Cash Flow Acceleration Strategies: The Edge You’re Ignoring

Why deposit timing is a competitive variable—not a back-end function—and how slower funding compounds against you

Learn why 3-5 day deposit windows create a compounding disadvantage in eCommerce. This piece reframes cash flow acceleration strategies as an operational weapon, showing how faster funding lets competitors restock, reprice, and capture demand while you wait.

TL;DR

- Deposit timing is a competitive variable, not a fixed constraint – The 3 to 5 day standard deposit window costs eCommerce businesses real revenue by delaying inventory restocks and blocking supplier discount opportunities.

- Faster funding compounds over time – Getting paid next-day instead of in 3 days means dozens of additional selling days per year for high-velocity products and fewer stockouts.

- Think of deposit speed as inventory velocity – The bottleneck in your cash-to-product-to-cash cycle likely isn’t demand or logistics. It’s the gap between sale and usable funds.

- Model it or miss it – If your cash flow forecast treats deposit timing as fixed, you’re optimizing around a constraint that next-day funding providers have already eliminated.

Your Competitor Restocked Yesterday. You’re Still Waiting on a Deposit.

There’s a quiet race happening in eCommerce that most operators don’t even realize they’re losing. It has nothing to do with ad spend, conversion rate optimization, or product design. It’s about when your money lands. The difference between getting paid today and getting paid Thursday is the difference between restocking a bestseller before it goes out of stock and watching a competitor capture that demand instead. Cash flow acceleration strategies aren’t abstract finance talk. They’re the reason one store grows and another one stalls.

How faster deposits help eCommerce businesses restock faster, avoid stockouts, and improve inventory velocity.

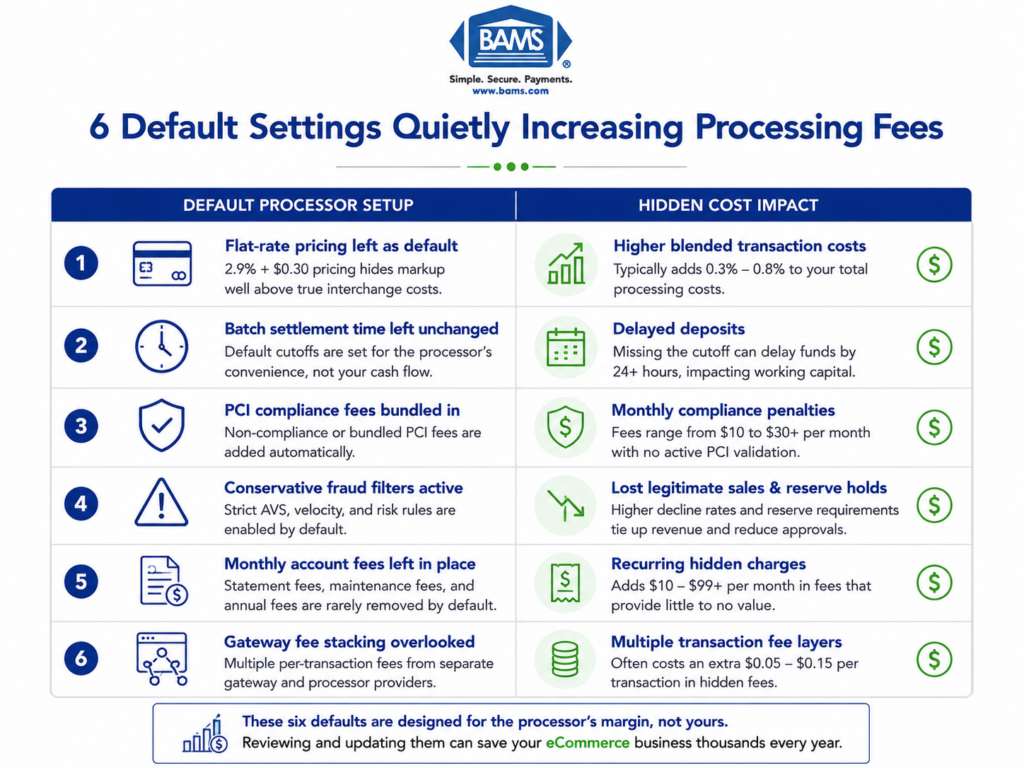

The Myth of the “Standard” Deposit Window

Somewhere along the way, eCommerce managers accepted 3 to 5 business day deposit windows as normal. Understandable. Most payment processors default to it. The language in onboarding docs treats it as standard operating procedure, like sales tax or shipping labels. Just part of doing business.

