5 Signs Your Cash Flow Forecast Is Lying to You

Why deposit lag — not overspending — is the hidden source of your eCommerce cash flow challenges

Learn to diagnose five misleading signals in your cash flow forecast that trace back to deposit timing, not spending habits. Built for eCommerce managers who already forecast but keep getting blindsided by gaps between projected and actual cash positions.

TL;DR

- Your forecast conflates “earned” with “available” – Recording revenue on the transaction date instead of the deposit date creates a systematic overestimate of daily cash on hand, which is the root cause of most cash flow challenges in eCommerce.

- Five symptoms point to one cause – Bloated emergency buffers, missed inventory windows, unnecessary credit draws, Monday cash surprises, and scaling inaccuracy all trace back to deposit timing lag, not spending behavior.

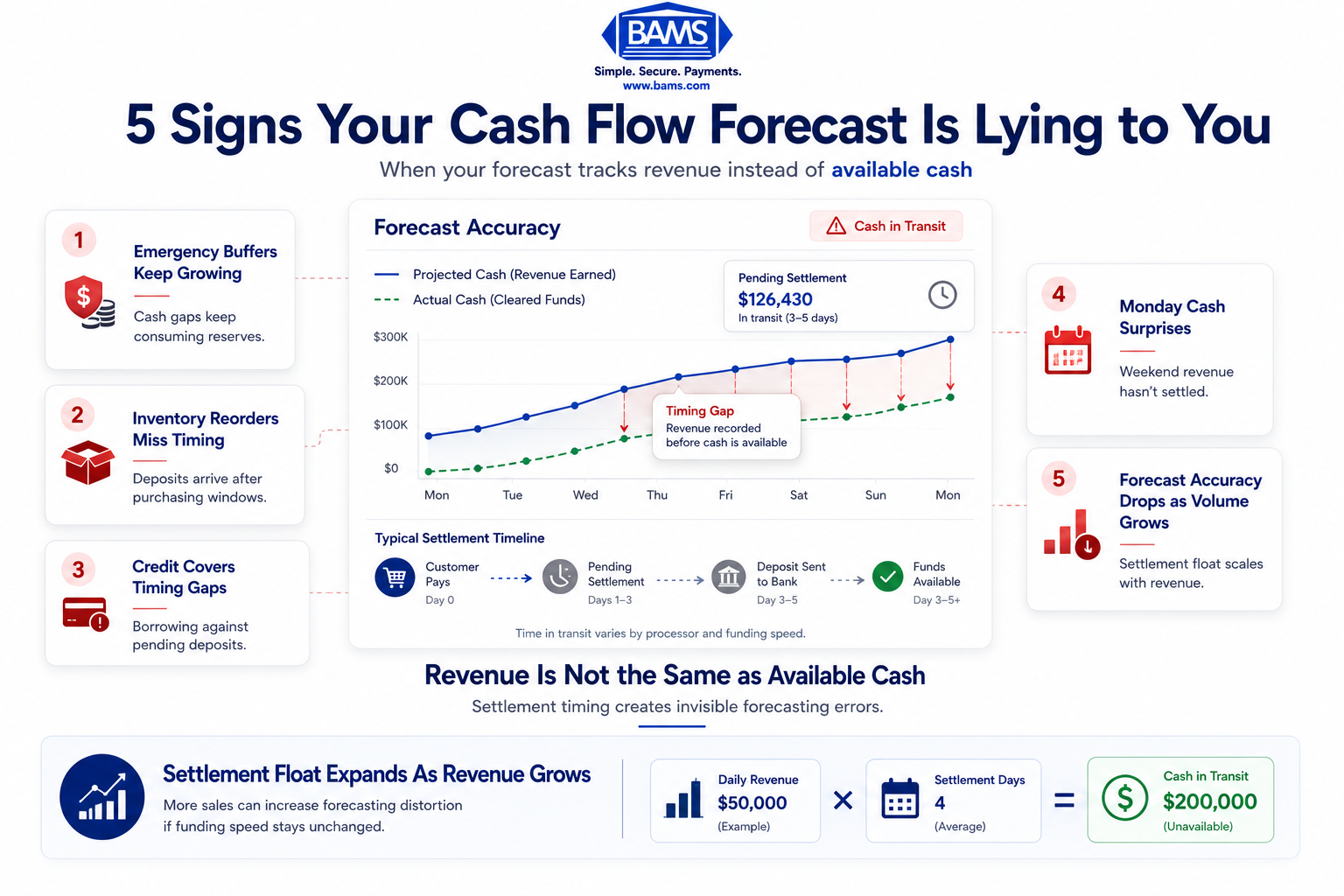

- Settlement float scales with revenue – As your sales volume grows, the absolute dollar amount stuck in transit grows proportionally, making forecasts less accurate at the exact moment you need them most.

- Two quick fixes improve accuracy immediately – Add a “cleared funds” date column to your forecast and calculate your settlement float (daily revenue × settlement days) to see how much cash is perpetually unavailable.

