Low Cost Merchant Services: Why the Rate Is Lying

The advertised rate hides what B2B transactions actually cost — effective rate is the only number that matters

Learn why ‘low cost’ merchant services often cost more on B2B and high-ticket orders. Discover how effective processing rate exposes hidden costs that advertised rates obscure, and why Level 2/3 optimization is the real benchmark.

TL;DR

- Advertised rates are misleading for B2B – Your effective processing rate on commercial card orders is the only honest cost metric. A “low” base rate means nothing if transactions aren’t qualifying at Level 2 or Level 3 interchange tiers.

- Level 3 optimization saves 30-40% on interchange – Submitting enhanced transaction data (line items, tax, shipping details) can reduce interchange costs by roughly $1,000/month on $100K in commercial card volume.

- Most processors don’t qualify your transactions – Many providers process B2B orders at Level 1 by default and pocket the same markup, leaving you to absorb inflated interchange without knowing it.

- Measure the gap, not the rate – Ask your processor to show qualification levels on your last 50 commercial card transactions. If they can’t, your “low cost” provider is costing you more than you think.

The Cheapest Rate on Your Statement Might Be the Most Expensive Thing About It

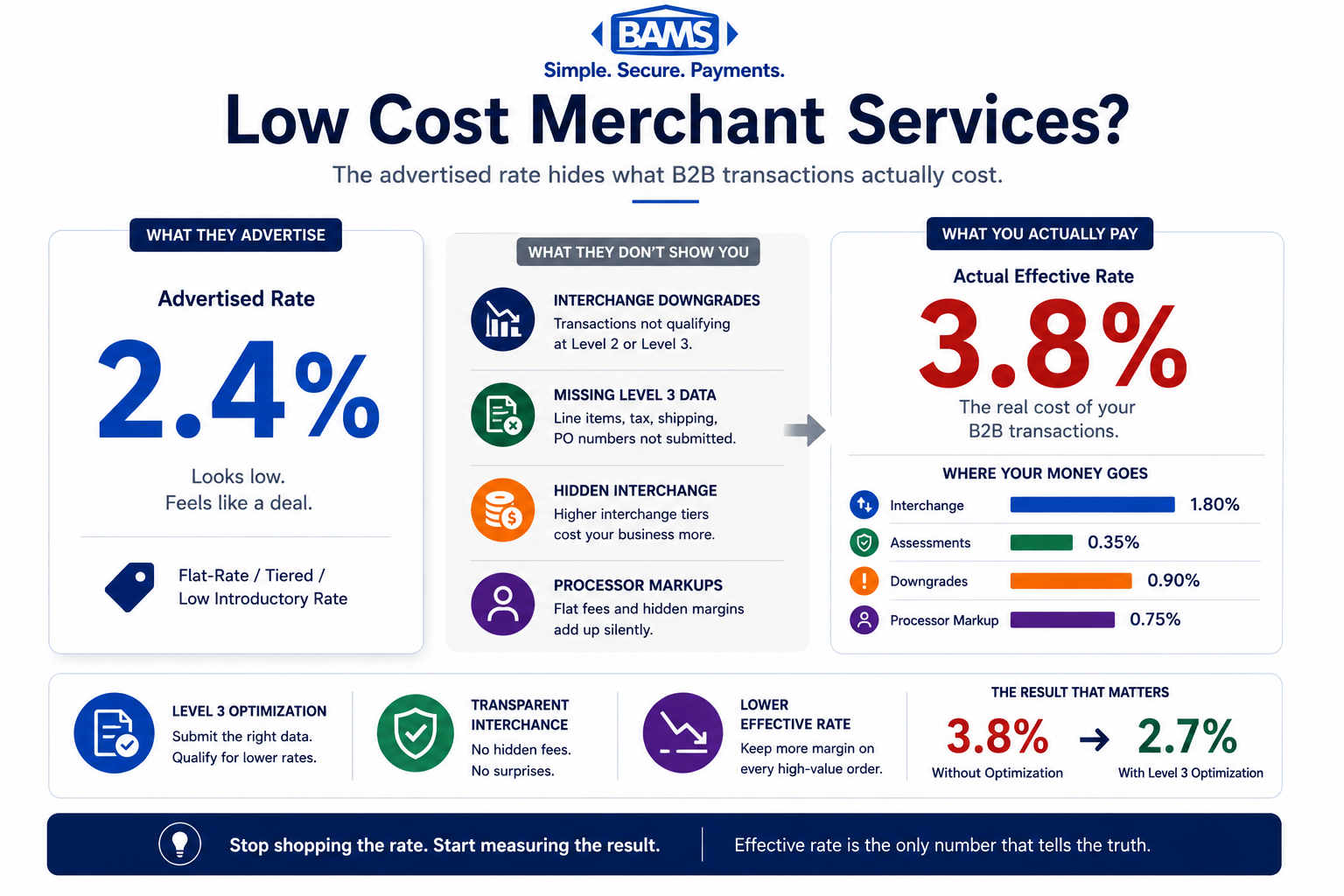

Here’s a scenario that plays out constantly in eCommerce: a merchant switches to a provider advertising low cost merchant services, watches the base rate drop by a few basis points, and celebrates. Then three months later, the effective processing rate on B2B and high-ticket orders hasn’t budged. Sometimes it’s worse. The “savings” were cosmetic. The real costs were hiding in the transactions that mattered most.