And for a long time, it was fine. When your competitors operated under the same constraint, the playing field stayed level. Everyone waited. Everyone budgeted around the gap. Everyone treated deposit timing as a fixed, back-end function that didn’t deserve strategic attention.

But that era is over. Faster funding options exist now. And the businesses adopting them aren’t just getting a minor convenience upgrade. They’re gaining a compounding operational advantage that widens every single week.

The Real Variable Nobody’s Modeling

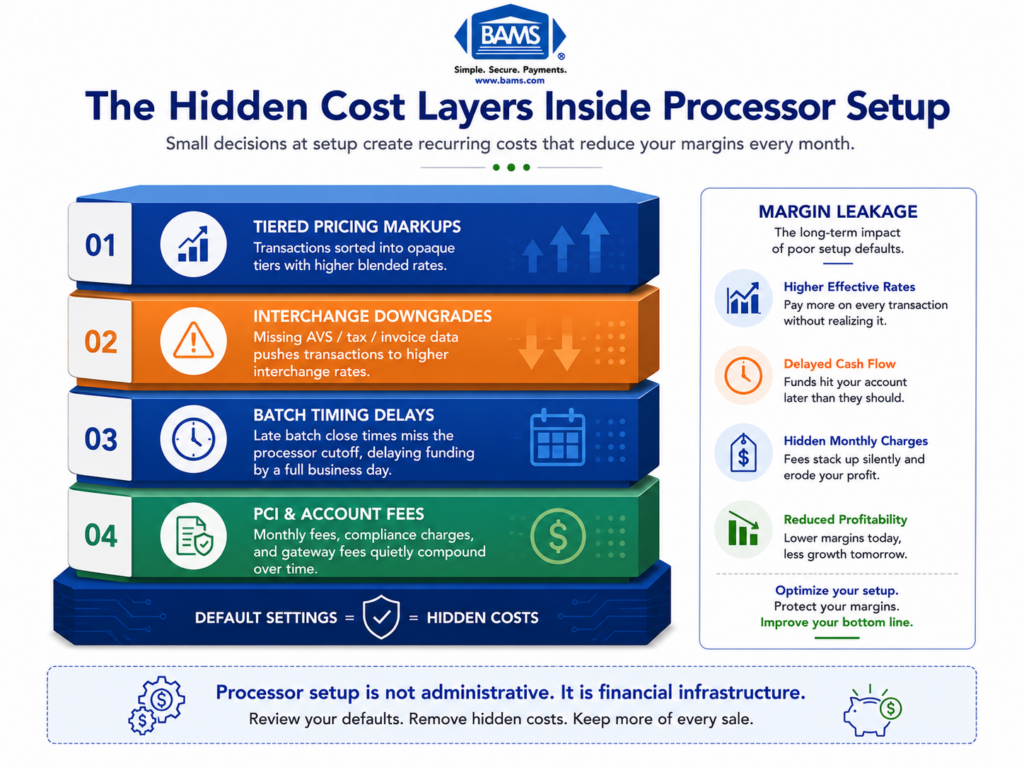

Here’s what we actually believe: deposit timing is not a processing detail. It is a competitive variable with measurable inventory and revenue consequences, and treating it as anything less is leaving money on the table every cycle.

Most eCommerce cash flow forecasting models account for revenue, COGS, ad spend, and payment terms with suppliers. Almost none of them model the gap between when a customer pays and when that money is actually usable. That gap is where growth quietly dies.

