade,” “non-qual,” or “EIRF.” Calculate the total. Then ask your processor which specific transactions triggered downgrades and what data fields were missing. If they can’t answer, that’s your first red flag.

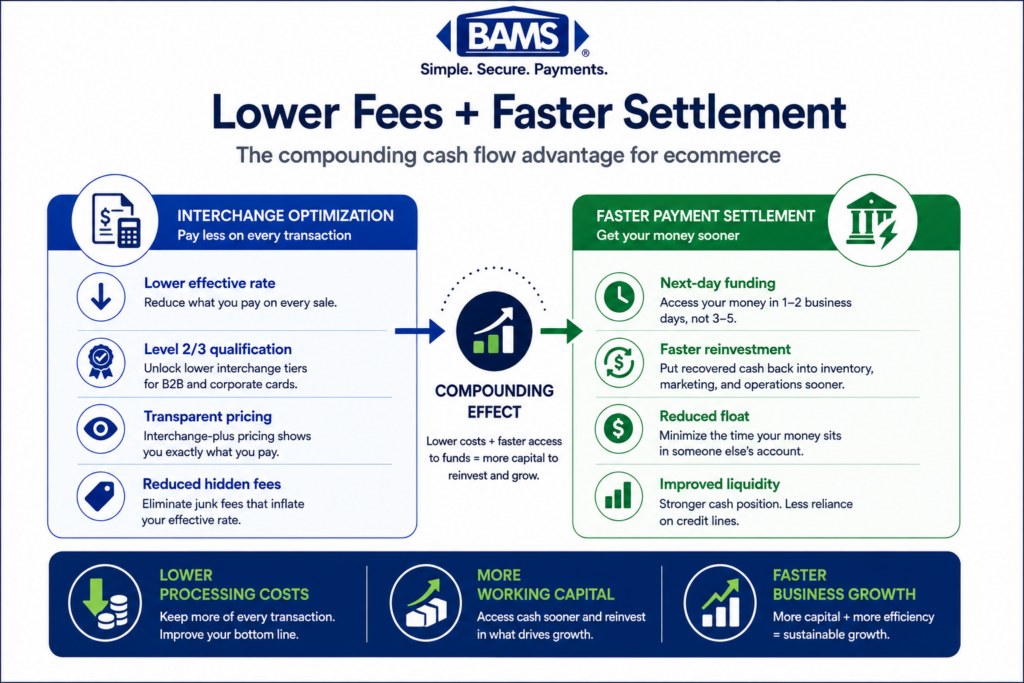

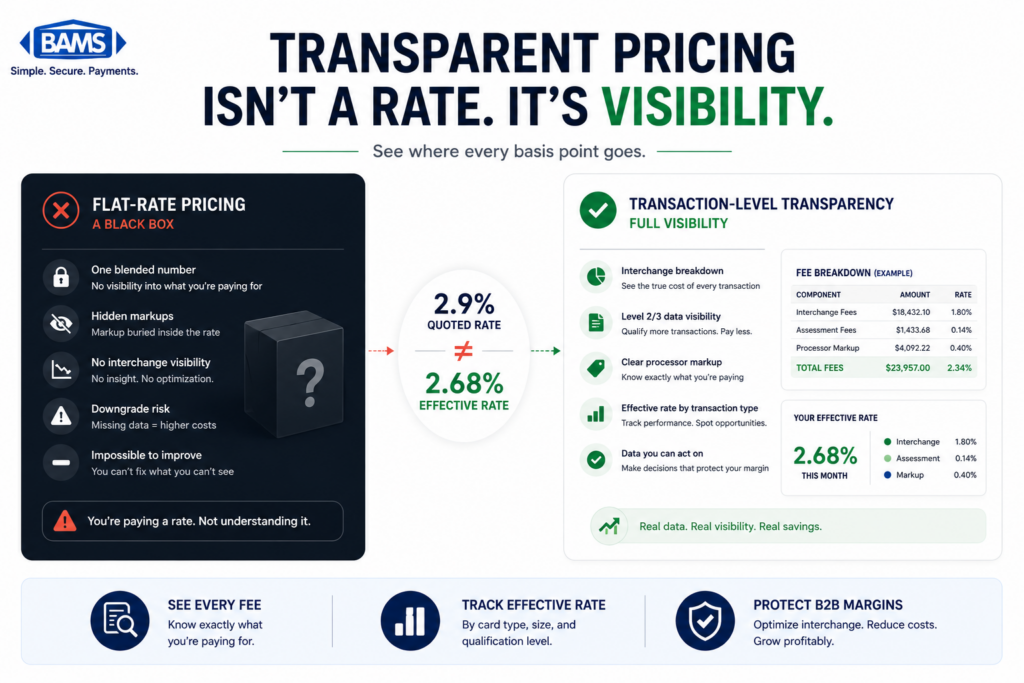

2. “Interchange-Plus” Labels Without Actual Level 2/3 Data Submission

Why it matters:Interchange-plus pricing is marketed as the transparent alternative to tiered pricing. And it can be, when the processor actually submits the enhanced data (tax amounts, line-item details, customer codes) required for Level 2 and Level 3 qualification. Many processors advertise interchange-plus but never submit the data needed to unlock lower rates on B2B and government card transactions.