- Deposit speed is negotiable, not fixed – Moving from 3-5 day settlement to next-day funding compresses the timing gap, reduces the need for a short-term cash buffer, and aligns your forecast with your actual bank balance.

Your Forecast Looks Fine. Your Bank Account Disagrees.

You built the spreadsheet and you mapped revenue against expenses. You even padded the numbers a little for safety. And yet, every other week, you’re scrambling to cover a supplier payment or delaying an ad spend increase because the money isn’t there yet. The forecast said it would be.

This is one of the most common cash flow challenges in eCommerce, and it rarely traces back to overspending. It traces back to timing. Specifically, the gap between when a customer pays you and when that money actually lands in your operating account. Small Business Administration resources consistently highlight cash flow management as one of the biggest operational pressures facing growing businesses.

For eCommerce managers processing hundreds or thousands of daily transactions, deposit lag is the silent variable that corrupts every downstream projection.

What This List Covers (and What It Doesn’t)

This is for eCommerce managers at established online businesses (10-50 employees) who already have a forecasting process but keep getting blindsided by gaps between projected and actual cash positions. If you’re looking for general advice on tightening receivables or invoicing faster, that content exists everywhere. This isn’t that.

Instead, these are five diagnostic signals that your cash flow forecast is producing misleading output. Each one points upstream to the same root cause: deposit timing. We’ll walk through what each signal looks like, why it fools you, and how to correct for it without rebuilding your entire financial model.

How We Selected These Signals

Each signal was chosen based on three criteria: it appears frequently in eCommerce operations, it’s commonly misattributed to spending behavior rather than deposit timing, and it can be corrected through process or infrastructure changes (not just budgetary discipline). The goal is diagnosis before prescription.

Five Signals Your Cash Flow Forecast Is Lying to You

Five operational warning signs that reveal your ecommerce forecast is overstating available cash.

1. You Keep Building Emergency Buffers That Never Feel Big Enough

Why it matters: A short-term cash buffer is supposed to be a safety net, not a permanent operating requirement. If you find yourself repeatedly increasing your reserve target because the current one keeps getting tapped, the buffer isn’t the problem. Your forecast is systematically overestimating how much cash is available on any given day.

What it looks like today: Federal Reserve Small Business Employer Firms Report findings continue to show that liquidity and uneven cash positioning remain persistent operational concerns for growing businesses. For eCommerce operators on 3-5 day deposit cycles, those reserves get consumed by the gap between when sales register in your dashboard and when funds clear.

How to correct it: Separate “booked revenue” from “cleared funds” in your forecast. Add a column for expected deposit date, not transaction date. If your processor offers next-day funding, this gap shrinks from days to hours, which means your buffer can actually function as a buffer instead of a revolving loan to yourself.

2. Inventory Reorders Consistently Miss the Window

Why it matters: In eCommerce, reorder timing is everything. Order too early, you tie up cash. Order too late, you lose sales. When your forecast says you have the cash to reorder on Tuesday but the funds don’t clear until Friday, you’ve missed a three-day window that can cascade into stockouts, backorders, and lost customers.

What it looks like today: eCommerce managers often attribute missed reorder windows to demand volatility or supplier lead times. But when you trace it back, the constraint is usually liquidity on the day the purchase order needs to go out. NACHA ACH Network resources continue to emphasize how settlement timing directly affects operational liquidity and purchasing flexibility.

How to correct it: Map your reorder triggers against your actual deposit schedule, not your sales calendar. If you process $15,000 on Monday and your supplier payment is due Wednesday, a 3-day settlement cycle makes that $15,000 invisible to your purchasing team. Compressing deposit timing to next-day changes the math entirely.

3. You’re Using Credit to Bridge Gaps Your Revenue Should Cover

Why it matters: 60% of SMBs report using personal or business credit to bridge cash gaps. In many cases, the business is profitable on paper. Revenue exceeds expenses. But the timing mismatch between inflows and outflows forces the business to borrow against itself. That’s not a spending problem. It’s a settlement problem.

What it looks like today: You see a healthy sales week in your eCommerce dashboard. Meanwhile, you’re drawing on a line of credit to cover payroll or a marketing invoice because those deposits haven’t landed yet. Your forecast told you the cash was there. Technically, it was. Just not in your account.

How to correct it: Track your “credit bridge frequency” (how often you draw on credit to cover timing gaps, not genuine shortfalls). If it happens more than once a month, your forecast is treating pending deposits as liquid cash. Fix the input, or fix the deposit speed. A merchant services partner like BAMS, which offers next-day funding, can eliminate multi-day settlement delays that force unnecessary borrowing.

4. Weekend and Holiday Sales Create Monday Morning Surprises

Why it matters: eCommerce doesn’t stop on weekends. But banking does. If your business processes significant volume on Friday evening through Sunday, those funds may not begin settlement until Monday, with arrival on Tuesday or Wednesday. Your forecast likely treats weekend revenue as a single block. Your bank treats it as a queue.