A low advertised processing rate can still produce a high effective rate when commercial card transactions fail to qualify at Level 2 or Level 3 interchange tiers.

Why “Low Rate” Became the Only Sales Pitch That Matters

The merchant services industry trained buyers to shop on one number: the advertised rate. It makes sense. When you’re comparing providers, a lower percentage feels like a lower cost. And for years, if your business was mostly consumer transactions at predictable ticket sizes, that shortcut worked well enough.

But the B2B eCommerce landscape has shifted. More businesses accept commercial cards, purchasing cards, and government P-cards. These transactions carry different interchange categories, and they don’t automatically qualify for the lowest rates. A provider quoting you 2.4% on a flat-rate model isn’t lying. They’re just not telling you that your $8,000 commercial card order could have processed at 1.9% if the right data had been submitted.

The advertised rate became a distraction. A comfortable one, because it’s easy to compare. But easy comparisons aren’t the same as accurate ones.

The Only Number That Tells the Truth

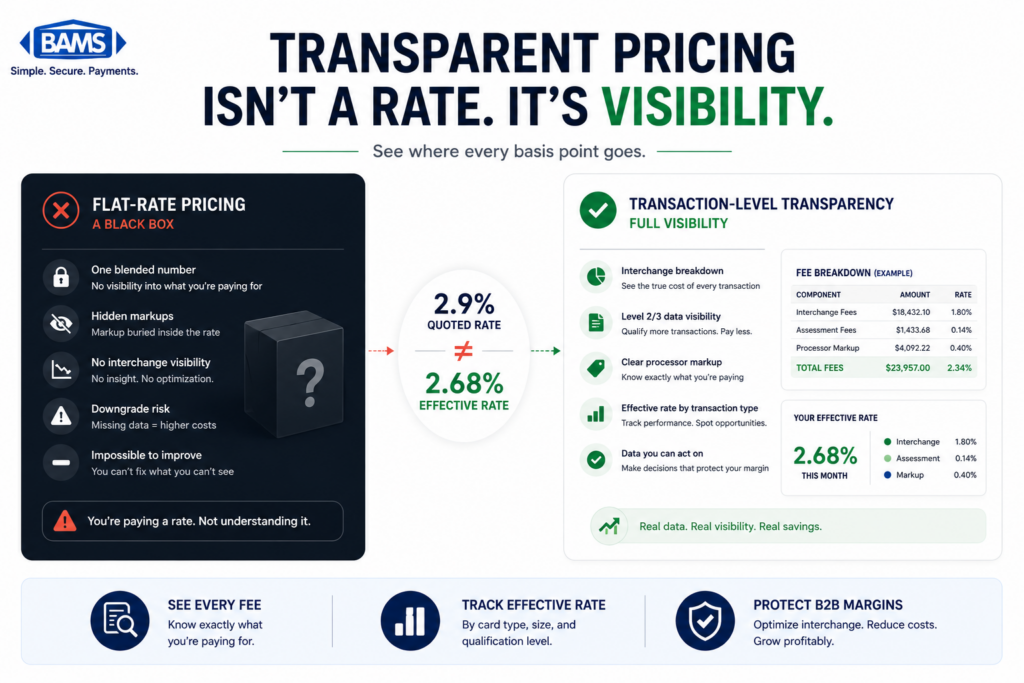

Your effective processing rate on B2B orders is the only honest measure of what you’re paying. Not the base rate. Not the interchange-plus markup in isolation. The total cost divided by total volume, segmented by transaction type. That’s the number. Everything else is marketing.

