Merchant Services Compared: Security That Pays vs. Costs You

How payment security enhancements affect your cash flow, fraud rates, and deposit speed

Learn which merchant services protect your revenue without delaying deposits. This comparison reveals how fraud protection measures impact cash flow and why security-first providers outperform reactive alternatives.

TL;DR

- Security-enhanced merchant services speed up deposits by using real-time fraud detection instead of manual review queues that hold your funds for days

- Proactive chargeback defense protects your cash flow by resolving disputes before they trigger automatic holds and push you into high-risk categories

- Layered authentication reduces fraud without killing sales as proven by €900 million annual fraud reduction in EU/UK after implementing 3D Secure

- Transparent pricing matters as much as security features because hidden fees erode the benefits of faster deposits and better fraud protection

- Switch providers when deposit delays cost more than switching since migration typically takes 2-4 weeks and the ROI on better fraud protection is immediate for established businesses

The Real Cost of Delayed Deposits in eCommerce

Your eCommerce business processed $50,000 in sales last week. The money sits in limbo for 3-5 business days while your supplier invoices come due tomorrow. This cash flow gap forces you to dip into credit lines, delay inventory orders, or miss early payment discounts.

The problem often traces back to your merchant services provider’s approach to security. Some providers use extensive fraud holds and manual reviews that delay your deposits. Others implement smart payment security enhancements that protect transactions without strangling your cash flow.

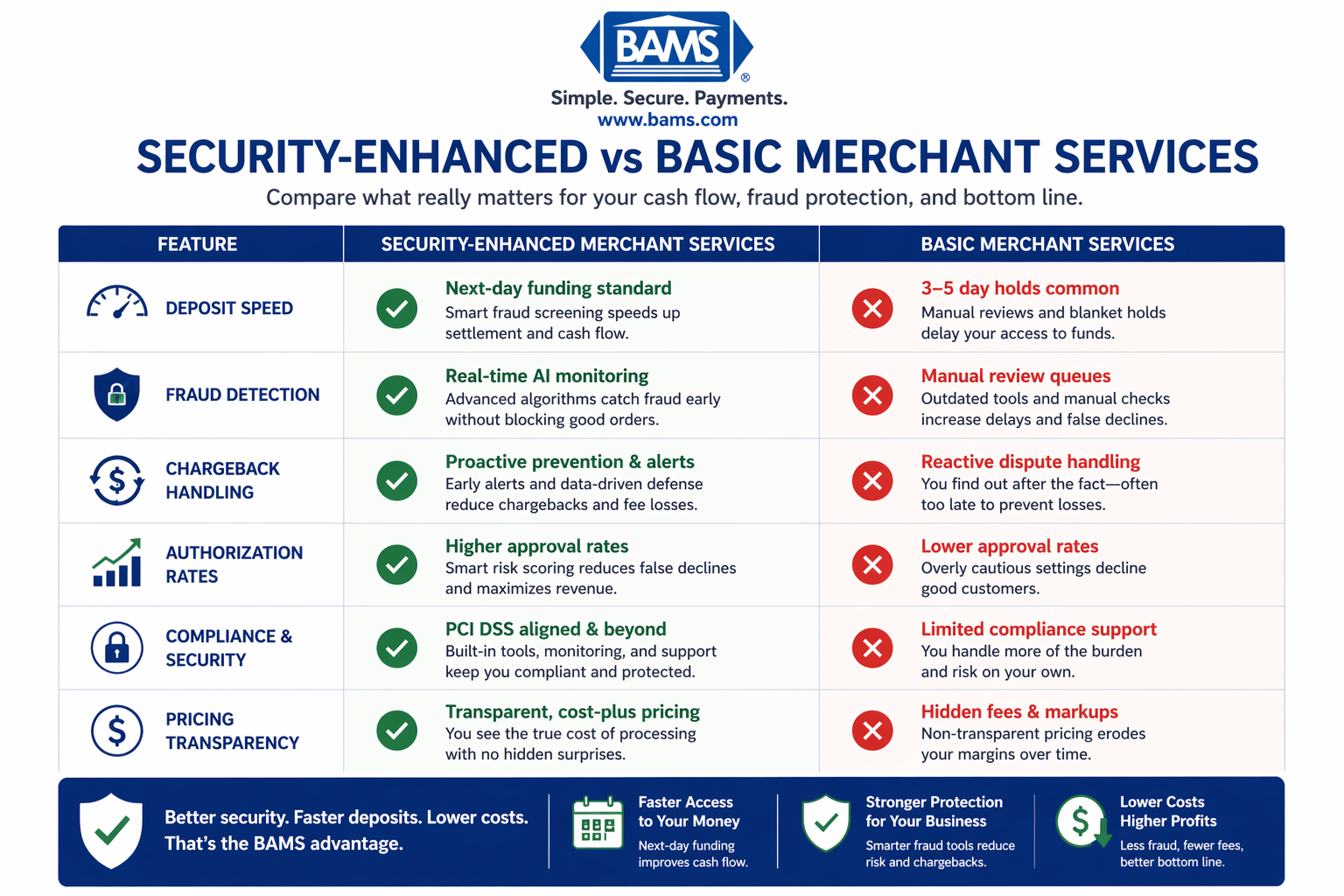

Quick Verdict: Security-First vs. Security-Negligent Merchant Services

A clear comparison of how security-enhanced merchant services outperform basic providers in deposit speed, fraud protection, and cost transparency.