What it looks like today: Monday arrives and your forecast shows a strong cash position based on weekend sales. But your actual bank balance reflects Thursday’s deposits. You planned a Monday supplier payment based on projected availability. Now you’re short, and the next deposit is 48 hours away. 1 in 3 businesses report that payment delays and settlement timing reduce their forecasting accuracy.

How to correct it: Build weekend and holiday lag explicitly into your forecast model. Don’t average daily revenue across seven days. Instead, model a “cash dark” period from Friday evening through Monday morning (or later, depending on your processor’s batch cutoff times and payout schedule). Then schedule outflows accordingly.

5. Your Forecast Accuracy Drops as Transaction Volume Grows

Why it matters: This is the most counterintuitive signal. More sales should mean more predictable revenue. But if your deposit cycle is 3-5 days and your volume is increasing, the absolute dollar amount sitting in settlement limbo grows proportionally. A 20% revenue increase doesn’t just mean 20% more cash. It means 20% more cash that’s delayed.

What it looks like today: Around 45% of SMBs don’t track cash flow regularly, and among those who do, few adjust their models for volume-dependent settlement exposure. You might forecast $200,000 in monthly revenue with a 3-day average settlement. That means roughly $20,000 is perpetually in transit. Scale to $300,000 and that float jumps to $30,000, a $10,000 increase in cash you can see but can’t use.

How to correct it: Add a “settlement float” line to your forecast that scales with volume. Calculate it as: (average daily revenue) × (settlement days). Then treat that number as unavailable. If reducing settlement days is an option (through next-day or same-day funding), your float shrinks and your forecast gets closer to reality.

The Pattern Behind All Five Signals

How pending deposits quietly create gaps between projected cash and actual bank balances.

Every signal on this list shares the same upstream cause: the forecast treats revenue recognition and cash availability as the same event. They aren’t. In eCommerce, where transactions happen continuously but settlements happen in batches on banking schedules, the gap between “earned” and “available” is the single largest source of forecasting error.

The downstream symptoms (bloated buffers, missed reorders, unnecessary credit usage, Monday surprises, scaling inaccuracy) all look like different problems. They invite different fixes. But they’re all expressions of one structural mismatch. Correcting for deposit timing at the model level addresses all five simultaneously. Compressing deposit timing at the infrastructure level (through your choice of payment processor and funding terms) reduces the magnitude of the problem itself.

Where to Start: Constraints and Priorities

You don’t need to overhaul your entire forecasting process. Start with two changes. First, add a “cleared funds” date to every revenue line in your forecast, distinct from the transaction date. This single adjustment will immediately surface timing gaps you’ve been averaging away. Second, calculate your current settlement float and compare it to your cash buffer. If the float exceeds the buffer, that’s your most urgent vulnerability.

From there, evaluate whether your current deposit cycle is a fixed constraint or a negotiable one. Many eCommerce operators accept 3-5 day settlement as standard without realizing that faster funding options exist and can fundamentally change the accuracy of short-term forecasts. The goal isn’t perfection. It’s closing the gap between what your forecast promises and what your bank account delivers.

Frequently Asked Questions

What is a cash flow acceleration strategy?

A cash flow acceleration strategy is any operational or financial change that reduces the time between earning revenue and having access to those funds. For eCommerce businesses, the most direct lever is deposit speed. Moving from a 3-5 day settlement cycle to next-day funding compresses the gap and makes more cash available for daily operations, purchasing, and growth spending.

How does deposit timing affect cash flow forecasting?

Most forecasts record revenue on the transaction date, not the date funds actually clear your bank account. This creates a systematic overestimate of available cash on any given day. The longer your deposit cycle, the larger this discrepancy becomes, especially during high-volume periods like weekends, holidays, or promotional events.

Why is optimizing merchant services important for cash flow?

Your merchant services provider controls two variables that directly impact cash flow: processing fees (which reduce the amount you receive) and funding speed (which determines when you receive it). Choosing a provider with transparent pricing and next-day funding can reduce both cost and timing uncertainty, giving your forecast more accurate inputs.

How can businesses improve cash flow forecasting with real-time data?

Start by separating booked revenue from cleared funds in your model. Use your processor’s reporting tools to track actual deposit dates, then compare them against your forecast assumptions. Automated cash flow tools from accounting platforms can help by syncing bank feeds with transaction data, but the key input is settlement timing, which depends on your payment processor.

What is a short-term cash buffer and how large should it be?

A short-term cash buffer is a reserve of liquid funds set aside to cover timing gaps between inflows and outflows. For eCommerce businesses, a useful benchmark is to hold at least the value of your settlement float (average daily revenue multiplied by settlement days) plus one week of fixed operating expenses. If you’re constantly tapping this buffer, the issue is likely deposit lag, not insufficient reserves.

Can faster payment processing actually reduce the need for business credit?

Yes. When businesses use credit lines to bridge the gap between earning revenue and receiving deposits, the cost is real (interest, fees, credit utilization). Compressing settlement from 3-5 days to next-day funding eliminates most of these timing-driven borrowing events. The revenue was always sufficient. It just wasn’t accessible fast enough.