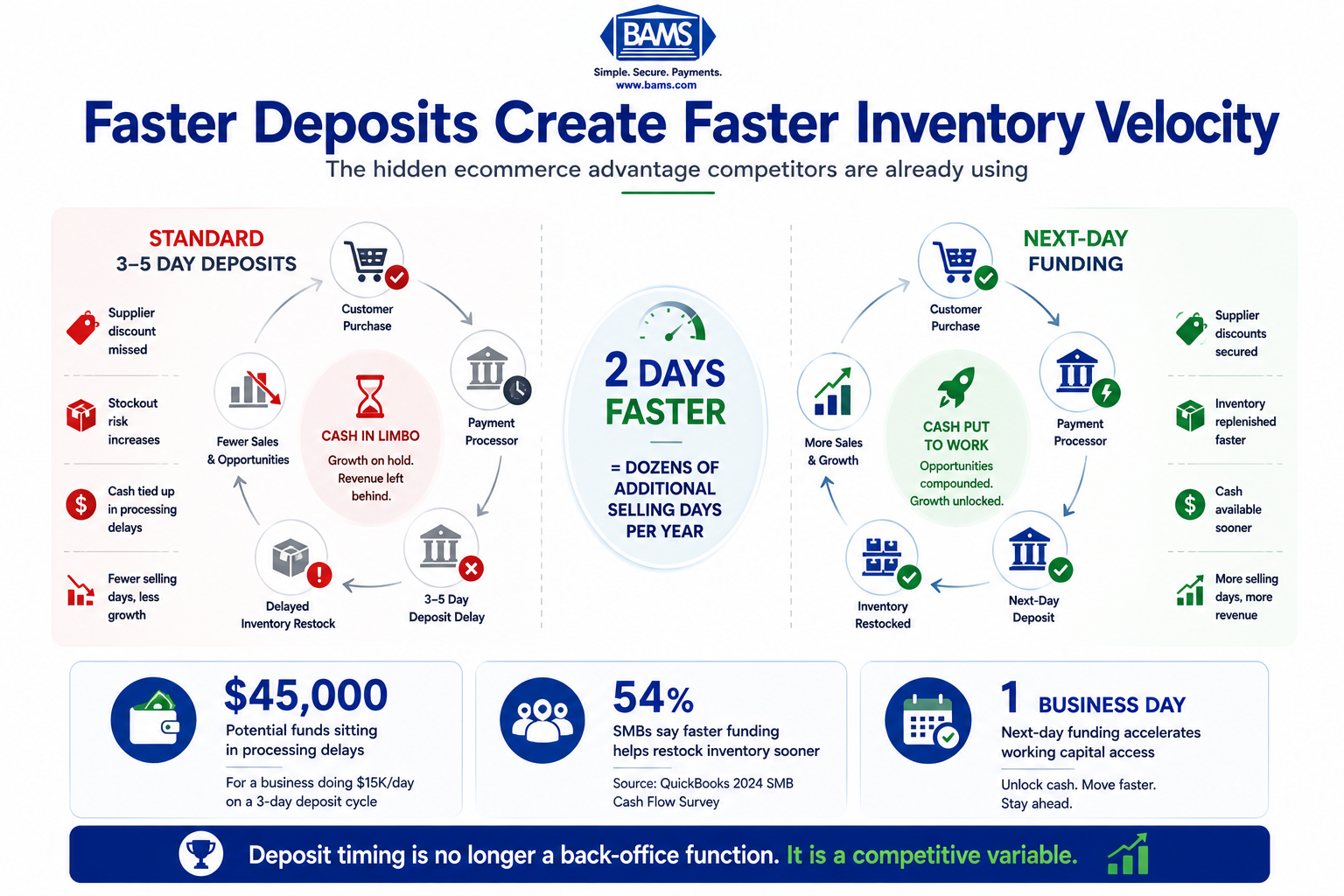

How Three Days Becomes Three Thousand Dollars

Let’s make this concrete. Say you run a mid-size eCommerce store doing $15,000 in daily revenue. On a standard 3-day deposit cycle, you’re always sitting on roughly $45,000 in limbo. Money that’s been earned, money that’s technically yours, but money you can’t deploy.

Now imagine a supplier offers a 48-hour window on a bulk discount for your top-selling SKU. You know the product moves. You know the margin improvement is significant. But your deposit from Monday’s sales won’t clear until Thursday. By then, the discount window has closed. Or worse, a competitor with faster access to their funds already locked in the order.