Choose security-enhanced merchant services if you want faster deposits, lower chargeback rates, and predictable cash flow. These providers invest in real-time fraud detection, proactive chargeback defense, and layered authentication that speeds up legitimate transactions.

Reconsider basic merchant services if they rely on blanket holds, manual reviews, and reactive fraud responses. These approaches delay your deposits, increase false declines, and leave you vulnerable to sophisticated fraud that slips through outdated defenses.

|

Criterion |

Security-Enhanced Services |

Security-Negligent Services |

Winner |

|---|---|---|---|

|

Deposit Speed |

Next-day funding standard |

3-5 day holds common |

Security-Enhanced |

|

Fraud Detection |

Real-time AI monitoring |

Manual review queues |

Security-Enhanced |

|

Chargeback Defense |

Proactive alerts and prevention |

Reactive dispute handling |

Security-Enhanced |

|

False Decline Rate |

Lower (smart risk scoring) |

Higher (blanket rules) |

Security-Enhanced |

|

Compliance Support |

PCI DSS guidance included |

Self-service compliance |

Security-Enhanced |

|

Cost Transparency |

Clear, itemized pricing |

Hidden fees, bundled rates |

Security-Enhanced |

Evaluation Criteria: What Actually Matters for eCommerce Deposits

Not all security features affect your deposit timing equally. Here’s what to prioritize when comparing merchant services for your established online business.

Deposit speed directly impacts your working capital. Every day your funds sit in processing is a day you can’t reinvest in inventory or marketing.

Fraud detection accuracy determines whether legitimate orders get approved instantly or flagged for review. Poor detection means either missed fraud or frustrated customers.

Chargeback prevention matters because disputes trigger automatic holds and can push you into high-risk categories with longer settlement times.

Authorization rates affect both revenue and deposit predictability. Declined legitimate transactions mean lost sales and customer churn.

Compliance infrastructure protects you from fines. Strong compliance infrastructure is critical, as the PCI Security Standards Council outlines strict requirements for protecting payment data and preventing breaches.

Head-to-Head: Fraud Protection Measures That Speed Up or Slow Down Deposits

Real-Time Fraud Detection vs. Manual Review Queues

Security-enhanced providers use machine learning models that analyze transaction patterns in milliseconds. They score risk based on device fingerprinting, behavioral analytics, and network intelligence. Legitimate transactions clear instantly while only truly suspicious orders get flagged.

Security-negligent providers rely on static rule sets and manual review teams. Orders over certain amounts, from new customers, or with mismatched billing addresses get queued for human review. This creates 24-48 hour delays even for legitimate purchases. Modern payment systems use advanced authorization and fraud detection frameworks to reduce risk while maintaining speed, as outlined by Visa.

Verdict: Real-time detection wins. It catches more fraud while approving more legitimate orders faster. The result is quicker deposits and happier customers.

Proactive Chargeback Defense vs. Reactive Dispute Handling

Security-enhanced providers offer chargeback defense through pre-dispute alerts, automated refund triggers for obvious fraud, and real-time notification when a customer contacts their bank. You can resolve issues before they become chargebacks.

Security-negligent providers notify you after the chargeback hits your account. By then, funds are already held, and you’re playing defense. Win rates on reactive disputes hover around 20-30%.

Verdict: Proactive defense wins decisively. Preventing chargebacks keeps your merchant account in good standing and avoids the reserve requirements that delay deposits.

Layered Authentication vs. Single-Point Verification

Security-enhanced providers implement what Mastercard calls the three pillars: Verified Token, Enhanced Data Sharing, and Seamless Authentication. These layers work together to verify identity without adding friction.

Security-negligent providers rely primarily on CVV matching and basic AVS checks. These single-point verifications miss sophisticated fraud while flagging legitimate international customers or those with P.O. boxes.

Verdict: Layered authentication provides better protection with less friction. Layered authentication and tokenization significantly reduce fraud while maintaining transaction speed, as demonstrated by modern payment security frameworks from Visa.

Transparent Pricing vs. Hidden Fee Structures

Security-enhanced providers offer clear, itemized statements showing exactly what you pay for processing, security features, and compliance support. You can calculate your true cost per transaction and forecast expenses accurately.

Security-negligent providers bundle fees, add surcharges for “premium” security features, and bury costs in complex tiered pricing. You discover the true cost only after reconciling monthly statements.

Verdict: Transparency wins. Unclear pricing is a major sign you need a new processor. Hidden fees erode margins and make cash flow planning impossible.