Where the Real Money Disappears on B2B Transactions

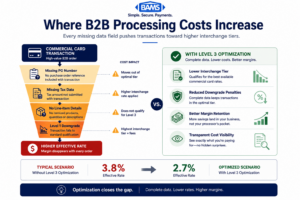

Let’s talk about what actually happens when a commercial card hits your checkout. Card networks like Visa and Mastercard set interchange rates in tiers. The tier your transaction lands in depends on how much data you submit with it. This is the Level 2/Level 3 optimization framework, and it’s where most eCommerce businesses in the 10-50 employee range are quietly losing money.

Incomplete commercial card transaction data causes interchange downgrades that inflate effective processing rates on B2B orders.

The Three Levels, Simply

Level 1 is a standard consumer transaction. You pass basic card and amount data. Level 2 adds customer codes and tax information. Level 3 goes further: line-item details, product descriptions, quantities, ship-to addresses. The more data you provide, the lower the interchange rate the card networks charge, because Level 3 transactions are more secure and less prone to fraud, which is exactly why Visa and Mastercard incentivize them with lower rates. Card networks such as Visa incentivize enhanced transaction data because Level 2 and Level 3 transactions provide greater transparency and lower fraud exposure for commercial card processing.

Here’s the math that should keep you up at night. A B2B operation processing $100,000 per month in commercial card volume at Level 1 pays roughly $2,900 in interchange. That same volume, qualified at Level 3, drops to approximately $1,900. That’s $1,000 per month in savings, a 34% reduction, and it comes from submitting data your systems likely already have.

Multiply that across a year. $12,000. For a business doing $1.2 million in annual B2B card volume, that’s not a rounding error. That’s a hire. That’s an ad budget. That’s margin you’re handing to card networks for no reason.

Most Processors Don’t Qualify Your Transactions (and Don’t Tell You)

This is the part that should make you angry. Many providers advertising low cost merchant services aren’t submitting Level 2 or Level 3 data on your behalf. They process the transaction at Level 1, pocket the same markup either way, and you absorb the inflated interchange. Your statement shows a rate. It doesn’t show what the rate could have been.

B2B merchants commonly see fee reductions of 30-40% through proper Level 2 and Level 3 optimization. But “proper” is doing a lot of work in that sentence. It requires your processor to actually map and transmit the enhanced data fields. Tax amounts, line-item details, merchant category codes. If your provider isn’t doing this, their low rate is subsidized by your high interchange.

And here’s a recent development worth noting: as of January 2026, Visa retired its Level 2 program entirely, folding everything into its Commercial Enhanced Data Program (CEDP). Level 3 data is now the primary path to interchange savings on Visa commercial cards. If your processor hasn’t adapted to this change, you’re not just missing discounts. You’re operating on an outdated framework.

According to Federal Reserve interchange fee data, interchange remains one of the largest cost components in card acceptance, making qualification optimization especially important for high-ticket B2B transactions.

How to Know If You’re Getting Qualified

Pull your last three monthly statements. Look at the interchange detail section. If every commercial card transaction shows the same interchange category, that’s a red flag. Legitimate Level 3 qualification produces different rate tiers depending on the card type and data submitted. Uniformity usually means your processor is batching everything at Level 1.

If your statement doesn’t break out interchange by qualification level at all, that’s an even bigger problem. You can’t optimize what you can’t see. A transparent pricing model should show you exactly where each transaction lands, not bury it in a blended rate.

What Changes If You Start Measuring the Right Number

If your effective processing rate on B2B orders is the benchmark (and it should be), then several things shift immediately. First, you stop comparing providers on advertised rates and start comparing on qualified interchange outcomes. That eliminates 80% of the smoke and mirrors in merchant services sales pitches.