This isn’t hypothetical. According to Small Business Administration resources, cash flow management remains one of the most common operational challenges for growing businesses. The issue usually isn’t revenue generation itself. It’s gaining access to revenue quickly enough to capitalize on inventory and purchasing opportunities.

Why a 3–5 day funding delay compounds into lost operational speed across eCommerce businesses.

The problem isn’t revenue. It’s access to revenue.

54% of SMB leaders say faster access to funds would help them stock inventory sooner and take advantage of supplier discounts or bulk buys. That statistic alone should reframe how every eCommerce manager evaluates their payment processor.

Consider the compounding effect. If faster deposits let you restock even one high-velocity product two days sooner per cycle, you avoid stockouts, maintain your search ranking on marketplace listings, and capture revenue that would otherwise evaporate. Over 52 weeks, those two days per cycle translate into dozens of additional selling days for your best products.

This is where a processor like BAMS changes the math. Their next-day funding collapses that deposit window, turning Tuesday’s sales into Wednesday’s working capital. For eCommerce operators managing tight inventory cycles, that shift from forecasting around a 3-day gap to forecasting around a 1-day gap is transformational. It’s not about convenience. It’s about velocity.

The pattern we’ve seen is consistent: businesses that streamline payment processing and shorten their cash conversion cycle don’t just improve their balance sheet. They make faster, bolder purchasing decisions because the capital is there when the opportunity appears.

What Changes When You Stop Waiting

If this thesis is right, the implications ripple through your entire operation. Inventory planning gets simpler because you’re working with real cash, not projected deposits. Supplier relationships improve because you can pay faster and negotiate from strength. Ad spend becomes more aggressive because you’re not rationing capital across a multi-day gap.

The cost of ignoring this is subtle but real. Every day your money sits in a processing queue, you’re effectively extending an interest-free loan to your payment processor. Meanwhile, nearly 1 in 3 small businesses cite cash flow as the top reason they use short-term financing. Many are borrowing to cover gaps that faster deposits would eliminate entirely. NACHA ACH Network resources continue to emphasize the importance of faster settlement timing and efficient ACH processing for improving business liquidity and operational flexibility

If your forecasting model doesn’t account for deposit timing as a variable you can change, you’re optimizing around a constraint that no longer needs to exist.

Rethinking Cash Flow as Inventory Velocity

Here’s the reframe: stop thinking about deposit speed as a payments feature. Start thinking about it as inventory velocity.

Every hour your earned revenue sits inaccessible is an hour your inventory isn’t turning. Your cash-to-product-to-cash cycle has a bottleneck, and for most eCommerce businesses, that bottleneck isn’t demand or supply chain logistics. It’s the gap between sale and deposit. Financial stability solutions aren’t just about having enough cash. They’re about having cash at the right moment.

The businesses that figure this out don’t just forecast better. They move faster. They buy at better prices. They never miss a restock window. And over time, that operational tempo becomes a moat their slower-funded competitors can’t cross.

Speed Isn’t a Feature. It’s a Strategy.

The eCommerce operators who win over the next few years won’t necessarily have the best products or the biggest ad budgets. They’ll be the ones who eliminated every unnecessary delay between earning revenue and deploying it. Deposit timing is the most overlooked lever in eCommerce operations. The question isn’t whether you can afford to get paid faster. It’s whether you can afford not to.

Frequently Asked Questions

What is a cash flow acceleration strategy?

A cash flow acceleration strategy is any approach that shortens the time between earning revenue and having usable funds. For eCommerce businesses, the most direct lever is reducing deposit hold times from your payment processor so you can reinvest in inventory and operations faster.

How does deposit timing affect cash flow forecasting?

When deposits arrive in 1 day instead of 3 to 5, your forecast becomes more accurate because you’re working with real cash rather than projected balances. This reduces reliance on short-term financing and lets you make purchasing decisions based on actual liquidity.

Which payment solutions can help reduce processing fees and improve cash flow?

Look for merchant services providers that offer next-day funding, transparent pricing without hidden markups, and proactive support. Combining faster deposits with lower processing costs directly improves your net cash position each cycle.

Sources