What it looks like today: Your statement shows interchange-plus formatting, but every corporate or purchasing card transaction settles at the standard commercial rate. There’s no visible distinction between a consumer Visa and a corporate Visa with full Level 3 data attached.

How to apply it: Request a transaction-level report showing the interchange category each transaction qualified at. If your processor can’t produce this, or if all commercial card transactions show the same rate regardless of data richness, you’re paying for a label without the optimization behind it.

3. PCI Non-Compliance and “Compliance Program” Fees

Why it matters: PCI compliance fees are legitimate. But the range of what processors charge varies wildly, from $70 per year to $30+ per month. Some processors charge a monthly “PCI non-compliance fee” that never goes away, even after you complete your SAQ. Others bundle a “compliance program” fee that includes no actual compliance support. Understanding what PCI compliance fees should actually cost is one of the clearest indicators of processor transparency.

What it looks like today: Your statement includes a monthly line item between $9.95 and $34.95 labeled “PCI fee,” “PCI non-compliance,” or “security program fee.” You may also see a separate annual fee on top of the monthly charge.

How to apply it: Confirm your PCI compliance status with your processor. If you’ve completed your Self-Assessment Questionnaire and are still being charged a non-compliance fee, dispute it in writing. If your annual PCI costs exceed $120, ask exactly what services that fee covers.

4. Batch and Statement Fees That Scale Without Justification

Why it matters: Batch fees (charged each time you settle your daily transactions) and monthly statement fees seem small individually. A $0.25 batch fee across 30 daily settlements is $7.50/month, which sounds negligible. But processors often stack these alongside account maintenance fees, gateway fees, and “technology” fees that collectively add $50 to $150/month in costs that have no direct relationship to your transaction volume or the service you receive.

What it looks like today: Your monthly statement has a section of fixed fees that hasn’t changed since you signed up, even as your volume has grown. These fees were set during onboarding and never renegotiated.

How to apply it: List every fixed monthly fee on your statement. For each one, write down what service it corresponds to. If you can’t identify the service, or if two fees seem to cover the same function, flag them for your next conversation with your processor. Negotiating processing fees starts with knowing what you’re being charged for.

5. Network Assessment and Card Brand Fee Markups

Why it matters: Visa, Mastercard, and other networks charge assessment fees (typically 0.13% to 0.15%) that every processor must pass through. The hidden cost isn’t the assessment itself. It’s the markup your processor adds on top, sometimes doubling or tripling the actual network fee. Because these fees are small per transaction, they rarely get scrutinized.

What it looks like today: Your statement shows “Visa assessment” or “MC network access fee” as a separate line, but the rate listed is higher than Visa’s published schedule. Or the fees are bundled into a single “card brand fees” line with no breakdown.

How to apply it: Compare the assessment rates on your statement against the current published schedules from Visa and Mastercard. Any difference is your processor’s markup. Even a 0.05% overage on $500K in annual volume costs you $250/year, and most markups are larger than that.

6. Early Termination Fees and Auto-Renewal Traps

Why it matters:Opaque billing practices and hidden contract clauses create switching costs that keep merchants locked into unfavorable pricing. Early termination fees (ETFs) of $295 to $595 are common, and many contracts auto-renew for 1 to 3 years with a narrow cancellation window. California’s SB 478 “Honest Pricing Law” now requires advertised prices to include all mandatory fees, but contract-embedded penalties remain a separate issue that merchants must audit independently.

What it looks like today: You signed a 3-year contract that auto-renewed. You didn’t notice because the renewal clause was on page 14 of your original agreement. Now switching processors means paying a termination fee that wipes out months of potential savings.

How to apply it: Locate your original processing agreement. Search for “term,” “renewal,” and “termination.” Note the contract end date, the auto-renewal period, and the cancellation notice window. Calendar these dates now so you can renegotiate or switch before the next renewal locks in.

7. Effective Rate Drift From Unmonitored Card Mix Changes

Why it matters: Your effective processing rate (total fees divided by total volume) is the single number that tells you whether your costs are trending up or down. But most eCommerce businesses never track it month over month. As your customer base shifts (more corporate cards, more international cards, more rewards cards), your card mix changes, and your effective rate drifts upward without any visible fee increase on your statement.