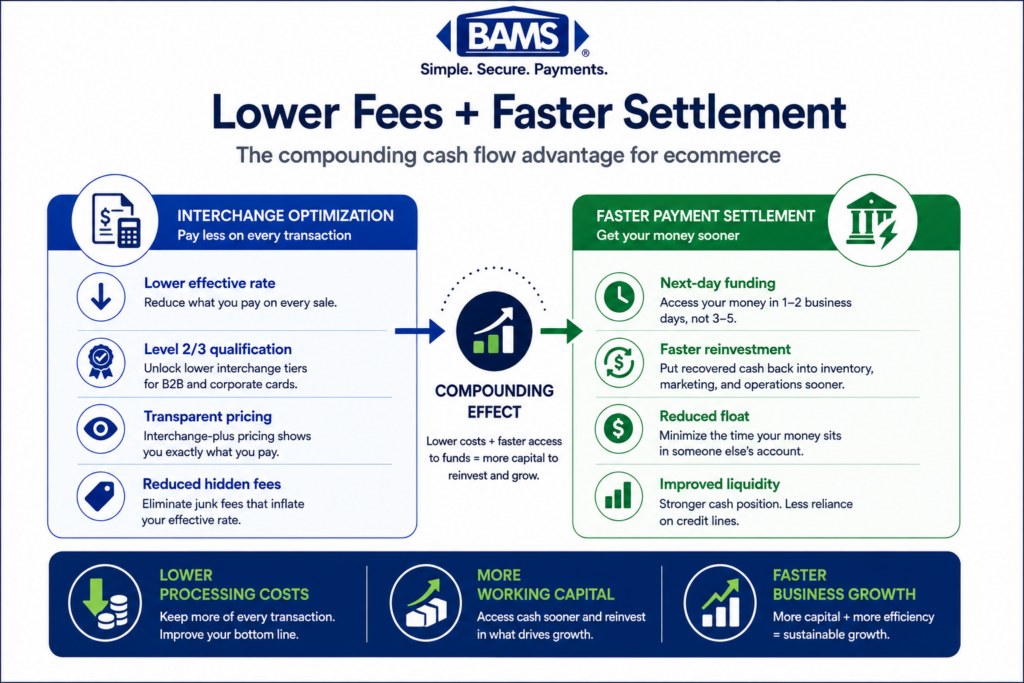

Second, you realize that interchange savings and cash flow timing aren’t separate conversations. Getting $1,000 back per month in lower interchange doesn’t help if your processor holds funds for three days. The combination of Level 2/3 optimization with guaranteed next day funding is where the compounding advantage lives. BAMS pairs both: transparent interchange-plus pricing with Level 2/3 data qualification and next-day funding, so the savings actually hit your account when they matter.

Third, you start asking your current processor uncomfortable questions. “Show me the qualification level on my last 50 commercial card transactions.” If they can’t, or won’t, that tells you everything.

A Better Way to Think About Processing Costs

Stop thinking of your processing rate as a single number. Think of it as a spectrum. Every transaction has a floor (the lowest interchange it could qualify for) and a ceiling (the default rate if no enhanced data is submitted). Your processor’s job is to push every transaction toward the floor. Your job is to verify they’re actually doing it. PCI Security Standards Council guidance also emphasizes the importance of transaction visibility, operational oversight, and secure payment data handling for merchants processing commercial card payments.

The question isn’t “what’s your rate?” The question is “what’s the gap between my floor and my ceiling, and who’s closing it?” That reframe turns merchant services from a commodity comparison into a performance conversation. And performance is measurable.

For a deeper look at how to audit your statement for hidden costs and calculate your true effective rate, the math is straightforward once you know what to look for.

The Expensive Illusion of Cheap

Low cost merchant services that don’t qualify your B2B transactions aren’t low cost. They’re low effort. And you’re the one paying the difference. The businesses that win on processing aren’t chasing the lowest advertised rate. They’re measuring the effective rate on every transaction type, demanding transparency at the interchange level, and choosing partners who do the work to earn the lowest tiers. That’s not a negotiation tactic. That’s a standard.

Frequently Asked Questions

What is interchange-plus pricing and why does it matter for B2B transactions?

Interchange-plus pricing separates the card network’s base cost (interchange) from your processor’s markup, so you can see exactly what you’re paying and where. For B2B transactions, this transparency is critical because it reveals whether your orders are qualifying at Level 2 or Level 3 interchange tiers, where the real savings happen.

How can I tell if my processor is actually qualifying transactions at Level 3?

Check your monthly statement’s interchange detail section. If all commercial card transactions show the same interchange category or your statement doesn’t break out qualification levels at all, your processor likely isn’t submitting the enhanced data needed for Level 3 rates.

What are common hidden fees in merchant services that inflate B2B processing costs?

Beyond obvious markups, the biggest hidden cost is interchange downgrade. When your processor fails to submit Level 2 or Level 3 data, transactions default to higher interchange tiers. This can add 0.5% to 1.0% per transaction, which on high-ticket B2B orders compounds into thousands of dollars annually.