Dedicated Support vs. Ticket Queue Support

Security-enhanced providers assign dedicated account managers who know your business, can expedite holds, and proactively alert you to issues. When a legitimate high-value order gets flagged, one call resolves it.

Security-negligent providers route you through generic support queues. Complex issues get escalated multiple times. A flagged order might sit in review for days while you lose the sale.

Verdict: Dedicated support wins for established businesses. The time saved on issue resolution and the revenue protected from faster hold releases justify any premium.

Use Case Mapping: Which Approach Fits Your Business

A simplified decision guide to determine when to upgrade to security-enhanced merchant services for better cash flow and protection.

If you process over $100,000 monthly, choose security-enhanced services. The cost of delayed deposits at this volume exceeds any premium for better fraud protection. Next-day funding on $100K means $100K working for you instead of sitting in limbo.

If you sell high-ticket items ($500+), choose security-enhanced services. High-value transactions trigger more manual reviews with basic providers. Smart risk scoring clears legitimate big purchases faster.

If you have international customers, choose security-enhanced services. Basic AVS checks fail on international addresses, causing false declines. Layered authentication verifies identity without relying on U.S.-centric address matching.

If you’re in a high-chargeback category (digital goods, subscriptions, travel), choose security-enhanced services. Proactive chargeback defense keeps you out of monitoring programs that mandate reserve holds.

If you’re processing under $10,000 monthly, basic services might suffice temporarily. But as you scale, the deposit delays and fraud exposure will cost more than upgrading.

What Both Approaches Get Wrong

Even security-enhanced merchant services can’t solve every deposit delay. Card network settlement windows create baseline timing that no processor can bypass. Weekends and holidays still pause the banking system.

Migration and Switching: What It Actually Takes

Switching merchant services providers typically takes 2-4 weeks for full integration. Your payment gateway may need reconfiguration, and you’ll want to run parallel processing briefly to ensure continuity.

Data portability varies by provider. Tokenized card data sometimes transfers, sometimes doesn’t. Recurring billing customers may need to re-enter payment information, creating churn risk.

Switching costs include potential early termination fees (check your contract), integration development time, and the learning curve for new reporting tools.

When switching makes sense: If your current provider’s deposit delays cost you more monthly than switching costs, move now. If you’re losing sales to false declines or bleeding money to chargebacks, the ROI on better fraud protection measures is immediate.

Final Recommendation: Invest in Security That Accelerates Your Business

For established eCommerce businesses processing meaningful volume, security-enhanced merchant services aren’t a luxury. They’re a competitive requirement. The math is straightforward: faster deposits improve cash flow, better fraud detection increases authorization rates, and proactive chargeback defense protects your merchant account standing.

The providers that treat fraud protection as a core service rather than an upsell consistently deliver faster funding and lower total cost of processing. Look for guaranteed next-day funding, dedicated account management, and transparent pricing as baseline requirements.

Your payment processor should make money flow faster, not slower. If yours doesn’t, that’s the clearest sign it’s time to switch.

Frequently Asked Questions

What are faster deposit strategies in merchant services?

Faster deposit strategies include next-day funding programs, real-time fraud detection that clears transactions without manual holds, and maintaining low chargeback ratios to avoid reserve requirements. Providers with smart risk scoring approve legitimate transactions instantly, while those using manual review queues create 24-48 hour delays.

Why is payment optimization important for businesses?

Payment optimization directly impacts your working capital and customer experience. Faster deposits mean you can reinvest in inventory sooner. Higher authorization rates mean fewer lost sales. Lower processing costs improve margins. For a business processing $500,000 annually, even small improvements in each area can add tens of thousands to your bottom line.

How can I improve my payment authorization rates?

Improve authorization rates by using a processor with intelligent retry logic, implementing 3D Secure for liability shift without friction, ensuring your billing descriptors are clear to reduce confusion-based declines, and offering multiple payment methods including digital wallets. Processors with network tokens also see higher approval rates on recurring transactions.

What role does fraud protection play in payment optimization?

Fraud protection directly affects deposit timing, authorization rates, and processing costs. Poor fraud detection leads to either excessive chargebacks (triggering reserve holds and higher fees) or excessive false declines (losing legitimate sales). Smart fraud protection catches actual fraud while approving good transactions faster.

Which payment processing fees can I reduce to optimize costs?

Focus on interchange optimization through Level 2/3 data submission for B2B transactions, negotiate assessment fees with sufficient volume, eliminate unnecessary gateway fees by consolidating services, and avoid processors that charge for PCI compliance as a separate line item. Cost-plus pricing typically offers better transparency than tiered or bundled rates.

When should I consider expanding my payment options?

Expand payment options when you see cart abandonment at checkout, receive customer requests for specific methods, or want to enter new markets. Digital wallets reduce friction and fraud simultaneously. Buy-now-pay-later options can increase average order value. International payment methods open new customer segments.