What it looks like today: Your processor hasn’t raised their markup, but your monthly costs have increased by 10% to 15% over the past year. No single line item explains the change. The cause is a gradual shift toward higher-interchange card types that your processor hasn’t flagged or optimized for.

How to apply it: Calculate your effective processing rate for each of the past six months. If it’s trending upward, request a card mix report from your processor. This tells you which card types are driving the increase. For B2B merchants, a rising effective rate often signals that commercial card transactions aren’t being submitted with Level 2/3 data, which is exactly where BAMS focuses its cost-reduction analysis through transparent interchange-plus pricing and dedicated account management.

What These Hidden Fees Have in Common

A visual breakdown of how small merchant processing fees compound into major annual margin loss.

Every item on this list shares a root cause: the gap between what your processor says you’re paying and what you’re actually paying. That gap persists because most merchant statements are designed for compliance, not clarity. They satisfy reporting requirements without making it easy to spot overcharges.

The second pattern is compounding. No single hidden fee will bankrupt your business. A $9.95 monthly fee here, a 0.10% markup there. But choosing a processor based on advertised rates alone ignores the cumulative effect of these charges. For a business processing $500K annually, even a 0.3% aggregate overpayment equals $1,500 per year in preventable cost.

The third pattern is that these fees punish inaction. Processors rarely volunteer to lower your rates or flag downgrades. The diagnostic burden falls entirely on you, which means the businesses that audit regularly pay less than those that don’t, regardless of which processor they use.

Where to Start Without Overhauling Everything

You don’t need to tackle all seven items this month. Start with two actions that take less than an hour combined. First, calculate your effective processing rate for the past three months. If it’s above 2.5% and you’re processing B2B or high-ticket orders, you’re likely leaving money on the table through missed Level 2/3 qualification.

Second, pull your most recent statement and circle every line item you can’t immediately explain. That list becomes your agenda for the next call with your processor. If they can’t explain each charge clearly, or if they deflect with jargon, that tells you everything you need to know about whether your current pricing is actually transparent.

Real transaction cost savings come from sustained attention, not one-time negotiations. Build a quarterly review habit, and the hidden fees lose their hiding places.

Frequently Asked Questions

What is interchange-plus pricing and how does it work?

Interchange-plus pricing separates your processing cost into two visible components: the interchange rate set by the card network (Visa, Mastercard) and a fixed markup charged by your processor. This model gives you transparency into the actual cost of each transaction. However, the label alone doesn’t guarantee savings. Your processor must also submit the required transaction data to qualify orders at the lowest available interchange tier, especially for B2B and corporate card payments.

What are the common hidden fees in merchant services that businesses should watch out for?

The most frequent hidden fees include PCI non-compliance charges, interchange downgrade surcharges, inflated network assessment fees, batch and statement fees, and early termination penalties. Individually, each may look small. Collectively, they can cost a small business roughly $2,400 per year. The key diagnostic step is comparing every line item on your statement against the specific service it’s supposed to cover.

Why should businesses consider Level 2/3 optimization for B2B transactions?

Level 2 and Level 3 data optimization reduces interchange rates on commercial, corporate, and government card transactions by submitting enhanced transaction details (tax amounts, line-item data, customer codes) to the card networks. For B2B merchants with average order values above $500, the savings per transaction can range from 0.5% to 1.0%. Without this optimization, those transactions default to higher standard commercial rates, even if you’re on an interchange-plus pricing model.

How can I tell if my processor is actually qualifying transactions at Level 3?

Request a transaction-level interchange qualification report from your processor. This report should show the specific interchange category each transaction settled at. If all commercial card transactions show the same rate, or if your processor can’t produce this report, your transactions are likely settling at standard (higher) rates regardless of what your pricing agreement says.

When is a good time to negotiate processing fees with your merchant services provider?

The strongest negotiating windows are when your contract is approaching its renewal date, when your processing volume has increased significantly since your last agreement, or when you’ve completed a statement audit that reveals specific overcharges. Come prepared with your effective processing rate, a list of unexplained fees, and competing offers. Processors are more responsive when you can point to specific line items rather than asking for a general discount.

Which payment processing model is more cost-effective for high-volume transactions?

For businesses processing $250K or more annually, interchange-plus pricing with active Level 2/3 data submission typically delivers the lowest effective rate. Tiered pricing bundles transactions into qualified, mid-qualified, and non-qualified buckets, which obscures actual interchange costs and often results in higher overall fees. The key is not just the pricing model label, but whether your processor actively works to qualify each transaction at the lowest available rate.

Sources